Key Insights

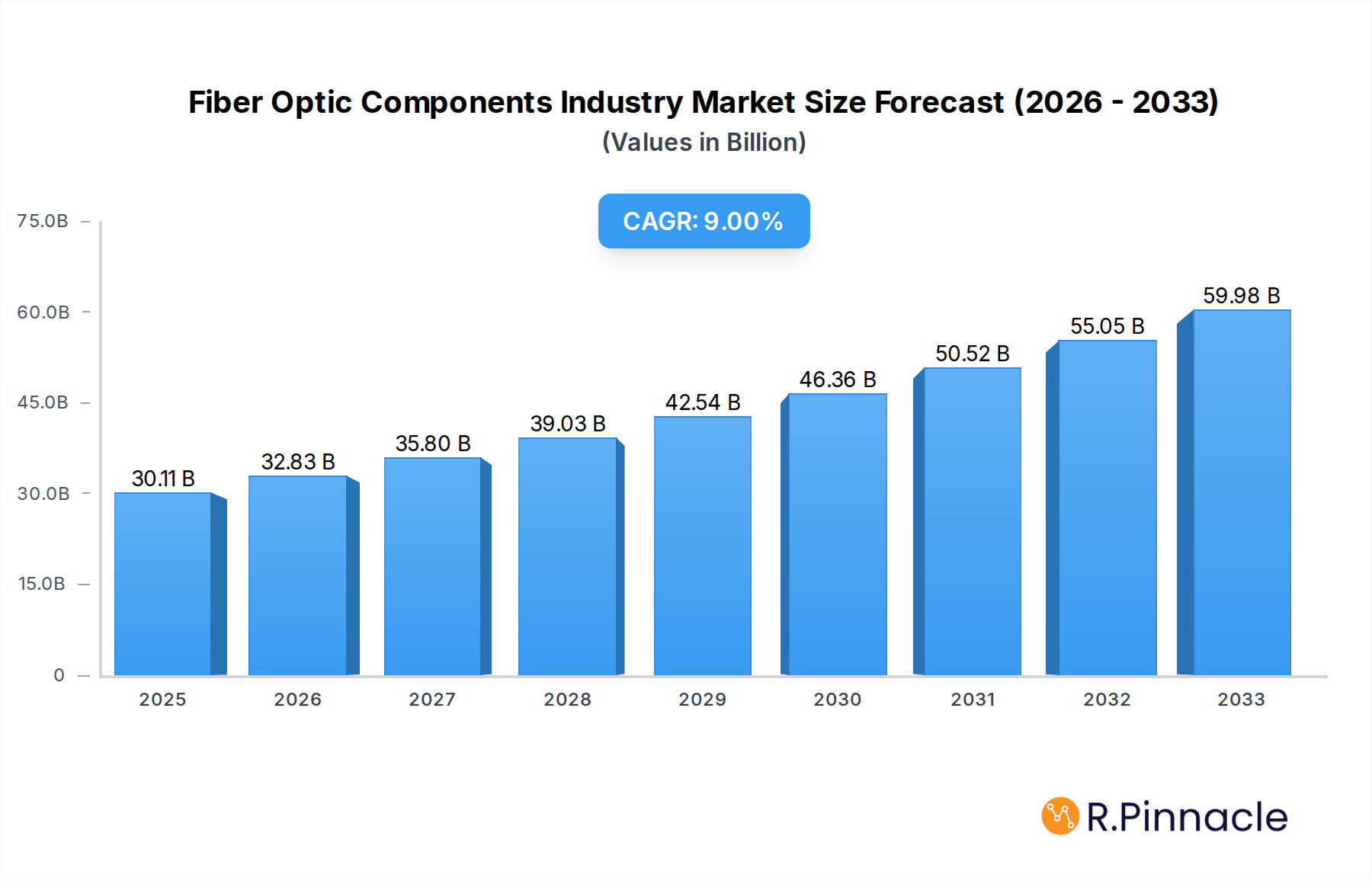

The global Fiber Optic Components Industry is experiencing robust expansion, projected to reach an estimated market size of $30.11 billion in 2025. This growth is fueled by an impressive Compound Annual Growth Rate (CAGR) of 9.3% over the forecast period. A primary driver for this surge is the ever-increasing demand for high-speed data transmission across various sectors, including telecommunications, data centers, and the expanding landscape of 5G deployment. The proliferation of connected devices, the burgeoning adoption of cloud computing, and the critical need for reliable and efficient communication infrastructure are all contributing to this upward trajectory. Furthermore, the analytical and medical equipment sectors, which increasingly rely on precise optical sensing and data transfer, are also playing a significant role in market expansion. Innovations in optical technology, leading to more sophisticated and cost-effective components like advanced transceivers and active optical cables, are further stimulating market penetration and adoption.

Fiber Optic Components Industry Market Size (In Billion)

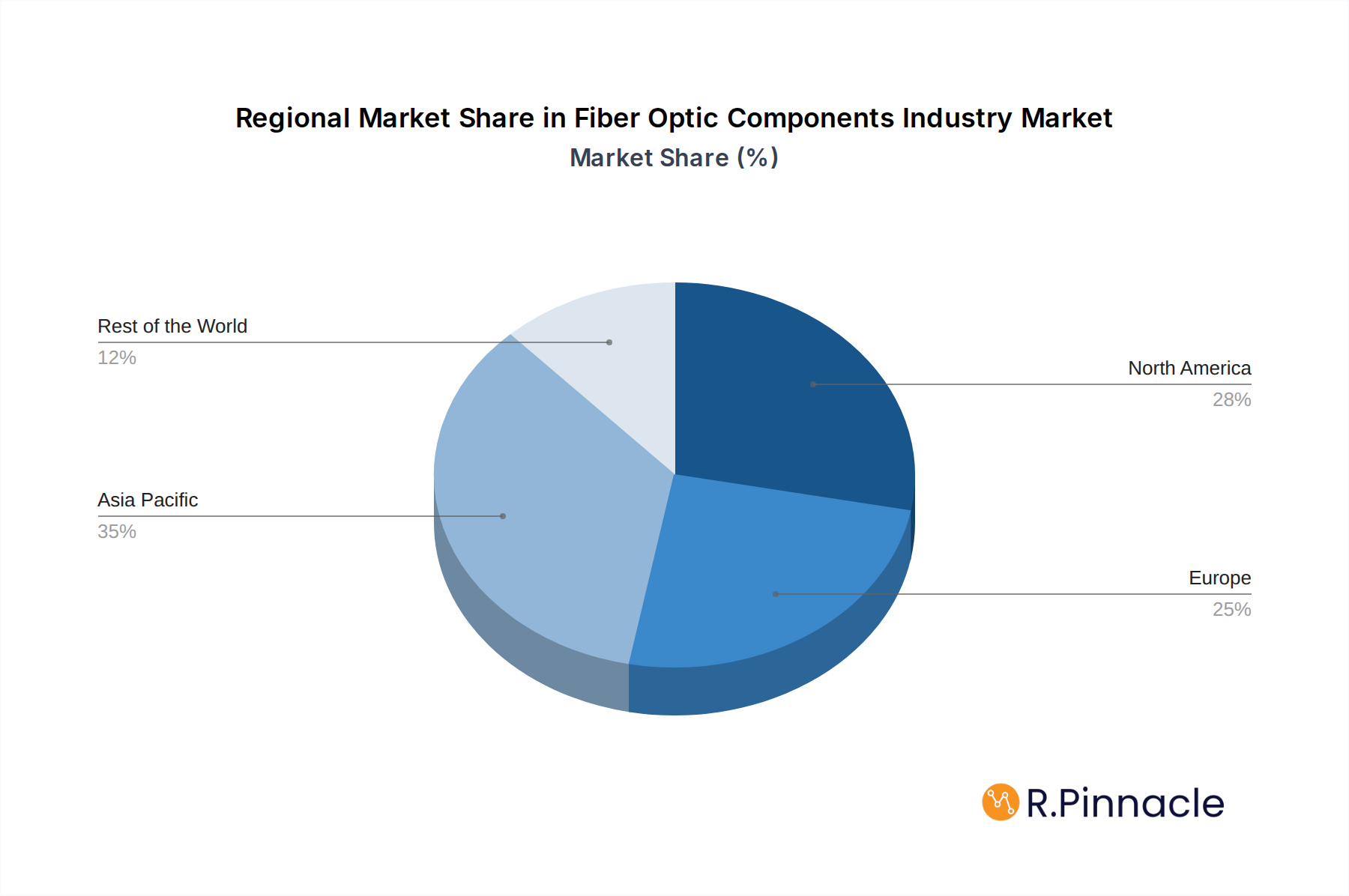

The market is characterized by a dynamic competitive landscape, with leading companies such as Broadcom Corporation, II-VI Incorporated, and Lumentum Operations LLC at the forefront of innovation and production. These players are continually investing in research and development to enhance component performance, reduce latency, and cater to the evolving demands of a data-intensive world. While the growth is substantial, potential restraints such as fluctuating raw material costs and the need for continuous infrastructure upgrades could present challenges. However, the persistent global push for enhanced connectivity, the increasing integration of fiber optics in emerging technologies like the Internet of Things (IoT) and Artificial Intelligence (AI), and the continuous development of specialized applications like distributed sensing are expected to outweigh these limitations. Geographically, Asia Pacific, led by China and Japan, is anticipated to be a major growth hub, driven by significant investments in digital infrastructure and manufacturing capabilities, while North America and Europe remain established markets with substantial ongoing demand.

Fiber Optic Components Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global Fiber Optic Components industry, providing critical insights into market structure, dynamics, key players, and future trends. With a study period spanning from 2019 to 2033 and a base year of 2025, this report is an essential resource for understanding the billion-dollar market landscape, driven by relentless innovation and expanding applications.

Fiber Optic Components Industry Market Structure & Innovation Trends

The global Fiber Optic Components market exhibits a moderately concentrated structure, with key players investing heavily in research and development to maintain their competitive edge. Innovation drivers are primarily fueled by the escalating demand for higher bandwidth, faster data transmission speeds, and the burgeoning adoption of 5G networks and data centers. Regulatory frameworks, particularly those promoting digital infrastructure development and standardization, play a crucial role in shaping market growth. While product substitutes exist in some niche applications, the superior performance of fiber optics in terms of speed, capacity, and reliability limits their widespread impact. End-user demographics are increasingly diverse, encompassing telecommunications providers, enterprise networks, cloud service providers, and industries leveraging advanced sensing and medical technologies. Mergers and acquisitions (M&A) activity has been a significant factor in market consolidation and strategic expansion, with deal values in the billions as companies seek to enhance their product portfolios and market reach. For instance, the estimated M&A deal value in the last five years has reached approximately $XX billion.

Fiber Optic Components Industry Market Dynamics & Trends

The Fiber Optic Components industry is poised for substantial expansion, projected to witness a Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033. This robust growth is propelled by several interconnected market dynamics. The relentless expansion of global data traffic, driven by video streaming, cloud computing, IoT devices, and the proliferation of digital services, necessitates a corresponding increase in network capacity, directly benefiting the demand for fiber optic components. The ongoing rollout of 5G infrastructure worldwide is a paramount growth accelerator, requiring high-performance fiber optic cables and transceivers for base stations and core networks. Furthermore, the massive expansion of hyperscale data centers and enterprise networks, catering to the ever-increasing data storage and processing needs, is a significant contributor to market penetration. Technological disruptions, such as advancements in optical sensing technologies for industrial automation and healthcare, are opening up new application avenues. Consumer preferences for seamless, high-speed connectivity across all devices and services are indirectly fueling the demand for better underlying infrastructure. The competitive landscape is characterized by intense innovation and strategic partnerships, with companies striving to offer cost-effective, high-performance solutions to meet evolving market demands. The market penetration of advanced fiber optic solutions is expected to reach XX% by the end of the forecast period.

Dominant Regions & Segments in Fiber Optic Components Industry

North America, particularly the United States, is a dominant region in the Fiber Optic Components industry, driven by its early adoption of advanced telecommunications infrastructure, a robust data center ecosystem, and significant investments in 5G deployment. The region's economic policies favor technological innovation and infrastructure development, further solidifying its leadership. Asia-Pacific, led by China, is experiencing rapid growth and is a significant contributor to the global market share, fueled by massive investments in 5G networks, extensive fiber-to-the-home (FTTH) initiatives, and a strong manufacturing base for optical components.

Key Segment Dominance:

Type:

- Transceivers: This segment is a major growth engine, driven by the insatiable demand for high-speed data transmission in data centers, telecommunications networks, and enterprise applications. The increasing adoption of 100GbE, 400GbE, and upcoming 800GbE technologies is a primary driver.

- Cables: The backbone of any fiber optic network, optical cables, particularly single-mode and multi-mode fiber, continue to see robust demand due to network expansion and upgrades.

- Active Optical Cables (AOCs): These are gaining traction for their ease of use and cost-effectiveness in short-reach data center interconnects.

Application:

- Communications: This is the largest application segment, encompassing telecommunications (mobile, broadband) and enterprise networking. The ongoing upgrades to higher bandwidth and the expansion of 5G are critical.

- Distributed Sensing: This segment is witnessing significant growth, with fiber optics being increasingly utilized in infrastructure monitoring (bridges, pipelines), environmental sensing, and industrial safety systems due to their precision and durability.

- Analytical and Medical Equipment: The precision and high data transfer capabilities of fiber optics are crucial for advanced medical imaging, diagnostics, and laboratory instrumentation.

The dominance of these segments is reinforced by ongoing technological advancements, substantial R&D investments, and supportive government initiatives aimed at enhancing digital connectivity and advancing specialized applications.

Fiber Optic Components Industry Product Innovations

Recent product innovations in the Fiber Optic Components industry are centered around enhancing speed, efficiency, and miniaturization. This includes the development of next-generation pluggable transceivers supporting higher data rates like 800Gbps and beyond, crucial for the evolving demands of hyperscale data centers. Advancements in optical amplifier technologies are enabling longer transmission distances with reduced signal loss. Innovations in connector design are focused on improving reliability and ease of installation. The integration of advanced materials and manufacturing techniques is leading to more cost-effective and higher-performance components, giving companies a competitive advantage in key markets like 5G and AI infrastructure.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Fiber Optic Components market across various segmentations to provide granular insights.

- Type Segmentation: The report covers Cables, Amplifiers, Active Optical Cables, Splitters, Connectors, Transceivers, and Other Types. Each segment's market size, growth projections, and competitive dynamics are detailed. For example, the Transceivers segment is projected to reach $XX billion by 2033, driven by the demand for higher data rates in communications.

- Application Segmentation: The analysis encompasses Distributed Sensing, Communications, Analytical and Medical Equipment, and Lighting. The Communications segment, expected to dominate with a market size of $XX billion in 2025, is further scrutinized for its sub-segments and growth drivers.

Key Drivers of Fiber Optic Components Industry Growth

The growth of the Fiber Optic Components industry is primarily driven by the exponential increase in global data traffic, necessitating higher bandwidth and faster transmission speeds. The widespread deployment of 5G networks and the expansion of hyperscale data centers are significant accelerators. Technological advancements in areas like Coherent Optics and advanced optical amplifiers are enabling more efficient and longer-distance data transmission. Government initiatives promoting digital infrastructure development and increased investments in telecommunications are also crucial economic drivers. Furthermore, the growing adoption of fiber optic sensors in industrial automation, healthcare, and infrastructure monitoring applications is opening up new avenues for market expansion.

Challenges in the Fiber Optic Components Industry Sector

Despite robust growth, the Fiber Optic Components industry faces several challenges. High upfront investment costs associated with deploying fiber optic infrastructure can be a barrier, particularly in emerging economies. Intense competition among manufacturers leads to price pressures, impacting profit margins. Supply chain disruptions, as evidenced by recent global events, can affect the availability of raw materials and finished components, leading to production delays and increased costs. The rapid pace of technological advancement requires continuous R&D investment, which can be a significant financial burden for smaller players. Furthermore, regulatory complexities and standardization challenges in certain regions can slow down market adoption. The estimated impact of these challenges on market growth is approximately XX%.

Emerging Opportunities in Fiber Optic Components Industry

Emerging opportunities in the Fiber Optic Components industry are abundant, driven by ongoing technological evolution and expanding market needs. The increasing demand for high-speed connectivity for AI and machine learning applications presents a significant opportunity. The continued growth of the Internet of Things (IoT) and edge computing will necessitate more localized and distributed fiber optic networks. Advancements in optical computing and quantum communication, though nascent, represent potential future growth areas. The expanding use of fiber optic sensing in smart cities, renewable energy infrastructure, and advanced manufacturing provides niche but growing market segments. Furthermore, the ongoing upgrades of existing networks and the expansion into underserved regions offer substantial untapped potential.

Leading Players in the Fiber Optic Components Industry Market

- Broadcom Corporation

- II-VI Incorporated

- Source Photonics Inc

- Mwtechnologies LDA

- OptiEnz Sensors LLC

- Furukawa Electric Co Ltd

- Acacia Communications Inc

- Reflex Photonics Inc

- NeoPhotonics Corporation

- Fiber Mountain Inc

- Lumentum Operations LLC

- Shenzhen Nokoxin Technology Co Ltd

- O-Net Tech Group

- Accelink Technologies Corporation

- EMCORE Corporation

- Oclaro Inc

- Sumitomo Electric Industries Ltd

- Fujitsu Optical Components Limited

Key Developments in Fiber Optic Components Industry Industry

- 2024: Launch of new 800Gbps QSFP-DD optical transceivers by leading players to support next-generation data center architectures.

- 2023: Significant M&A activity as companies consolidate to expand product portfolios and market reach in the high-speed networking segment.

- 2022: Increased investment in R&D for Coherent Optical technologies to enable longer-reach and higher-capacity optical networks.

- 2021: Growing adoption of Active Optical Cables (AOCs) for cost-effective short-reach connectivity in data centers.

- 2020: Accelerated deployment of fiber optic infrastructure for 5G network rollouts across major global markets.

- 2019: Advancements in optical amplifier technology leading to improved signal integrity and extended reach in long-haul networks.

Future Outlook for Fiber Optic Components Industry Market

The future outlook for the Fiber Optic Components industry is exceptionally bright, driven by an accelerating demand for ubiquitous, high-speed data connectivity. The continued expansion of 5G, the massive growth of AI and machine learning workloads, and the proliferation of IoT devices will relentlessly drive the need for advanced fiber optic solutions. The increasing focus on digital transformation across all sectors, from healthcare to manufacturing, will further fuel market growth. Innovations in areas like silicon photonics and advanced packaging will lead to more integrated and cost-effective components. Strategic partnerships and continued M&A activity will shape a dynamic competitive landscape. The market is expected to witness sustained double-digit growth, creating significant opportunities for innovation and investment in the coming years.

Fiber Optic Components Industry Segmentation

-

1. Type**

- 1.1. Cables

- 1.2. Amplifiers

- 1.3. Active Optical Cables

- 1.4. Splitters

- 1.5. Connectors

- 1.6. Transceivers

- 1.7. Other Types

-

2. Application

- 2.1. Distributed Sensing

- 2.2. Communications

- 2.3. Analytical and Medical Equipment

- 2.4. Lighting

Fiber Optic Components Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

- 4. Rest of the World

Fiber Optic Components Industry Regional Market Share

Geographic Coverage of Fiber Optic Components Industry

Fiber Optic Components Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type**

- 5.1.1. Cables

- 5.1.2. Amplifiers

- 5.1.3. Active Optical Cables

- 5.1.4. Splitters

- 5.1.5. Connectors

- 5.1.6. Transceivers

- 5.1.7. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Distributed Sensing

- 5.2.2. Communications

- 5.2.3. Analytical and Medical Equipment

- 5.2.4. Lighting

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type**

- 6. Global Fiber Optic Components Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type**

- 6.1.1. Cables

- 6.1.2. Amplifiers

- 6.1.3. Active Optical Cables

- 6.1.4. Splitters

- 6.1.5. Connectors

- 6.1.6. Transceivers

- 6.1.7. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Distributed Sensing

- 6.2.2. Communications

- 6.2.3. Analytical and Medical Equipment

- 6.2.4. Lighting

- 6.1. Market Analysis, Insights and Forecast - by Type**

- 7. North America Fiber Optic Components Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type**

- 7.1.1. Cables

- 7.1.2. Amplifiers

- 7.1.3. Active Optical Cables

- 7.1.4. Splitters

- 7.1.5. Connectors

- 7.1.6. Transceivers

- 7.1.7. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Distributed Sensing

- 7.2.2. Communications

- 7.2.3. Analytical and Medical Equipment

- 7.2.4. Lighting

- 7.1. Market Analysis, Insights and Forecast - by Type**

- 8. Europe Fiber Optic Components Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type**

- 8.1.1. Cables

- 8.1.2. Amplifiers

- 8.1.3. Active Optical Cables

- 8.1.4. Splitters

- 8.1.5. Connectors

- 8.1.6. Transceivers

- 8.1.7. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Distributed Sensing

- 8.2.2. Communications

- 8.2.3. Analytical and Medical Equipment

- 8.2.4. Lighting

- 8.1. Market Analysis, Insights and Forecast - by Type**

- 9. Asia Pacific Fiber Optic Components Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type**

- 9.1.1. Cables

- 9.1.2. Amplifiers

- 9.1.3. Active Optical Cables

- 9.1.4. Splitters

- 9.1.5. Connectors

- 9.1.6. Transceivers

- 9.1.7. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Distributed Sensing

- 9.2.2. Communications

- 9.2.3. Analytical and Medical Equipment

- 9.2.4. Lighting

- 9.1. Market Analysis, Insights and Forecast - by Type**

- 10. Rest of the World Fiber Optic Components Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type**

- 10.1.1. Cables

- 10.1.2. Amplifiers

- 10.1.3. Active Optical Cables

- 10.1.4. Splitters

- 10.1.5. Connectors

- 10.1.6. Transceivers

- 10.1.7. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Distributed Sensing

- 10.2.2. Communications

- 10.2.3. Analytical and Medical Equipment

- 10.2.4. Lighting

- 10.1. Market Analysis, Insights and Forecast - by Type**

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Broadcom Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 II-VI Incorporated

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Source Photonics Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Mwtechnologies LDA

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 OptiEnz Sensors LLC

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Furukawa Electric Co Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Acacia Communications Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Reflex Photonics Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 NeoPhotonics Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Fiber Mountain Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Lumentum Operations LLC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Shenzhen Nokoxin Technology Co Ltd

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 O-Net Tech Group

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Accelink Technologies Corporation

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 EMCORE Corporation

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.16 Oclaro Inc

- 11.1.16.1. Company Overview

- 11.1.16.2. Products

- 11.1.16.3. Company Financials

- 11.1.16.4. SWOT Analysis

- 11.1.17 Sumitomo Electric Industries Ltd

- 11.1.17.1. Company Overview

- 11.1.17.2. Products

- 11.1.17.3. Company Financials

- 11.1.17.4. SWOT Analysis

- 11.1.18 Fujitsu Optical Components Limited

- 11.1.18.1. Company Overview

- 11.1.18.2. Products

- 11.1.18.3. Company Financials

- 11.1.18.4. SWOT Analysis

- 11.1.1 Broadcom Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Fiber Optic Components Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fiber Optic Components Industry Revenue (billion), by Type** 2025 & 2033

- Figure 3: North America Fiber Optic Components Industry Revenue Share (%), by Type** 2025 & 2033

- Figure 4: North America Fiber Optic Components Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Fiber Optic Components Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Fiber Optic Components Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fiber Optic Components Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Fiber Optic Components Industry Revenue (billion), by Type** 2025 & 2033

- Figure 9: Europe Fiber Optic Components Industry Revenue Share (%), by Type** 2025 & 2033

- Figure 10: Europe Fiber Optic Components Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe Fiber Optic Components Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Fiber Optic Components Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Fiber Optic Components Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Fiber Optic Components Industry Revenue (billion), by Type** 2025 & 2033

- Figure 15: Asia Pacific Fiber Optic Components Industry Revenue Share (%), by Type** 2025 & 2033

- Figure 16: Asia Pacific Fiber Optic Components Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Asia Pacific Fiber Optic Components Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Fiber Optic Components Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Fiber Optic Components Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Fiber Optic Components Industry Revenue (billion), by Type** 2025 & 2033

- Figure 21: Rest of the World Fiber Optic Components Industry Revenue Share (%), by Type** 2025 & 2033

- Figure 22: Rest of the World Fiber Optic Components Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Rest of the World Fiber Optic Components Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Rest of the World Fiber Optic Components Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Fiber Optic Components Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fiber Optic Components Industry Revenue billion Forecast, by Type** 2020 & 2033

- Table 2: Global Fiber Optic Components Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Fiber Optic Components Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fiber Optic Components Industry Revenue billion Forecast, by Type** 2020 & 2033

- Table 5: Global Fiber Optic Components Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Fiber Optic Components Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Fiber Optic Components Industry Revenue billion Forecast, by Type** 2020 & 2033

- Table 10: Global Fiber Optic Components Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fiber Optic Components Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Germany Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fiber Optic Components Industry Revenue billion Forecast, by Type** 2020 & 2033

- Table 17: Global Fiber Optic Components Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global Fiber Optic Components Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: China Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Japan Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: India Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Fiber Optic Components Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global Fiber Optic Components Industry Revenue billion Forecast, by Type** 2020 & 2033

- Table 24: Global Fiber Optic Components Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Fiber Optic Components Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fiber Optic Components Industry?

The projected CAGR is approximately 9.3%.

2. Which companies are prominent players in the Fiber Optic Components Industry?

Key companies in the market include Broadcom Corporation, II-VI Incorporated, Source Photonics Inc, Mwtechnologies LDA, OptiEnz Sensors LLC, Furukawa Electric Co Ltd, Acacia Communications Inc, Reflex Photonics Inc, NeoPhotonics Corporation, Fiber Mountain Inc, Lumentum Operations LLC, Shenzhen Nokoxin Technology Co Ltd, O-Net Tech Group, Accelink Technologies Corporation, EMCORE Corporation, Oclaro Inc, Sumitomo Electric Industries Ltd, Fujitsu Optical Components Limited.

3. What are the main segments of the Fiber Optic Components Industry?

The market segments include Type**, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.11 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Deployment of Data Centers; Increasing Internet Penetration and Data Traffic; Intensifying Demand for Bandwidth and Reliability.

6. What are the notable trends driving market growth?

Fiber Optic Cables to Dominate the Market.

7. Are there any restraints impacting market growth?

Complexity in System Design and Function.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fiber Optic Components Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fiber Optic Components Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fiber Optic Components Industry?

To stay informed about further developments, trends, and reports in the Fiber Optic Components Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence