Key Insights

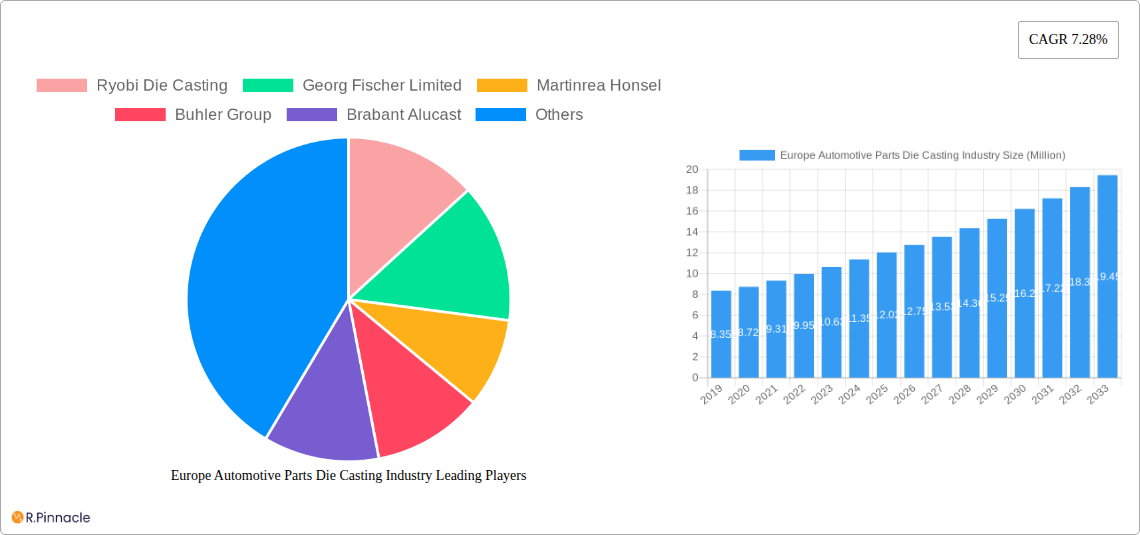

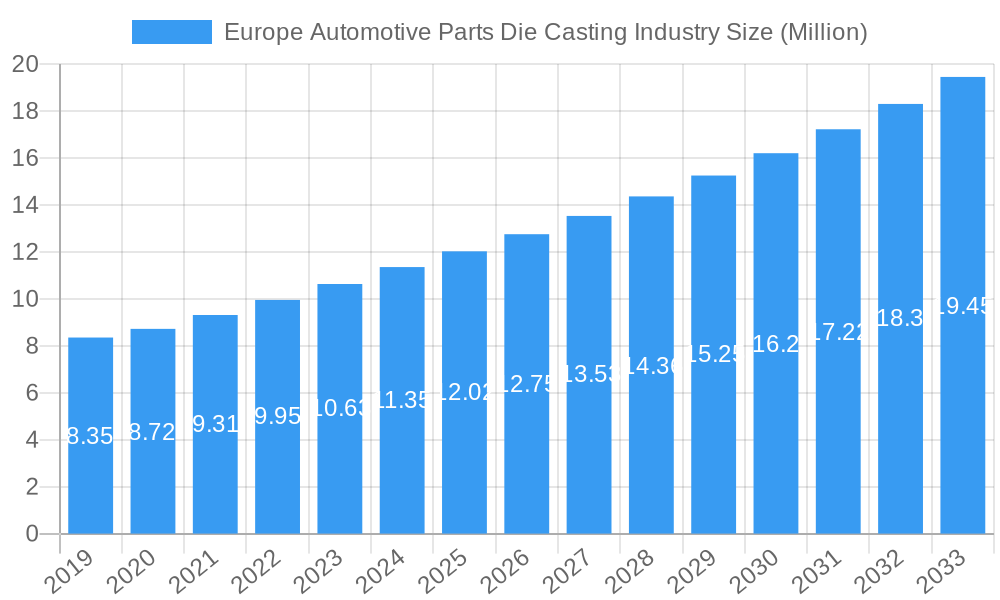

The European automotive parts die casting industry is poised for significant growth, projected to reach 12.02 Million in value by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 7.28% through 2033. This robust expansion is primarily fueled by the increasing demand for lightweight and fuel-efficient vehicles. As stringent emission regulations continue to shape the automotive landscape, manufacturers are heavily investing in advanced materials like aluminum and zinc alloys for critical components such as engine parts, transmission components, and structural parts. The rise of electric vehicles (EVs) also presents a substantial opportunity, driving the need for specialized die-cast components for battery housings, motor casings, and thermal management systems. Key players like Ryobi Die Casting, Georg Fischer Limited, and Nemak are at the forefront, innovating with advanced die casting techniques, including sophisticated vacuum die casting and pressure die casting processes, to meet the evolving needs of automakers for higher precision, improved strength-to-weight ratios, and cost-effectiveness.

Europe Automotive Parts Die Casting Industry Market Size (In Million)

Despite the optimistic outlook, the industry faces certain restraints. Volatility in raw material prices, particularly for aluminum and zinc, can impact profitability and necessitate strategic hedging and sourcing. Furthermore, the increasing complexity of automotive parts and the need for highly skilled labor for advanced die casting operations present ongoing challenges. However, the overarching trend towards vehicle electrification, autonomous driving technologies, and stringent safety standards continues to propel the demand for high-performance, precisely engineered die-cast components. Europe's established automotive manufacturing base, coupled with a strong focus on technological innovation and sustainability, positions it as a pivotal region in the global automotive parts die casting market. The industry's ability to adapt to these dynamics, particularly by embracing sustainable manufacturing practices and investing in R&D for next-generation components, will be crucial for continued success.

Europe Automotive Parts Die Casting Industry Company Market Share

Europe Automotive Parts Die Casting Industry Market Analysis: Future-Proofing Your Strategy (2019–2033)

This comprehensive report provides an in-depth analysis of the Europe Automotive Parts Die Casting Industry, offering actionable insights and strategic recommendations for industry stakeholders. Leveraging real-time data and expert analysis, we explore market dynamics, identify growth drivers, and forecast future trends. Our study covers the period from 2019 to 2033, with a base year of 2025, offering a robust outlook for the next decade. This report is essential for manufacturers, suppliers, investors, and policymakers seeking to navigate the evolving landscape of automotive parts die casting in Europe.

Europe Automotive Parts Die Casting Industry Market Structure & Innovation Trends

The Europe Automotive Parts Die Casting industry exhibits a moderately consolidated market structure, with key players dominating significant market share. Innovation is primarily driven by the increasing demand for lightweight components, enhanced fuel efficiency, and the burgeoning electric vehicle (EV) market. Regulatory frameworks, particularly those concerning emissions and sustainability, are increasingly influencing product development and manufacturing processes. While product substitutes exist, the inherent advantages of die-cast parts in terms of strength, precision, and cost-effectiveness maintain their competitive edge. End-user demographics are shifting towards younger, environmentally conscious consumers, demanding more sustainable and technologically advanced vehicles. Mergers and acquisitions (M&A) activities are strategic, aimed at expanding technological capabilities and market reach. For instance, M&A deals in the past have focused on acquiring expertise in advanced casting techniques and securing access to emerging EV component markets, with estimated deal values in the hundreds of millions of Euros. The market share of top players is estimated to be around 60-70%, indicating a degree of concentration.

Europe Automotive Parts Die Casting Industry Market Dynamics & Trends

The Europe Automotive Parts Die Casting industry is experiencing a dynamic transformation, propelled by a confluence of growth drivers and technological disruptions. The accelerating adoption of electric vehicles (EVs) represents a pivotal trend, significantly influencing demand for specific die-cast components like battery housings, motor casings, and structural elements for lighter chassis designs. This shift is supported by government incentives and growing consumer preference for sustainable transportation, driving market penetration of EV-related die-cast parts. Furthermore, stringent emission regulations across Europe are compelling automakers to focus on reducing vehicle weight, thereby increasing the demand for high-performance, lightweight aluminum and magnesium alloy die castings. Advanced manufacturing techniques, including sophisticated vacuum die casting and high-pressure die casting processes, are becoming standard, enabling the production of intricate and robust parts with superior mechanical properties. Technological disruptions are also emerging in the form of advanced simulation software and AI-driven process optimization, enhancing efficiency and reducing production costs. Consumer preferences are increasingly leaning towards vehicles with enhanced safety features, greater energy efficiency, and integrated smart technologies, all of which benefit from precisely engineered die-cast components. The competitive dynamics are intensifying, with established players investing heavily in R&D and capacity expansion, while new entrants are focusing on niche segments and innovative material applications. The overall Compound Annual Growth Rate (CAGR) for the Europe Automotive Parts Die Casting Industry is projected to be between 6% and 8% during the forecast period. The market penetration of advanced die-cast components in new vehicle architectures is expected to grow by an estimated 15-20% by 2030.

Dominant Regions & Segments in Europe Automotive Parts Die Casting Industry

The Germany region stands as the dominant force within the Europe Automotive Parts Die Casting Industry, owing to its robust automotive manufacturing base, extensive research and development capabilities, and strong governmental support for technological innovation. Germany's automotive sector, a global leader, consistently drives demand for high-quality die-cast components. The region benefits from a well-established ecosystem of Tier 1 suppliers, die casters, and material providers, fostering collaboration and efficiency.

Production Process Type:

- Pressure Die Casting: This remains the most prevalent production process due to its efficiency, high production rates, and ability to produce complex shapes with tight tolerances. Its dominance is driven by its suitability for mass production of a wide range of automotive components.

- Vacuum Die Casting: Gaining significant traction, particularly for high-strength aluminum alloys and complex structural parts requiring superior mechanical properties and reduced porosity. Its application is growing with the demand for lighter and more resilient components in modern vehicles.

- Other Production Process Types: While less dominant, these include gravity die casting and low-pressure die casting, often used for specific applications where cost-effectiveness or unique material properties are paramount.

Metal Type:

- Aluminum: This is the leading metal type, owing to its excellent strength-to-weight ratio, corrosion resistance, and recyclability. Its increasing use is directly linked to the industry's push for lightweighting.

- Zinc: Continues to be important for components requiring high ductility, wear resistance, and intricate detail, such as lock mechanisms and trim components.

- Other Metal Types: Magnesium alloys are gaining attention for their even lower density compared to aluminum, especially for EV components, though their adoption is still in a growth phase.

Application Type:

- Engine Parts: While the shift to EVs may reduce the demand for traditional internal combustion engine (ICE) parts, existing and hybrid vehicle production still sustains this segment. This includes engine blocks, cylinder heads, and intake manifolds.

- Transmission Components: Crucial for both ICE and EV powertrains, including gearbox housings, clutch components, and torque converter housings. The complexity and precision required make die casting an ideal manufacturing method.

- Structural Parts: This segment is experiencing significant growth, driven by the demand for lighter vehicle frames, chassis components, and body-in-white parts that enhance safety and fuel efficiency.

- Other Application Types: This encompasses a broad range of components such as steering system parts, suspension components, and various interior and exterior trim elements.

Economic policies supporting advanced manufacturing and infrastructure development within Germany and other key European nations further reinforce the dominance of these segments.

Europe Automotive Parts Die Casting Industry Product Innovations

Product innovations in the Europe Automotive Parts Die Casting industry are primarily focused on enabling the transition to electric mobility and improving the efficiency of traditional vehicles. Manufacturers are developing advanced lightweight aluminum alloy components for EV battery enclosures, motor housings, and power electronics. Innovations in vacuum die casting and advanced mold design are crucial for achieving the high precision and structural integrity required for these critical EV parts. Furthermore, there's a growing emphasis on producing complex, integrated structural components that reduce the overall part count and assembly time, leading to cost savings and improved vehicle performance. The competitive advantage lies in the ability to offer optimized designs that enhance thermal management, electrical insulation, and overall vehicle safety while meeting stringent lightweighting targets.

Report Scope & Segmentation Analysis

This report meticulously dissects the Europe Automotive Parts Die Casting Industry across key segmentation parameters. We provide detailed analysis for:

Production Process Type:

- Vacuum Die Casting: This segment is projected for significant growth, driven by the increasing demand for high-performance components in premium vehicles and EVs. Market size is estimated to reach over EUR 1.5 Billion by 2033, with a CAGR of 7.5%.

- Pressure Die Casting: Remaining the largest segment, it will continue to dominate due to its widespread application in high-volume production. Projected market size exceeds EUR 4 Billion by 2033, with a CAGR of 6.2%.

- Other Production Process Types: This segment, while smaller, will see steady growth, catering to niche applications. Expected market size of around EUR 500 Million by 2033, with a CAGR of 5.8%.

Metal Type:

- Aluminum: This segment will exhibit the strongest growth, fueled by lightweighting initiatives and EV adoption. Expected market size over EUR 4.5 Billion by 2033, with a CAGR of 7.8%.

- Zinc: Stable growth is anticipated, driven by specific applications requiring its unique properties. Projected market size of around EUR 1.2 Billion by 2033, with a CAGR of 5.5%.

- Other Metal Types: Magnesium alloys are expected to experience exponential growth, albeit from a smaller base, as their lightweighting benefits become more widely realized. Projected market size of around EUR 800 Million by 2033, with a CAGR of 9.2%.

Application Type:

- Engine Parts: While facing a long-term decline in ICE vehicles, this segment will remain substantial due to hybrid powertrains and existing ICE fleet maintenance. Expected market size around EUR 2 Billion by 2033, with a CAGR of 4.5%.

- Transmission Components: Essential for both ICE and EV drivetrains, this segment will show robust growth. Projected market size exceeding EUR 2.5 Billion by 2033, with a CAGR of 6.8%.

- Structural Parts: This is a key growth area, driven by vehicle lightweighting and platform modularity. Expected market size over EUR 3 Billion by 2033, with a CAGR of 7.9%.

- Other Application Types: This diverse segment will experience steady growth, reflecting the broad applicability of die-cast parts. Projected market size of around EUR 1.5 Billion by 2033, with a CAGR of 6.0%.

Key Drivers of Europe Automotive Parts Die Casting Industry Growth

The Europe Automotive Parts Die Casting industry's growth is propelled by several interconnected factors. The global push towards electrification of vehicles is a primary driver, creating substantial demand for specialized EV components like battery housings and motor casings, which are ideally suited for die casting. Stringent environmental regulations across Europe, mandating reduced emissions, further incentivize lightweighting, thus boosting the demand for aluminum and magnesium alloy die castings. Technological advancements in die casting processes, such as improved automation, simulation software, and material science, enhance precision, efficiency, and cost-effectiveness. The automotive industry's focus on modularization and platform strategies also contributes, as die casting allows for the production of complex, integrated components that reduce assembly time and costs. Finally, the growing demand for enhanced vehicle performance and safety features directly translates into a need for high-strength, precisely engineered die-cast parts.

Challenges in the Europe Automotive Parts Die Casting Industry Sector

Despite strong growth prospects, the Europe Automotive Parts Die Casting industry faces several significant challenges. Rising raw material costs, particularly for aluminum and magnesium, can impact profitability and pricing strategies. Intensifying global competition, especially from emerging economies with lower production costs, puts pressure on European manufacturers. Supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can affect production schedules and material availability. The skilled labor shortage in advanced manufacturing and specialized die casting operations presents a hurdle for companies looking to expand or adopt new technologies. Furthermore, the transition to entirely electric vehicles poses a long-term challenge for manufacturers heavily reliant on traditional internal combustion engine (ICE) component production, requiring significant strategic adaptation and investment in new capabilities. The estimated impact of these challenges on market growth could be a reduction of 0.5% to 1% in the projected CAGR.

Emerging Opportunities in Europe Automotive Parts Die Casting Industry

The Europe Automotive Parts Die Casting industry is ripe with emerging opportunities. The rapid expansion of the electric vehicle (EV) market presents a significant avenue for growth, particularly in the production of battery components, electric motor housings, and lightweight structural elements for EV platforms. The increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies will drive demand for complex, high-precision die-cast sensor housings and electronic enclosures. Furthermore, the focus on sustainable manufacturing practices opens opportunities for companies that can adopt circular economy principles, utilize recycled materials, and minimize their environmental footprint. The trend towards vehicle lightweighting continues to be a key opportunity, driving innovation in the use of lighter alloys like magnesium for a wider range of structural and interior components. Finally, the reshoring initiatives in certain automotive supply chains could create new domestic manufacturing opportunities.

Leading Players in the Europe Automotive Parts Die Casting Industry Market

- Ryobi Die Casting

- Georg Fischer Limited

- Martinrea Honsel

- Buhler Group

- Brabant Alucast

- DGS Druckguss Systeme

- Nemak

- Dynacast

- Rheinmetall Automotive

Key Developments in Europe Automotive Parts Die Casting Industry Industry

- September 2022: Rheinmetall AG (Rheinmetall) secured a new EUR 20 million (USD 23.6 million) order for its cutting-edge air-divert valve, the Turbo Bypass Valve (TBV) Gen 6, further solidifying its position as a key player in the industry. This order adds to the series of recent successful orders received by the Group subsidiary. Production of the TBV Gen 6 will be carried out at Pierburg's Neuss, Germany, plant.

- May 2022: GF Casting Solutions, a division of Georg Fischer, announced its commitment to enhance the development of electric vehicle (EV) products and services. Leveraging its expertise and artificial intelligence (AI), the company aims to facilitate customers' transition to electric drive engines and e-mobility. By utilizing AI, GF Casting Solutions can deliver high-quality products that contribute positively to the environment.

Future Outlook for Europe Automotive Parts Die Casting Industry Market

The future outlook for the Europe Automotive Parts Die Casting Industry is exceptionally promising, driven by the sustained transition to electric mobility and an unwavering focus on vehicle lightweighting. The industry is poised for robust growth, with an estimated market expansion of over 50% in the next decade. Growth accelerators include the increasing integration of advanced die-cast components in next-generation EV architectures, the development of novel lightweight alloys, and the adoption of Industry 4.0 technologies for enhanced process control and efficiency. Strategic opportunities lie in expanding production capacity for EV-specific components, investing in R&D for magnesium alloys, and forging partnerships with electric vehicle manufacturers. The industry's ability to innovate and adapt to evolving automotive trends will be key to capitalizing on its significant future potential.

Europe Automotive Parts Die Casting Industry Segmentation

-

1. Production Process Type

- 1.1. Vacuum Die Casting

- 1.2. Pressure Die Casting

- 1.3. Other Production Process Types

-

2. Metal Type

- 2.1. Aluminum

- 2.2. Zinc

- 2.3. Other Metal Types

-

3. Application Type

- 3.1. Engine Parts

- 3.2. Transmission Components

- 3.3. Structural Parts

- 3.4. Other Application Types

Europe Automotive Parts Die Casting Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Italy

- 1.5. Russia

- 1.6. Rest of Europe

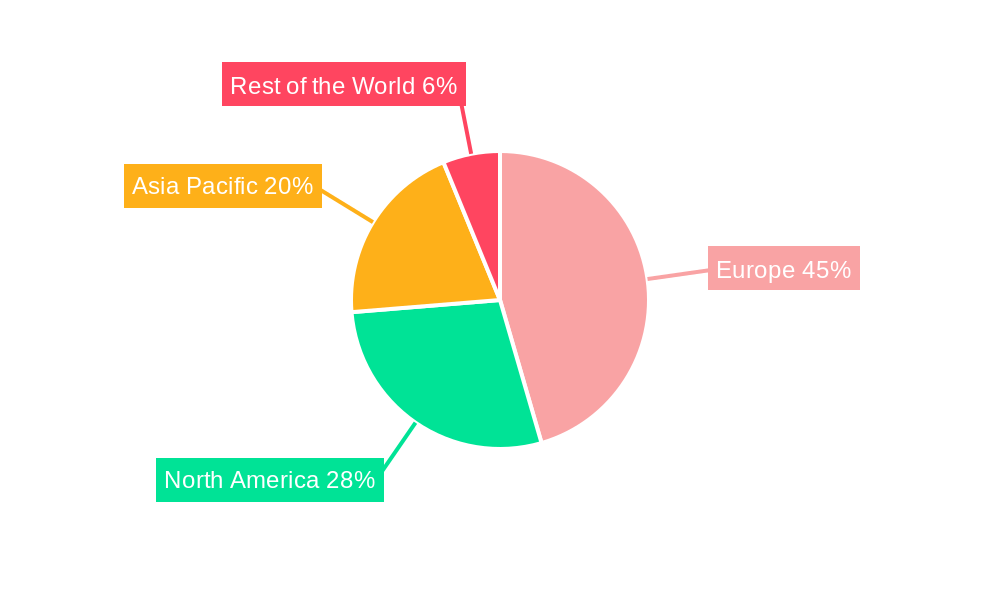

Europe Automotive Parts Die Casting Industry Regional Market Share

Geographic Coverage of Europe Automotive Parts Die Casting Industry

Europe Automotive Parts Die Casting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Vacuum Die Casting

- 5.1.2. Pressure Die Casting

- 5.1.3. Other Production Process Types

- 5.2. Market Analysis, Insights and Forecast - by Metal Type

- 5.2.1. Aluminum

- 5.2.2. Zinc

- 5.2.3. Other Metal Types

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Engine Parts

- 5.3.2. Transmission Components

- 5.3.3. Structural Parts

- 5.3.4. Other Application Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. Europe Automotive Parts Die Casting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Vacuum Die Casting

- 6.1.2. Pressure Die Casting

- 6.1.3. Other Production Process Types

- 6.2. Market Analysis, Insights and Forecast - by Metal Type

- 6.2.1. Aluminum

- 6.2.2. Zinc

- 6.2.3. Other Metal Types

- 6.3. Market Analysis, Insights and Forecast - by Application Type

- 6.3.1. Engine Parts

- 6.3.2. Transmission Components

- 6.3.3. Structural Parts

- 6.3.4. Other Application Types

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ryobi Die Casting

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Georg Fischer Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Martinrea Honsel

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Buhler Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Brabant Alucast

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 DGS Druckguss Systeme*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nemak

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Dynacast

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rheinmetall Automotive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Ryobi Die Casting

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Automotive Parts Die Casting Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Parts Die Casting Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 2: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Metal Type 2020 & 2033

- Table 3: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 4: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 6: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Metal Type 2020 & 2033

- Table 7: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 8: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Germany Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: United Kingdom Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: France Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Russia Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Rest of Europe Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Parts Die Casting Industry?

The projected CAGR is approximately 7.28%.

2. Which companies are prominent players in the Europe Automotive Parts Die Casting Industry?

Key companies in the market include Ryobi Die Casting, Georg Fischer Limited, Martinrea Honsel, Buhler Group, Brabant Alucast, DGS Druckguss Systeme*List Not Exhaustive, Nemak, Dynacast, Rheinmetall Automotive.

3. What are the main segments of the Europe Automotive Parts Die Casting Industry?

The market segments include Production Process Type, Metal Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Use of Aluminum in Die Casting Equipment to Increase Market Demand.

6. What are the notable trends driving market growth?

Increasing Demand from the Commercial Vehicle Segment.

7. Are there any restraints impacting market growth?

Fluctuations in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

September 2022: Rheinmetall AG (Rheinmetall) secured a new EUR 20 million (USD 23.6 million) order for its cutting-edge air-divert valve, the Turbo Bypass Valve (TBV) Gen 6, further solidifying its position as a key player in the industry. This order adds to the series of recent successful orders received by the Group subsidiary. Production of the TBV Gen 6 will be carried out at Pierburg's Neuss, Germany, plant.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Parts Die Casting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Parts Die Casting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Parts Die Casting Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Parts Die Casting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence