Key Insights

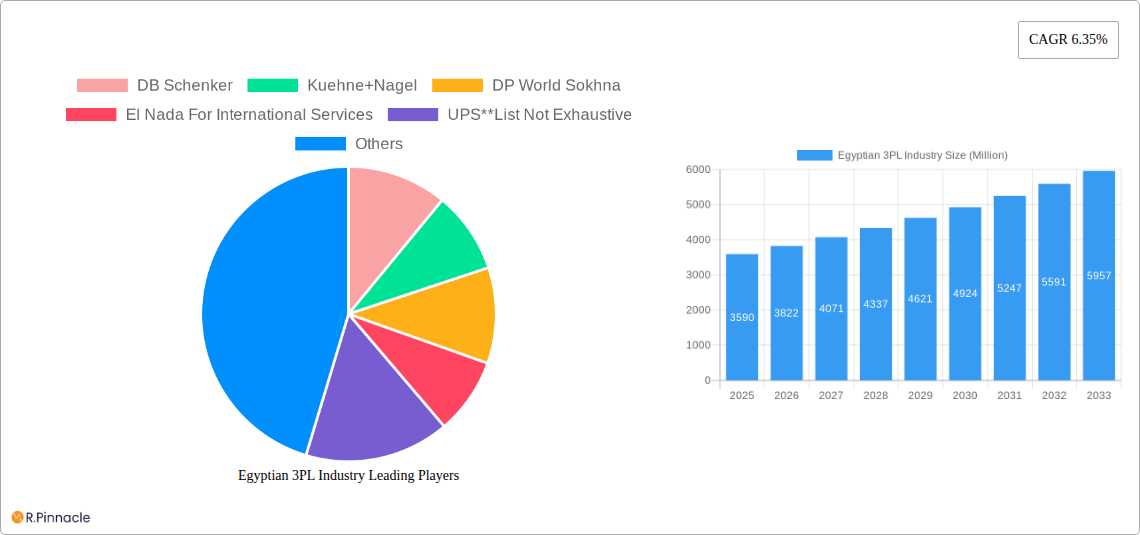

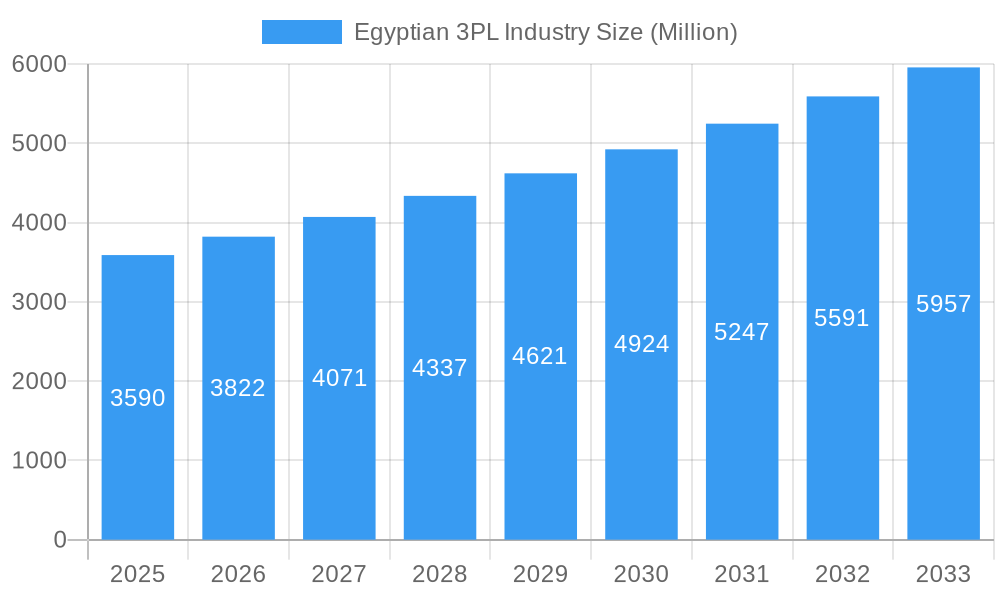

The Egyptian 3PL (Third-Party Logistics) industry, valued at $3.59 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 6.35% from 2025 to 2033. This expansion is fueled by several key drivers. The burgeoning e-commerce sector in Egypt significantly contributes to the demand for efficient warehousing, distribution, and domestic transportation management. Furthermore, the growth of manufacturing and automotive industries, coupled with increasing foreign direct investment, creates a strong need for reliable and scalable 3PL solutions. The rise of specialized services, such as value-added warehousing focusing on temperature-controlled storage (particularly crucial for pharmaceuticals) and specialized handling for the oil & gas sector, further boosts market growth. While challenges exist, such as infrastructure limitations in certain regions and fluctuating fuel prices, the overall positive economic outlook and increasing focus on supply chain optimization are expected to mitigate these constraints. Key players like DHL Supply Chain, FedEx, and Kuehne+Nagel are strategically positioning themselves to capitalize on these opportunities, leading to increased competition and innovation within the sector.

Egyptian 3PL Industry Market Size (In Billion)

The segmentation of the Egyptian 3PL market reveals significant opportunities across various service and end-user categories. Domestic transportation management currently holds the largest market share, closely followed by international transportation management, driven by increased cross-border trade. Value-added warehousing and distribution are experiencing rapid growth, particularly within the pharmaceutical and food sectors demanding specialized handling and storage. Among end-users, the manufacturing and automotive sectors are leading the demand, followed by the distributive trade (wholesale, retail, and e-commerce), highlighting the strong interconnectedness between the 3PL industry and the broader Egyptian economy. The projected growth trajectory suggests a promising future for the Egyptian 3PL sector, with continued investment in infrastructure and technological advancements expected to further enhance efficiency and scalability.

Egyptian 3PL Industry Company Market Share

Egyptian 3PL Industry: Market Analysis & Growth Forecast (2019-2033)

This comprehensive report provides a detailed analysis of the Egyptian 3PL (Third-Party Logistics) industry, offering invaluable insights for industry professionals, investors, and strategists. The report covers the period from 2019 to 2033, with a focus on the estimated year 2025. It leverages extensive research to forecast market trends and identify key opportunities within this rapidly evolving sector. The Egyptian 3PL market, valued at xx Million in 2025, is projected to experience significant growth, reaching xx Million by 2033, exhibiting a CAGR of xx%. Key players like DB Schenker, Kuehne+Nagel, DP World Sokhna, and DHL Supply Chain are shaping the landscape, alongside numerous other significant contributors.

Egyptian 3PL Industry Market Structure & Innovation Trends

The Egyptian 3PL market is characterized by a dynamic and evolving competitive landscape. The market exhibits a moderately concentrated structure, with a few dominant international and local players holding significant market share. This concentration is influenced by substantial capital investment requirements, economies of scale, and the strategic importance of established networks and technological infrastructure. For instance, key players like DB Schenker and Kuehne+Nagel often lead in integrated logistics solutions, while DP World Sokhna leverages its port-centric advantages. The market is further shaped by regulatory frameworks that, while aiming for streamlining, also present compliance considerations for operational efficiency and market access. Drivers of innovation are predominantly technological, with a strong emphasis on digitalization, automation, and AI-powered logistics solutions to enhance efficiency, reduce costs, and improve service delivery. The growing e-commerce sector is a significant catalyst, spurring demand for specialized last-mile delivery solutions and advanced fulfillment services. This has also led to increased M&A activities as larger players seek to consolidate their market positions or acquire specialized capabilities. Understanding the interplay of these structural elements and innovation trends is crucial for forecasting market trajectory and identifying strategic opportunities.

- Market Concentration: The Egyptian 3PL market exhibits a moderately concentrated structure, with a few major players holding significant market share. For instance, DB Schenker holds an estimated significant market share in integrated logistics and freight forwarding, while DP World Sokhna commands a substantial presence in port-based logistics and supply chain solutions. (Note: Specific percentages require up-to-date market research data).

- Innovation Drivers: The industry is propelled by rapid technological advancements including sophisticated automation in warehousing, AI-powered predictive analytics for demand forecasting and route optimization, and the adoption of IoT for real-time asset tracking. Government initiatives focused on national infrastructure development, such as new ports and transportation corridors, coupled with efforts to streamline customs and regulatory processes, are also significant contributors to innovation and operational efficiency.

- Regulatory Frameworks: Analysis of existing and proposed regulations is critical. These include laws pertaining to trade, transportation, customs procedures, and labor. Future policy shifts impacting market access, cross-border logistics, and data privacy will significantly influence pricing strategies, operational costs, and strategic expansion plans for 3PL providers.

- Product Substitutes: While traditional 3PL services remain robust, the rise of e-commerce has spurred the development of specialized, agile fulfillment and last-mile delivery solutions, which can be considered evolving substitutes or complementary services. In-house logistics departments within large corporations also represent a form of internal competition, though many opt for outsourcing to gain expertise and cost efficiencies.

- End-User Demographics: The distribution of 3PL services is diversifying across various end-user industries. The manufacturing sector requires robust inbound and outbound logistics, the retail sector demands agile inventory management and last-mile delivery, and the healthcare industry necessitates specialized handling and temperature-controlled logistics. These varying demands shape the market’s structure and drive the development of tailored service offerings.

- M&A Activities: The Egyptian 3PL sector has witnessed strategic mergers and acquisitions aimed at expanding service portfolios, geographical reach, and technological capabilities. Notable activities have included acquisitions of smaller, niche providers by larger players seeking to enhance their last-mile delivery networks or gain expertise in specialized sectors. (Note: Specific deal values require up-to-date market research data).

Egyptian 3PL Industry Market Dynamics & Trends

This section delves into the key growth drivers and trends shaping the Egyptian 3PL market. It examines technological disruptions, changing consumer preferences, and the competitive landscape to provide a comprehensive overview of market dynamics. Key aspects include:

- Market Growth Drivers: Increased e-commerce activity, rising foreign direct investment (FDI) in Egypt, and government initiatives promoting logistics infrastructure development are contributing to market expansion. The growth is further fueled by the increasing complexity of supply chains and the need for efficient logistics solutions.

- Technological Disruptions: The adoption of automation, big data analytics, and blockchain technology is transforming the industry, leading to enhanced efficiency, transparency, and cost optimization.

- Consumer Preferences: Evolving consumer expectations regarding speed, transparency, and traceability in deliveries are driving demand for innovative 3PL solutions. The rise of omnichannel retailing has created a need for flexibility and responsiveness from 3PL providers.

- Competitive Dynamics: The report analyzes the competitive strategies of leading players, including pricing models, service offerings, and market positioning. The highly competitive nature of the market is analyzed through a review of companies' expansion strategies and market share dynamics.

Dominant Regions & Segments in Egyptian 3PL Industry

This section pinpoints the leading geographical regions and service/end-user segments within the Egyptian 3PL market, providing a detailed analysis of their dominance.

By Service:

- Domestic Transportation Management: [Paragraph discussing the dominance, key drivers, and market size of domestic transportation management. Include factors like road infrastructure, transportation regulations, and the prevalence of domestic trade.]

- International Transportation Management: [Paragraph discussing the dominance, key drivers, and market size of international transportation management. Include factors like port capacity, trade agreements, and global supply chain connections.]

- Value-added Warehousing and Distribution: [Paragraph discussing the dominance, key drivers, and market size of value-added warehousing and distribution. Include factors like warehousing infrastructure, technological advancements in warehouse management, and demand for specialized services.]

By End User:

- Manufacturing and Automotive: [Paragraph discussing the dominance, key drivers, and market size of the Manufacturing and Automotive segments. Include factors like industrial production levels, FDI in the manufacturing sector, and the complexity of automotive logistics.]

- Oil & Gas and Chemical: [Paragraph discussing the dominance, key drivers, and market size of the Oil & Gas and Chemical segments. Include factors like production levels, export volumes, and specialized handling requirements.]

- Distributive Trade (Wholesale and Retail trade including e-commerce): [Paragraph discussing the dominance, key drivers, and market size of Distributive Trade. Include factors like e-commerce growth, retail expansion, and the need for efficient last-mile delivery solutions.]

- Pharma & Healthcare: [Paragraph discussing the dominance, key drivers, and market size of Pharma & Healthcare. Include factors like stringent regulatory requirements, temperature-sensitive logistics, and the need for secure handling.]

- Construction: [Paragraph discussing the dominance, key drivers, and market size of the Construction sector. Include factors like infrastructure development projects, construction material logistics, and the demand for specialized transportation services.]

- Other End Users: [Paragraph covering other end-user segments and their relative importance within the Egyptian 3PL market.]

Egyptian 3PL Industry Product Innovations

The Egyptian 3PL industry is experiencing a transformative wave of product and service innovations, largely fueled by digital advancements and the imperative to enhance efficiency and customer satisfaction. Leading innovations include the widespread adoption of advanced Warehouse Management Systems (WMS) and Transportation Management Systems (TMS), which are now increasingly integrated with AI for predictive analytics, optimizing inventory levels, and forecasting demand with greater accuracy. Route optimization software is becoming more sophisticated, leveraging real-time traffic data and vehicle telematics to minimize transit times and fuel consumption. The integration of the Internet of Things (IoT) devices provides unprecedented real-time visibility into asset location, condition (e.g., temperature, humidity), and performance. Blockchain technology is emerging as a key enabler for enhanced transparency, traceability, and security across complex supply chains, particularly for high-value goods and pharmaceuticals. These technological leaps are not just about operational improvements; they are critical for 3PL providers to differentiate themselves, meet the escalating expectations of clients for speed and reliability, and proactively adapt to the rapidly evolving demands of the global and local markets.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Egyptian 3PL market segmented by service type (Domestic Transportation Management, International Transportation Management, Value-added Warehousing and Distribution) and end-user industry (Manufacturing and Automotive, Oil & Gas and Chemical, Distributive Trade, Pharma & Healthcare, Construction, Other). Each segment's market size, growth projections, and competitive dynamics are detailed within the report, offering a granular understanding of the market's structure and future trajectory. For example, the e-commerce boom significantly drives the growth of the value-added warehousing and distribution segment, leading to increased investment in automated warehouses and fulfillment centers.

Key Drivers of Egyptian 3PL Industry Growth

The growth of the Egyptian 3PL industry is fueled by a confluence of factors. Significant infrastructure investments by the government are improving transportation networks, facilitating smoother logistics operations. The rapid expansion of the e-commerce sector generates immense demand for efficient delivery and warehousing solutions. Furthermore, the rising foreign direct investment (FDI) in Egypt stimulates economic activity and boosts the demand for 3PL services across various sectors. Finally, favorable government regulations create a conducive environment for industry growth and innovation.

Challenges in the Egyptian 3PL Industry Sector

Despite the promising growth outlook, the Egyptian 3PL industry faces several challenges. Bureaucracy and complex regulatory procedures can impede operational efficiency. Infrastructure limitations, particularly in certain regions, pose constraints on timely delivery. Furthermore, intense competition among established players and new entrants necessitates continuous innovation and adaptation to maintain market share. These issues contribute to higher operational costs and can impact overall profitability.

Emerging Opportunities in Egyptian 3PL Industry

The Egyptian 3PL industry presents numerous emerging opportunities. The expansion of e-commerce, particularly in less-served areas, creates considerable scope for specialized last-mile delivery services. The increasing adoption of advanced technologies such as AI and blockchain presents opportunities for enhanced efficiency and transparency. Furthermore, growth in specific sectors like healthcare and pharmaceuticals, with their stringent regulatory requirements, necessitates specialized 3PL solutions.

Leading Players in the Egyptian 3PL Industry Market

- DB Schenker

- Kuehne+Nagel

- DP World Sokhna

- El Nada For International Services

- UPS

- FedEx

- Intex Express

- Expeditors

- DCM

- Eastern Logistics

- Agility

- Panalpina (now part of DSV)

- Aramex

- DHL Supply Chain

Key Developments in Egyptian 3PL Industry Industry

- Q1 2024: DB Schenker expands its advanced warehousing and distribution hub in Greater Cairo, enhancing its capacity for e-commerce fulfillment and temperature-controlled logistics.

- Q4 2023: New government regulations are implemented to streamline customs clearance procedures for imported goods, significantly reducing transit times and operational costs for 3PL providers.

- Q3 2023: Aramex inaugurates a state-of-the-art, automated e-commerce fulfillment center in Alexandria, boosting its capacity to handle peak season volumes and improve delivery accuracy.

- Q2 2023: A strategic merger between two prominent local 3PL providers, "Logistics Solutions Egypt" and "Nile Transport," is finalized, creating a stronger entity with expanded service offerings and national reach.

- Q1 2024: DHL Supply Chain announces significant investment in its fleet, incorporating electric and hybrid vehicles to reduce its carbon footprint and meet sustainability targets.

Future Outlook for Egyptian 3PL Industry Market

The Egyptian 3PL market is on a trajectory of robust and sustained growth, underpinned by several key economic and demographic factors. The continuous expansion of the e-commerce sector, coupled with the government's ambitious infrastructure development projects, including new industrial zones and transportation networks, will create significant demand for efficient logistics services. Increasing foreign direct investment in various sectors will also necessitate sophisticated supply chain solutions. Future success for 3PL providers will hinge on their ability to make strategic investments in cutting-edge technology, such as AI-driven logistics, automation, and advanced data analytics, to offer value-added services. The development of specialized logistics capabilities for high-growth sectors like pharmaceuticals, automotive, and cold chain will be a key differentiator. Companies that can demonstrate agility, offer end-to-end supply chain visibility, and adapt quickly to evolving consumer preferences and regulatory changes will be best positioned to capture substantial market share and achieve sustainable, long-term growth in this increasingly competitive and vital industry.

Egyptian 3PL Industry Segmentation

-

1. Service

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Oil & Gas and Chemical

- 2.3. Distribu

- 2.4. Pharma & Healthcare

- 2.5. Construction

- 2.6. Other End Users

Egyptian 3PL Industry Segmentation By Geography

- 1. Egypt

Egyptian 3PL Industry Regional Market Share

Geographic Coverage of Egyptian 3PL Industry

Egyptian 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Oil & Gas and Chemical

- 5.2.3. Distribu

- 5.2.4. Pharma & Healthcare

- 5.2.5. Construction

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Egyptian 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Oil & Gas and Chemical

- 6.2.3. Distribu

- 6.2.4. Pharma & Healthcare

- 6.2.5. Construction

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kuehne+Nagel

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DP World Sokhna

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 El Nada For International Services

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 UPS**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FedEx

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Intex Express

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Expeditors

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 DCM

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Eastern Logistics

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Agility

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Panalpina

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Aramex

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 DHL Supply Chain

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Egyptian 3PL Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Egyptian 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Egyptian 3PL Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 2: Egyptian 3PL Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Egyptian 3PL Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Egyptian 3PL Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 5: Egyptian 3PL Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Egyptian 3PL Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Egyptian 3PL Industry?

The projected CAGR is approximately 6.35%.

2. Which companies are prominent players in the Egyptian 3PL Industry?

Key companies in the market include DB Schenker, Kuehne+Nagel, DP World Sokhna, El Nada For International Services, UPS**List Not Exhaustive, FedEx, Intex Express, Expeditors, DCM, Eastern Logistics, Agility, Panalpina, Aramex, DHL Supply Chain.

3. What are the main segments of the Egyptian 3PL Industry?

The market segments include Service, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.59 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing volume of international trade4.; The rise of trade agreements between nations.

6. What are the notable trends driving market growth?

Growth in Maritime Transport in Egypt.

7. Are there any restraints impacting market growth?

4.; Surge in fuel costs affecting the market4.; Increasing trade tension.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Egyptian 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Egyptian 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Egyptian 3PL Industry?

To stay informed about further developments, trends, and reports in the Egyptian 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence