Key Insights

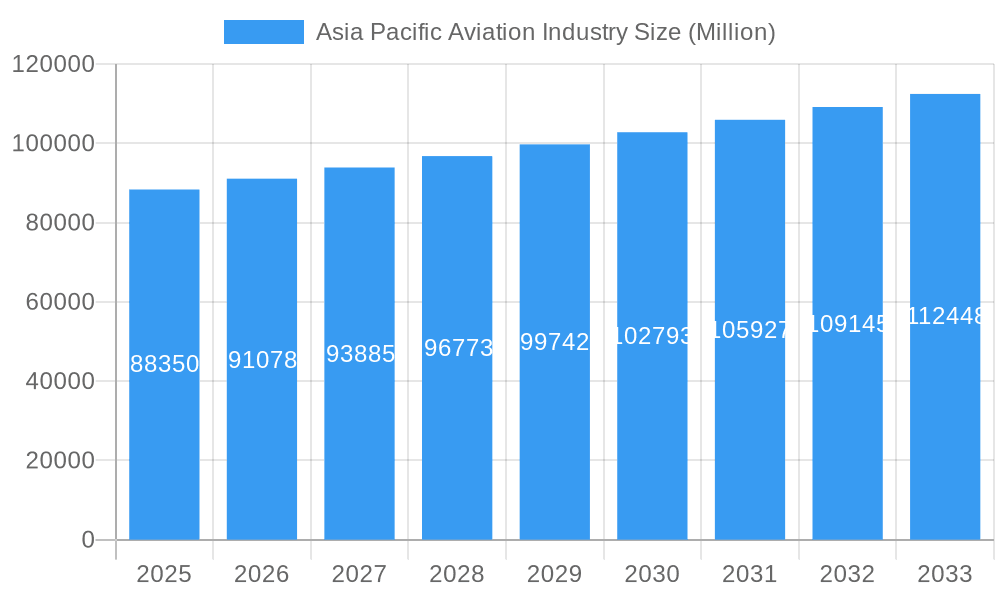

The Asia-Pacific aviation industry, valued at $88.35 billion in 2025, is projected to experience steady growth, driven by factors such as rising disposable incomes, increasing air travel demand, and robust economic expansion across the region. Key growth drivers include the burgeoning middle class in countries like China and India, fueling a surge in leisure and business travel. Furthermore, government initiatives to improve infrastructure, including airport expansions and upgrades, are significantly contributing to the industry's expansion. The segment encompassing commercial aircraft is expected to dominate the market share, given the increasing need for efficient and reliable passenger transportation within the densely populated regions. However, challenges remain, including geopolitical uncertainties, fluctuating fuel prices, and the potential impact of environmental regulations on the industry's sustainability. Competition amongst established players like Boeing, Airbus, and regional manufacturers is fierce, leading to innovation in aircraft design and technological advancements to improve fuel efficiency and enhance passenger experience. The robust growth forecast for the Asia-Pacific aviation industry reflects a positive outlook for the coming decade, though careful navigation of these challenges is crucial for sustained success.

Asia Pacific Aviation Industry Market Size (In Billion)

The forecast period from 2025 to 2033 presents opportunities for strategic expansion and investment. Specific countries within the Asia-Pacific region, like China, Japan, India, and South Korea, are expected to contribute significantly to the overall growth, driven by their substantial domestic air travel markets and expanding international connectivity. The military aircraft segment will likely see moderate growth, primarily driven by government defense budgets and regional security concerns. The general aviation segment, including private and business jets, will also show growth, though potentially at a slower pace compared to commercial aircraft. This growth trajectory highlights the need for increased investment in aviation infrastructure, skilled workforce development, and the adoption of sustainable practices to mitigate environmental impact. Manufacturers are focusing on the development of fuel-efficient aircraft and exploring alternative fuels to meet growing environmental concerns and evolving regulatory landscapes.

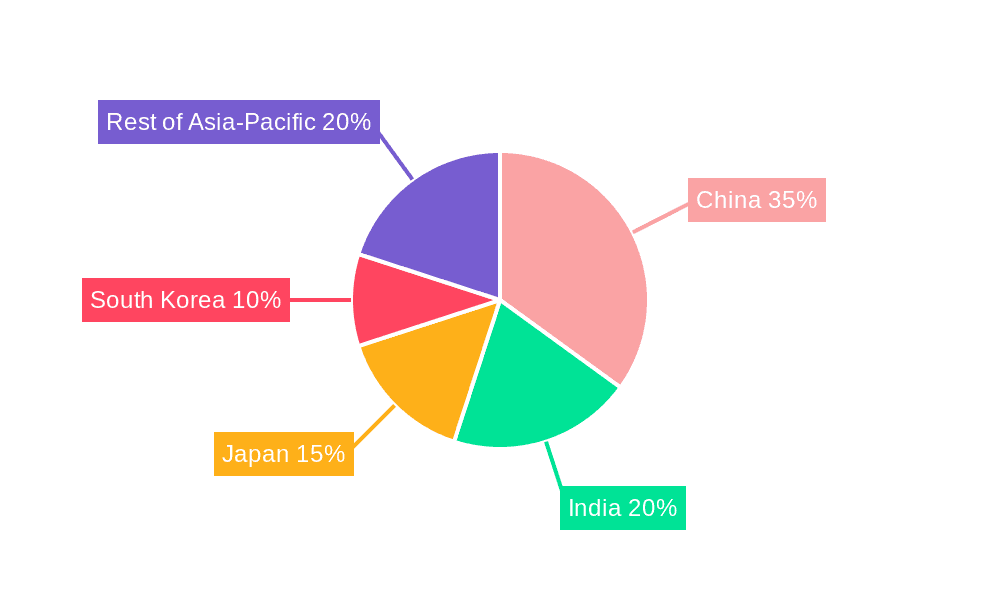

Asia Pacific Aviation Industry Company Market Share

Asia Pacific Aviation Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Asia Pacific aviation industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report analyzes market structure, dynamics, key players, and future growth prospects. The report leverages extensive data analysis to forecast robust growth and identify lucrative investment opportunities within this dynamic sector. Expect detailed breakdowns by segment (Freighter, Military Aircraft, Non-combat Aircraft, General Aviation, and Commercial Aircraft), revealing market leaders and high-growth areas. This is your definitive guide to navigating the complexities and unlocking the potential of the Asia Pacific aviation market.

Asia Pacific Aviation Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory influences within the Asia Pacific aviation industry. The market is characterized by a mix of large multinational corporations and regional players. Market concentration is moderate, with several key players holding significant market share. However, emerging players continue to challenge the established order.

- Market Share: The Boeing Company and Airbus SE hold the largest market shares in the commercial aircraft segment, followed by Commercial Aircraft Corporation of China Ltd (COMAC) which is steadily increasing its share. In the military aircraft segment, players like Lockheed Martin Corporation and General Dynamics Corporation hold prominent positions. Precise market share figures for 2025 are projected to be xx%.

- M&A Activity: The Asia Pacific aviation industry has witnessed considerable M&A activity in recent years, with deal values exceeding USD xx Million in the period between 2019-2024. These activities primarily focus on strengthening technology portfolios, expanding regional reach, and gaining access to new markets. These trends will likely continue, driven by consolidation and the pursuit of economies of scale.

- Innovation Drivers: Key innovation drivers include the development of more fuel-efficient aircraft, advancements in aerospace materials, and the integration of digital technologies for enhanced operational efficiency. Regulatory frameworks are playing a pivotal role in shaping innovation trajectories, encouraging sustainable practices, and ensuring safety standards. Substitutes for air travel, such as high-speed rail, are gaining traction in certain markets, posing a moderate challenge to air travel growth. End-user demographics show a rising middle class fueling demand, particularly in regions with growing economies.

Asia Pacific Aviation Industry Market Dynamics & Trends

The Asia Pacific aviation industry is characterized by strong growth drivers, significant technological advancements, evolving consumer preferences, and intense competitive dynamics. The industry has experienced fluctuating growth in recent years, due to the impact of geopolitical events and the COVID-19 pandemic. This report projects a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, driven by factors such as increasing air passenger traffic, robust economic growth in several key markets, and expanding airfreight volumes. Market penetration is expected to increase significantly in secondary and tertiary cities within the region. Technological disruptions, such as the development of electric and hybrid-electric aircraft, are also expected to reshape the industry's landscape in the coming years.

Dominant Regions & Segments in Asia Pacific Aviation Industry

The Asia Pacific aviation industry exhibits significant regional variations. While China, India, Japan, and Australia remain leading markets for both passenger and cargo transportation, other Southeast Asian nations are experiencing rapid growth. Several factors contribute to this varied landscape.

- Commercial Aircraft: China is a dominant market, with significant growth fueled by its burgeoning middle class and expanding economic activity. India is also witnessing rapid growth due to increased domestic and international connectivity.

- Military Aircraft: Many Asia Pacific countries are investing heavily in modernizing their defense fleets, driving demand for advanced military aircraft. Japan and South Korea are key markets.

- General Aviation: Australia and certain Southeast Asian countries show promising growth in general aviation driven by leisure travel, tourism, and business needs.

- Key Drivers: Strong economic growth, government investments in infrastructure (airports and air traffic control), and increasing disposable income are key contributors to regional dominance.

Asia Pacific Aviation Industry Product Innovations

The Asia Pacific aviation industry is characterized by ongoing product innovation, focusing on enhanced fuel efficiency, advanced avionics, and increased passenger comfort. Manufacturers are increasingly adopting lighter materials, improving aerodynamic designs, and integrating digital technologies for improved operational efficiency and sustainability. These innovations are aimed at enhancing competitive advantages and meeting the evolving demands of passengers and airlines.

Report Scope & Segmentation Analysis

This report segments the Asia Pacific aviation industry into key categories: Freighter, Military Aircraft, Non-combat Aircraft, and Commercial Aircraft. Each segment presents distinct growth projections, market sizes, and competitive dynamics. The Commercial Aircraft segment is the largest, followed by the Freighter segment. Within each segment, individual aircraft types (e.g., single-aisle, twin-aisle) exhibit varying growth trajectories. The military aircraft segment shows steady growth driven by defense spending in the region, while the general aviation sector experiences moderate growth.

Key Drivers of Asia Pacific Aviation Industry Growth

Several factors contribute to the growth of the Asia Pacific aviation industry. Firstly, the region's robust economic expansion fuels rising disposable incomes and increased travel demand. Secondly, government investments in infrastructure development, particularly airport upgrades and expansion, enhance connectivity. Thirdly, technological advancements, such as fuel-efficient aircraft and improved navigation systems, drive operational efficiencies and reduce costs. Fourthly, supportive government policies and deregulation in some areas further boost sector growth.

Challenges in the Asia Pacific Aviation Industry Sector

The Asia Pacific aviation industry faces several challenges, including escalating fuel prices, increasing competition, and regulatory complexities in different markets. Supply chain disruptions also impact manufacturing and maintenance activities. These factors could lead to increased operating costs and potentially affect the industry's overall profitability. The estimated impact on the overall revenue is projected to be USD xx Million in 2025.

Emerging Opportunities in Asia Pacific Aviation Industry

The Asia Pacific aviation industry presents several emerging opportunities. Growth in low-cost carriers, expansion into underserved markets, and the rise of air cargo demand present significant potentials. Technological innovations, such as drone delivery systems and advanced air mobility, could also create new revenue streams and business models. The development of sustainable aviation fuels (SAFs) presents a crucial opportunity to mitigate environmental concerns.

Leading Players in the Asia Pacific Aviation Industry Market

- Textron Inc

- Dassault Aviation SA

- Commercial Aircraft Corporation of China Ltd

- General Dynamics Corporation

- Leonardo SpA

- Lockheed Martin Corporation

- Airbus SE

- Hindustan Aeronautics Limited (HAL)

- Korea Aerospace Industries Ltd

- Honda Motor Co Ltd

- Aviation Industry Corporation of China

- ROSTEC

- Kawasaki Heavy Industries Ltd

- The Boeing Company

Key Developments in Asia Pacific Aviation Industry

- February 2022: Singapore Airlines placed a firm order for seven Airbus A350F aircraft, with options for five more, replacing Boeing 747-400F aircraft. Deliveries begin Q4 2025.

- February 2022: Boeing awarded a USD 103.7 Million contract by the US Department of Defense to supply Thailand with eight AH-6 helicopters, replacing AH-1F Cobras. Deliveries expected through 2024.

Future Outlook for Asia Pacific Aviation Industry Market

The Asia Pacific aviation industry is poised for continued growth, driven by increasing passenger traffic, expanding air freight volumes, and government initiatives supporting infrastructure development. Strategic opportunities lie in leveraging technological advancements, focusing on sustainability, and capitalizing on the growth of emerging markets. This presents significant opportunities for airlines, manufacturers, and related businesses to capture substantial market share and drive long-term profitability.

Asia Pacific Aviation Industry Segmentation

-

1. Type

-

1.1. Commercial Aviation

- 1.1.1. Passenger Aircraft

- 1.1.2. Freighter

-

1.2. Military Aviation

- 1.2.1. Combat Aircraft

- 1.2.2. Non-combat Aircraft

-

1.3. General Aviation

- 1.3.1. Helicopter

- 1.3.2. Piston Fixed-wing Aircraft

- 1.3.3. Turboprop Aircraft

- 1.3.4. Business Jets

-

1.1. Commercial Aviation

-

2. Geography

- 2.1. China

- 2.2. India

- 2.3. Japan

- 2.4. South Korea

- 2.5. Australia

- 2.6. Rest of Asia-Pacific

Asia Pacific Aviation Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. South Korea

- 5. Australia

- 6. Rest of Asia Pacific

Asia Pacific Aviation Industry Regional Market Share

Geographic Coverage of Asia Pacific Aviation Industry

Asia Pacific Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.97% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Commercial Aircraft Segment Projected to Witness the Highest CAGR During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. Passenger Aircraft

- 5.1.1.2. Freighter

- 5.1.2. Military Aviation

- 5.1.2.1. Combat Aircraft

- 5.1.2.2. Non-combat Aircraft

- 5.1.3. General Aviation

- 5.1.3.1. Helicopter

- 5.1.3.2. Piston Fixed-wing Aircraft

- 5.1.3.3. Turboprop Aircraft

- 5.1.3.4. Business Jets

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. China

- 5.2.2. India

- 5.2.3. Japan

- 5.2.4. South Korea

- 5.2.5. Australia

- 5.2.6. Rest of Asia-Pacific

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. South Korea

- 5.3.5. Australia

- 5.3.6. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. Passenger Aircraft

- 6.1.1.2. Freighter

- 6.1.2. Military Aviation

- 6.1.2.1. Combat Aircraft

- 6.1.2.2. Non-combat Aircraft

- 6.1.3. General Aviation

- 6.1.3.1. Helicopter

- 6.1.3.2. Piston Fixed-wing Aircraft

- 6.1.3.3. Turboprop Aircraft

- 6.1.3.4. Business Jets

- 6.1.1. Commercial Aviation

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. China

- 6.2.2. India

- 6.2.3. Japan

- 6.2.4. South Korea

- 6.2.5. Australia

- 6.2.6. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. India Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Commercial Aviation

- 7.1.1.1. Passenger Aircraft

- 7.1.1.2. Freighter

- 7.1.2. Military Aviation

- 7.1.2.1. Combat Aircraft

- 7.1.2.2. Non-combat Aircraft

- 7.1.3. General Aviation

- 7.1.3.1. Helicopter

- 7.1.3.2. Piston Fixed-wing Aircraft

- 7.1.3.3. Turboprop Aircraft

- 7.1.3.4. Business Jets

- 7.1.1. Commercial Aviation

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. China

- 7.2.2. India

- 7.2.3. Japan

- 7.2.4. South Korea

- 7.2.5. Australia

- 7.2.6. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Japan Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Commercial Aviation

- 8.1.1.1. Passenger Aircraft

- 8.1.1.2. Freighter

- 8.1.2. Military Aviation

- 8.1.2.1. Combat Aircraft

- 8.1.2.2. Non-combat Aircraft

- 8.1.3. General Aviation

- 8.1.3.1. Helicopter

- 8.1.3.2. Piston Fixed-wing Aircraft

- 8.1.3.3. Turboprop Aircraft

- 8.1.3.4. Business Jets

- 8.1.1. Commercial Aviation

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. China

- 8.2.2. India

- 8.2.3. Japan

- 8.2.4. South Korea

- 8.2.5. Australia

- 8.2.6. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. South Korea Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Commercial Aviation

- 9.1.1.1. Passenger Aircraft

- 9.1.1.2. Freighter

- 9.1.2. Military Aviation

- 9.1.2.1. Combat Aircraft

- 9.1.2.2. Non-combat Aircraft

- 9.1.3. General Aviation

- 9.1.3.1. Helicopter

- 9.1.3.2. Piston Fixed-wing Aircraft

- 9.1.3.3. Turboprop Aircraft

- 9.1.3.4. Business Jets

- 9.1.1. Commercial Aviation

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. China

- 9.2.2. India

- 9.2.3. Japan

- 9.2.4. South Korea

- 9.2.5. Australia

- 9.2.6. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Commercial Aviation

- 10.1.1.1. Passenger Aircraft

- 10.1.1.2. Freighter

- 10.1.2. Military Aviation

- 10.1.2.1. Combat Aircraft

- 10.1.2.2. Non-combat Aircraft

- 10.1.3. General Aviation

- 10.1.3.1. Helicopter

- 10.1.3.2. Piston Fixed-wing Aircraft

- 10.1.3.3. Turboprop Aircraft

- 10.1.3.4. Business Jets

- 10.1.1. Commercial Aviation

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. China

- 10.2.2. India

- 10.2.3. Japan

- 10.2.4. South Korea

- 10.2.5. Australia

- 10.2.6. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Asia Pacific Asia Pacific Aviation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Commercial Aviation

- 11.1.1.1. Passenger Aircraft

- 11.1.1.2. Freighter

- 11.1.2. Military Aviation

- 11.1.2.1. Combat Aircraft

- 11.1.2.2. Non-combat Aircraft

- 11.1.3. General Aviation

- 11.1.3.1. Helicopter

- 11.1.3.2. Piston Fixed-wing Aircraft

- 11.1.3.3. Turboprop Aircraft

- 11.1.3.4. Business Jets

- 11.1.1. Commercial Aviation

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. China

- 11.2.2. India

- 11.2.3. Japan

- 11.2.4. South Korea

- 11.2.5. Australia

- 11.2.6. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2025

- 12.2. Company Profiles

- 12.2.1 Textron Inc

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Dassault Aviation SA

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Commercial Aircraft Corporation of China Ltd

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 General Dynamics Corporation

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Leonardo SpA

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Lockheed Martin Corporation

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Airbus SE

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Hindustan Aeronautics Limited (HAL)

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Korea Aerospace Industries Ltd

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Honda Motor Co Ltd

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.11 Aviation Industry Corporation of Chin

- 12.2.11.1. Overview

- 12.2.11.2. Products

- 12.2.11.3. SWOT Analysis

- 12.2.11.4. Recent Developments

- 12.2.11.5. Financials (Based on Availability)

- 12.2.12 ROSTEC

- 12.2.12.1. Overview

- 12.2.12.2. Products

- 12.2.12.3. SWOT Analysis

- 12.2.12.4. Recent Developments

- 12.2.12.5. Financials (Based on Availability)

- 12.2.13 Kawasaki Heavy Industries Ltd

- 12.2.13.1. Overview

- 12.2.13.2. Products

- 12.2.13.3. SWOT Analysis

- 12.2.13.4. Recent Developments

- 12.2.13.5. Financials (Based on Availability)

- 12.2.14 The Boeing Company

- 12.2.14.1. Overview

- 12.2.14.2. Products

- 12.2.14.3. SWOT Analysis

- 12.2.14.4. Recent Developments

- 12.2.14.5. Financials (Based on Availability)

- 12.2.1 Textron Inc

List of Figures

- Figure 1: Asia Pacific Aviation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Aviation Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: Asia Pacific Aviation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 15: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Asia Pacific Aviation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Asia Pacific Aviation Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 21: Asia Pacific Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Aviation Industry?

The projected CAGR is approximately 2.97%.

2. Which companies are prominent players in the Asia Pacific Aviation Industry?

Key companies in the market include Textron Inc, Dassault Aviation SA, Commercial Aircraft Corporation of China Ltd, General Dynamics Corporation, Leonardo SpA, Lockheed Martin Corporation, Airbus SE, Hindustan Aeronautics Limited (HAL), Korea Aerospace Industries Ltd, Honda Motor Co Ltd, Aviation Industry Corporation of Chin, ROSTEC, Kawasaki Heavy Industries Ltd, The Boeing Company.

3. What are the main segments of the Asia Pacific Aviation Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 88.35 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Commercial Aircraft Segment Projected to Witness the Highest CAGR During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In February 2022, Singapore Airlines (SIA) placed a firm order for seven Airbus A350F aircraft, with an option for additional five aircraft at the Singapore Airshow 2022. The new Airbus A350F aircraft are planned to replace the seven Boeing 747-400F aircraft in service. The delivery of the aircraft is scheduled to begin by the fourth quarter of 2025.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Aviation Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence