Key Insights

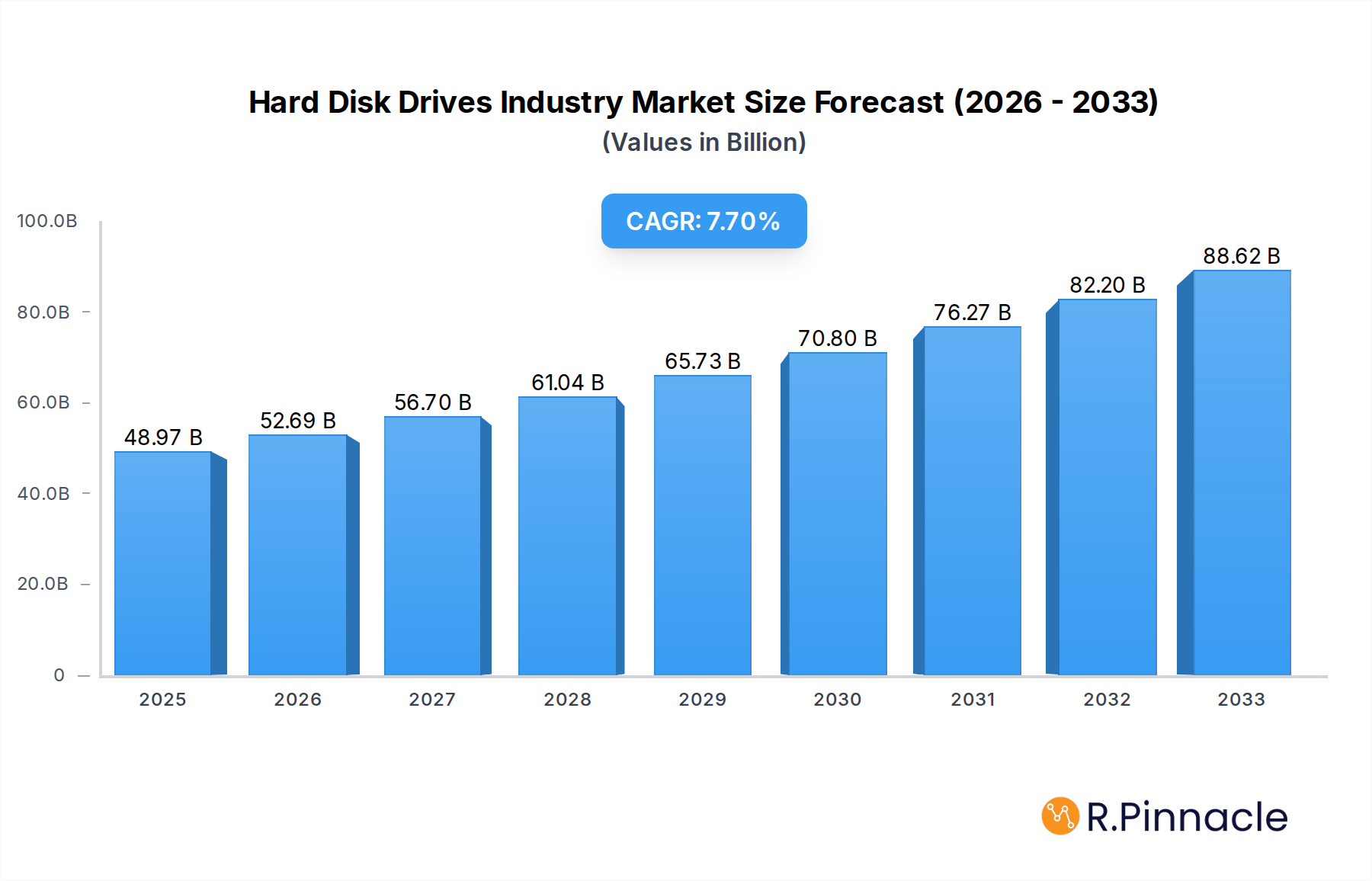

The Hard Disk Drives (HDD) industry is poised for robust growth, with a projected market size of $48.97 billion in 2025, expanding at a Compound Annual Growth Rate (CAGR) of 7.6% through 2033. This sustained expansion is driven by the escalating demand for high-capacity storage solutions across a multitude of applications. The proliferation of data generated by cloud computing, big data analytics, the Internet of Things (IoT), and the ever-increasing content consumption in mobile and consumer electronics segments are primary growth accelerators. Furthermore, enterprise demand for reliable and cost-effective storage for data centers and nearline applications continues to be a significant pillar of market strength. Despite the rise of Solid State Drives (SSDs), HDDs maintain a competitive edge in cost-per-gigabyte for bulk storage, ensuring their continued relevance, particularly in large-scale data archiving and backup scenarios.

Hard Disk Drives Industry Market Size (In Billion)

Key trends shaping the HDD market include advancements in perpendicular magnetic recording (PMR) and shingled magnetic recording (SMR) technologies, enabling higher areal densities and thus increased storage capacities within form factors like 2.5-inch and 3.5-inch drives. The market segmentation by application reveals a dynamic landscape, with significant contributions from mobile, consumer electronics, desktop computers, and the critical enterprise and nearline sectors. Geographically, North America, particularly the United States, and the Asia-Pacific region, led by China and Taiwan, are expected to be major consumption hubs due to their strong technology sectors and massive data generation. While the growth trajectory is impressive, challenges such as intense price competition and the continued adoption of alternative storage technologies like SSDs present some restraints. However, strategic innovations in drive technology and optimized supply chain management by key players such as Western Digital, Seagate, and Toshiba Corporation are expected to navigate these challenges and sustain the industry's upward momentum.

Hard Disk Drives Industry Company Market Share

This in-depth report provides a detailed analysis of the global Hard Disk Drives (HDD) industry, covering market structure, dynamics, regional dominance, product innovations, and future projections from 2019 to 2033. Leveraging high-ranking keywords such as "HDD market share," "data storage solutions," "enterprise HDDs," and "consumer electronics storage," this report aims to boost search visibility and provide actionable insights for industry professionals, investors, and stakeholders.

Hard Disk Drives Industry Market Structure & Innovation Trends

The Hard Disk Drives (HDD) market exhibits a moderately concentrated structure, dominated by a few key players who continuously drive innovation. The primary innovation drivers include the relentless demand for higher storage capacities, improved performance metrics (seek times, transfer speeds), and enhanced reliability, especially for enterprise-grade applications. Regulatory frameworks, while not overtly restrictive for HDD development, focus on energy efficiency and data security standards, influencing product design. Potential product substitutes, primarily Solid State Drives (SSDs), offer speed advantages but often at a higher cost per terabyte, maintaining HDDs' relevance for bulk storage. End-user demographics span from individual consumers seeking affordable storage for media to large enterprises requiring petabytes of data archiving and active storage. Mergers and acquisitions (M&A) have shaped the market landscape, with strategic consolidation aimed at increasing market share and expanding technological capabilities. For instance, past M&A activities have seen significant deal values in the billions, consolidating research and development efforts. The overall market share distribution is dynamic, with companies like Seagate and Western Digital holding substantial portions.

- Market Concentration: Moderately concentrated, with a few major players dominating.

- Innovation Drivers: Increased capacity, enhanced performance, improved reliability, cost-effectiveness.

- Regulatory Impact: Focus on energy efficiency and data security standards.

- Product Substitutes: Solid State Drives (SSDs) for speed, but HDDs remain cost-effective for bulk storage.

- End-User Segments: Consumer, SMB, Enterprise, Cloud/Data Centers.

- M&A Activities: Strategic consolidations to gain market share and R&D synergies. Estimated M&A deal values in billions.

Hard Disk Drives Industry Market Dynamics & Trends

The Hard Disk Drives (HDD) industry is undergoing a dynamic evolution, driven by a confluence of factors that are reshaping its growth trajectory. The overarching market growth is propelled by the exponential increase in data generation across all sectors, from the burgeoning Internet of Things (IoT) devices to the ever-expanding digital media consumption by consumers and the massive data lakes required by enterprises for analytics and AI. This insatiable appetite for data necessitates cost-effective, high-capacity storage solutions, a segment where HDDs continue to excel. Technological disruptions, particularly in recording technologies like Shingled Magnetic Recording (SMR) and the nascent Heat-Assisted Magnetic Recording (HAMR), are enabling manufacturers to push the boundaries of areal density, significantly increasing per-drive capacities. These advancements are crucial for maintaining HDD relevance in a landscape increasingly influenced by the performance advantages of SSDs.

Consumer preferences are also playing a pivotal role. While consumers are increasingly adopting SSDs for their primary operating systems and gaming due to superior speed, the demand for large-capacity, affordable storage for photos, videos, and backups remains robust. This is evidenced by the sustained popularity of external HDDs and network-attached storage (NAS) devices. For businesses, the economic viability of HDDs for archiving, nearline storage, and even bulk data processing continues to be a key determinant. The competitive dynamics within the HDD market are intense, characterized by significant investment in research and development, strategic partnerships, and aggressive pricing strategies. Companies are constantly vying to offer the highest capacity drives at the lowest cost per terabyte, which is a critical metric for enterprise and hyperscale data center customers.

The market penetration of HDDs is still substantial, especially within enterprise and cloud storage infrastructures, where the total cost of ownership, including capacity and power efficiency, is a primary consideration. While the CAGR for the overall storage market may be influenced by the rapid growth of SSDs in certain segments, the HDD market is expected to maintain a steady, albeit more moderate, growth rate, driven by its inherent advantages in capacity and cost. The transition to higher capacities, such as the recent introduction of 22TB and 30TB drives, and the ongoing development towards 50TB and beyond, signifies a clear trend of evolving HDD technology to meet future storage demands. The market penetration in developing economies, where cost sensitivity is higher, also presents a significant growth opportunity.

- Market Growth Drivers: Exponential data growth, IoT expansion, digital media consumption, enterprise data analytics, cloud storage demands.

- Technological Disruptions: Shingled Magnetic Recording (SMR), Heat-Assisted Magnetic Recording (HAMR), perpendicular magnetic recording (PMR) advancements.

- Consumer Preferences: Demand for affordable high-capacity storage for media, backups, and archiving.

- Competitive Dynamics: Intense R&D investment, strategic partnerships, aggressive pricing, focus on cost-per-terabyte.

- Market Penetration: Strong in enterprise, cloud, and consumer backup segments; growing in developing economies.

- CAGR: Moderate but steady growth, driven by specific high-capacity requirements.

Dominant Regions & Segments in Hard Disk Drives Industry

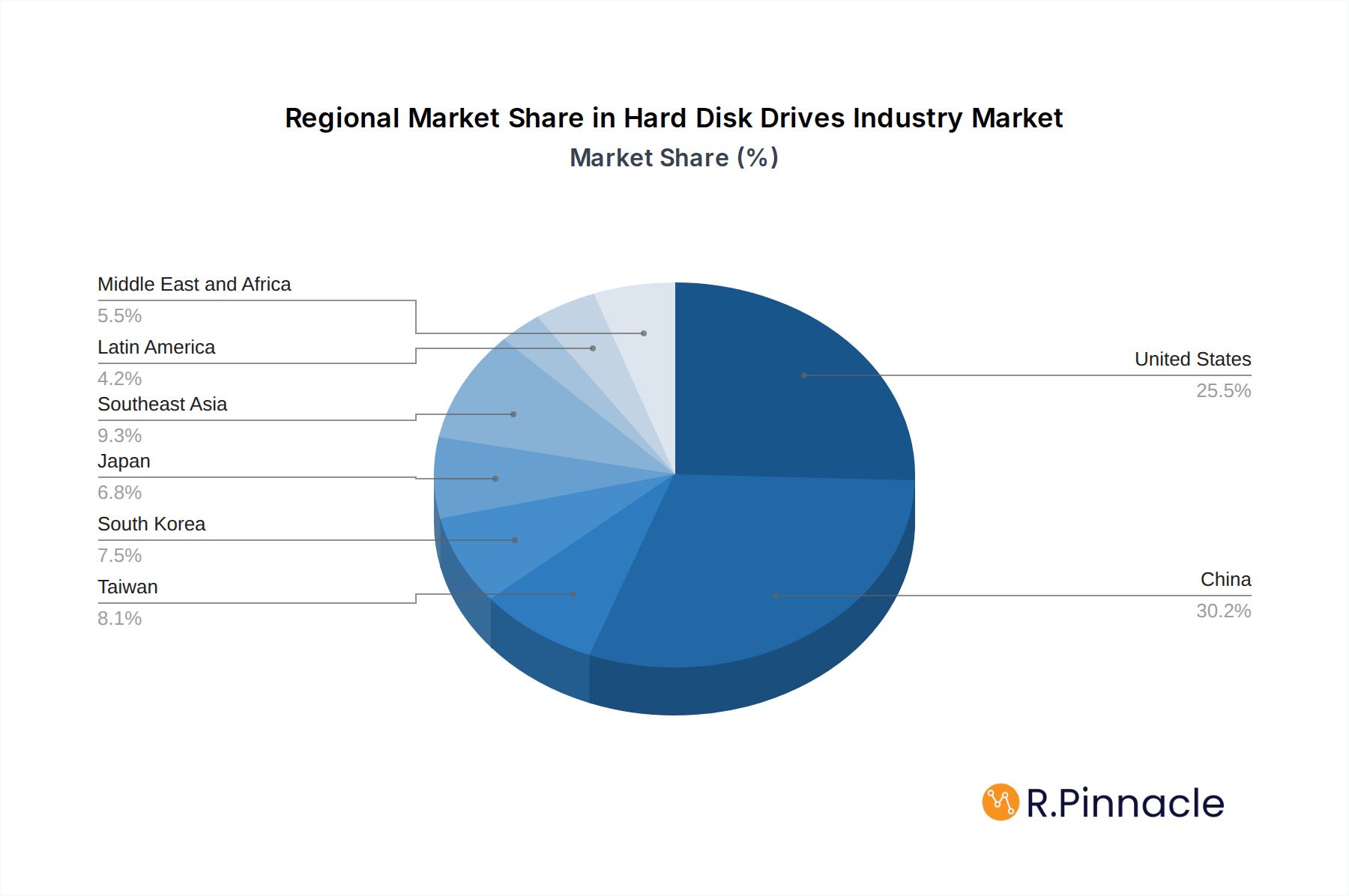

The Hard Disk Drives (HDD) industry's regional dominance is intricately linked to manufacturing capabilities, technological innovation hubs, and the concentration of major end-user markets. Asia-Pacific, particularly China and Taiwan, stands out as the leading region, owing to its extensive manufacturing infrastructure, skilled labor force, and its pivotal role in the global electronics supply chain. China's burgeoning domestic demand for consumer electronics, enterprise solutions, and government data storage initiatives further solidifies its position. Taiwan, a long-standing powerhouse in technology manufacturing, contributes significantly through component production and assembly.

In terms of Form Factor, the 3.5-inch HDD segment continues to dominate the market, primarily serving the enterprise, desktop, and nearline storage applications where high capacity and cost-effectiveness are paramount. While 2.5-inch drives are crucial for mobile and laptop applications, the sheer data volumes handled by servers, data centers, and desktop workstations gravitate towards the larger form factor. The "Others" category, encompassing specialized form factors, is a smaller but growing segment driven by niche applications.

The Application segment clearly shows Enterprise and Nearline as the dominant forces. The insatiable demand for data storage in data centers, cloud computing environments, and for business-critical operations drives the adoption of high-capacity, reliable HDDs. Nearline storage, bridging the gap between high-performance online storage and low-cost offline archival, is also a significant growth area. Consumer and Desktop applications remain important, but their growth is somewhat tempered by the increasing adoption of SSDs for primary system drives. Mobile applications, while a significant market, have largely transitioned to SSDs or eMMC storage.

Geographically, beyond the manufacturing prowess of Asia-Pacific, the United States represents a massive consumption market, particularly for enterprise and cloud storage solutions. Its advanced technological ecosystem and the presence of major cloud service providers fuel substantial demand for HDDs. South Korea and Japan are also significant markets, driven by their strong consumer electronics and advanced industrial sectors. Southeast Asia, Australia, and New Zealand are growing markets, with increasing adoption of digital technologies. Latin America and the Middle East and Africa represent emerging markets with significant growth potential as their digital infrastructure expands.

- Leading Region: Asia-Pacific (China, Taiwan) due to manufacturing dominance and strong domestic demand.

- Dominant Form Factor: 3.5-inch HDDs, catering to enterprise, desktop, and nearline needs.

- Leading Application Segments: Enterprise and Nearline storage, driven by data center and cloud computing demands.

- Key Country Markets: United States (consumption), China (manufacturing & consumption), Taiwan (manufacturing), South Korea, Japan.

- Emerging Markets: Southeast Asia, Latin America, Middle East & Africa.

- Economic Policies: Government initiatives supporting digital infrastructure and data storage.

- Infrastructure Development: Expansion of data centers and cloud facilities in key regions.

Hard Disk Drives Industry Product Innovations

Product innovation in the Hard Disk Drives (HDD) industry is primarily focused on increasing storage density and enhancing energy efficiency. Recent advancements like Toshiba's MG10F Series 22TB HDD showcase the adoption of helium-sealed designs and conventional magnetic recording (CMR) to achieve higher capacities, offering a 10% improvement over previous generations. Seagate's pioneering work with Heat-Assisted Magnetic Recording (HAMR) technology, evidenced by their launch of 30+ TB drives, represents a significant leap forward, paving the way for future drives exceeding 50TB. These innovations offer competitive advantages by delivering more data storage per unit at a reduced cost per terabyte, directly addressing the growing demands of cloud-scale and traditional data-center use cases. The continuous pursuit of higher capacity drives ensures HDDs remain a cost-effective solution for bulk data storage needs.

Report Scope & Segmentation Analysis

This report encompasses a comprehensive analysis of the Hard Disk Drives market, segmented by Form Factor, Application, and Geography.

Form Factor: The market is segmented into 2.5-inch, 3.5-inch, and Other form factors. The 3.5-inch segment is projected to hold the largest market share due to its prevalence in enterprise and desktop applications. The 2.5-inch segment will cater to mobile computing and smaller form-factor enterprise solutions.

Application: Key applications analyzed include Mobile, Consumer, Desktop, Enterprise, Nearline, and Other Applications. The Enterprise and Nearline segments are expected to witness the highest growth rates, driven by data center expansion and cloud storage needs. Consumer and Desktop segments will maintain steady growth, while mobile applications are increasingly dominated by SSDs.

Geography: The report covers the United States, China, Taiwan, South Korea, Japan, Southeast Asia, Australia and New Zealand, Latin America, and the Middle East and Africa. Asia-Pacific is expected to lead in both manufacturing and consumption, with significant growth anticipated in the United States and emerging markets.

Key Drivers of Hard Disk Drives Industry Growth

The growth of the Hard Disk Drives (HDD) industry is underpinned by several critical factors.

- Explosive Data Growth: The continuous surge in data generation from diverse sources like IoT devices, social media, and big data analytics is a primary driver, necessitating vast and cost-effective storage solutions.

- Cost-Effectiveness for Bulk Storage: HDDs continue to offer the lowest cost per terabyte compared to other storage technologies, making them indispensable for archiving, backup, and nearline storage.

- Enterprise and Cloud Demand: The massive expansion of data centers and cloud infrastructure, driven by the need for scalable storage for businesses and consumers, fuels sustained demand for high-capacity enterprise-grade HDDs.

- Technological Advancements: Innovations such as HAMR and SMR are enabling manufacturers to produce higher capacity drives, meeting the evolving storage requirements of users.

- Emerging Markets: Growing digitalization and increasing internet penetration in developing economies are opening up new avenues for HDD adoption.

Challenges in the Hard Disk Drives Industry Sector

Despite robust growth drivers, the Hard Disk Drives (HDD) industry faces several significant challenges.

- Competition from SSDs: Solid State Drives (SSDs) offer superior performance (speed and latency), posing a direct threat, especially in performance-sensitive applications and consumer laptops where price premiums are acceptable.

- Technological Transition Costs: The development and implementation of next-generation recording technologies like HAMR involve substantial R&D investment and manufacturing retooling, impacting profitability.

- Supply Chain Volatility: Geopolitical factors, natural disasters, and component shortages can disrupt the complex global supply chain for HDD manufacturing, leading to production delays and increased costs.

- Market Saturation in Certain Segments: In mature markets and for certain consumer applications, the replacement cycle for HDDs might be lengthening as users consolidate data or migrate to cloud solutions.

- Evolving Data Center Architectures: While HDDs remain vital, the rise of tiered storage strategies and the increasing use of NVMe SSDs in high-performance computing environments present a competitive challenge for traditional HDD roles.

Emerging Opportunities in Hard Disk Drives Industry

The Hard Disk Drives (HDD) industry is poised to capitalize on several emerging opportunities.

- Growth of Big Data and AI/ML: The massive data requirements for training AI models and analyzing big data create a sustained demand for high-capacity, cost-effective storage solutions that HDDs excel at providing.

- Expansion of Cloud and Hyperscale Data Centers: Continuous global expansion of cloud infrastructure by major providers is a significant opportunity, requiring millions of HDDs for their vast storage needs.

- Archival and Cold Storage Solutions: As data retention policies become more stringent and data volumes grow, the demand for affordable, long-term archival and cold storage solutions will increase, a stronghold for HDDs.

- Emerging Markets Digitalization: The ongoing digital transformation in developing economies presents substantial growth potential for consumer and business storage solutions.

- Specialized Applications: Niche markets such as surveillance systems, automotive data logging, and industrial IoT continue to require robust and high-capacity HDD solutions.

Leading Players in the Hard Disk Drives Industry Market

- Toshiba Corporation

- Lenovo Group Limited

- Transcend Information Inc

- ADATA Technology Co Ltd

- Hewlett Packard Enterprise Development LP

- Seagate Technology Holdings PLC

- Western Digital Corporation

- Schneider Electric

- Buffalo Americas Inc

- Sony Corporation

Key Developments in Hard Disk Drives Industry Industry

- September 2023: Toshiba Electronic Devices and Storage Corporation announced the release of its MG10F Series 22TB HDD, a conventional magnetic recording (CMR) HDD that leverages Toshiba's 10-disk helium-sealed design. The MG10F 22TB delivers 10% more capacity than Toshiba's prior generation 20TB model. Designed and engineered to meet the growing data storage needs of its largest customers, the MG10F 22TB HDDs are compatible with a wide range of applications and workloads for both cloud-scale and traditional data-center use cases. This development reinforces Toshiba's commitment to high-capacity enterprise solutions.

- January 2023: Seagate announced the launch of the industry's first 30+ TB hard drive that uses its heat-assisted magnetic recording (HAMR) technology while reaffirming its commitment to release HDDs with capacities of 50 TB and higher in a few years. This milestone demonstrates Seagate's technological leadership in pushing the boundaries of HDD capacity and signals future advancements in storage density.

Future Outlook for Hard Disk Drives Industry Market

The future outlook for the Hard Disk Drives (HDD) industry remains positive, driven by the relentless growth of data and the continued need for cost-effective, high-capacity storage. While SSDs will continue to dominate performance-critical applications, HDDs will remain the backbone of bulk storage, archival, and nearline storage in data centers and enterprise environments. The ongoing advancements in recording technologies, such as HAMR and potentially Microwave-Assisted Magnetic Recording (MAMR), are expected to push HDD capacities well beyond current levels, ensuring their relevance for decades to come. Strategic opportunities lie in further catering to the evolving needs of cloud hyperscalers, leveraging AI and big data trends, and expanding market presence in rapidly digitalizing emerging economies. The industry's ability to innovate and deliver higher capacities at competitive price points will be crucial for sustaining its growth trajectory and securing its position in the evolving digital landscape.

Hard Disk Drives Industry Segmentation

-

1. Form Factor

- 1.1. 2.5 inch

- 1.2. 3.5 inch and Others

-

2. Application

- 2.1. Mobile

- 2.2. Consumer

- 2.3. Desktop

- 2.4. Enterprise

- 2.5. Nearline

- 2.6. Other Applications

-

3. Geography

- 3.1. United States

- 3.2. China

- 3.3. Taiwan

- 3.4. South Korea

- 3.5. Japan

- 3.6. Southeast Asia

- 3.7. Australia and New Zealand

- 3.8. Latin America

- 3.9. Middle East and Africa

Hard Disk Drives Industry Segmentation By Geography

- 1. United States

- 2. China

- 3. Taiwan

- 4. South Korea

- 5. Japan

- 6. Southeast Asia

- 7. Australia and New Zealand

- 8. Latin America

- 9. Middle East and Africa

Hard Disk Drives Industry Regional Market Share

Geographic Coverage of Hard Disk Drives Industry

Hard Disk Drives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 5.1.1. 2.5 inch

- 5.1.2. 3.5 inch and Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Mobile

- 5.2.2. Consumer

- 5.2.3. Desktop

- 5.2.4. Enterprise

- 5.2.5. Nearline

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. China

- 5.3.3. Taiwan

- 5.3.4. South Korea

- 5.3.5. Japan

- 5.3.6. Southeast Asia

- 5.3.7. Australia and New Zealand

- 5.3.8. Latin America

- 5.3.9. Middle East and Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. China

- 5.4.3. Taiwan

- 5.4.4. South Korea

- 5.4.5. Japan

- 5.4.6. Southeast Asia

- 5.4.7. Australia and New Zealand

- 5.4.8. Latin America

- 5.4.9. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 6. Global Hard Disk Drives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Form Factor

- 6.1.1. 2.5 inch

- 6.1.2. 3.5 inch and Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Mobile

- 6.2.2. Consumer

- 6.2.3. Desktop

- 6.2.4. Enterprise

- 6.2.5. Nearline

- 6.2.6. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. China

- 6.3.3. Taiwan

- 6.3.4. South Korea

- 6.3.5. Japan

- 6.3.6. Southeast Asia

- 6.3.7. Australia and New Zealand

- 6.3.8. Latin America

- 6.3.9. Middle East and Africa

- 6.1. Market Analysis, Insights and Forecast - by Form Factor

- 7. United States Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Form Factor

- 7.1.1. 2.5 inch

- 7.1.2. 3.5 inch and Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Mobile

- 7.2.2. Consumer

- 7.2.3. Desktop

- 7.2.4. Enterprise

- 7.2.5. Nearline

- 7.2.6. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. China

- 7.3.3. Taiwan

- 7.3.4. South Korea

- 7.3.5. Japan

- 7.3.6. Southeast Asia

- 7.3.7. Australia and New Zealand

- 7.3.8. Latin America

- 7.3.9. Middle East and Africa

- 7.1. Market Analysis, Insights and Forecast - by Form Factor

- 8. China Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Form Factor

- 8.1.1. 2.5 inch

- 8.1.2. 3.5 inch and Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Mobile

- 8.2.2. Consumer

- 8.2.3. Desktop

- 8.2.4. Enterprise

- 8.2.5. Nearline

- 8.2.6. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. China

- 8.3.3. Taiwan

- 8.3.4. South Korea

- 8.3.5. Japan

- 8.3.6. Southeast Asia

- 8.3.7. Australia and New Zealand

- 8.3.8. Latin America

- 8.3.9. Middle East and Africa

- 8.1. Market Analysis, Insights and Forecast - by Form Factor

- 9. Taiwan Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Form Factor

- 9.1.1. 2.5 inch

- 9.1.2. 3.5 inch and Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Mobile

- 9.2.2. Consumer

- 9.2.3. Desktop

- 9.2.4. Enterprise

- 9.2.5. Nearline

- 9.2.6. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. China

- 9.3.3. Taiwan

- 9.3.4. South Korea

- 9.3.5. Japan

- 9.3.6. Southeast Asia

- 9.3.7. Australia and New Zealand

- 9.3.8. Latin America

- 9.3.9. Middle East and Africa

- 9.1. Market Analysis, Insights and Forecast - by Form Factor

- 10. South Korea Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Form Factor

- 10.1.1. 2.5 inch

- 10.1.2. 3.5 inch and Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Mobile

- 10.2.2. Consumer

- 10.2.3. Desktop

- 10.2.4. Enterprise

- 10.2.5. Nearline

- 10.2.6. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. United States

- 10.3.2. China

- 10.3.3. Taiwan

- 10.3.4. South Korea

- 10.3.5. Japan

- 10.3.6. Southeast Asia

- 10.3.7. Australia and New Zealand

- 10.3.8. Latin America

- 10.3.9. Middle East and Africa

- 10.1. Market Analysis, Insights and Forecast - by Form Factor

- 11. Japan Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Form Factor

- 11.1.1. 2.5 inch

- 11.1.2. 3.5 inch and Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Mobile

- 11.2.2. Consumer

- 11.2.3. Desktop

- 11.2.4. Enterprise

- 11.2.5. Nearline

- 11.2.6. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. United States

- 11.3.2. China

- 11.3.3. Taiwan

- 11.3.4. South Korea

- 11.3.5. Japan

- 11.3.6. Southeast Asia

- 11.3.7. Australia and New Zealand

- 11.3.8. Latin America

- 11.3.9. Middle East and Africa

- 11.1. Market Analysis, Insights and Forecast - by Form Factor

- 12. Southeast Asia Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Form Factor

- 12.1.1. 2.5 inch

- 12.1.2. 3.5 inch and Others

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Mobile

- 12.2.2. Consumer

- 12.2.3. Desktop

- 12.2.4. Enterprise

- 12.2.5. Nearline

- 12.2.6. Other Applications

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. United States

- 12.3.2. China

- 12.3.3. Taiwan

- 12.3.4. South Korea

- 12.3.5. Japan

- 12.3.6. Southeast Asia

- 12.3.7. Australia and New Zealand

- 12.3.8. Latin America

- 12.3.9. Middle East and Africa

- 12.1. Market Analysis, Insights and Forecast - by Form Factor

- 13. Australia and New Zealand Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Form Factor

- 13.1.1. 2.5 inch

- 13.1.2. 3.5 inch and Others

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Mobile

- 13.2.2. Consumer

- 13.2.3. Desktop

- 13.2.4. Enterprise

- 13.2.5. Nearline

- 13.2.6. Other Applications

- 13.3. Market Analysis, Insights and Forecast - by Geography

- 13.3.1. United States

- 13.3.2. China

- 13.3.3. Taiwan

- 13.3.4. South Korea

- 13.3.5. Japan

- 13.3.6. Southeast Asia

- 13.3.7. Australia and New Zealand

- 13.3.8. Latin America

- 13.3.9. Middle East and Africa

- 13.1. Market Analysis, Insights and Forecast - by Form Factor

- 14. Latin America Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Form Factor

- 14.1.1. 2.5 inch

- 14.1.2. 3.5 inch and Others

- 14.2. Market Analysis, Insights and Forecast - by Application

- 14.2.1. Mobile

- 14.2.2. Consumer

- 14.2.3. Desktop

- 14.2.4. Enterprise

- 14.2.5. Nearline

- 14.2.6. Other Applications

- 14.3. Market Analysis, Insights and Forecast - by Geography

- 14.3.1. United States

- 14.3.2. China

- 14.3.3. Taiwan

- 14.3.4. South Korea

- 14.3.5. Japan

- 14.3.6. Southeast Asia

- 14.3.7. Australia and New Zealand

- 14.3.8. Latin America

- 14.3.9. Middle East and Africa

- 14.1. Market Analysis, Insights and Forecast - by Form Factor

- 15. Middle East and Africa Hard Disk Drives Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - by Form Factor

- 15.1.1. 2.5 inch

- 15.1.2. 3.5 inch and Others

- 15.2. Market Analysis, Insights and Forecast - by Application

- 15.2.1. Mobile

- 15.2.2. Consumer

- 15.2.3. Desktop

- 15.2.4. Enterprise

- 15.2.5. Nearline

- 15.2.6. Other Applications

- 15.3. Market Analysis, Insights and Forecast - by Geography

- 15.3.1. United States

- 15.3.2. China

- 15.3.3. Taiwan

- 15.3.4. South Korea

- 15.3.5. Japan

- 15.3.6. Southeast Asia

- 15.3.7. Australia and New Zealand

- 15.3.8. Latin America

- 15.3.9. Middle East and Africa

- 15.1. Market Analysis, Insights and Forecast - by Form Factor

- 16. Competitive Analysis

- 16.1. Company Profiles

- 16.1.1 Toshiba Corporation

- 16.1.1.1. Company Overview

- 16.1.1.2. Products

- 16.1.1.3. Company Financials

- 16.1.1.4. SWOT Analysis

- 16.1.2 Lenovo Group Limited

- 16.1.2.1. Company Overview

- 16.1.2.2. Products

- 16.1.2.3. Company Financials

- 16.1.2.4. SWOT Analysis

- 16.1.3 Transcend Information Inc

- 16.1.3.1. Company Overview

- 16.1.3.2. Products

- 16.1.3.3. Company Financials

- 16.1.3.4. SWOT Analysis

- 16.1.4 ADATA Technology Co Ltd

- 16.1.4.1. Company Overview

- 16.1.4.2. Products

- 16.1.4.3. Company Financials

- 16.1.4.4. SWOT Analysis

- 16.1.5 Hewlett Packard Enterprise Development LP

- 16.1.5.1. Company Overview

- 16.1.5.2. Products

- 16.1.5.3. Company Financials

- 16.1.5.4. SWOT Analysis

- 16.1.6 Seagate Technology Holdings PLC

- 16.1.6.1. Company Overview

- 16.1.6.2. Products

- 16.1.6.3. Company Financials

- 16.1.6.4. SWOT Analysis

- 16.1.7 Western Digital Corporation

- 16.1.7.1. Company Overview

- 16.1.7.2. Products

- 16.1.7.3. Company Financials

- 16.1.7.4. SWOT Analysis

- 16.1.8 Schneider Electric

- 16.1.8.1. Company Overview

- 16.1.8.2. Products

- 16.1.8.3. Company Financials

- 16.1.8.4. SWOT Analysis

- 16.1.9 Buffalo Americas Inc *List Not Exhaustive

- 16.1.9.1. Company Overview

- 16.1.9.2. Products

- 16.1.9.3. Company Financials

- 16.1.9.4. SWOT Analysis

- 16.1.10 Sony Corporation

- 16.1.10.1. Company Overview

- 16.1.10.2. Products

- 16.1.10.3. Company Financials

- 16.1.10.4. SWOT Analysis

- 16.1.1 Toshiba Corporation

- 16.2. Market Entropy

- 16.2.1 Company's Key Areas Served

- 16.2.2 Recent Developments

- 16.3. Company Market Share Analysis 2025

- 16.3.1 Top 5 Companies Market Share Analysis

- 16.3.2 Top 3 Companies Market Share Analysis

- 16.4. List of Potential Customers

- 17. Research Methodology

List of Figures

- Figure 1: Global Hard Disk Drives Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: United States Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 3: United States Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 4: United States Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: United States Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: United States Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 7: United States Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: United States Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: United States Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: China Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 11: China Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 12: China Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: China Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: China Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 15: China Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: China Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: China Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Taiwan Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 19: Taiwan Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 20: Taiwan Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Taiwan Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Taiwan Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 23: Taiwan Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Taiwan Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Taiwan Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South Korea Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 27: South Korea Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 28: South Korea Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: South Korea Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: South Korea Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 31: South Korea Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 32: South Korea Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: South Korea Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Japan Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 35: Japan Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 36: Japan Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 37: Japan Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Japan Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 39: Japan Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 40: Japan Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Japan Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Southeast Asia Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 43: Southeast Asia Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 44: Southeast Asia Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 45: Southeast Asia Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Southeast Asia Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 47: Southeast Asia Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 48: Southeast Asia Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 49: Southeast Asia Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Australia and New Zealand Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 51: Australia and New Zealand Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 52: Australia and New Zealand Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 53: Australia and New Zealand Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 54: Australia and New Zealand Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 55: Australia and New Zealand Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 56: Australia and New Zealand Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 57: Australia and New Zealand Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 58: Latin America Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 59: Latin America Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 60: Latin America Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 61: Latin America Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Latin America Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 63: Latin America Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 64: Latin America Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 65: Latin America Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Hard Disk Drives Industry Revenue (billion), by Form Factor 2025 & 2033

- Figure 67: Middle East and Africa Hard Disk Drives Industry Revenue Share (%), by Form Factor 2025 & 2033

- Figure 68: Middle East and Africa Hard Disk Drives Industry Revenue (billion), by Application 2025 & 2033

- Figure 69: Middle East and Africa Hard Disk Drives Industry Revenue Share (%), by Application 2025 & 2033

- Figure 70: Middle East and Africa Hard Disk Drives Industry Revenue (billion), by Geography 2025 & 2033

- Figure 71: Middle East and Africa Hard Disk Drives Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 72: Middle East and Africa Hard Disk Drives Industry Revenue (billion), by Country 2025 & 2033

- Figure 73: Middle East and Africa Hard Disk Drives Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 2: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Global Hard Disk Drives Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 6: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 10: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 14: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 18: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 22: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 26: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 27: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 28: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 30: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 31: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 32: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 33: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 34: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 35: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 36: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Global Hard Disk Drives Industry Revenue billion Forecast, by Form Factor 2020 & 2033

- Table 38: Global Hard Disk Drives Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global Hard Disk Drives Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 40: Global Hard Disk Drives Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hard Disk Drives Industry?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Hard Disk Drives Industry?

Key companies in the market include Toshiba Corporation, Lenovo Group Limited, Transcend Information Inc, ADATA Technology Co Ltd, Hewlett Packard Enterprise Development LP, Seagate Technology Holdings PLC, Western Digital Corporation, Schneider Electric, Buffalo Americas Inc *List Not Exhaustive, Sony Corporation.

3. What are the main segments of the Hard Disk Drives Industry?

The market segments include Form Factor, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 48.97 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Storage Space.

6. What are the notable trends driving market growth?

Increasing Need for Storage Space to Drive the Market.

7. Are there any restraints impacting market growth?

Development of Alternative Storage Devices/Technologies.

8. Can you provide examples of recent developments in the market?

September 2023: Toshiba Electronic Devices and Storage Corporation announced the release of its MG10F Series 22TB HDD, a conventional magnetic recording (CMR) HDD that leverages Toshiba's 10-disk helium-sealed design. The MG10F 22TB delivers 10% more capacity than Toshiba's prior generation 20TB model. Designed and engineered to meet the growing data storage needs of its largest customers, the MG10F 22TB HDDs are compatible with a wide range of applications and workloads for both cloud-scale and traditional data-center use cases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hard Disk Drives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hard Disk Drives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hard Disk Drives Industry?

To stay informed about further developments, trends, and reports in the Hard Disk Drives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence