Key Insights

The global Armored Vehicle Upgrade and Retrofit market is projected for substantial growth, driven by rising geopolitical instability, the critical need for enhanced force protection, and the ever-evolving landscape of battlefield threats. With an estimated market size of $51.6 billion in the base year 2025, the industry is expected to expand at a Compound Annual Growth Rate (CAGR) of 3.3% through 2033. This growth is predominantly fueled by defense ministries worldwide prioritizing the modernization of existing armored fleets over the acquisition of entirely new platforms. Key demand drivers include the necessity for improved survivability against asymmetric warfare, the integration of advanced C4ISR systems, and the adaptation of legacy vehicles for enhanced mobility and firepower. The increased deployment of Mine-Resistant Ambush-Protected (MRAP) vehicles and ongoing upgrades to Infantry Fighting Vehicles (IFVs) and Main Battle Tanks (MBTs) highlight the market's focus on immediate operational effectiveness and strategic adaptability.

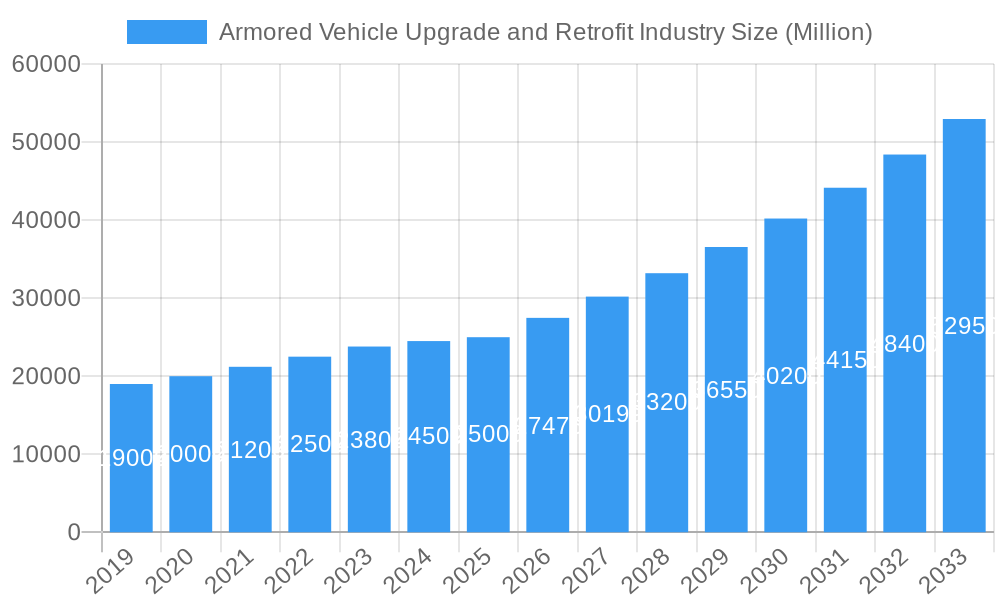

Armored Vehicle Upgrade and Retrofit Industry Market Size (In Billion)

The market is segmented by vehicle type, with Armored Personnel Carriers (APCs), Infantry Fighting Vehicles (IFVs), Mine-Resistant Ambush-Protected (MRAP) vehicles, and Main Battle Tanks (MBTs) constituting the leading segments. While initial investment in new armored vehicles is significant, the cost-effectiveness of upgrades and retrofits presents a strategically viable option for nations aiming to maintain a modernized and capable defense posture. Emerging trends encompass the integration of Active Protection Systems (APS), advanced armor technologies such as composite and reactive armor, and the incorporation of digital battle management systems. However, potential restraints include budget limitations in some defense sectors, complex logistical challenges associated with large-scale fleet modernizations, and the dynamic nature of warfare requiring continuous strategic recalibration of upgrade strategies. Leading companies such as Textron Inc., THALES, Oshkosh Corporation, General Dynamics Corporation, and BAE Systems PLC are instrumental in this dynamic market, offering comprehensive solutions to meet the evolving requirements of global armed forces.

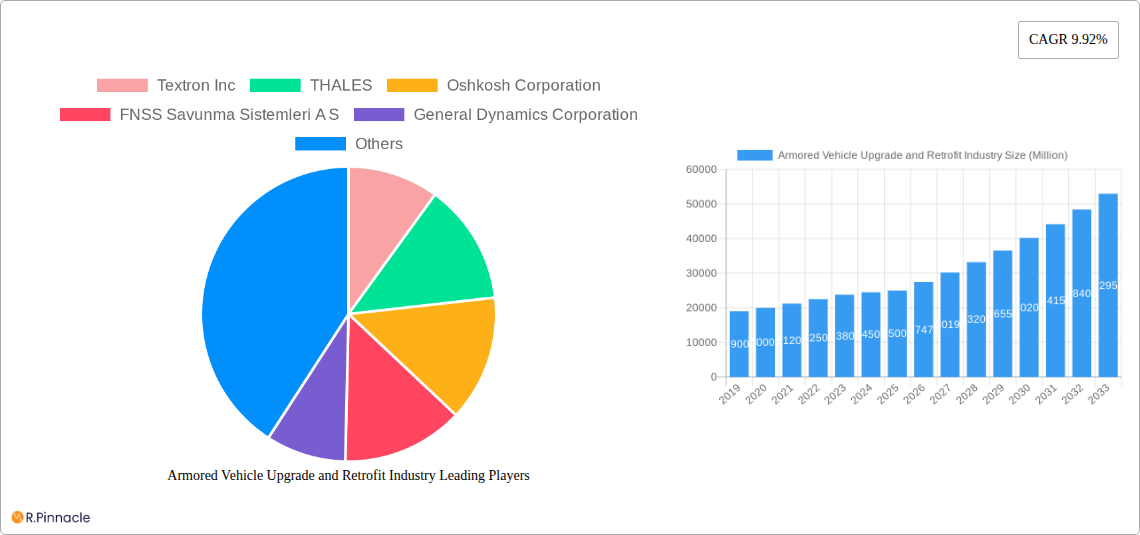

Armored Vehicle Upgrade and Retrofit Industry Company Market Share

Armored Vehicle Upgrade and Retrofit Industry: Comprehensive Market Analysis and Future Projections (2019-2033)

Unlock critical insights into the global Armored Vehicle Upgrade and Retrofit market with this in-depth report. Spanning from 2019 to 2033, this analysis provides a strategic roadmap for stakeholders navigating the evolving defense landscape. The report leverages high-ranking keywords like "armored vehicle modernization," "military vehicle retrofitting," "APC upgrades," "IFV refurbishment," "MRAP lifecycle extension," and "MBT enhancement" to ensure maximum visibility and engagement for industry professionals.

This comprehensive study, with a base year of 2025 and an estimated year also of 2025, details market structures, dynamics, key drivers, challenges, and future outlook. It encompasses vital segments such as Armored Personnel Carriers (APC), Infantry Fighting Vehicles (IFV), Mine-resistant Ambush Protected (MRAP), Main Battle Tanks (MBT), and Other Vehicle Types. Gain actionable intelligence from leading companies including Textron Inc, THALES, Oshkosh Corporation, FNSS Savunma Sistemleri A S, General Dynamics Corporation, Rheinmetall AG, Elbit Systems Ltd, Patria Group, Nexter Group, BAE Systems PLC, Bharat Electronics Limited (BEL), and Ruag International Holding AG.

Armored Vehicle Upgrade and Retrofit Industry Market Structure & Innovation Trends

The Armored Vehicle Upgrade and Retrofit industry exhibits a moderately concentrated market structure, with a few key players like General Dynamics Corporation, BAE Systems PLC, and Rheinmetall AG holding significant market shares, estimated to be between 15-20% each for the top three. Innovation is primarily driven by the urgent need for enhanced survivability, operational efficiency, and the integration of advanced C4ISR systems. Regulatory frameworks, particularly stringent military specifications and procurement processes by national defense ministries, significantly influence market entry and product development. Product substitutes are limited, given the specialized nature of armored vehicles, but advancements in active protection systems and drone integration are creating new competitive dynamics. End-user demographics are predominantly national defense forces and security agencies, with a growing interest in cost-effective upgrade solutions over complete platform replacement. Mergers and acquisitions (M&A) are strategic tools for consolidating capabilities and expanding market reach; recent M&A deal values have reached upwards of $500 Million, indicating active consolidation within the sector.

Armored Vehicle Upgrade and Retrofit Industry Market Dynamics & Trends

The Armored Vehicle Upgrade and Retrofit industry is experiencing robust growth, primarily fueled by ongoing geopolitical tensions and the imperative for military forces worldwide to maintain and enhance their existing armored fleets. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.8% during the forecast period of 2025–2033. This expansion is intrinsically linked to the extended lifecycle of current armored platforms and the significant cost savings offered by retrofitting compared to acquiring entirely new vehicles. Technological disruptions are at the forefront of market evolution, with a strong emphasis on integrating next-generation sensors, advanced communication suites, improved ballistic protection, and sophisticated electronic warfare capabilities. Consumer preferences within defense procurement lean towards modularity, scalability, and platforms that can be rapidly adapted to evolving battlefield threats. The competitive dynamics are characterized by intense bidding processes for government contracts, strategic alliances between prime contractors and specialized technology providers, and a continuous drive for innovation to outpace adversaries. Market penetration is high in established defense markets, with emerging economies showing increasing adoption of modernization programs as their defense budgets grow. The shift towards digitalized warfare and the integration of artificial intelligence into vehicle systems are also significant influencing factors shaping consumer demand and industry strategies. Furthermore, the need to counter asymmetric threats and the proliferation of advanced anti-tank weaponry are accelerating the demand for advanced armor upgrades and active protection systems.

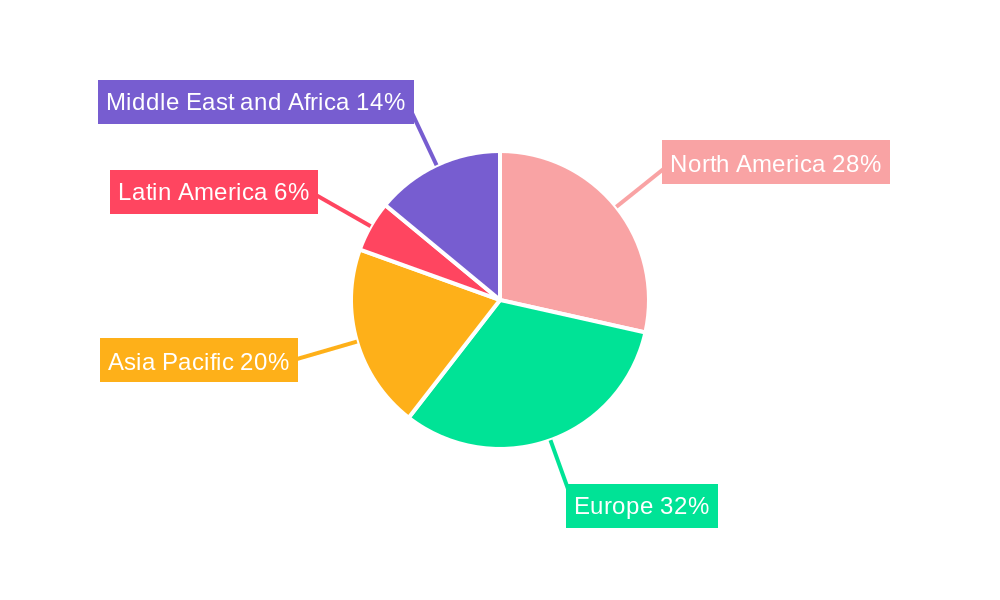

Dominant Regions & Segments in Armored Vehicle Upgrade and Retrofit Industry

North America, particularly the United States, currently dominates the Armored Vehicle Upgrade and Retrofit market, driven by substantial defense spending and a proactive approach to modernizing its extensive armored vehicle inventory. The US military's continuous operational demands and its commitment to maintaining technological superiority necessitate ongoing upgrade and retrofit programs. Key drivers for this regional dominance include robust economic policies supporting defense industrial bases, advanced technological infrastructure, and a strong ecosystem of defense contractors.

- Dominant Region: North America (USA)

- Economic Policies: High defense budgets allocated to modernization and sustainment programs.

- Technological Infrastructure: Advanced research and development capabilities leading to cutting-edge upgrade solutions.

- Geopolitical Imperatives: Continuous need for a technologically superior and readily deployable armored force.

- Procurement Processes: Well-established and consistent procurement cycles for vehicle upgrades.

Among the vehicle types, the Infantry Fighting Vehicle (IFV) segment is experiencing significant growth and commands a substantial market share, estimated to be around 30% of the total upgrade and retrofit market. This is due to IFVs being the backbone of modern infantry operations, requiring constant enhancement in firepower, mobility, and crew protection.

- Dominant Segment: Infantry Fighting Vehicle (IFV)

- Operational Versatility: IFVs are critical for troop transport, direct fire support, and reconnaissance missions, demanding continuous upgrades to remain effective.

- Technological Integration: Integration of advanced weapon systems, digital fire control, and active protection systems are high priorities.

- Cost-Effectiveness: Upgrading existing IFV platforms offers a more economical solution than procuring new ones for many nations.

- Modernization Initiatives: Numerous countries are actively engaged in upgrading their IFV fleets to counter emerging threats.

Other significant segments include Armored Personnel Carriers (APC) and Main Battle Tanks (MBT), both of which are undergoing extensive modernization to incorporate advanced survivability features and digital combat systems. Mine-resistant Ambush Protected (MRAP) vehicles also represent a crucial segment, particularly in regions with persistent counter-insurgency operations, focusing on enhanced mine and IED protection.

Armored Vehicle Upgrade and Retrofit Industry Product Innovations

Product innovations in the Armored Vehicle Upgrade and Retrofit industry are focused on enhancing survivability, situational awareness, and lethality. Key developments include the integration of modular active protection systems (APS) to counter threats like RPGs and ATGMs, advanced composite armor materials for improved ballistic protection with reduced weight, and sophisticated C4ISR integration for enhanced network-centric warfare capabilities. These innovations provide a competitive advantage by extending the operational lifespan of existing platforms, reducing acquisition costs, and ensuring readiness against evolving threats.

Report Scope & Segmentation Analysis

This report segments the Armored Vehicle Upgrade and Retrofit industry by vehicle type. The Armored Personnel Carrier (APC) segment is expected to see a healthy growth rate, driven by the need for protected troop mobility in various operational environments. Infantry Fighting Vehicle (IFV) upgrades are a major focus, with significant market share expected due to their combat-intensive roles. The Mine-resistant Ambush Protected (MRAP) segment will continue to be relevant, with ongoing demand for enhanced protection against IEDs and ambushes. Main Battle Tank (MBT) modernization efforts are crucial for maintaining battlefield dominance, focusing on upgrades to firepower, protection, and networked capabilities. Other Vehicle Types, including reconnaissance vehicles and command vehicles, will also see tailored upgrade programs reflecting their specific operational needs and evolving threats.

Key Drivers of Armored Vehicle Upgrade and Retrofit Industry Growth

Several factors are propelling the growth of the Armored Vehicle Upgrade and Retrofit industry. Firstly, geopolitical instability and the need to maintain a modernized military deterrent are significant drivers. Secondly, the escalating cost of acquiring new armored platforms makes retrofitting a more economically viable option for many nations. Technological advancements in areas like active protection systems, advanced armor, and digital integration are compelling defense forces to upgrade existing fleets. Furthermore, the extended service life of current armored vehicles necessitates periodic modernization to meet emerging threats and operational requirements.

Challenges in the Armored Vehicle Upgrade and Retrofit Industry Sector

The Armored Vehicle Upgrade and Retrofit industry faces several challenges. Regulatory hurdles and stringent military specifications can lengthen development and procurement cycles. Supply chain disruptions, particularly for specialized components and raw materials, can impact production timelines and costs. Intense competition among established and emerging players can lead to pricing pressures and reduced profit margins. Additionally, the obsolescence of older platforms can sometimes limit the scope and effectiveness of certain upgrades, necessitating more comprehensive and costly solutions.

Emerging Opportunities in Armored Vehicle Upgrade and Retrofit Industry

Emerging opportunities in the Armored Vehicle Upgrade and Retrofit industry are diverse. The increasing demand from emerging economies for modernized defense capabilities presents significant market potential. The development and integration of unmanned and optionally manned vehicle technologies offer new avenues for upgrades. Innovations in modular design and open architecture systems allow for more flexible and future-proof retrofitting. Furthermore, the growing emphasis on cyber-security for vehicle systems creates opportunities for specialized upgrade packages.

Leading Players in the Armored Vehicle Upgrade and Retrofit Industry Market

- Textron Inc

- THALES

- Oshkosh Corporation

- FNSS Savunma Sistemleri A S

- General Dynamics Corporation

- Rheinmetall AG

- Elbit Systems Ltd

- Patria Group

- Nexter Group

- BAE Systems PLC

- Bharat Electronics Limited (BEL)

- Ruag International Holding AG

Key Developments in Armored Vehicle Upgrade and Retrofit Industry Industry

- 2023: Rheinmetall AG secures a multi-million dollar contract for modernization of Leopard 2 MBTs with enhanced protection and digital systems.

- 2023: BAE Systems PLC announces successful integration of new active protection system on an Armored Personnel Carrier demonstrator.

- 2022: Oshkosh Corporation awarded a significant contract for the upgrade and sustainment of its MRAP vehicles for extended service life.

- 2022: Elbit Systems Ltd delivers advanced C4ISR upgrade kits for IFVs to a European customer.

- 2021: THALES partners with FNSS Savunma Sistemleri A S for the upgrade of Turkish-made armored vehicles with advanced sensor technology.

- 2020: General Dynamics Corporation completes a major retrofit program for its Abrams MBTs, enhancing firepower and survivability.

Future Outlook for Armored Vehicle Upgrade and Retrofit Industry Market

The future outlook for the Armored Vehicle Upgrade and Retrofit industry is exceptionally strong, characterized by sustained demand driven by ongoing global security concerns and the need for technological superiority. The market is poised for continued growth as nations prioritize modernizing their existing armored fleets to adapt to new warfare doctrines and emerging threats. Strategic investments in advanced technologies such as AI-enabled systems, drone integration, and enhanced electronic warfare capabilities will define future upgrade programs. The trend towards modularity and platform-agnostic solutions will also gain momentum, offering greater flexibility and cost-efficiency for defense forces worldwide.

Armored Vehicle Upgrade and Retrofit Industry Segmentation

-

1. Vehicle Type

- 1.1. Armored Personnel Carrier (APC)

- 1.2. Infantry Fighting Vehicle (IFV)

- 1.3. Mine-resistant Ambush Protected (MRAP)

- 1.4. Main Battle Tank (MBT)

- 1.5. Other Vehicle Types

Armored Vehicle Upgrade and Retrofit Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Egypt

- 5.4. Turkey

- 5.5. Rest of Middle East and Africa

Armored Vehicle Upgrade and Retrofit Industry Regional Market Share

Geographic Coverage of Armored Vehicle Upgrade and Retrofit Industry

Armored Vehicle Upgrade and Retrofit Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Armored Personnel Carrier (APC)

- 5.1.2. Infantry Fighting Vehicle (IFV)

- 5.1.3. Mine-resistant Ambush Protected (MRAP)

- 5.1.4. Main Battle Tank (MBT)

- 5.1.5. Other Vehicle Types

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Armored Personnel Carrier (APC)

- 6.1.2. Infantry Fighting Vehicle (IFV)

- 6.1.3. Mine-resistant Ambush Protected (MRAP)

- 6.1.4. Main Battle Tank (MBT)

- 6.1.5. Other Vehicle Types

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Armored Personnel Carrier (APC)

- 7.1.2. Infantry Fighting Vehicle (IFV)

- 7.1.3. Mine-resistant Ambush Protected (MRAP)

- 7.1.4. Main Battle Tank (MBT)

- 7.1.5. Other Vehicle Types

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Armored Personnel Carrier (APC)

- 8.1.2. Infantry Fighting Vehicle (IFV)

- 8.1.3. Mine-resistant Ambush Protected (MRAP)

- 8.1.4. Main Battle Tank (MBT)

- 8.1.5. Other Vehicle Types

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Armored Personnel Carrier (APC)

- 9.1.2. Infantry Fighting Vehicle (IFV)

- 9.1.3. Mine-resistant Ambush Protected (MRAP)

- 9.1.4. Main Battle Tank (MBT)

- 9.1.5. Other Vehicle Types

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Latin America Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Armored Personnel Carrier (APC)

- 10.1.2. Infantry Fighting Vehicle (IFV)

- 10.1.3. Mine-resistant Ambush Protected (MRAP)

- 10.1.4. Main Battle Tank (MBT)

- 10.1.5. Other Vehicle Types

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.1.1. Armored Personnel Carrier (APC)

- 11.1.2. Infantry Fighting Vehicle (IFV)

- 11.1.3. Mine-resistant Ambush Protected (MRAP)

- 11.1.4. Main Battle Tank (MBT)

- 11.1.5. Other Vehicle Types

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Textron Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 THALES

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Oshkosh Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 FNSS Savunma Sistemleri A S

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 General Dynamics Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rheinmetall AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Elbit Systems Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Patria Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nexter Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 BAE Systems PLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Bharat Electronics Limited (BEL

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ruag International Holding AG

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Textron Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Armored Vehicle Upgrade and Retrofit Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 3: North America Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 7: Europe Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: Europe Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 11: Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 15: Latin America Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Latin America Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Latin America Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 19: Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 8: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: France Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Germany Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Russia Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Rest of Europe Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: China Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: India Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Japan Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: South Korea Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Asia Pacific Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 22: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 23: Brazil Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of Latin America Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 26: Global Armored Vehicle Upgrade and Retrofit Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Arab Emirates Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Saudi Arabia Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Egypt Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Turkey Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East and Africa Armored Vehicle Upgrade and Retrofit Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Armored Vehicle Upgrade and Retrofit Industry?

The projected CAGR is approximately 3.3%.

2. Which companies are prominent players in the Armored Vehicle Upgrade and Retrofit Industry?

Key companies in the market include Textron Inc, THALES, Oshkosh Corporation, FNSS Savunma Sistemleri A S, General Dynamics Corporation, Rheinmetall AG, Elbit Systems Ltd, Patria Group, Nexter Group, BAE Systems PLC, Bharat Electronics Limited (BEL, Ruag International Holding AG.

3. What are the main segments of the Armored Vehicle Upgrade and Retrofit Industry?

The market segments include Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 51.6 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Infantry Fighting Vehicle (IFV) Segment Dominates the Market During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Armored Vehicle Upgrade and Retrofit Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Armored Vehicle Upgrade and Retrofit Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Armored Vehicle Upgrade and Retrofit Industry?

To stay informed about further developments, trends, and reports in the Armored Vehicle Upgrade and Retrofit Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence