Key Insights

The UK Banking as a Service (BaaS) market is projected for substantial growth, fueled by technological innovation, evolving customer needs, and a supportive regulatory environment. With a market size of £1.1 billion in the base year 2024, the BaaS sector is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 12.6%, reaching an estimated value of over £1.1 billion by 2024. Key growth drivers include the increasing demand for embedded finance, enabling non-financial entities to integrate banking functions into their offerings. Digital transformation within traditional banking, alongside the rise of challenger banks and FinTechs, is accelerating BaaS adoption. These platforms facilitate agile development, cost efficiencies, and faster product launches, crucial for competitive businesses. An API-first strategy and cloud-native infrastructure are central to this expansion, enhancing connectivity and scalability.

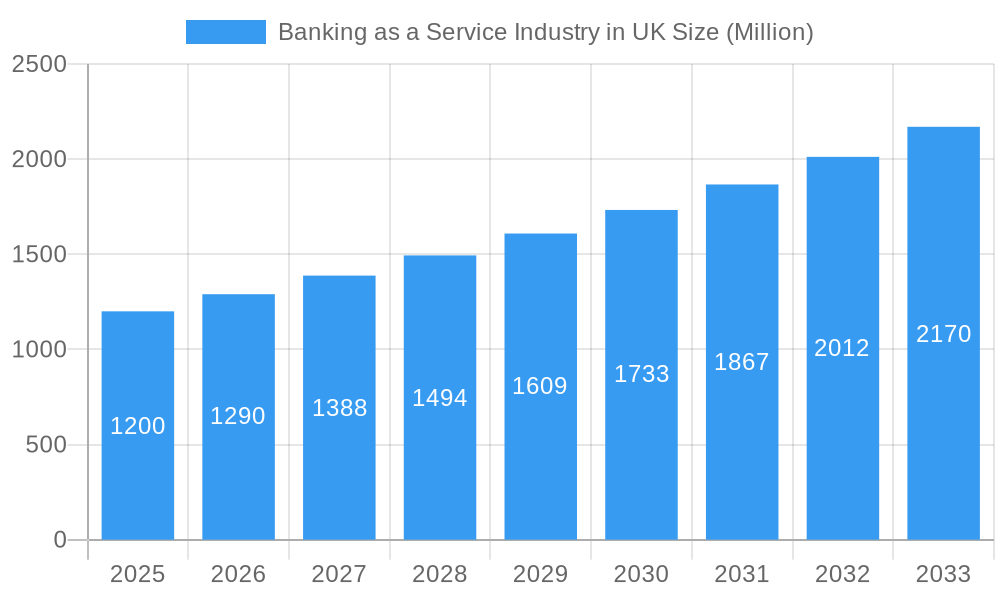

Banking as a Service Industry in UK Market Size (In Billion)

The UK BaaS market features dynamic segmentation in platform and service components. Professional services, including integration, consulting, and implementation, will be in high demand. Managed services, providing ongoing operational support, represent another significant growth avenue. API-based BaaS solutions lead in product types due to their flexibility and integration ease, while cloud-based BaaS offers scalability and cost benefits. Large enterprises are leveraging BaaS to enhance customer offerings and streamline operations. Small and medium-sized enterprises (SMEs) gain access to advanced financial tools. Banks, challenger banks, and FinTechs are primary end-users driving BaaS innovation. While data security and regulatory compliance present challenges, continuous innovation and evolving industry standards are mitigating these concerns, reinforcing the UK's leadership in the global BaaS market.

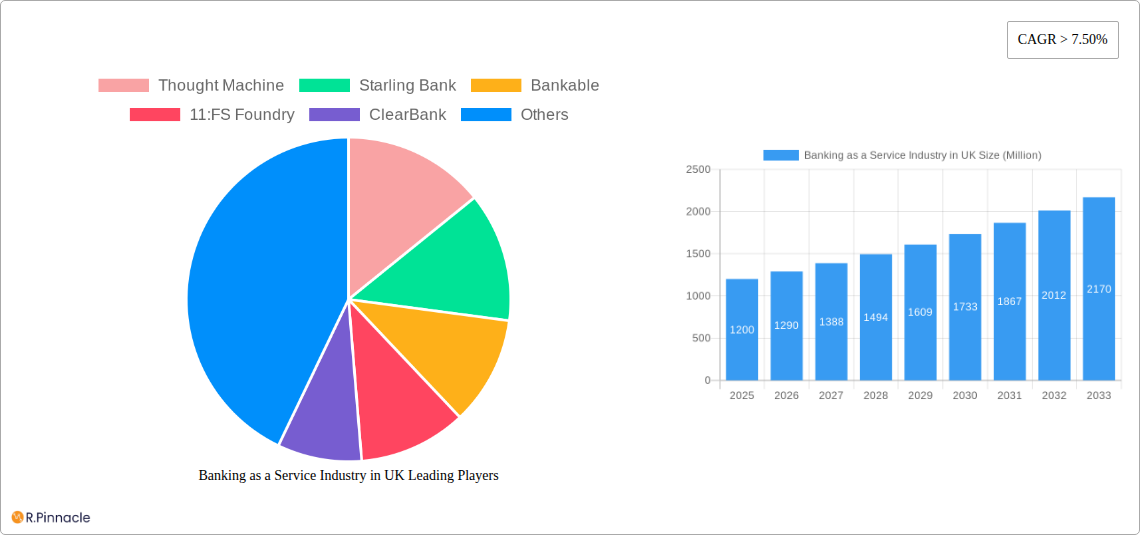

Banking as a Service Industry in UK Company Market Share

Unlocking the UK's Banking as a Service (BaaS) Landscape: A Comprehensive Industry Report (2019-2033)

This in-depth report provides an authoritative analysis of the UK's rapidly evolving Banking as a Service (BaaS) industry. Delve into market dynamics, innovation trends, and strategic opportunities shaping the future of embedded finance. With data spanning from 2019 to 2033, this report is an essential resource for banks, fintech corporations, NBFCs, technology providers, and investors seeking to capitalize on the immense growth potential of BaaS in the UK. Our analysis covers key segments including API-based BaaS, cloud-based BaaS, professional and managed services, and caters to both large enterprises and SMEs.

Banking as a Service Industry in UK Market Structure & Innovation Trends

The UK's Banking as a Service (BaaS) market exhibits a moderately concentrated structure, driven by a handful of key platform providers and a growing ecosystem of specialized service enablers. Innovation is primarily fueled by the relentless demand for seamless, embedded financial experiences, propelled by advancements in API technology and cloud infrastructure. Regulatory frameworks, such as Open Banking, continue to be a significant catalyst, fostering competition and encouraging new business models. Product substitutes, while present in traditional banking, are increasingly being challenged by the agility and cost-effectiveness of BaaS solutions. The end-user demographic is broad, encompassing traditional banks seeking to modernize, nimble fintech corporations launching innovative products, and various other businesses looking to integrate financial services. Mergers and acquisitions (M&A) activity is on the rise, with deal values estimated to reach several hundred million Pounds as larger players consolidate their positions or acquire specialized capabilities. For instance, the strategic acquisition of BaaS platforms or fintechs with strong API capabilities is a common M&A target. The market share of leading BaaS providers is dynamic, with significant growth anticipated for those offering comprehensive and scalable solutions. Key innovation drivers include the pursuit of superior customer experience, operational efficiency gains, and the development of niche financial products tailored to specific industry verticals.

Banking as a Service Industry in UK Market Dynamics & Trends

The UK's Banking as a Service (BaaS) market is experiencing exponential growth, driven by a confluence of technological advancements, evolving consumer expectations, and supportive regulatory initiatives. The Compound Annual Growth Rate (CAGR) is projected to be substantial, with market penetration steadily increasing across diverse sectors. Technological disruptions, particularly the widespread adoption of cloud-based BaaS and API-based BaaS solutions, have lowered entry barriers for new financial service providers and enabled existing institutions to offer more agile and personalized customer experiences. The proliferation of smartphones and the increasing comfort of consumers with digital transactions have further fueled demand for embedded financial services, seamlessly integrated into non-financial platforms. From e-commerce checkout to ride-sharing apps, consumers now expect financial functionalities to be an intuitive part of their daily digital interactions. This shift in consumer preference is compelling businesses across various industries to explore BaaS offerings, leading to a diversification of end-users beyond traditional banking.

The competitive dynamics within the UK BaaS landscape are characterized by intense innovation and strategic partnerships. Established banks are increasingly partnering with or acquiring BaaS providers to accelerate their digital transformation journeys, while fintechs are leveraging BaaS to scale their operations and expand their product portfolios. The rise of specialized BaaS platforms, offering niche functionalities such as payment processing, account management, or lending orchestration, is creating a more sophisticated and fragmented market. This fragmentation, however, also presents opportunities for collaboration and ecosystem building. The focus on enhancing customer journeys, reducing operational costs, and creating new revenue streams are the primary growth drivers. Furthermore, the ongoing evolution of regulatory frameworks, such as those encouraging data sharing and competition, is creating a fertile ground for BaaS adoption. The anticipated market size for BaaS in the UK is projected to reach tens of billions of Pounds by the end of the forecast period, underscoring its significance as a transformative force in the financial services industry. The ongoing investment in next-generation technologies, including AI and blockchain, is expected to further accelerate this growth by enabling more sophisticated and secure BaaS solutions.

Dominant Regions & Segments in Banking as a Service Industry in UK

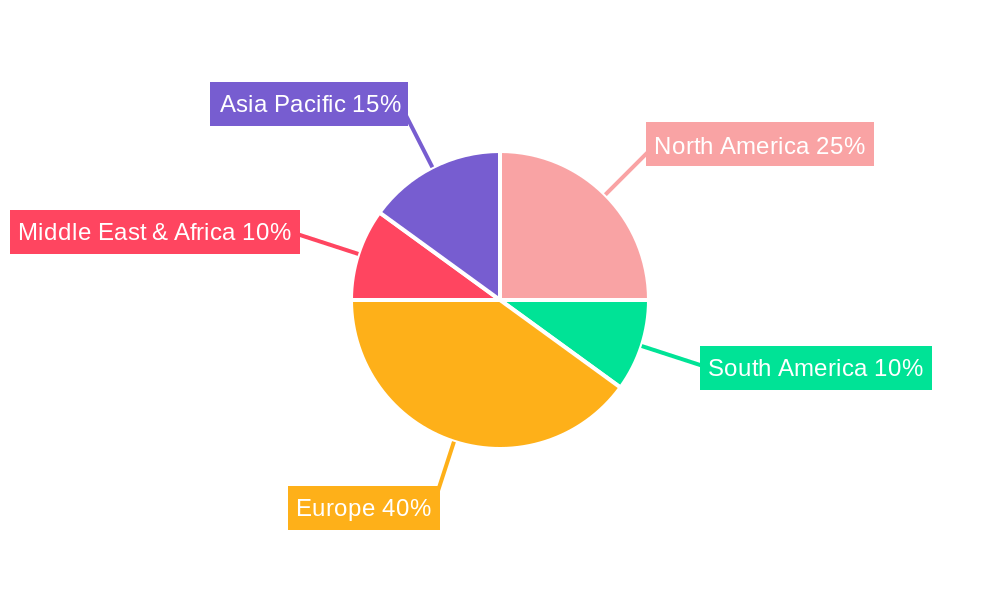

The United Kingdom stands as the dominant region in the European Banking as a Service (BaaS) market, largely due to its progressive regulatory environment, robust financial infrastructure, and a vibrant fintech ecosystem. Within the UK, the Component: Platform segment is currently the most dominant, forming the foundational layer upon which other BaaS services are built. Key drivers for this dominance include significant investment in cloud infrastructure and the widespread adoption of API-first strategies by financial institutions and technology providers. The Service: Professional Service segment also plays a crucial role, providing the expertise necessary for implementation, customization, and ongoing support, vital for integrating complex BaaS solutions. Economic policies that encourage innovation and competition, such as the Financial Conduct Authority's (FCA) sandbox initiatives, have further propelled the growth of this segment.

Analyzing Product Type, API-based BaaS leads the market, offering unparalleled flexibility and enabling seamless integration of financial functionalities into third-party applications. The ease with which businesses can leverage APIs to embed payments, accounts, or lending capabilities directly into their platforms is a primary driver of its dominance. Cloud-based BaaS is a close contender, providing scalability, cost-effectiveness, and rapid deployment capabilities, which are essential for both large enterprises and small and medium enterprises (SMEs). In terms of Enterprise Size, Large enterprise currently holds a significant market share, benefiting from the resources to invest in and integrate sophisticated BaaS solutions. However, the Small & Medium enterprise segment is showing rapid growth, driven by the accessibility and cost-effectiveness of cloud-based and API-driven BaaS offerings that allow them to compete with larger players.

The End-User landscape is dominated by NBFC/Fintech Corporations, who are at the forefront of leveraging BaaS to launch innovative products and services. Their agile nature and focus on digital customer experiences make them natural adopters of BaaS. Banks are also increasingly embracing BaaS, either to enhance their existing offerings or to collaborate with fintechs. Other end-users, including retailers and e-commerce platforms looking to offer embedded financial services, represent a growing but currently smaller segment. Infrastructure development, such as the availability of high-speed internet and secure data centers, is a critical enabler for the dominance of cloud and API-based BaaS. Furthermore, the presence of established payment networks and a culture of digital innovation within the UK contribute significantly to the leading position of these segments.

Banking as a Service Industry in UK Product Innovations

The UK BaaS industry is witnessing a surge in product innovations centered around enhancing embedded finance capabilities and streamlining operational efficiencies. Key developments include the creation of more granular and specialized APIs that allow for the integration of a wider range of financial services, from basic payment processing to complex lending and investment functionalities. Cloud-native BaaS platforms are offering enhanced scalability and security, enabling financial institutions and fintechs to deploy new products and services with unprecedented speed. Competitive advantages are being derived from offering end-to-end solutions that cover the entire financial lifecycle, from customer onboarding and Know Your Customer (KYC) processes to transaction management and regulatory compliance. Technological trends such as AI-powered fraud detection and personalized financial advice are being integrated into BaaS offerings, improving both customer experience and risk management. Market fit is being achieved through a deep understanding of specific industry needs, leading to vertical-specific BaaS solutions for sectors like healthcare, travel, and gaming.

Report Scope & Segmentation Analysis

This report meticulously analyzes the UK Banking as a Service (BaaS) industry across several key dimensions. The Component segmentation includes Platform, the core infrastructure enabling BaaS, and Service, further divided into Professional Service (consulting, implementation) and Managed Service (ongoing operations, support). Growth projections for the platform segment are robust, driven by increasing demand for scalable infrastructure. The Product Type segmentation focuses on API-based BaaS, emphasizing its flexibility and rapid integration capabilities, and Cloud-based BaaS, highlighting its scalability and cost-effectiveness. API-based BaaS is expected to witness significant market share gains due to its inherent agility. The Enterprise Size segmentation distinguishes between Large enterprise, which benefits from comprehensive integration, and Small & Medium enterprise, which gains access to advanced financial tools at a lower cost. SMEs represent a high-growth segment with substantial market potential. Finally, the End-User segmentation categorizes market participants as Banks, NBFC/Fintech Corporations, and Others, with fintechs leading current adoption and driving competitive dynamics. The market size for NBFC/Fintech Corporations is projected to grow exponentially.

Key Drivers of Banking as a Service Industry in UK Growth

The UK's Banking as a Service (BaaS) industry is propelled by several potent growth drivers. Technological advancements, particularly the maturity of API technology and the widespread adoption of cloud computing, have made it easier and more cost-effective to integrate financial services. The economic imperative for businesses to enhance customer experience and create new revenue streams by embedding financial products into their core offerings is a significant motivator. Furthermore, regulatory tailwinds, such as the commitment to Open Banking principles and initiatives promoting financial innovation, create a fertile ground for BaaS expansion. The increasing demand for personalized and seamless digital experiences from consumers is also a crucial driver, forcing non-financial companies to adopt BaaS to remain competitive. For example, the integration of payment gateways within retail apps is a direct response to this consumer preference.

Challenges in the Banking as a Service Industry in UK Sector

Despite its strong growth trajectory, the UK Banking as a Service (BaaS) sector faces several significant challenges. Regulatory hurdles remain a primary concern, with evolving compliance requirements and the need for robust data security and privacy measures demanding constant attention and investment. Supply chain complexities, particularly the reliance on third-party technology providers and the intricate web of partnerships required for comprehensive BaaS offerings, can lead to operational vulnerabilities and delays. Competitive pressures are intensifying as more players enter the market, leading to potential commoditization of certain services and a need for continuous differentiation. The cost of technology investment and integration, while decreasing, can still be substantial for some businesses, acting as a barrier to entry. For instance, the implementation of secure API gateways and compliance with stringent AML/KYC regulations can require significant upfront capital expenditure, impacting the adoption rates for smaller entities.

Emerging Opportunities in Banking as a Service Industry in UK

The UK Banking as a Service (BaaS) industry is ripe with emerging opportunities, driven by evolving consumer preferences and technological advancements. The expansion of embedded finance into new verticals, such as embedded insurance, embedded investments, and embedded lending beyond traditional credit products, presents a vast untapped market. The increasing adoption of decentralized finance (DeFi) principles and technologies could also pave the way for novel BaaS offerings, providing greater transparency and efficiency. Consumer demand for highly personalized financial solutions, facilitated by AI and machine learning, offers opportunities for BaaS providers to offer intelligent financial advice and tailored product recommendations. Furthermore, the growing focus on sustainability and ESG (Environmental, Social, and Governance) factors is creating a demand for BaaS solutions that support green finance initiatives and ethical investing. The development of BaaS solutions catering to the specific needs of the gig economy and freelance workforce, offering tailored payment and benefits, is another promising avenue.

Leading Players in the Banking as a Service Industry in UK Market

- Thought Machine

- Starling Bank

- Bankable

- 11:FS Foundry

- ClearBank

- Solarisbank

- Treezor

- Unnax

- Cambr

Key Developments in Banking as a Service Industry in UK Industry

- April 2022: PEXA, the Australian-founded fintech, developed a new payment scheme, PEXA Pay. In parallel, PEXA partnered with ClearBank, a UK-based clearing and embedded banking platform, to expand access to its upcoming remortgage platform, signaling increased collaboration in embedded payments.

- July 2021: Paysafe (NYSE: PSFE) announced a new partnership with Bankable, a global architect of 'banking-as-a-service' solutions. This global agreement will see the two companies collaborate to launch a broad range of integrated, omnichannel banking services from Paysafe, underscoring the growing trend of partnerships to expand service offerings.

Future Outlook for Banking as a Service Industry in UK Market

The future outlook for the UK Banking as a Service (BaaS) market is exceptionally bright, poised for sustained and accelerated growth. The continued maturation of API technology and the increasing adoption of cloud-native architectures will further democratize access to financial services, enabling a wider array of businesses to embed banking functionalities. Strategic opportunities lie in the deepening integration of BaaS into everyday digital experiences, moving beyond simple payment gateways to encompass holistic financial management tools. The rise of vertical-specific BaaS solutions, tailored to the unique needs of industries like healthcare, supply chain finance, and sustainability initiatives, will unlock significant market potential. Furthermore, the UK's proactive regulatory stance on financial innovation, coupled with ongoing investment in advanced technologies like AI for personalized financial services and enhanced security, will continue to position it as a global leader in the BaaS landscape. The anticipated market size is set to reach tens of billions of Pounds, driven by both expansion in existing segments and the emergence of entirely new BaaS applications.

Banking as a Service Industry in UK Segmentation

-

1. Component

- 1.1. Platform

-

1.2. Service

- 1.2.1. Professional Service

- 1.2.2. Managed Service

-

2. Product Type

- 2.1. API based BaaS

- 2.2. Cloud-based BaaS

-

3. Enterprise Size

- 3.1. Large enterprise

- 3.2. Small & Medium enterprise

-

4. End-User

- 4.1. Banks

- 4.2. NBFC/Fintech Corporations

- 4.3. Others

Banking as a Service Industry in UK Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Banking as a Service Industry in UK Regional Market Share

Geographic Coverage of Banking as a Service Industry in UK

Banking as a Service Industry in UK REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Platform

- 5.1.2. Service

- 5.1.2.1. Professional Service

- 5.1.2.2. Managed Service

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. API based BaaS

- 5.2.2. Cloud-based BaaS

- 5.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.3.1. Large enterprise

- 5.3.2. Small & Medium enterprise

- 5.4. Market Analysis, Insights and Forecast - by End-User

- 5.4.1. Banks

- 5.4.2. NBFC/Fintech Corporations

- 5.4.3. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Banking as a Service Industry in UK Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Platform

- 6.1.2. Service

- 6.1.2.1. Professional Service

- 6.1.2.2. Managed Service

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. API based BaaS

- 6.2.2. Cloud-based BaaS

- 6.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.3.1. Large enterprise

- 6.3.2. Small & Medium enterprise

- 6.4. Market Analysis, Insights and Forecast - by End-User

- 6.4.1. Banks

- 6.4.2. NBFC/Fintech Corporations

- 6.4.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Banking as a Service Industry in UK Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Platform

- 7.1.2. Service

- 7.1.2.1. Professional Service

- 7.1.2.2. Managed Service

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. API based BaaS

- 7.2.2. Cloud-based BaaS

- 7.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.3.1. Large enterprise

- 7.3.2. Small & Medium enterprise

- 7.4. Market Analysis, Insights and Forecast - by End-User

- 7.4.1. Banks

- 7.4.2. NBFC/Fintech Corporations

- 7.4.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. South America Banking as a Service Industry in UK Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Platform

- 8.1.2. Service

- 8.1.2.1. Professional Service

- 8.1.2.2. Managed Service

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. API based BaaS

- 8.2.2. Cloud-based BaaS

- 8.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.3.1. Large enterprise

- 8.3.2. Small & Medium enterprise

- 8.4. Market Analysis, Insights and Forecast - by End-User

- 8.4.1. Banks

- 8.4.2. NBFC/Fintech Corporations

- 8.4.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Europe Banking as a Service Industry in UK Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Platform

- 9.1.2. Service

- 9.1.2.1. Professional Service

- 9.1.2.2. Managed Service

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. API based BaaS

- 9.2.2. Cloud-based BaaS

- 9.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.3.1. Large enterprise

- 9.3.2. Small & Medium enterprise

- 9.4. Market Analysis, Insights and Forecast - by End-User

- 9.4.1. Banks

- 9.4.2. NBFC/Fintech Corporations

- 9.4.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Middle East & Africa Banking as a Service Industry in UK Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Platform

- 10.1.2. Service

- 10.1.2.1. Professional Service

- 10.1.2.2. Managed Service

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. API based BaaS

- 10.2.2. Cloud-based BaaS

- 10.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 10.3.1. Large enterprise

- 10.3.2. Small & Medium enterprise

- 10.4. Market Analysis, Insights and Forecast - by End-User

- 10.4.1. Banks

- 10.4.2. NBFC/Fintech Corporations

- 10.4.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Asia Pacific Banking as a Service Industry in UK Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Platform

- 11.1.2. Service

- 11.1.2.1. Professional Service

- 11.1.2.2. Managed Service

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. API based BaaS

- 11.2.2. Cloud-based BaaS

- 11.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 11.3.1. Large enterprise

- 11.3.2. Small & Medium enterprise

- 11.4. Market Analysis, Insights and Forecast - by End-User

- 11.4.1. Banks

- 11.4.2. NBFC/Fintech Corporations

- 11.4.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Thought Machine

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Starling Bank

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bankable

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 11

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Thought Machine

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Banking as a Service Industry in UK Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Banking as a Service Industry in UK Revenue (billion), by Component 2025 & 2033

- Figure 3: North America Banking as a Service Industry in UK Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Banking as a Service Industry in UK Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America Banking as a Service Industry in UK Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Banking as a Service Industry in UK Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 7: North America Banking as a Service Industry in UK Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 8: North America Banking as a Service Industry in UK Revenue (billion), by End-User 2025 & 2033

- Figure 9: North America Banking as a Service Industry in UK Revenue Share (%), by End-User 2025 & 2033

- Figure 10: North America Banking as a Service Industry in UK Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Banking as a Service Industry in UK Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Banking as a Service Industry in UK Revenue (billion), by Component 2025 & 2033

- Figure 13: South America Banking as a Service Industry in UK Revenue Share (%), by Component 2025 & 2033

- Figure 14: South America Banking as a Service Industry in UK Revenue (billion), by Product Type 2025 & 2033

- Figure 15: South America Banking as a Service Industry in UK Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: South America Banking as a Service Industry in UK Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 17: South America Banking as a Service Industry in UK Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 18: South America Banking as a Service Industry in UK Revenue (billion), by End-User 2025 & 2033

- Figure 19: South America Banking as a Service Industry in UK Revenue Share (%), by End-User 2025 & 2033

- Figure 20: South America Banking as a Service Industry in UK Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Banking as a Service Industry in UK Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Banking as a Service Industry in UK Revenue (billion), by Component 2025 & 2033

- Figure 23: Europe Banking as a Service Industry in UK Revenue Share (%), by Component 2025 & 2033

- Figure 24: Europe Banking as a Service Industry in UK Revenue (billion), by Product Type 2025 & 2033

- Figure 25: Europe Banking as a Service Industry in UK Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Europe Banking as a Service Industry in UK Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 27: Europe Banking as a Service Industry in UK Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 28: Europe Banking as a Service Industry in UK Revenue (billion), by End-User 2025 & 2033

- Figure 29: Europe Banking as a Service Industry in UK Revenue Share (%), by End-User 2025 & 2033

- Figure 30: Europe Banking as a Service Industry in UK Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Banking as a Service Industry in UK Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Banking as a Service Industry in UK Revenue (billion), by Component 2025 & 2033

- Figure 33: Middle East & Africa Banking as a Service Industry in UK Revenue Share (%), by Component 2025 & 2033

- Figure 34: Middle East & Africa Banking as a Service Industry in UK Revenue (billion), by Product Type 2025 & 2033

- Figure 35: Middle East & Africa Banking as a Service Industry in UK Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: Middle East & Africa Banking as a Service Industry in UK Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 37: Middle East & Africa Banking as a Service Industry in UK Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 38: Middle East & Africa Banking as a Service Industry in UK Revenue (billion), by End-User 2025 & 2033

- Figure 39: Middle East & Africa Banking as a Service Industry in UK Revenue Share (%), by End-User 2025 & 2033

- Figure 40: Middle East & Africa Banking as a Service Industry in UK Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Banking as a Service Industry in UK Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Banking as a Service Industry in UK Revenue (billion), by Component 2025 & 2033

- Figure 43: Asia Pacific Banking as a Service Industry in UK Revenue Share (%), by Component 2025 & 2033

- Figure 44: Asia Pacific Banking as a Service Industry in UK Revenue (billion), by Product Type 2025 & 2033

- Figure 45: Asia Pacific Banking as a Service Industry in UK Revenue Share (%), by Product Type 2025 & 2033

- Figure 46: Asia Pacific Banking as a Service Industry in UK Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 47: Asia Pacific Banking as a Service Industry in UK Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 48: Asia Pacific Banking as a Service Industry in UK Revenue (billion), by End-User 2025 & 2033

- Figure 49: Asia Pacific Banking as a Service Industry in UK Revenue Share (%), by End-User 2025 & 2033

- Figure 50: Asia Pacific Banking as a Service Industry in UK Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Banking as a Service Industry in UK Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 4: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 5: Global Banking as a Service Industry in UK Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 7: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 9: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 10: Global Banking as a Service Industry in UK Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 15: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 16: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 17: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 18: Global Banking as a Service Industry in UK Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 23: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 24: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 25: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 26: Global Banking as a Service Industry in UK Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 37: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 38: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 39: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 40: Global Banking as a Service Industry in UK Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Banking as a Service Industry in UK Revenue billion Forecast, by Component 2020 & 2033

- Table 48: Global Banking as a Service Industry in UK Revenue billion Forecast, by Product Type 2020 & 2033

- Table 49: Global Banking as a Service Industry in UK Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 50: Global Banking as a Service Industry in UK Revenue billion Forecast, by End-User 2020 & 2033

- Table 51: Global Banking as a Service Industry in UK Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Banking as a Service Industry in UK Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Banking as a Service Industry in UK?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Banking as a Service Industry in UK?

Key companies in the market include Thought Machine, Starling Bank, Bankable, 11:FS Foundry, ClearBank, Solarisbank, Treezor, Unnax, Cambr**List Not Exhaustive.

3. What are the main segments of the Banking as a Service Industry in UK?

The market segments include Component, Product Type, Enterprise Size, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Demand for Embedded Finance is Driving Banking as a Service.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

On April 2022, PEXA, the Australian-founded fintech developed of a brand new payment scheme - PEXA Pay. At the same time, PEXA has partnered with ClearBank, clearing and embedded banking platform in the UK, to broaden access to its forthcoming remortgage platform.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Banking as a Service Industry in UK," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Banking as a Service Industry in UK report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Banking as a Service Industry in UK?

To stay informed about further developments, trends, and reports in the Banking as a Service Industry in UK, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence