Key Insights

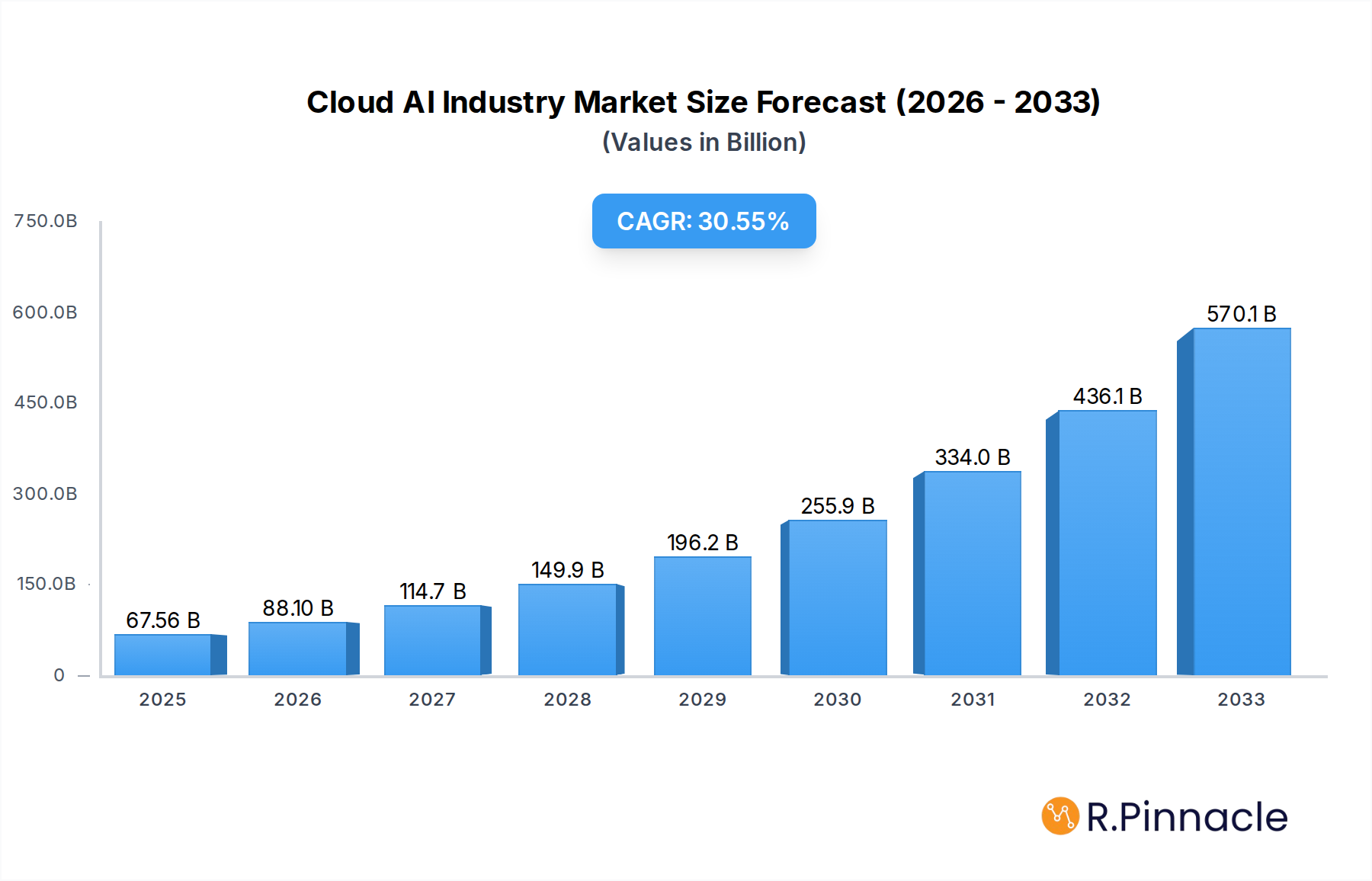

The global Cloud AI market is experiencing unprecedented growth, projected to reach an estimated $67.56 billion by 2025, driven by a remarkable 32.37% CAGR. This explosive expansion is fueled by the increasing adoption of AI-powered solutions and services across a diverse range of industries. Key drivers include the growing demand for enhanced data processing capabilities, the proliferation of big data, and the need for intelligent automation to improve operational efficiency and customer experiences. The integration of AI into cloud platforms allows businesses to leverage sophisticated machine learning, natural language processing, and computer vision technologies without the need for substantial on-premises infrastructure. This democratization of AI capabilities is a significant catalyst for market expansion. Furthermore, the escalating need for personalized customer interactions, predictive analytics for business intelligence, and advanced cybersecurity measures are pushing organizations to invest heavily in cloud AI. The market is segmented into solutions and services, with end-user verticals such as BFSI, Healthcare, Automotive, Retail, Government, and Education being primary adopters. These sectors are realizing the transformative potential of cloud AI in areas like fraud detection, personalized medicine, autonomous driving, supply chain optimization, and intelligent citizen services.

Cloud AI Industry Market Size (In Billion)

The competitive landscape is dominated by major technology players, including IBM Corporation, Google LLC, Microsoft Corporation, and Amazon Web Services Inc., alongside specialized AI firms like AIBrain LLC and SoundHound Inc. These companies are actively engaged in research and development, strategic partnerships, and mergers and acquisitions to expand their cloud AI offerings and capture market share. Emerging trends like the rise of edge AI, responsible AI development, and the increasing use of AI in hybrid and multi-cloud environments are further shaping the market trajectory. While the market presents immense opportunities, potential restraints such as data privacy concerns, the complexity of AI implementation, and the scarcity of skilled AI professionals could pose challenges. However, the sustained investment in AI research and the continuous evolution of cloud infrastructure are expected to mitigate these obstacles, paving the way for sustained and robust growth in the Cloud AI industry throughout the forecast period of 2025-2033.

Cloud AI Industry Company Market Share

Cloud AI Industry Market Report: Unveiling the Future of Intelligent Cloud Solutions

Gain unparalleled insights into the rapidly evolving Cloud AI industry with this comprehensive report. Spanning 2019–2033, with a deep dive into the 2025 base and estimated year, this analysis provides strategic intelligence for industry leaders, investors, and technology professionals navigating the complex landscape of artificial intelligence powered by cloud infrastructure. Discover market dynamics, innovation trends, dominant regions, and key players shaping the future of intelligent cloud services.

Cloud AI Industry Market Structure & Innovation Trends

The Cloud AI industry exhibits a dynamic market structure characterized by a blend of highly concentrated segments dominated by major tech giants and a growing number of innovative startups. Market concentration is evident in the core infrastructure and platform offerings, where companies like Google Cloud, Amazon Web Services Inc., and Microsoft Corporation command significant market share, estimated to be in the range of 70-75% for their AI-as-a-Service (AIaaS) solutions. Innovation is primarily driven by advancements in machine learning algorithms, natural language processing, computer vision, and the increasing demand for scalable and accessible AI solutions. Regulatory frameworks are gradually evolving, focusing on data privacy, ethical AI deployment, and algorithmic transparency. Product substitutes are emerging in the form of on-premise AI solutions for highly sensitive data, though the cost-effectiveness and scalability of cloud AI continue to drive adoption. End-user demographics are broadening beyond early adopters to include traditional enterprises across various verticals seeking to leverage AI for operational efficiency and competitive advantage. Mergers and acquisitions (M&A) are a significant feature, with estimated deal values reaching several billion dollars annually as larger players acquire specialized AI capabilities and smaller innovative firms seek strategic partnerships for growth. For instance, recent acquisitions by leading cloud providers of specialized AI startups targeting specific industry verticals underscore this trend, contributing to market consolidation and accelerated innovation.

Cloud AI Industry Market Dynamics & Trends

The Cloud AI industry is experiencing robust market growth, projected to exhibit a Compound Annual Growth Rate (CAGR) of approximately 30-35% over the forecast period of 2025–2033. This surge is propelled by several key market growth drivers. The exponential increase in data generation across all sectors necessitates sophisticated analytical tools, which AI-powered cloud services readily provide. Businesses are increasingly recognizing the transformative potential of AI in areas such as customer personalization, predictive maintenance, fraud detection, and automated customer support, leading to a higher adoption rate and consequently, increased market penetration. Technological disruptions are at the forefront, with continuous advancements in deep learning, generative AI, and edge AI expanding the scope of applications and performance capabilities. The integration of AI with existing cloud infrastructure is fostering hybrid and multi-cloud strategies, allowing organizations to optimize resource utilization and cost-efficiency. Consumer preferences are shifting towards hyper-personalized experiences and intelligent automation, compelling businesses to invest in Cloud AI solutions to meet these evolving demands. Competitive dynamics are fierce, characterized by intense innovation, strategic partnerships, and aggressive pricing strategies among market leaders and emerging players. The accessibility of powerful AI tools through cloud platforms has democratized AI development, fostering a vibrant ecosystem of solution providers and application developers. The trend towards responsible AI, emphasizing fairness, accountability, and transparency, is also gaining traction, influencing product development and market strategies.

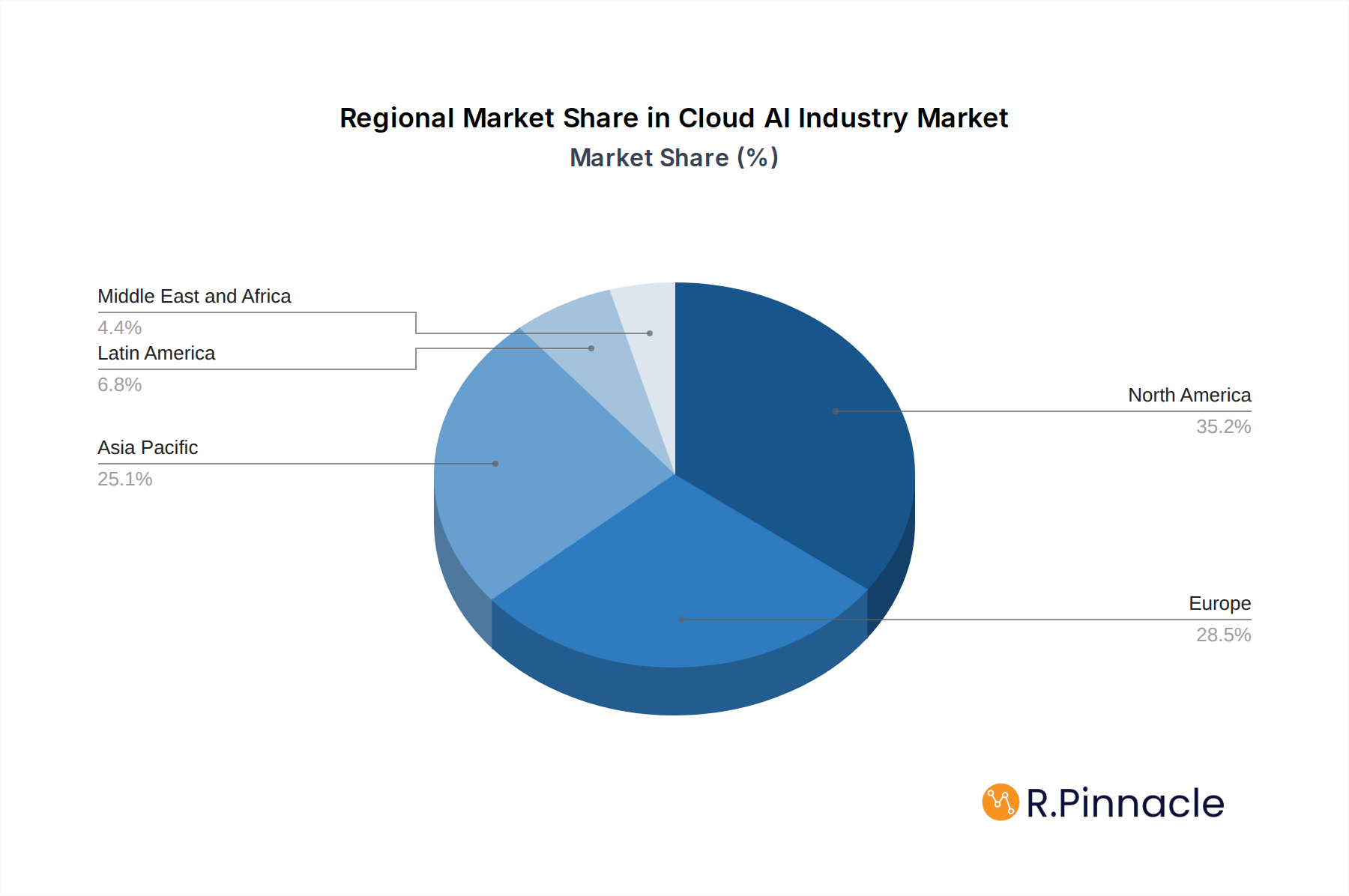

Dominant Regions & Segments in Cloud AI Industry

North America currently dominates the Cloud AI industry, driven by its mature technology infrastructure, significant venture capital funding, and a high concentration of leading technology companies. The United States, in particular, is a powerhouse, accounting for an estimated 45-50% of the global Cloud AI market share. Key drivers for this dominance include strong government support for AI research and development, a large pool of skilled AI talent, and early adoption of cloud technologies by enterprises.

- End-user Vertical Dominance:

- BFSI: This sector leads in Cloud AI adoption due to its critical need for fraud detection, risk management, personalized financial advice, and automated customer service. The sheer volume of sensitive data and the high stakes involved make AI solutions invaluable.

- Healthcare: The application of Cloud AI in healthcare is rapidly expanding, encompassing drug discovery, personalized medicine, diagnostic imaging analysis, and predictive patient care. The potential for improved patient outcomes and operational efficiency is a major catalyst.

- Retail: Cloud AI is revolutionizing the retail experience through personalized recommendations, inventory management, demand forecasting, and enhanced customer engagement. The ability to analyze vast amounts of customer data for tailored offerings is paramount.

- Automotive: The automotive sector is leveraging Cloud AI for autonomous driving technology, predictive maintenance, in-car infotainment systems, and manufacturing optimization. The drive towards smart and connected vehicles fuels significant investment.

- Government: Government agencies are increasingly adopting Cloud AI for smart city initiatives, public safety, cybersecurity, and optimizing public services, driven by the need for efficiency and better citizen engagement.

- Education: Cloud AI is being integrated for personalized learning platforms, automated grading, student performance analysis, and administrative task automation, aiming to enhance educational outcomes and accessibility.

The Asia-Pacific region is emerging as the fastest-growing market, fueled by increasing digital transformation initiatives, a burgeoning middle class, and significant investments in AI research and infrastructure by countries like China and India. Economic policies supporting technological innovation and the rapid development of cloud infrastructure are critical factors contributing to this growth.

Cloud AI Industry Product Innovations

Recent product innovations in the Cloud AI industry are characterized by the development of more sophisticated and accessible AI models, including advancements in generative AI for content creation and natural language understanding for enhanced human-computer interaction. Solution providers are focusing on democratizing AI by offering pre-trained models, low-code/no-code AI platforms, and specialized AI tools for specific industry applications. Competitive advantages are being gained through enhanced AI model accuracy, scalability, cost-effectiveness, and seamless integration with existing cloud services. The trend towards explainable AI (XAI) is also driving innovation, enabling users to understand how AI models arrive at their decisions, thereby fostering trust and broader adoption.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Cloud AI industry across various segments, providing detailed insights into market sizes, growth projections, and competitive dynamics.

Type:

- Solution: This segment encompasses AI platforms, pre-built AI models, and AI development tools delivered via the cloud. Projected to witness substantial growth due to increasing demand for specialized AI capabilities.

- Service: This segment includes AI consulting, implementation, and managed services provided by cloud vendors and third-party providers. Its growth is tied to the increasing complexity of AI deployments and the need for expert guidance.

End-user Vertical:

- BFSI: High growth is anticipated due to stringent security and regulatory needs, driving demand for AI in fraud detection and risk management.

- Healthcare: Significant expansion expected with AI revolutionizing diagnostics, personalized treatment, and drug discovery.

- Automotive: Robust growth is projected, fueled by advancements in autonomous driving and connected vehicle technologies.

- Retail: Continued strong growth driven by personalization, supply chain optimization, and e-commerce expansion.

- Government: Moderate to significant growth as public sector entities increasingly adopt AI for efficiency and citizen services.

- Education: Emerging segment with growing adoption for personalized learning and administrative automation.

- Other End-user Vertical: Encompasses diverse industries like manufacturing, energy, and media, collectively contributing to market expansion.

Key Drivers of Cloud AI Industry Growth

The Cloud AI industry's growth is propelled by a confluence of factors. Technologically, rapid advancements in machine learning algorithms, neural networks, and processing power enable more sophisticated AI applications. Economically, the increasing demand for operational efficiency, cost reduction, and enhanced customer experiences across all sectors is a primary driver. Businesses are recognizing AI as a critical tool for competitive differentiation. Regulatory factors, while sometimes presenting hurdles, also drive innovation in areas like data privacy and ethical AI, fostering a more responsible and trustworthy AI ecosystem. The widespread availability and scalability of cloud computing infrastructure make AI solutions accessible and cost-effective for a broader range of organizations, from large enterprises to small and medium-sized businesses.

Challenges in the Cloud AI Industry Sector

Despite its rapid growth, the Cloud AI industry faces several challenges. Regulatory hurdles related to data privacy, security, and algorithmic bias can slow down adoption and necessitate careful compliance strategies. Supply chain issues, particularly concerning specialized hardware like GPUs, can impact the availability and cost of AI processing power. Competitive pressures are intense, with established players and emerging startups constantly vying for market share, leading to pricing wars and the need for continuous innovation. The scarcity of skilled AI talent remains a significant barrier, limiting the pace of development and deployment. Additionally, the complexity of integrating AI solutions into existing legacy systems can be a deterrent for some organizations. Quantifiable impacts include increased development costs and longer deployment cycles due to these challenges.

Emerging Opportunities in Cloud AI Industry

Emerging opportunities in the Cloud AI industry are abundant, driven by new technological frontiers and evolving consumer preferences. The rise of generative AI presents significant opportunities for content creation, personalized marketing, and product design. Edge AI, bringing AI processing closer to data sources, unlocks new possibilities in real-time analytics for IoT devices and autonomous systems. The growing emphasis on sustainability is creating demand for AI-powered solutions in areas like energy management, resource optimization, and climate modeling. Furthermore, the expansion of AI into new markets and industries, such as agriculture, logistics, and entertainment, offers vast untapped potential. Consumer demand for hyper-personalized experiences and predictive services continues to grow, encouraging businesses to invest in intelligent cloud solutions.

Leading Players in the Cloud AI Industry Market

- AIBrain LLC

- Infosys Limited

- Wipro Limited

- SoundHound Inc

- IBM Corporation

- Google LLC

- Salesforce com Inc

- Microsoft Corporation

- Twilio Inc

- Amazon Web Services Inc

- Visenze Pte Ltd

- Cloudminds Technology

Key Developments in Cloud AI Industry Industry

- November 2022: ToGL Technology Sdn Bhd and Huawei Technologies (Malaysia) Sdn Bhd formalized their collaboration to create cloud-based digital solutions in Malaysia. This cooperation includes modern cloud and artificial intelligence (AI) services and experiences, aiming to bolster digital transformation in the region.

- November 2022: mCloud Technologies Corp., a provider of AI-powered asset management and Environmental, Social, and Governance (ESG) solutions, announced a strategic partnership with Google Cloud. This collaboration will integrate mCloud's AssetCare platform with Google Cloud's capabilities and services, including Google Earth Engine, to launch three AI-powered sustainability applications.

Future Outlook for Cloud AI Industry Market

The future outlook for the Cloud AI industry is exceptionally strong, with growth accelerators including the continued democratization of AI through accessible platforms and tools, further advancements in AI model capabilities, and the increasing adoption of AI across a wider spectrum of industries. The ongoing integration of AI with emerging technologies like the Internet of Things (IoT), 5G, and blockchain will unlock novel applications and drive significant market expansion. Strategic opportunities lie in developing specialized AI solutions for niche markets, focusing on ethical and responsible AI development, and leveraging hybrid and multi-cloud strategies to cater to diverse organizational needs. The market is poised for sustained innovation and growth, making Cloud AI a critical component of future digital economies.

Cloud AI Industry Segmentation

-

1. Type

- 1.1. Solution

- 1.2. Service

-

2. End-user Vertical

- 2.1. BFSI

- 2.2. Healthcare

- 2.3. Automotive

- 2.4. Retail

- 2.5. Government

- 2.6. Education

- 2.7. Other End-user Vertical

Cloud AI Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Cloud AI Industry Regional Market Share

Geographic Coverage of Cloud AI Industry

Cloud AI Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 32.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solution

- 5.1.2. Service

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. BFSI

- 5.2.2. Healthcare

- 5.2.3. Automotive

- 5.2.4. Retail

- 5.2.5. Government

- 5.2.6. Education

- 5.2.7. Other End-user Vertical

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Cloud AI Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solution

- 6.1.2. Service

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. BFSI

- 6.2.2. Healthcare

- 6.2.3. Automotive

- 6.2.4. Retail

- 6.2.5. Government

- 6.2.6. Education

- 6.2.7. Other End-user Vertical

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Cloud AI Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Solution

- 7.1.2. Service

- 7.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.2.1. BFSI

- 7.2.2. Healthcare

- 7.2.3. Automotive

- 7.2.4. Retail

- 7.2.5. Government

- 7.2.6. Education

- 7.2.7. Other End-user Vertical

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Cloud AI Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Solution

- 8.1.2. Service

- 8.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.2.1. BFSI

- 8.2.2. Healthcare

- 8.2.3. Automotive

- 8.2.4. Retail

- 8.2.5. Government

- 8.2.6. Education

- 8.2.7. Other End-user Vertical

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Cloud AI Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Solution

- 9.1.2. Service

- 9.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.2.1. BFSI

- 9.2.2. Healthcare

- 9.2.3. Automotive

- 9.2.4. Retail

- 9.2.5. Government

- 9.2.6. Education

- 9.2.7. Other End-user Vertical

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Cloud AI Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Solution

- 10.1.2. Service

- 10.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.2.1. BFSI

- 10.2.2. Healthcare

- 10.2.3. Automotive

- 10.2.4. Retail

- 10.2.5. Government

- 10.2.6. Education

- 10.2.7. Other End-user Vertical

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Cloud AI Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Solution

- 11.1.2. Service

- 11.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.2.1. BFSI

- 11.2.2. Healthcare

- 11.2.3. Automotive

- 11.2.4. Retail

- 11.2.5. Government

- 11.2.6. Education

- 11.2.7. Other End-user Vertical

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AIBrain LLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Infosys Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Wipro Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SoundHound Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IBM Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Google LLC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Salesforce com Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Microsoft Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Twilio Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Amazon Web Services Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Visenze Pte Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Cloudminds Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 AIBrain LLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cloud AI Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Cloud AI Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Cloud AI Industry Revenue (Million), by Type 2025 & 2033

- Figure 4: North America Cloud AI Industry Volume (K Unit), by Type 2025 & 2033

- Figure 5: North America Cloud AI Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Cloud AI Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Cloud AI Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 8: North America Cloud AI Industry Volume (K Unit), by End-user Vertical 2025 & 2033

- Figure 9: North America Cloud AI Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 10: North America Cloud AI Industry Volume Share (%), by End-user Vertical 2025 & 2033

- Figure 11: North America Cloud AI Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Cloud AI Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Cloud AI Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Cloud AI Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Cloud AI Industry Revenue (Million), by Type 2025 & 2033

- Figure 16: Europe Cloud AI Industry Volume (K Unit), by Type 2025 & 2033

- Figure 17: Europe Cloud AI Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Cloud AI Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Europe Cloud AI Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 20: Europe Cloud AI Industry Volume (K Unit), by End-user Vertical 2025 & 2033

- Figure 21: Europe Cloud AI Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 22: Europe Cloud AI Industry Volume Share (%), by End-user Vertical 2025 & 2033

- Figure 23: Europe Cloud AI Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Cloud AI Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Cloud AI Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Cloud AI Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Cloud AI Industry Revenue (Million), by Type 2025 & 2033

- Figure 28: Asia Pacific Cloud AI Industry Volume (K Unit), by Type 2025 & 2033

- Figure 29: Asia Pacific Cloud AI Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Cloud AI Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Asia Pacific Cloud AI Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 32: Asia Pacific Cloud AI Industry Volume (K Unit), by End-user Vertical 2025 & 2033

- Figure 33: Asia Pacific Cloud AI Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 34: Asia Pacific Cloud AI Industry Volume Share (%), by End-user Vertical 2025 & 2033

- Figure 35: Asia Pacific Cloud AI Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Cloud AI Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Cloud AI Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Cloud AI Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Latin America Cloud AI Industry Revenue (Million), by Type 2025 & 2033

- Figure 40: Latin America Cloud AI Industry Volume (K Unit), by Type 2025 & 2033

- Figure 41: Latin America Cloud AI Industry Revenue Share (%), by Type 2025 & 2033

- Figure 42: Latin America Cloud AI Industry Volume Share (%), by Type 2025 & 2033

- Figure 43: Latin America Cloud AI Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 44: Latin America Cloud AI Industry Volume (K Unit), by End-user Vertical 2025 & 2033

- Figure 45: Latin America Cloud AI Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 46: Latin America Cloud AI Industry Volume Share (%), by End-user Vertical 2025 & 2033

- Figure 47: Latin America Cloud AI Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Latin America Cloud AI Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Latin America Cloud AI Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Latin America Cloud AI Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Cloud AI Industry Revenue (Million), by Type 2025 & 2033

- Figure 52: Middle East and Africa Cloud AI Industry Volume (K Unit), by Type 2025 & 2033

- Figure 53: Middle East and Africa Cloud AI Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Middle East and Africa Cloud AI Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Middle East and Africa Cloud AI Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 56: Middle East and Africa Cloud AI Industry Volume (K Unit), by End-user Vertical 2025 & 2033

- Figure 57: Middle East and Africa Cloud AI Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 58: Middle East and Africa Cloud AI Industry Volume Share (%), by End-user Vertical 2025 & 2033

- Figure 59: Middle East and Africa Cloud AI Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Cloud AI Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Middle East and Africa Cloud AI Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Cloud AI Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 5: Global Cloud AI Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Cloud AI Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 10: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 11: Global Cloud AI Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Cloud AI Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 15: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 16: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 17: Global Cloud AI Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Cloud AI Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 21: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 22: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 23: Global Cloud AI Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Cloud AI Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 26: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 27: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 28: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 29: Global Cloud AI Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Cloud AI Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Cloud AI Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 32: Global Cloud AI Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 33: Global Cloud AI Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 34: Global Cloud AI Industry Volume K Unit Forecast, by End-user Vertical 2020 & 2033

- Table 35: Global Cloud AI Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Cloud AI Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud AI Industry?

The projected CAGR is approximately 32.37%.

2. Which companies are prominent players in the Cloud AI Industry?

Key companies in the market include AIBrain LLC, Infosys Limited, Wipro Limited, SoundHound Inc, IBM Corporation, Google LLC, Salesforce com Inc, Microsoft Corporation, Twilio Inc, Amazon Web Services Inc, Visenze Pte Ltd, Cloudminds Technology.

3. What are the main segments of the Cloud AI Industry?

The market segments include Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.56 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Big Data Volume; Increasing Demand for Virtual Assistants; Growing Adoption of Cloud-based Service and Application.

6. What are the notable trends driving market growth?

Growing Adoption of Cloud-based Service and Application.

7. Are there any restraints impacting market growth?

Loss of Control on Security in Case of Attack.

8. Can you provide examples of recent developments in the market?

November 2022 - ToGL Technology Sdn Bhd and Huawei Technologies (Malaysia) Sdn Bhd have formalized their collaboration to create cloud-based digital solutions in Malaysia. Modern cloud and artificial intelligence (AI) services and experiences are a part of the cooperation,

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud AI Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud AI Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud AI Industry?

To stay informed about further developments, trends, and reports in the Cloud AI Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence