Key Insights

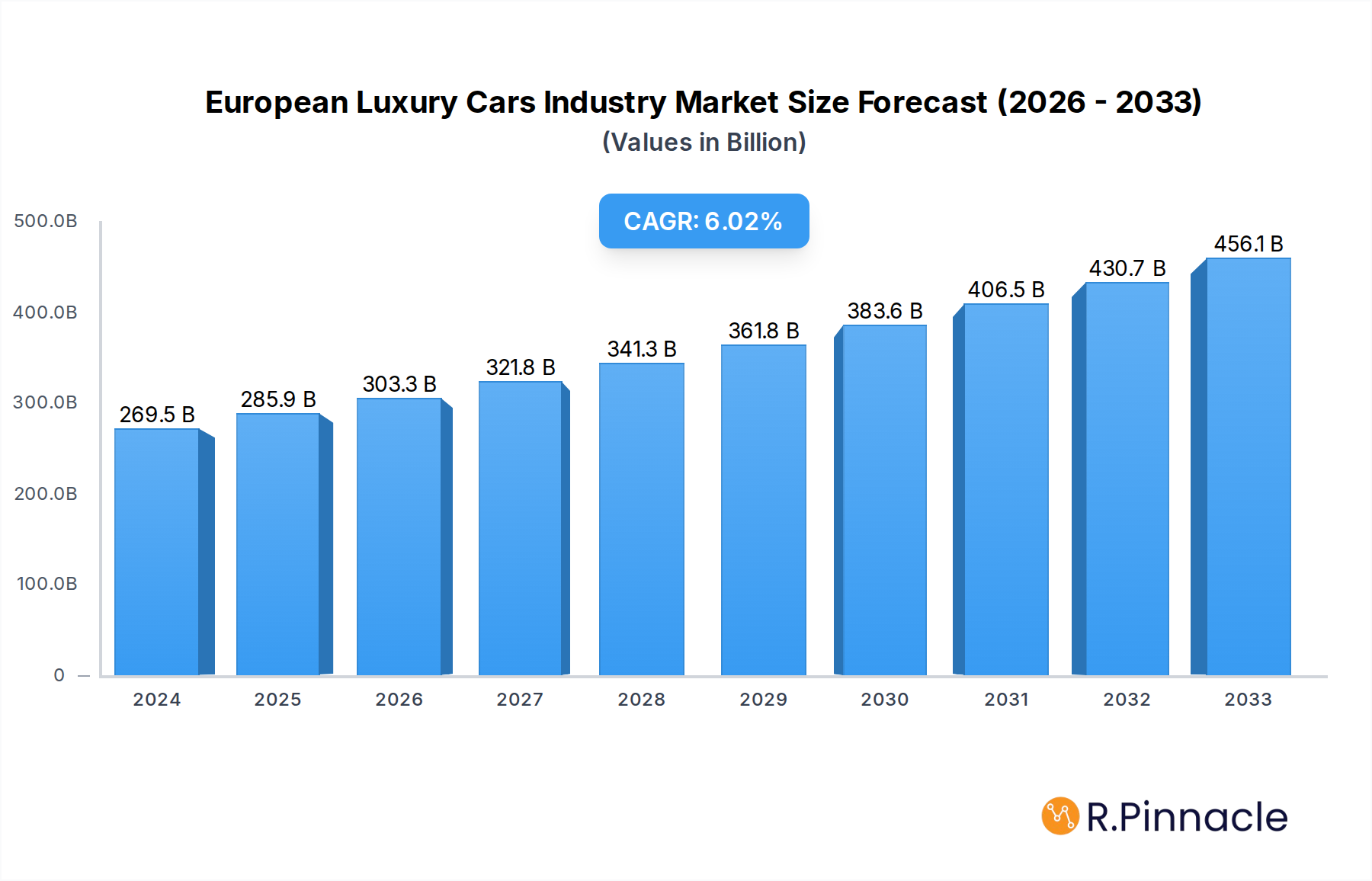

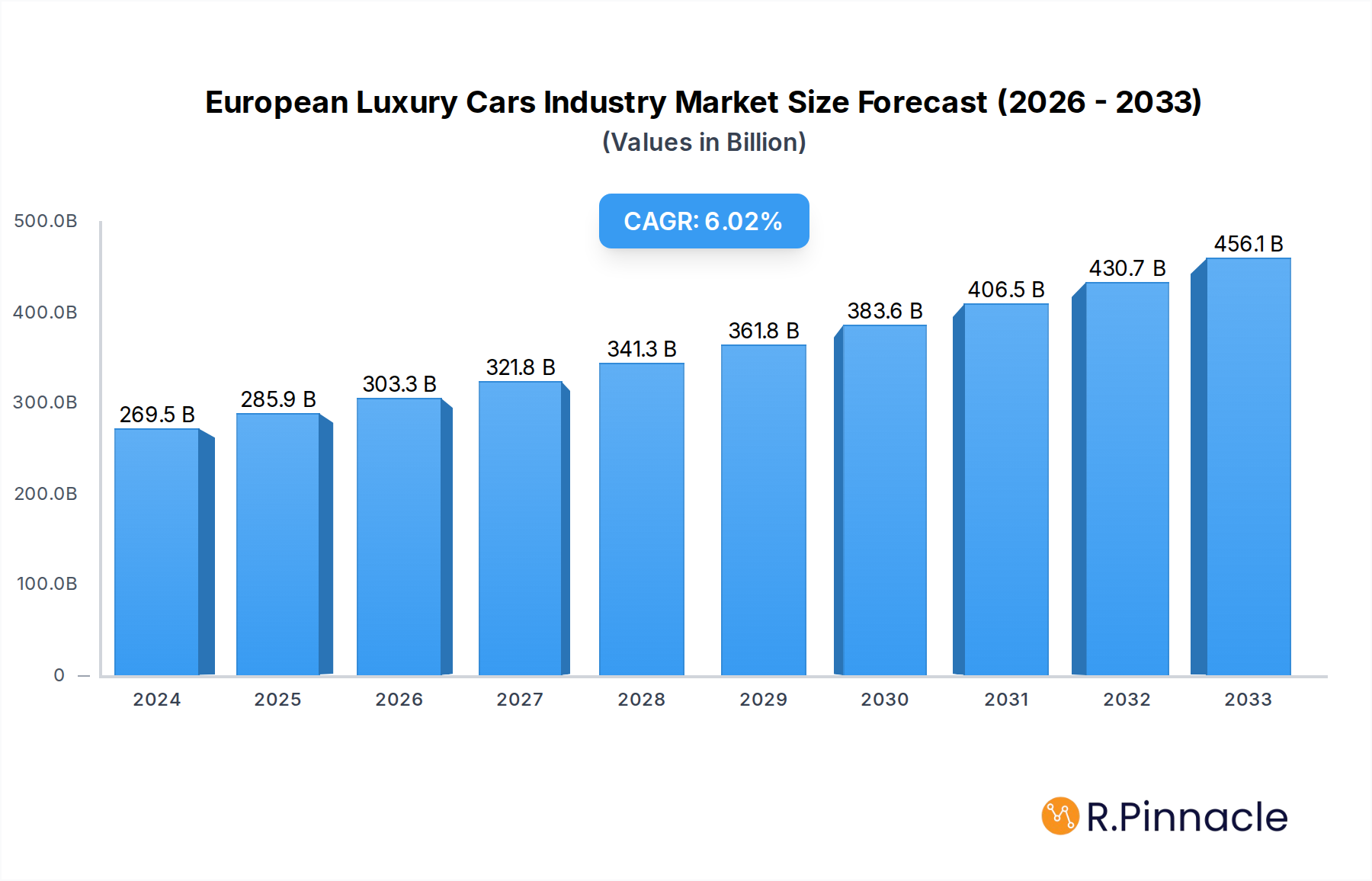

The European luxury car market is poised for significant expansion, projecting a robust market size of USD 269,495.7 million in 2024 and an impressive Compound Annual Growth Rate (CAGR) of 6.3% through 2033. This growth is primarily fueled by evolving consumer preferences for advanced technology, sustainable mobility solutions, and enhanced driving experiences. The increasing demand for electrified powertrains, particularly within the premium segment, is a major driver, aligning with Europe's stringent environmental regulations and growing consumer consciousness. Furthermore, the introduction of new luxury models across various vehicle types, including sophisticated SUVs and elegantly designed sedans and hatchbacks, is captivating a discerning customer base. The "experience economy" trend, where consumers prioritize unique and premium encounters, also plays a crucial role, with luxury car manufacturers focusing on personalized services, innovative in-car technology, and exclusive ownership benefits to cater to this demand.

European Luxury Cars Industry Market Size (In Billion)

The market's trajectory is further shaped by key trends such as the increasing adoption of autonomous driving features, advanced connectivity services, and the growing popularity of multi-purpose luxury vehicles that blend practicality with opulence. While the transition towards electric vehicles presents opportunities, the ongoing investment in research and development for internal combustion engine (ICE) efficiency continues to cater to a segment of the market. Key industry players like Mercedes-Benz Group AG, Hyundai Motor Company, and Tesla Inc. are actively investing in product innovation and market penetration strategies to capture market share. Geographically, Western European nations are expected to continue leading the market due to higher disposable incomes and a strong existing luxury car culture, although Eastern European markets are showing promising growth potential as their economies develop. Challenges such as fluctuating raw material costs and geopolitical uncertainties are being navigated by strategic market positioning and supply chain diversification.

European Luxury Cars Industry Company Market Share

European Luxury Cars Industry Market Report: Growth Drivers, Innovations, and Forecasts (2019–2033)

This comprehensive report delves into the dynamic European luxury car market, offering in-depth analysis of market structure, key dynamics, regional dominance, and product innovations. With a study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period of 2025–2033, this report provides critical insights for automotive manufacturers, suppliers, investors, and industry stakeholders seeking to understand and capitalize on emerging trends in the luxury automotive sector. Leveraging high-ranking keywords such as "European luxury cars," "electric vehicle market Europe," "automotive industry trends," and "luxury car market share," this report aims to enhance search visibility and provide actionable intelligence for industry professionals.

European Luxury Cars Industry Market Structure & Innovation Trends

The European luxury car market exhibits a moderately concentrated structure, with a few key players holding significant market share. For instance, Mercedes-Benz Group AG and BMW AG consistently command substantial portions of the premium segment. Innovation remains a primary driver of market dynamics, fueled by the relentless pursuit of advanced automotive technologies, particularly in the realm of electrification and autonomous driving. Regulatory frameworks, such as stringent emission standards set by the European Union, are profoundly shaping product development and market entry strategies, pushing manufacturers towards sustainable mobility solutions. The threat of product substitutes is relatively low within the pure luxury segment, though the increasing sophistication of high-end mainstream vehicles presents a competitive challenge. End-user demographics are shifting towards a younger, tech-savvy consumer base with a growing appreciation for sustainability and digital integration. Mergers and Acquisitions (M&A) activities, while not as frequent as in other sectors, are strategic and often focused on acquiring niche technologies or expanding market reach. For example, the acquisition of technology startups by major automotive groups signals a move towards integrating cutting-edge digital and autonomous capabilities. The overall market share of electric luxury vehicles is rapidly expanding, driven by both consumer demand and regulatory incentives, projected to reach significant penetration by 2033.

- Market Concentration: Dominated by key premium brands with substantial market share.

- Innovation Drivers: Electrification, autonomous driving, connectivity, and sustainable materials.

- Regulatory Frameworks: Strict emission standards (e.g., Euro 7), safety regulations, and incentives for EVs.

- Product Substitutes: High-end mainstream vehicles, with luxury brands differentiating through brand prestige, performance, and bespoke features.

- End-User Demographics: Growing affluent millennial and Gen Z consumer base, prioritizing sustainability, technology, and personalized experiences.

- M&A Activities: Strategic acquisitions of technology companies and niche automotive players for competitive advantage.

European Luxury Cars Industry Market Dynamics & Trends

The European luxury car market is experiencing a period of significant transformation, driven by a confluence of powerful market growth drivers and disruptive technological advancements. The overarching trend is the accelerating shift towards electric vehicles (EVs), propelled by both increasingly stringent environmental regulations and a growing consumer demand for sustainable mobility. This transition is not merely about powertrain; it encompasses a radical rethinking of vehicle design, performance, and user experience. Technological disruptions, including the development of advanced battery technologies offering greater range and faster charging, alongside sophisticated infotainment systems and the promise of widespread autonomous driving capabilities, are redefining luxury. Consumer preferences are evolving rapidly; alongside traditional markers of luxury such as brand prestige and craftsmanship, there is a pronounced emphasis on environmental consciousness, digital connectivity, and personalized services. The market penetration of EVs within the luxury segment is steadily increasing, with projections indicating a substantial shift away from internal combustion engines (ICE) over the forecast period. Competitive dynamics are intensifying as established luxury manufacturers vie with new entrants, including technology-focused EV startups. The strategic expansion of charging infrastructure across Europe is a crucial factor supporting this growth. The overall CAGR for the European luxury car market is robust, fueled by these interconnected trends. The increasing integration of advanced driver-assistance systems (ADAS) and the development of premium digital services are further differentiating luxury offerings and enhancing their appeal to a discerning clientele. The base year of 2025 marks a critical inflection point, with electric luxury vehicles poised for significant market share gains.

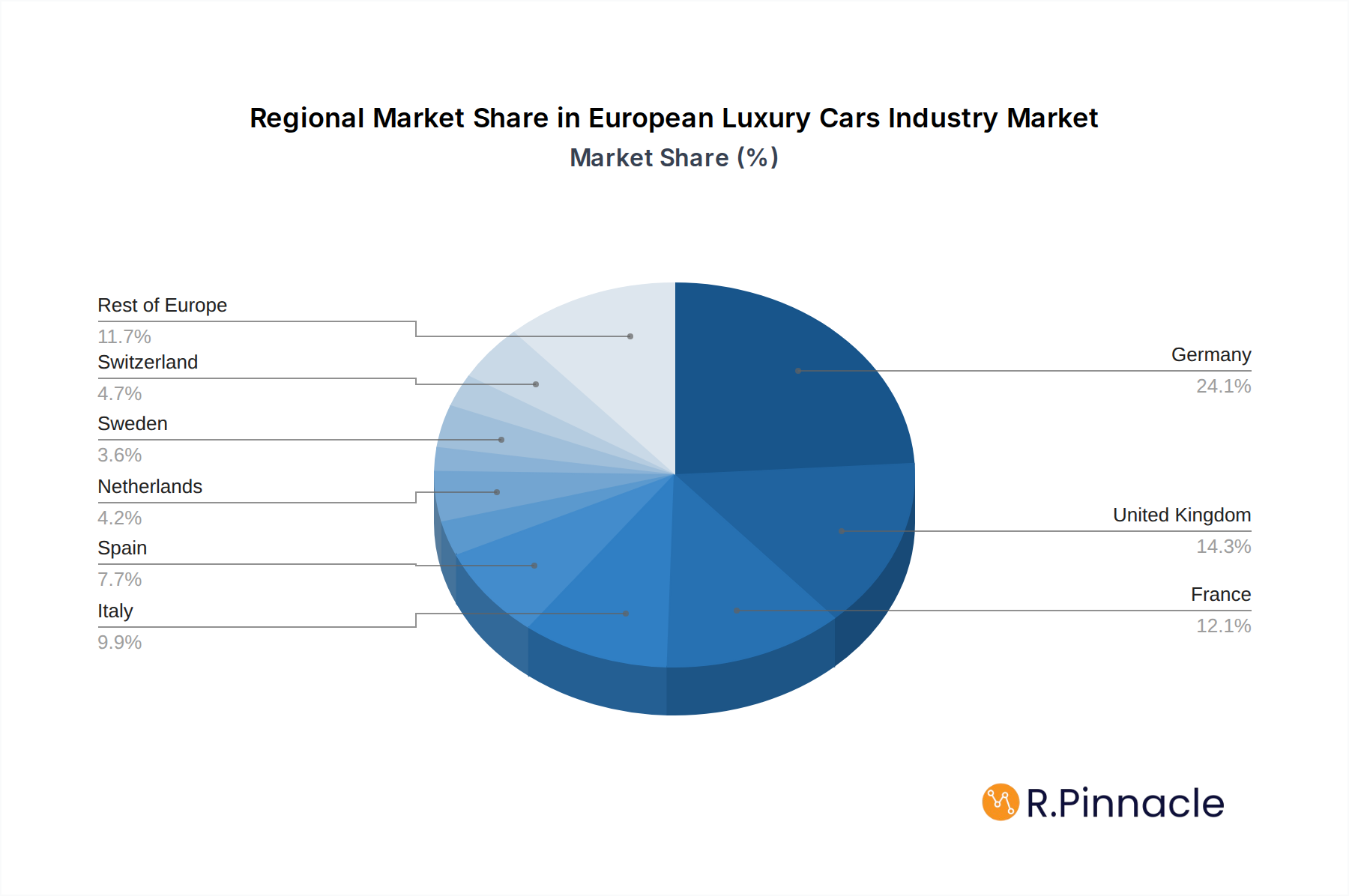

Dominant Regions & Segments in European Luxury Cars Industry

Germany stands as the dominant region within the European luxury car market, a testament to its established automotive manufacturing prowess and the strong presence of leading luxury brands like Mercedes-Benz, BMW, and Audi. Within Germany, metropolitan areas and affluent suburban regions represent the primary demand centers. The United Kingdom and France also represent significant markets, driven by high disposable incomes and a sophisticated consumer base.

- Leading Region: Germany, followed by the United Kingdom and France.

- Key Drivers for Regional Dominance:

- Economic Policies: Favorable economic conditions and high per capita income.

- Infrastructure: Well-developed road networks and a growing charging infrastructure for EVs.

- Consumer Preferences: Strong brand loyalty, demand for performance, and increasing adoption of sustainable technologies.

- Manufacturing Hubs: Presence of major luxury car manufacturers and their extensive supply chains.

In terms of vehicle type, the Sport Utility Vehicle (SUV) segment continues to exhibit remarkable dominance and growth across Europe. Luxury SUVs offer a compelling blend of practicality, elevated driving position, advanced technology, and the perceived safety and status associated with premium brands. Sedans, while historically a strong segment, are seeing their market share steadily challenged by the versatility and appeal of SUVs. Hatchbacks and Multi-purpose Vehicles (MPVs) hold a smaller, more niche position within the luxury segment, often catering to specific functional needs or brand loyalists.

- Dominant Vehicle Type: Sport Utility Vehicle (SUV).

- Key Drivers for SUV Dominance:

- Versatility and Practicality: Appeals to families and individuals seeking a balance of performance and utility.

- Perceived Safety and Comfort: Higher driving position and spacious interiors are highly valued.

- Technological Integration: Luxury SUVs often feature the latest in infotainment, connectivity, and driver assistance systems.

- Brand Image: Premium SUVs project an image of success and capability.

Regarding drive type, the landscape is rapidly bifurcating. While IC Engine vehicles still hold a significant share, the growth trajectory of Electric powertrains is undeniable and accelerating. Regulatory pressures, increasing battery efficiency, and expanding charging infrastructure are making electric luxury cars an increasingly attractive and viable option for consumers. The forecast period, 2025–2033, is expected to witness a significant surge in the market share of electric luxury vehicles, driven by substantial investments in R&D and production capacity by leading manufacturers.

- Dominant Drive Type: Transitioning from IC Engine towards Electric.

- Key Drivers for Electric Drive Dominance:

- Environmental Regulations: EU mandates and national incentives pushing for zero-emission vehicles.

- Technological Advancements: Improved battery range, faster charging times, and enhanced performance of EVs.

- Consumer Demand: Growing environmental awareness and desire for sustainable luxury.

- Government Support: Subsidies, tax breaks, and investment in charging infrastructure.

European Luxury Cars Industry Product Innovations

Product innovations in the European luxury car market are primarily focused on electrifying powertrains, enhancing digital integration, and advancing autonomous driving capabilities. Manufacturers are introducing a wider array of electric and plug-in hybrid models, offering competitive ranges and performance metrics. The integration of sophisticated AI-powered infotainment systems, seamless connectivity features, and over-the-air (OTA) software updates are becoming standard. Advanced driver-assistance systems (ADAS) are evolving towards higher levels of automation, aiming to improve safety and convenience. Bespoke customization options and premium material sourcing continue to be key differentiators, catering to the discerning tastes of luxury consumers. These innovations aim to enhance user experience, reduce environmental impact, and secure competitive advantages in a rapidly evolving market.

Report Scope & Segmentation Analysis

This report analyzes the European luxury cars industry segmented by Vehicle Type: Hatchback, Sedan, Sport Utility Vehicle, and Multi-purpose Vehicle. The Sport Utility Vehicle segment is projected to lead in market size and growth, driven by its broad appeal and versatility. The Sedan segment, while mature, will continue to attract a loyal customer base and see innovation in luxury electric and hybrid variants. The Hatchback segment will focus on premium compact luxury offerings, while the Multi-purpose Vehicle segment will cater to niche demands for ultimate comfort and space.

The industry is also segmented by Drive Type: IC Engine and Electric. While the IC Engine segment will maintain a considerable market share in the near term, the Electric segment is expected to experience exponential growth, driven by regulatory mandates and consumer preference for sustainable mobility. Projections indicate a significant shift towards electric luxury vehicles, with increasing market sizes and competitive dynamics emerging as more manufacturers invest heavily in EV technology and infrastructure.

Key Drivers of European Luxury Cars Industry Growth

The European luxury car industry's growth is propelled by several interconnected factors. Technological advancements, particularly in electrification and autonomous driving, are creating new product possibilities and attracting consumers seeking cutting-edge features. Stringent environmental regulations, while posing challenges, are also a significant catalyst for innovation, pushing manufacturers to develop more sustainable and fuel-efficient vehicles, especially premium electric cars. Rising disposable incomes in key European markets and an increasing demand for premium vehicles that offer superior performance, craftsmanship, and brand prestige are fundamental economic drivers. Furthermore, the growing consumer awareness and preference for environmentally friendly transportation solutions are accelerating the adoption of electric luxury vehicles.

- Technological Advancements: Electrification, AI, connectivity, and autonomous driving features.

- Regulatory Push: Stringent emission standards and incentives for EVs.

- Economic Growth: Increased disposable incomes and demand for premium products.

- Consumer Preferences: Growing demand for sustainability, connectivity, and bespoke experiences.

Challenges in the European Luxury Cars Industry Sector

The European luxury car sector faces significant challenges that could impede its growth trajectory. Supply chain disruptions, particularly concerning semiconductor chips and battery components, have led to production delays and increased costs, impacting vehicle availability. The substantial investment required for the transition to electric vehicles, coupled with the development of necessary charging infrastructure, presents a considerable financial hurdle for manufacturers. Evolving regulatory landscapes, including potentially stricter emission standards and new safety mandates, necessitate continuous adaptation and investment. Furthermore, intense competition from both established premium brands and newer, agile electric vehicle startups demands constant innovation and strategic market positioning. The high cost of luxury vehicles can also limit market penetration, especially during economic downturns.

- Supply Chain Volatility: Shortages of critical components like semiconductors and battery materials.

- High Investment Costs: Transitioning to EV production and developing charging infrastructure.

- Evolving Regulations: Need for continuous adaptation to stricter environmental and safety standards.

- Intense Competition: Pressure from both legacy automakers and new EV players.

- Economic Sensitivity: Luxury segment vulnerability to economic fluctuations and consumer spending power.

Emerging Opportunities in European Luxury Cars Industry

Despite the challenges, the European luxury car market presents numerous emerging opportunities. The rapid expansion of the electric vehicle market offers substantial growth potential for manufacturers who can deliver compelling luxury EVs with superior range and charging capabilities. The increasing demand for connected car services, including advanced infotainment, predictive maintenance, and personalized digital experiences, opens avenues for subscription-based revenue models. The development and integration of semi-autonomous and autonomous driving technologies represent a significant opportunity to differentiate luxury offerings and enhance safety and convenience. Furthermore, the growing emphasis on sustainability is creating opportunities for brands that can effectively communicate their environmental commitment through their products and manufacturing processes. The expansion of charging infrastructure across Europe is also a key enabler for further EV adoption.

- EV Market Expansion: Capitalizing on the growing demand for premium electric vehicles.

- Connected Car Services: Developing and monetizing advanced digital and infotainment features.

- Autonomous Driving Technology: Offering advanced ADAS and semi-autonomous driving capabilities.

- Sustainability Focus: Leveraging eco-friendly manufacturing and materials as a brand differentiator.

- Charging Infrastructure Growth: Benefiting from the expanding network supporting EV adoption.

Leading Players in the European Luxury Cars Industry Market

- Mercedes-Benz Group AG

- BMW AG

- Audi AG

- Bentley Motor

- Rolls-Royce Holding PLC

- Tesla Inc.

- Hyundai Motor Company

- Fiat Chrysler Automobiles

- Ford Motor Company

- AB Volvo

Key Developments in European Luxury Cars Industry Industry

- September 2022: MG Motor launched the MG4 electric in Europe. The MG4 electric features a lithium-ion battery with a capacity of 51 kWh and a range of up to 350 km.

- June 2022: Audi expanded its urban fast-charging hubs in the United Kingdom for luxury EV segments. The company had previously opened a semi-permanent charging site in Nuremberg, Germany, featuring six 320kW fast chargers and a lounge.

- May 2022: Electric car maker Lucid Group announced plans to launch a luxury sedan in Europe at the end of 2022, with the Lucid Air Dream Edition P and R sedans offered in limited numbers to consumers in Germany, Switzerland, Netherlands, and Norway.

- January 2022: European car brand Skoda Auto outlined plans for six new product launches, including an all-new sedan, aiming to triple sales growth.

- November 2021: BMW Group introduced its innovative eDrive Zones in an additional 20 European cities, including Copenhagen, Verona, and Toulouse, bringing the total to 138 cities benefiting from this technology. In eDrive Zones, BMW plug-in hybrid vehicles automatically switch to all-electric driving mode upon entering inner city areas.

Future Outlook for European Luxury Cars Industry Market

The future outlook for the European luxury car market is exceptionally promising, characterized by sustained growth driven by the accelerating transition to electric mobility and continuous technological advancements. The forecast period, 2025–2033, will witness a significant reshaping of the market as electric vehicles (EVs) claim an ever-larger share, fueled by ongoing innovation in battery technology and charging infrastructure expansion. Luxury brands will increasingly focus on delivering enhanced digital experiences, advanced connectivity, and higher levels of autonomous driving capabilities, catering to a discerning clientele that values both performance and sustainability. Strategic partnerships and a focus on personalized services will become crucial for maintaining brand loyalty and expanding market reach. The industry is poised for robust growth, with opportunities abounding for companies that can adapt to evolving consumer preferences and embrace the paradigm shift towards a cleaner, more connected, and technologically sophisticated automotive future.

European Luxury Cars Industry Segmentation

-

1. Vehicle Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sport Utility Vehicle

- 1.4. Multi-purpose Vehicle

-

2. Drive Type

- 2.1. IC Engine

- 2.2. Electric

European Luxury Cars Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Spain

- 5. Italy

- 6. Russia

- 7. Netherlands

- 8. Denmark

- 9. Sweden

- 10. Belgium

- 11. Switzerland

- 12. Rest of Europe

European Luxury Cars Industry Regional Market Share

Geographic Coverage of European Luxury Cars Industry

European Luxury Cars Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sport Utility Vehicle

- 5.1.4. Multi-purpose Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Drive Type

- 5.2.1. IC Engine

- 5.2.2. Electric

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Spain

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Netherlands

- 5.3.8. Denmark

- 5.3.9. Sweden

- 5.3.10. Belgium

- 5.3.11. Switzerland

- 5.3.12. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. European Luxury Cars Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Hatchback

- 6.1.2. Sedan

- 6.1.3. Sport Utility Vehicle

- 6.1.4. Multi-purpose Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Drive Type

- 6.2.1. IC Engine

- 6.2.2. Electric

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Germany European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Hatchback

- 7.1.2. Sedan

- 7.1.3. Sport Utility Vehicle

- 7.1.4. Multi-purpose Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Drive Type

- 7.2.1. IC Engine

- 7.2.2. Electric

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. United Kingdom European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Hatchback

- 8.1.2. Sedan

- 8.1.3. Sport Utility Vehicle

- 8.1.4. Multi-purpose Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Drive Type

- 8.2.1. IC Engine

- 8.2.2. Electric

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. France European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Hatchback

- 9.1.2. Sedan

- 9.1.3. Sport Utility Vehicle

- 9.1.4. Multi-purpose Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Drive Type

- 9.2.1. IC Engine

- 9.2.2. Electric

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Spain European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Hatchback

- 10.1.2. Sedan

- 10.1.3. Sport Utility Vehicle

- 10.1.4. Multi-purpose Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Drive Type

- 10.2.1. IC Engine

- 10.2.2. Electric

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Italy European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.1.1. Hatchback

- 11.1.2. Sedan

- 11.1.3. Sport Utility Vehicle

- 11.1.4. Multi-purpose Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Drive Type

- 11.2.1. IC Engine

- 11.2.2. Electric

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12. Russia European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 12.1.1. Hatchback

- 12.1.2. Sedan

- 12.1.3. Sport Utility Vehicle

- 12.1.4. Multi-purpose Vehicle

- 12.2. Market Analysis, Insights and Forecast - by Drive Type

- 12.2.1. IC Engine

- 12.2.2. Electric

- 12.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 13. Netherlands European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 13.1.1. Hatchback

- 13.1.2. Sedan

- 13.1.3. Sport Utility Vehicle

- 13.1.4. Multi-purpose Vehicle

- 13.2. Market Analysis, Insights and Forecast - by Drive Type

- 13.2.1. IC Engine

- 13.2.2. Electric

- 13.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 14. Denmark European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 14.1.1. Hatchback

- 14.1.2. Sedan

- 14.1.3. Sport Utility Vehicle

- 14.1.4. Multi-purpose Vehicle

- 14.2. Market Analysis, Insights and Forecast - by Drive Type

- 14.2.1. IC Engine

- 14.2.2. Electric

- 14.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 15. Sweden European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 15.1.1. Hatchback

- 15.1.2. Sedan

- 15.1.3. Sport Utility Vehicle

- 15.1.4. Multi-purpose Vehicle

- 15.2. Market Analysis, Insights and Forecast - by Drive Type

- 15.2.1. IC Engine

- 15.2.2. Electric

- 15.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 16. Belgium European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 16.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 16.1.1. Hatchback

- 16.1.2. Sedan

- 16.1.3. Sport Utility Vehicle

- 16.1.4. Multi-purpose Vehicle

- 16.2. Market Analysis, Insights and Forecast - by Drive Type

- 16.2.1. IC Engine

- 16.2.2. Electric

- 16.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 17. Switzerland European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 17.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 17.1.1. Hatchback

- 17.1.2. Sedan

- 17.1.3. Sport Utility Vehicle

- 17.1.4. Multi-purpose Vehicle

- 17.2. Market Analysis, Insights and Forecast - by Drive Type

- 17.2.1. IC Engine

- 17.2.2. Electric

- 17.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 18. Rest of Europe European Luxury Cars Industry Analysis, Insights and Forecast, 2020-2032

- 18.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 18.1.1. Hatchback

- 18.1.2. Sedan

- 18.1.3. Sport Utility Vehicle

- 18.1.4. Multi-purpose Vehicle

- 18.2. Market Analysis, Insights and Forecast - by Drive Type

- 18.2.1. IC Engine

- 18.2.2. Electric

- 18.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 19. Competitive Analysis

- 19.1. Company Profiles

- 19.1.1 Meredes-Benz Group AG

- 19.1.1.1. Company Overview

- 19.1.1.2. Products

- 19.1.1.3. Company Financials

- 19.1.1.4. SWOT Analysis

- 19.1.2 Hyundai Motor Company

- 19.1.2.1. Company Overview

- 19.1.2.2. Products

- 19.1.2.3. Company Financials

- 19.1.2.4. SWOT Analysis

- 19.1.3 Fiat Chrysler Automobiles

- 19.1.3.1. Company Overview

- 19.1.3.2. Products

- 19.1.3.3. Company Financials

- 19.1.3.4. SWOT Analysis

- 19.1.4 BMW AG

- 19.1.4.1. Company Overview

- 19.1.4.2. Products

- 19.1.4.3. Company Financials

- 19.1.4.4. SWOT Analysis

- 19.1.5 Bentley Motor

- 19.1.5.1. Company Overview

- 19.1.5.2. Products

- 19.1.5.3. Company Financials

- 19.1.5.4. SWOT Analysis

- 19.1.6 Tesla Inc

- 19.1.6.1. Company Overview

- 19.1.6.2. Products

- 19.1.6.3. Company Financials

- 19.1.6.4. SWOT Analysis

- 19.1.7 Audi AG

- 19.1.7.1. Company Overview

- 19.1.7.2. Products

- 19.1.7.3. Company Financials

- 19.1.7.4. SWOT Analysis

- 19.1.8 AB Volvo

- 19.1.8.1. Company Overview

- 19.1.8.2. Products

- 19.1.8.3. Company Financials

- 19.1.8.4. SWOT Analysis

- 19.1.9 Ford Motor Company

- 19.1.9.1. Company Overview

- 19.1.9.2. Products

- 19.1.9.3. Company Financials

- 19.1.9.4. SWOT Analysis

- 19.1.10 Rolls-Royce Holding PLC

- 19.1.10.1. Company Overview

- 19.1.10.2. Products

- 19.1.10.3. Company Financials

- 19.1.10.4. SWOT Analysis

- 19.1.1 Meredes-Benz Group AG

- 19.2. Market Entropy

- 19.2.1 Company's Key Areas Served

- 19.2.2 Recent Developments

- 19.3. Company Market Share Analysis 2025

- 19.3.1 Top 5 Companies Market Share Analysis

- 19.3.2 Top 3 Companies Market Share Analysis

- 19.4. List of Potential Customers

- 20. Research Methodology

List of Figures

- Figure 1: European Luxury Cars Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Luxury Cars Industry Share (%) by Company 2025

List of Tables

- Table 1: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 3: European Luxury Cars Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 6: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 8: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 9: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 11: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 12: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 14: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 15: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 17: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 18: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 20: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 21: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 23: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 24: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 26: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 27: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 29: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 30: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 32: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 33: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 35: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 36: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: European Luxury Cars Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 38: European Luxury Cars Industry Revenue billion Forecast, by Drive Type 2020 & 2033

- Table 39: European Luxury Cars Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Luxury Cars Industry?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the European Luxury Cars Industry?

Key companies in the market include Meredes-Benz Group AG, Hyundai Motor Company, Fiat Chrysler Automobiles, BMW AG, Bentley Motor, Tesla Inc, Audi AG, AB Volvo, Ford Motor Company, Rolls-Royce Holding PLC.

3. What are the main segments of the European Luxury Cars Industry?

The market segments include Vehicle Type, Drive Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 741.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Economy And Infrastructural Growth.

6. What are the notable trends driving market growth?

SUVs are anticipated to witness higher growth in the European Luxury Car Market.

7. Are there any restraints impacting market growth?

High Cost of Electric Commercial Vehicle May Hamper the Growth.

8. Can you provide examples of recent developments in the market?

Sept 2022: MG Motor launched MG4 electric in Europe. MG4 electric consists of a lithium-ion battery with a battery capacity of 51 kWh and a range of up to 350 km range.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Luxury Cars Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Luxury Cars Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Luxury Cars Industry?

To stay informed about further developments, trends, and reports in the European Luxury Cars Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence