Key Insights

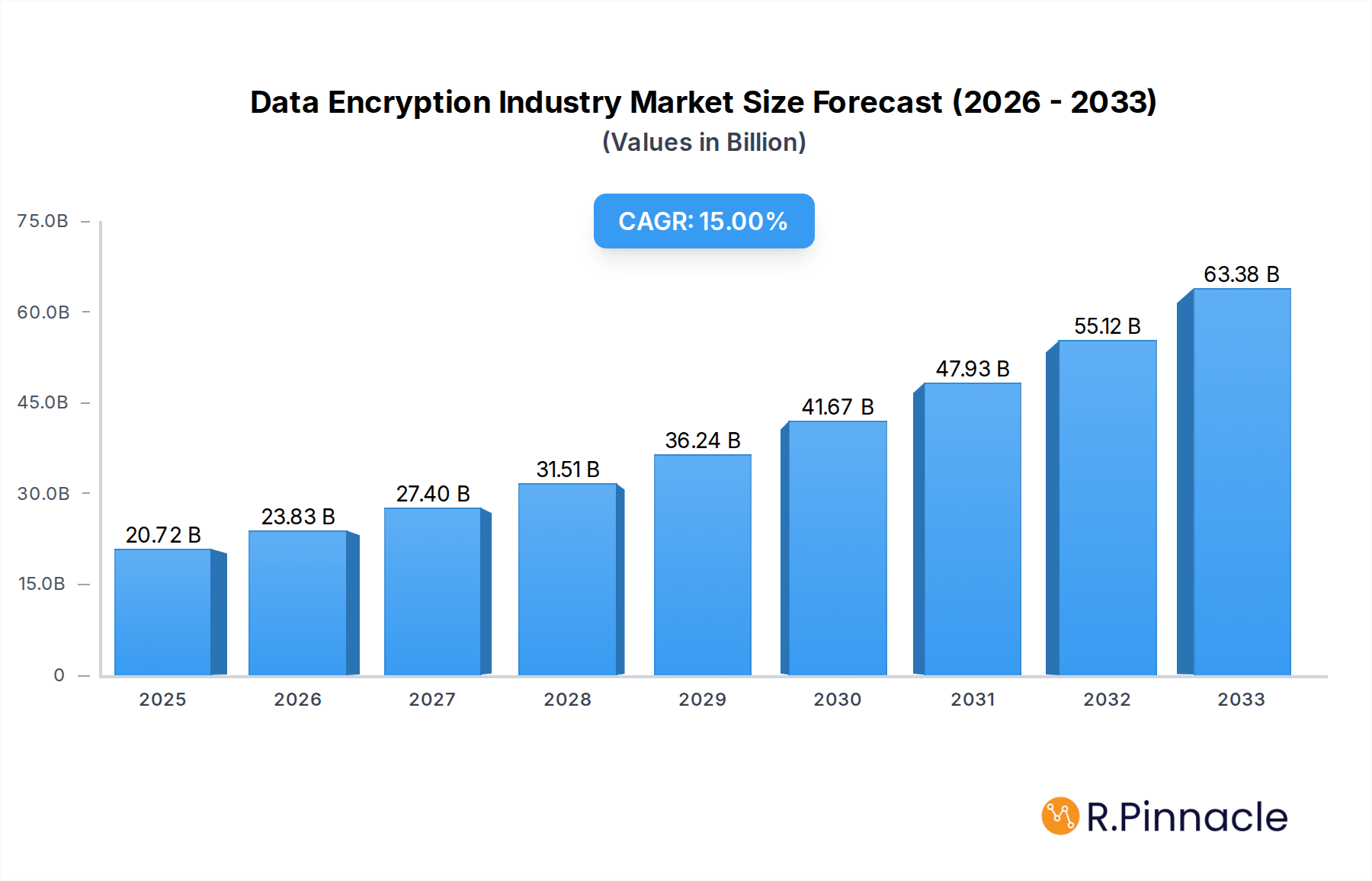

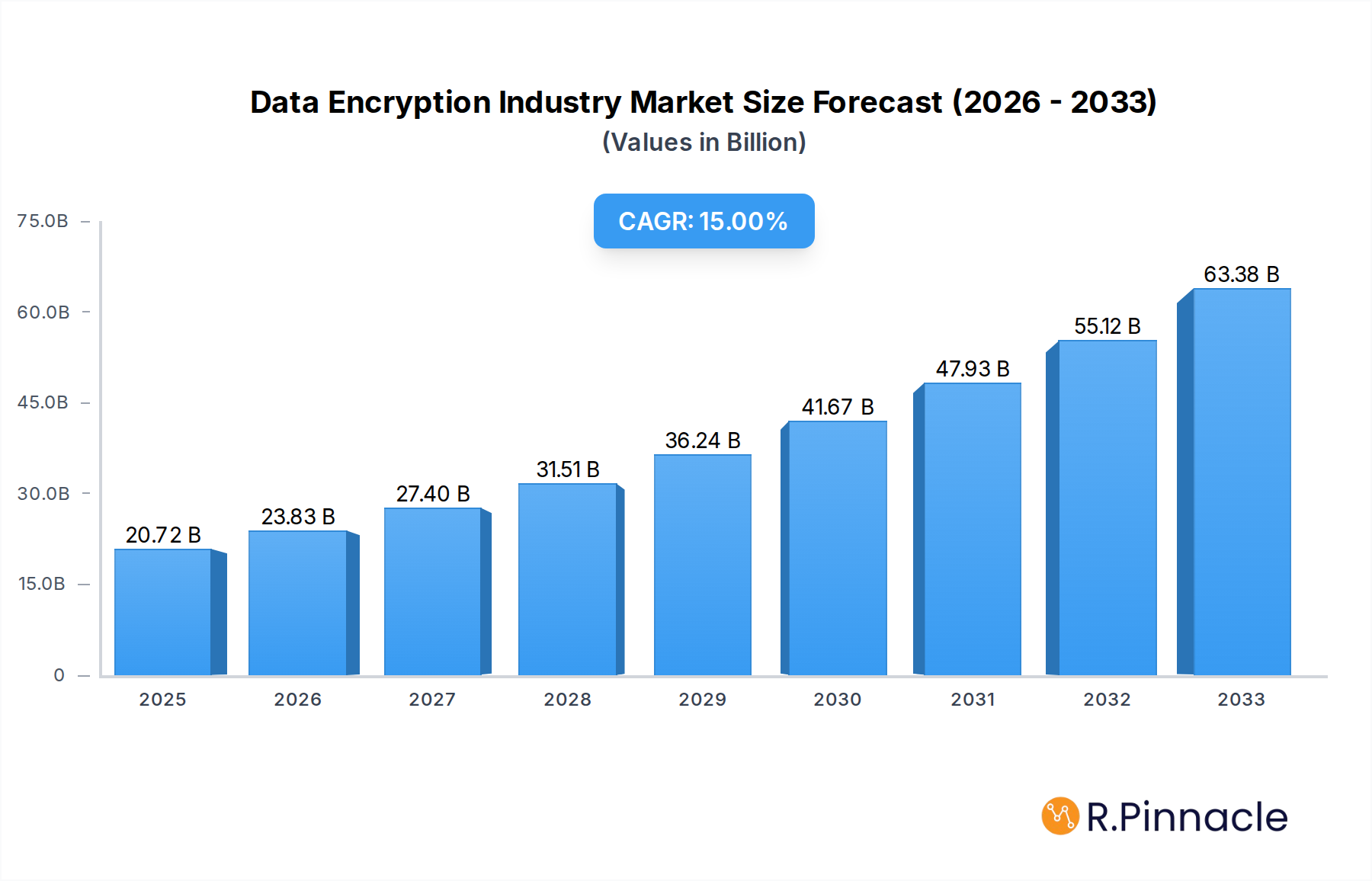

The global Data Encryption market is poised for robust expansion, projected to reach USD 20.72 billion in 2025. This significant market valuation is driven by an escalating need for data security across all sectors, fueled by the increasing volume of sensitive information being generated and stored. The market is anticipated to grow at a compound annual growth rate (CAGR) of 15% from 2025 to 2033, underscoring a strong and sustained upward trajectory. Key growth drivers include the pervasive rise in cyber threats, stringent data privacy regulations like GDPR and CCPA, and the widespread adoption of cloud computing and remote work models, all of which necessitate advanced encryption solutions. The demand is further propelled by enterprises prioritizing the protection of intellectual property, customer data, and financial transactions against sophisticated cyberattacks.

Data Encryption Industry Market Size (In Billion)

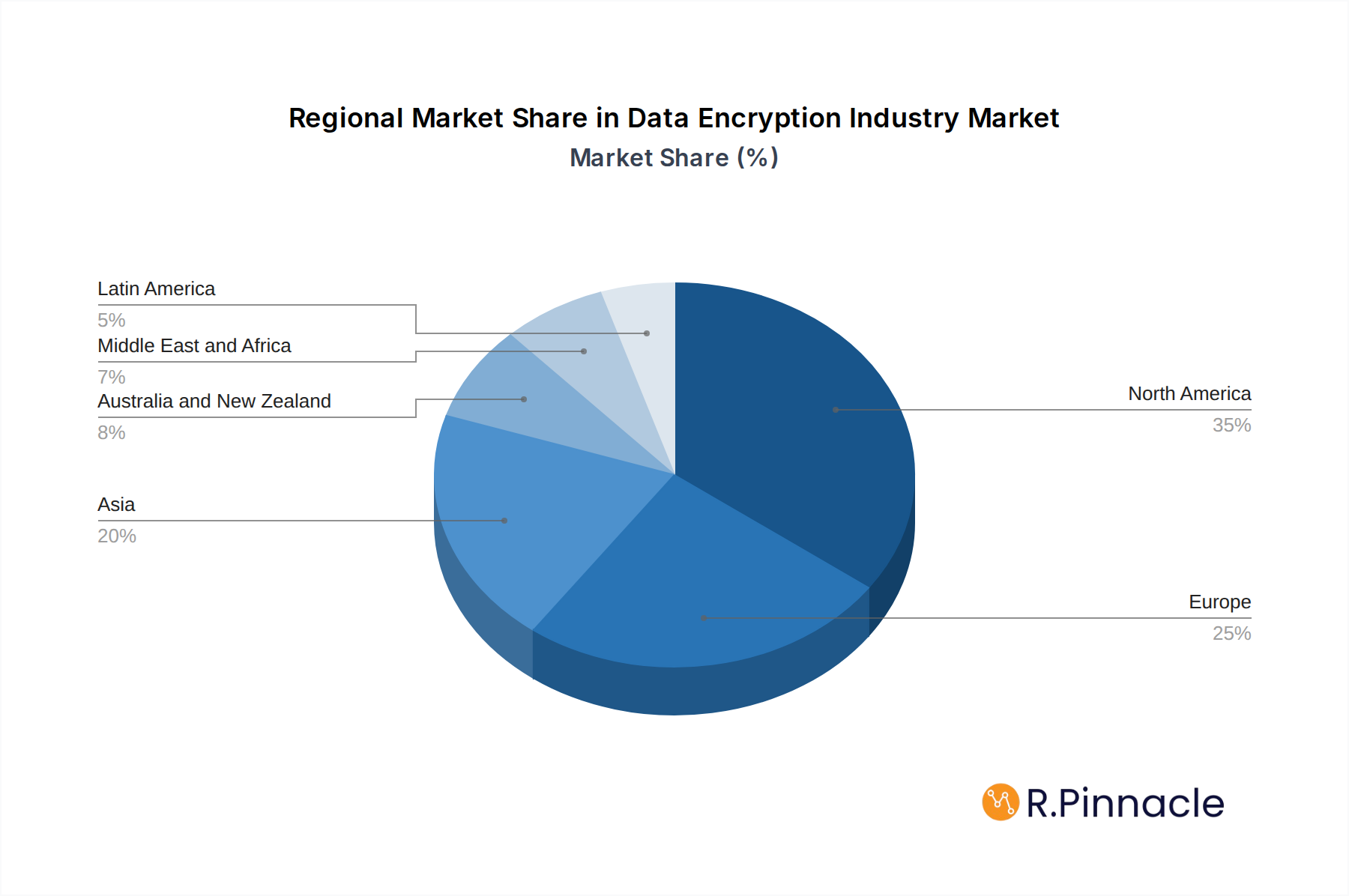

The market's segmentation reveals a diverse landscape catering to varied needs. In terms of components, software solutions are expected to lead, owing to their flexibility and scalability, closely followed by services that ensure proper implementation and ongoing management. The deployment model is tilting towards cloud-based encryption, reflecting the broader shift to cloud infrastructure, although on-premise solutions will remain crucial for highly regulated industries. Large enterprises are currently the dominant segment, but the rapid digital transformation among Small and Medium Enterprises (SMEs) indicates a substantial growth opportunity in this area. Functionally, Disk Encryption, Communication Encryption, and File/Folder Encryption are fundamental, while Cloud Encryption and Database Encryption are experiencing rapid adoption due to cloud migration. The IT & Telecommunication, BFSI, and Healthcare sectors are leading the charge in encryption adoption, followed by significant growth potential in Government, Retail, and Education. North America currently holds a dominant market share, attributed to its advanced technological infrastructure and proactive regulatory environment, with Asia projected to witness the fastest growth due to its burgeoning digital economy and increasing cybersecurity awareness.

Data Encryption Industry Company Market Share

Data Encryption Industry: Comprehensive Market Analysis & Future Outlook 2025-2033

This in-depth report provides a critical analysis of the global Data Encryption Industry, offering actionable insights for stakeholders navigating this rapidly evolving landscape. With a study period spanning from 2019 to 2033, and a base year of 2025, this comprehensive report leverages high-ranking keywords such as "data encryption solutions," "cybersecurity," "cloud encryption," and "enterprise data protection" to enhance search visibility. It delves into market structure, dynamics, key players, product innovations, and future trends, empowering industry professionals with the knowledge to make informed strategic decisions. The report forecasts a substantial market expansion driven by increasing data volumes, stringent regulations, and the pervasive threat of cyberattacks.

Data Encryption Industry Market Structure & Innovation Trends

The Data Encryption Industry exhibits a moderately concentrated market structure, characterized by a blend of established global technology giants and specialized cybersecurity firms. Innovation is a primary driver, fueled by the escalating sophistication of cyber threats and the increasing demand for robust data protection across diverse industries. Regulatory frameworks, such as GDPR and CCPA, are significantly shaping market dynamics, mandating stronger encryption protocols and driving adoption. Product substitutes, while present in broader security solutions, are largely outmatched by dedicated encryption technologies for core data security needs. End-user demographics range from large enterprises prioritizing comprehensive security solutions to small and medium enterprises seeking scalable and cost-effective encryption tools. Mergers and acquisitions (M&A) activity is a notable trend, with deal values in the billions of dollars, as larger players seek to acquire innovative technologies and expand their market reach. The market share distribution reflects the dominance of companies like Microsoft and IBM, with a significant portion also held by specialized providers.

Data Encryption Industry Market Dynamics & Trends

The Data Encryption Industry is experiencing robust growth, projected to reach hundreds of billions of dollars in market value. The Compound Annual Growth Rate (CAGR) is expected to remain in the double digits throughout the forecast period, driven by several key factors. The exponential increase in data generation across all sectors, coupled with the pervasive adoption of cloud computing and remote work, necessitates advanced data encryption solutions to protect sensitive information from unauthorized access and breaches. Technological disruptions, including advancements in quantum-resistant cryptography and AI-driven encryption management, are continuously shaping the market's trajectory, offering enhanced security and efficiency. Consumer preferences are increasingly leaning towards solutions that offer seamless integration, user-friendly interfaces, and verifiable security assurances. The competitive dynamics are intense, with ongoing innovation in product offerings, pricing strategies, and go-to-market approaches. Market penetration is significant, with a growing awareness of encryption's importance across all enterprise sizes and industry verticals. The shift towards cloud-native encryption services and managed encryption solutions is a pronounced trend, catering to the evolving IT infrastructure of businesses. The demand for end-to-end encryption, ensuring data protection from creation to archival, is also on the rise, further propelling market expansion.

Dominant Regions & Segments in Data Encryption Industry

North America currently dominates the Data Encryption Industry, driven by its strong technological infrastructure, high cybersecurity spending, and the presence of major technology corporations. The United States, in particular, leads in market penetration and innovation, with significant investments in advanced encryption solutions by both government and private sectors.

Component:

- Software: This segment is expected to hold a substantial market share due to the increasing demand for encryption software integrated into operating systems, applications, and cloud platforms. Key drivers include the need for policy-based encryption and granular access controls.

- Service: The growth of encryption-as-a-service (EaaS) and managed encryption services is fueling the expansion of this segment. Businesses are increasingly outsourcing their encryption management to specialized providers to reduce operational overhead and leverage expert knowledge.

Deployment Model:

- Cloud: The rapid adoption of cloud computing by enterprises of all sizes makes this a leading deployment model. Cloud encryption solutions offer scalability, flexibility, and cost-effectiveness, essential for modern business operations. Major drivers include multi-cloud strategies and the need for consistent security policies across hybrid environments.

- On-premise: While cloud adoption is surging, on-premise encryption remains crucial for highly regulated industries and organizations with specific data sovereignty requirements.

Enterprise Size:

- Large Enterprises: These organizations are the primary consumers of advanced data encryption solutions due to their extensive data volumes, complex IT infrastructures, and higher exposure to sophisticated cyber threats. They invest heavily in comprehensive encryption strategies, including disk encryption, communication encryption, and database encryption.

- Small & Medium Enterprises (SMEs): As awareness of data security grows, SMEs are increasingly adopting encryption solutions. The availability of more affordable and user-friendly options is driving their market penetration.

Function:

- Cloud Encryption: This sub-segment is experiencing the fastest growth, driven by the widespread adoption of cloud services. The need to secure data stored and processed in public, private, and hybrid cloud environments is paramount.

- Disk Encryption: Remains a fundamental encryption function, essential for protecting data at rest on endpoints and servers.

- Communication Encryption: Critical for securing data in transit, especially with the rise of remote work and distributed teams.

- Database Encryption: Vital for protecting sensitive information stored in databases, particularly in sectors like BFSI and Healthcare.

- File/Folder Encryption: Offers granular control over data protection at the file and folder level, catering to specific use cases.

Industry Vertical:

- IT & Telecommunication: This sector is a major adopter of encryption technologies due to the inherent need to protect vast amounts of sensitive customer and operational data.

- BFSI (Banking, Financial Services, and Insurance): Highly regulated, this vertical prioritizes robust data encryption to comply with stringent regulations and protect customer financial information.

- Healthcare: The sensitive nature of patient data makes encryption a critical component of healthcare IT infrastructure, driven by regulations like HIPAA.

- Government: National security and citizen data protection necessitate the widespread use of encryption across government agencies.

- Retail: Protecting customer payment information and personal data is crucial, driving encryption adoption in the retail sector.

- Education: Educational institutions are increasingly adopting encryption to safeguard student and staff data.

Data Encryption Industry Product Innovations

Product innovation in the Data Encryption Industry is characterized by the development of advanced key management solutions, quantum-resistant algorithms, and AI-powered threat detection for encryption systems. Companies are focusing on delivering seamless integration across hybrid and multi-cloud environments, with solutions like IBM's Unified Key Orchestrator exemplifying the trend towards simplified, centralized key management. The competitive advantage lies in offering robust, scalable, and user-friendly encryption that meets stringent compliance requirements while minimizing performance impact. Innovations are also geared towards enabling end-to-end encryption for greater data security assurance, meeting the market's growing demand for comprehensive data protection.

Report Scope & Segmentation Analysis

This report segments the Data Encryption Industry across several key dimensions: Component (Software, Service), Deployment Model (On-premise, Cloud), Enterprise Size (Large Enterprises, Small & Medium Enterprises), Function (Disk Encryption, Communication Encryption, File/Folder Encryption, Cloud Encryption, Database Encryption), and Industry Vertical (IT & Telecommunication, BFSI, Healthcare, Government, Retail, Education, Others). Each segment is analyzed for its market size, growth projections, and competitive dynamics during the forecast period of 2025–2033. For example, the Cloud Encryption segment is projected to exhibit a CAGR of xx%, driven by the increasing adoption of cloud services and the need for robust data protection in multi-cloud environments. Conversely, while On-premise deployment may see slower growth, it will remain critical for specific highly regulated sectors.

Key Drivers of Data Encryption Industry Growth

The Data Encryption Industry's growth is propelled by a confluence of powerful drivers. The escalating volume and value of data generated globally necessitate robust protection mechanisms. Increasing cybersecurity threats, ranging from ransomware to sophisticated state-sponsored attacks, are compelling organizations to invest in advanced encryption technologies. Stringent regulatory compliance mandates, such as GDPR and CCPA, requiring data privacy and protection, are significant accelerators. The widespread adoption of cloud computing and remote work models expands the attack surface, thereby increasing the demand for comprehensive encryption solutions. Furthermore, advancements in encryption algorithms and key management systems are making these solutions more accessible and effective for businesses of all sizes.

Challenges in the Data Encryption Industry Sector

Despite robust growth, the Data Encryption Industry faces several challenges. The complexity of implementing and managing encryption solutions can be a barrier, particularly for smaller organizations with limited IT resources. The ever-evolving threat landscape requires continuous updates and adaptations to encryption protocols, demanding significant R&D investment. Ensuring interoperability between different encryption systems and managing diverse encryption keys across hybrid cloud environments presents significant technical hurdles. Moreover, the cost of implementing and maintaining advanced encryption solutions can be substantial, posing a challenge for budget-constrained businesses. Regulatory fragmentation across different regions can also create compliance complexities.

Emerging Opportunities in Data Encryption Industry

The Data Encryption Industry is ripe with emerging opportunities. The rise of edge computing and the Internet of Things (IoT) presents a vast new frontier for data encryption, securing data generated at the edge. The growing demand for privacy-preserving technologies, such as homomorphic encryption and differential privacy, opens up new avenues for innovation. The increasing focus on sovereign cloud solutions and data localization requirements in various countries creates opportunities for specialized encryption services. Furthermore, the development of AI-powered encryption management platforms and quantum-resistant encryption solutions are poised to redefine data security in the coming years, offering enhanced protection against future threats.

Leading Players in the Data Encryption Industry Market

- Microsoft

- McAfee LLC

- Check Point Software Technologies Ltd

- Thales

- Broadcom Inc

- Trend Micro Incorporated

- Dell Inc

- Sophos Ltd

- Micro Focus International plc

- IBM

Key Developments in Data Encryption Industry Industry

- March 2022: IBM launched Unified Key Orchestrator, a multi-cloud key management solution available as a managed service through IBM Cloud Hyper Protect Crypto Services. This solution, based on the "Keep Your Own Key" concept, aids businesses in managing data encryption keys across multiple key stores and cloud environments, including IBM Cloud, AWS, and Microsoft Azure.

- February 2022: Sophos announced plans for new data centers in Mumbai, India, and Sao Paulo, Brazil, to commence operations in March and May respectively. These facilities aim to assist businesses in these regions in complying with increasingly important data sovereignty rules and regulations, particularly for firms in the banking, government, and other highly regulated sectors. Sophos Encryption services will leverage these new data centers, with plans to gradually extend availability to other Sophos portfolio products.

Future Outlook for Data Encryption Industry Market

The future outlook for the Data Encryption Industry is exceptionally bright, with continued strong growth anticipated throughout the forecast period. The persistent rise in cyber threats, coupled with evolving regulatory landscapes and the increasing adoption of cloud and hybrid environments, will fuel demand for sophisticated encryption solutions. Innovations in areas like quantum-resistant cryptography and AI-driven security will further enhance protection capabilities. The expansion into emerging areas like edge computing and IoT security presents significant untapped potential. Strategic opportunities lie in developing integrated, user-friendly, and scalable encryption solutions that cater to the diverse needs of enterprises, ensuring data confidentiality and integrity in an increasingly digital world.

Data Encryption Industry Segmentation

-

1. Component

- 1.1. Software

- 1.2. Service

-

2. Deployment Model

- 2.1. On-premise

- 2.2. Cloud

-

3. Enterprise Size

- 3.1. Large Enterprises

- 3.2. Small & Medium Enterprises

-

4. Function

- 4.1. Disk Encryption

- 4.2. Communication Encryption

- 4.3. File/Folder Encryption

- 4.4. Cloud Encryption

- 4.5. Database Encryption

-

5. Industry Vertical

- 5.1. IT & Telecommunication

- 5.2. BFSI

- 5.3. Healthcare

- 5.4. Government

- 5.5. Retail

- 5.6. Education

- 5.7. Others

Data Encryption Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Middle East and Africa

- 6. Latin America

Data Encryption Industry Regional Market Share

Geographic Coverage of Data Encryption Industry

Data Encryption Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Software

- 5.1.2. Service

- 5.2. Market Analysis, Insights and Forecast - by Deployment Model

- 5.2.1. On-premise

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.3.1. Large Enterprises

- 5.3.2. Small & Medium Enterprises

- 5.4. Market Analysis, Insights and Forecast - by Function

- 5.4.1. Disk Encryption

- 5.4.2. Communication Encryption

- 5.4.3. File/Folder Encryption

- 5.4.4. Cloud Encryption

- 5.4.5. Database Encryption

- 5.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.5.1. IT & Telecommunication

- 5.5.2. BFSI

- 5.5.3. Healthcare

- 5.5.4. Government

- 5.5.5. Retail

- 5.5.6. Education

- 5.5.7. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia

- 5.6.4. Australia and New Zealand

- 5.6.5. Middle East and Africa

- 5.6.6. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Data Encryption Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Software

- 6.1.2. Service

- 6.2. Market Analysis, Insights and Forecast - by Deployment Model

- 6.2.1. On-premise

- 6.2.2. Cloud

- 6.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.3.1. Large Enterprises

- 6.3.2. Small & Medium Enterprises

- 6.4. Market Analysis, Insights and Forecast - by Function

- 6.4.1. Disk Encryption

- 6.4.2. Communication Encryption

- 6.4.3. File/Folder Encryption

- 6.4.4. Cloud Encryption

- 6.4.5. Database Encryption

- 6.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.5.1. IT & Telecommunication

- 6.5.2. BFSI

- 6.5.3. Healthcare

- 6.5.4. Government

- 6.5.5. Retail

- 6.5.6. Education

- 6.5.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Software

- 7.1.2. Service

- 7.2. Market Analysis, Insights and Forecast - by Deployment Model

- 7.2.1. On-premise

- 7.2.2. Cloud

- 7.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.3.1. Large Enterprises

- 7.3.2. Small & Medium Enterprises

- 7.4. Market Analysis, Insights and Forecast - by Function

- 7.4.1. Disk Encryption

- 7.4.2. Communication Encryption

- 7.4.3. File/Folder Encryption

- 7.4.4. Cloud Encryption

- 7.4.5. Database Encryption

- 7.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 7.5.1. IT & Telecommunication

- 7.5.2. BFSI

- 7.5.3. Healthcare

- 7.5.4. Government

- 7.5.5. Retail

- 7.5.6. Education

- 7.5.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Europe Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Software

- 8.1.2. Service

- 8.2. Market Analysis, Insights and Forecast - by Deployment Model

- 8.2.1. On-premise

- 8.2.2. Cloud

- 8.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.3.1. Large Enterprises

- 8.3.2. Small & Medium Enterprises

- 8.4. Market Analysis, Insights and Forecast - by Function

- 8.4.1. Disk Encryption

- 8.4.2. Communication Encryption

- 8.4.3. File/Folder Encryption

- 8.4.4. Cloud Encryption

- 8.4.5. Database Encryption

- 8.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 8.5.1. IT & Telecommunication

- 8.5.2. BFSI

- 8.5.3. Healthcare

- 8.5.4. Government

- 8.5.5. Retail

- 8.5.6. Education

- 8.5.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Asia Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Software

- 9.1.2. Service

- 9.2. Market Analysis, Insights and Forecast - by Deployment Model

- 9.2.1. On-premise

- 9.2.2. Cloud

- 9.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.3.1. Large Enterprises

- 9.3.2. Small & Medium Enterprises

- 9.4. Market Analysis, Insights and Forecast - by Function

- 9.4.1. Disk Encryption

- 9.4.2. Communication Encryption

- 9.4.3. File/Folder Encryption

- 9.4.4. Cloud Encryption

- 9.4.5. Database Encryption

- 9.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 9.5.1. IT & Telecommunication

- 9.5.2. BFSI

- 9.5.3. Healthcare

- 9.5.4. Government

- 9.5.5. Retail

- 9.5.6. Education

- 9.5.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Australia and New Zealand Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Software

- 10.1.2. Service

- 10.2. Market Analysis, Insights and Forecast - by Deployment Model

- 10.2.1. On-premise

- 10.2.2. Cloud

- 10.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 10.3.1. Large Enterprises

- 10.3.2. Small & Medium Enterprises

- 10.4. Market Analysis, Insights and Forecast - by Function

- 10.4.1. Disk Encryption

- 10.4.2. Communication Encryption

- 10.4.3. File/Folder Encryption

- 10.4.4. Cloud Encryption

- 10.4.5. Database Encryption

- 10.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 10.5.1. IT & Telecommunication

- 10.5.2. BFSI

- 10.5.3. Healthcare

- 10.5.4. Government

- 10.5.5. Retail

- 10.5.6. Education

- 10.5.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Middle East and Africa Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Software

- 11.1.2. Service

- 11.2. Market Analysis, Insights and Forecast - by Deployment Model

- 11.2.1. On-premise

- 11.2.2. Cloud

- 11.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 11.3.1. Large Enterprises

- 11.3.2. Small & Medium Enterprises

- 11.4. Market Analysis, Insights and Forecast - by Function

- 11.4.1. Disk Encryption

- 11.4.2. Communication Encryption

- 11.4.3. File/Folder Encryption

- 11.4.4. Cloud Encryption

- 11.4.5. Database Encryption

- 11.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 11.5.1. IT & Telecommunication

- 11.5.2. BFSI

- 11.5.3. Healthcare

- 11.5.4. Government

- 11.5.5. Retail

- 11.5.6. Education

- 11.5.7. Others

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Latin America Data Encryption Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Component

- 12.1.1. Software

- 12.1.2. Service

- 12.2. Market Analysis, Insights and Forecast - by Deployment Model

- 12.2.1. On-premise

- 12.2.2. Cloud

- 12.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 12.3.1. Large Enterprises

- 12.3.2. Small & Medium Enterprises

- 12.4. Market Analysis, Insights and Forecast - by Function

- 12.4.1. Disk Encryption

- 12.4.2. Communication Encryption

- 12.4.3. File/Folder Encryption

- 12.4.4. Cloud Encryption

- 12.4.5. Database Encryption

- 12.5. Market Analysis, Insights and Forecast - by Industry Vertical

- 12.5.1. IT & Telecommunication

- 12.5.2. BFSI

- 12.5.3. Healthcare

- 12.5.4. Government

- 12.5.5. Retail

- 12.5.6. Education

- 12.5.7. Others

- 12.1. Market Analysis, Insights and Forecast - by Component

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Microsoft

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 McAfee LLC

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Check Point Software Technologies Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Thales

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Broadcom Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Trend Micro Incorporated

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Dell Inc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Sophos Ltd

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Micro Focus International plc*List Not Exhaustive

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 IBM

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Microsoft

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Data Encryption Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 3: North America Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 4: North America Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 5: North America Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 6: North America Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 7: North America Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 8: North America Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 9: North America Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 10: North America Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 11: North America Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 12: North America Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 15: Europe Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 16: Europe Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 17: Europe Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 18: Europe Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 19: Europe Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 20: Europe Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 21: Europe Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 22: Europe Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 23: Europe Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 24: Europe Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Europe Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 27: Asia Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 28: Asia Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 29: Asia Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 30: Asia Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 31: Asia Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 32: Asia Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 33: Asia Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 34: Asia Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 35: Asia Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 36: Asia Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 37: Asia Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Australia and New Zealand Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 39: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 40: Australia and New Zealand Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 41: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 42: Australia and New Zealand Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 43: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 44: Australia and New Zealand Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 45: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 46: Australia and New Zealand Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 47: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 48: Australia and New Zealand Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 49: Australia and New Zealand Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 51: Middle East and Africa Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 52: Middle East and Africa Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 53: Middle East and Africa Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 54: Middle East and Africa Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 55: Middle East and Africa Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 56: Middle East and Africa Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 57: Middle East and Africa Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 58: Middle East and Africa Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 59: Middle East and Africa Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 60: Middle East and Africa Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 61: Middle East and Africa Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Latin America Data Encryption Industry Revenue (billion), by Component 2025 & 2033

- Figure 63: Latin America Data Encryption Industry Revenue Share (%), by Component 2025 & 2033

- Figure 64: Latin America Data Encryption Industry Revenue (billion), by Deployment Model 2025 & 2033

- Figure 65: Latin America Data Encryption Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 66: Latin America Data Encryption Industry Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 67: Latin America Data Encryption Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 68: Latin America Data Encryption Industry Revenue (billion), by Function 2025 & 2033

- Figure 69: Latin America Data Encryption Industry Revenue Share (%), by Function 2025 & 2033

- Figure 70: Latin America Data Encryption Industry Revenue (billion), by Industry Vertical 2025 & 2033

- Figure 71: Latin America Data Encryption Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 72: Latin America Data Encryption Industry Revenue (billion), by Country 2025 & 2033

- Figure 73: Latin America Data Encryption Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 3: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 4: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 5: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 6: Global Data Encryption Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 8: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 9: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 10: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 11: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 12: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 14: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 15: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 16: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 17: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 18: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 20: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 21: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 22: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 23: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 24: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 26: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 27: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 28: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 29: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 30: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 32: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 33: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 34: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 35: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 36: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Global Data Encryption Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 38: Global Data Encryption Industry Revenue billion Forecast, by Deployment Model 2020 & 2033

- Table 39: Global Data Encryption Industry Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 40: Global Data Encryption Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 41: Global Data Encryption Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 42: Global Data Encryption Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Data Encryption Industry?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the Data Encryption Industry?

Key companies in the market include Microsoft, McAfee LLC, Check Point Software Technologies Ltd, Thales, Broadcom Inc, Trend Micro Incorporated, Dell Inc, Sophos Ltd, Micro Focus International plc*List Not Exhaustive, IBM.

3. What are the main segments of the Data Encryption Industry?

The market segments include Component, Deployment Model, Enterprise Size, Function, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.72 billion as of 2022.

5. What are some drivers contributing to market growth?

Regulatory Standards Related to Data Transfer and its Security; Growing Volume of Strength of Cyber Attacks and Mobile Theft.

6. What are the notable trends driving market growth?

IT & Telecommunication to Hold a Significant Share.

7. Are there any restraints impacting market growth?

Expensive Encryption Software Deployment and Maintenance costs; Utilization of Open-Source and Pirated Encryption Products.

8. Can you provide examples of recent developments in the market?

March 2022 - Unified Key Orchestrator, a multi-cloud key management solution made available as a managed service by IBM Cloud Hyper Protect Crypto Services, was officially launched. Unified Key Orchestrator, based on the "Keep Your Own Key" concept, assists businesses in managing their data encryption keys across numerous key stores and cloud environments, including keys handled locally on IBM Cloud, AWS, and Microsoft Azure.\

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Data Encryption Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Data Encryption Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Data Encryption Industry?

To stay informed about further developments, trends, and reports in the Data Encryption Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence