Key Insights

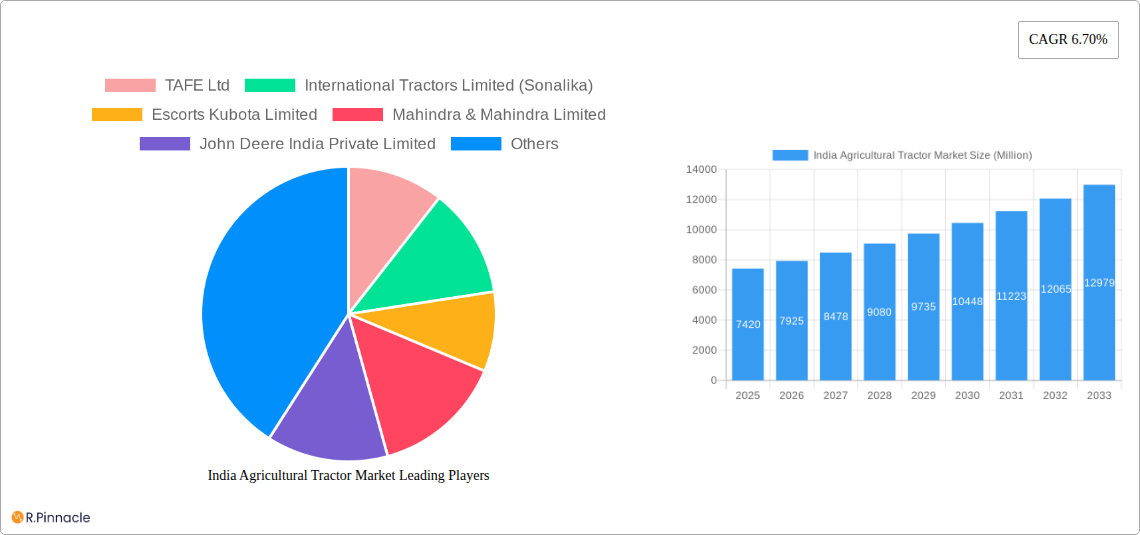

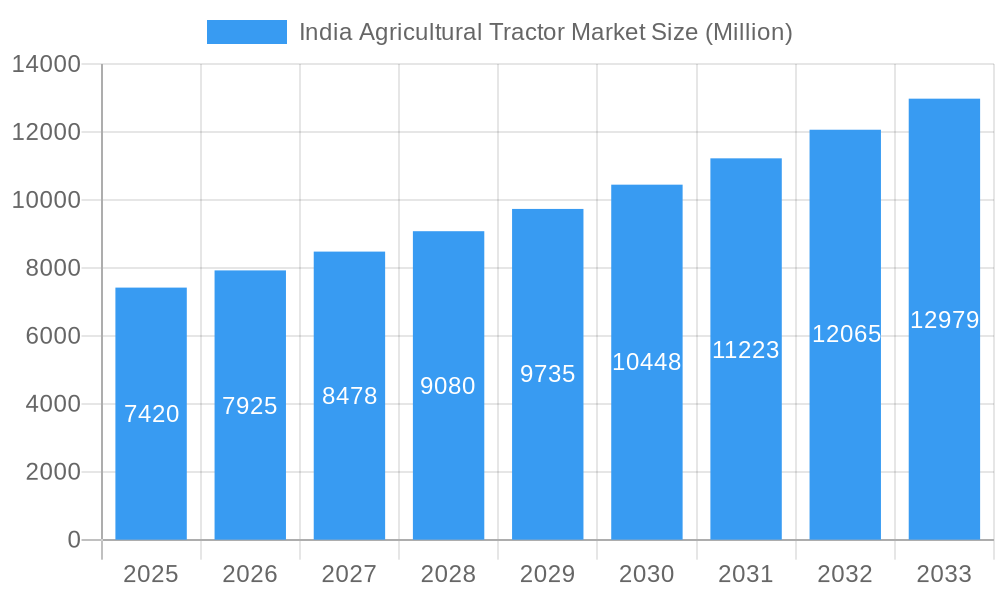

The India Agricultural Tractor Market is poised for substantial growth, projected to achieve a robust $7.42 billion in 2025. This thriving sector is anticipated to expand at a strong Compound Annual Growth Rate (CAGR) of 6.70% throughout the forecast period of 2025-2033. This impressive trajectory is primarily fueled by increasing government initiatives aimed at promoting agricultural mechanization, offering substantial subsidies on farm equipment, and fostering easy access to credit for farmers. A growing imperative for enhanced farm productivity, coupled with a persistent shortage of agricultural labor, compels farmers to adopt modern, efficient tractor solutions. Furthermore, rising rural incomes and the continuous demand for food production for India's vast and expanding population serve as fundamental growth drivers for the industry.

India Agricultural Tractor Market Market Size (In Million)

Key trends shaping the Indian agricultural tractor market include a definitive shift towards higher horsepower (HP) tractors, particularly within the 40 HP to 150 HP and 151 HP to 250 HP segments, as farmers seek greater efficiency for larger landholdings and more demanding implements. There is also a nascent yet growing interest in precision agriculture technologies that can optimize resource usage. While Internal Combustion Engine (ICE) models currently dominate the market, the emergence and development of electric tractors signal a future transition towards more sustainable farming practices. Utility and Row Crop Tractors remain the most sought-after types, with the adoption of 4-Wheel Drive (4WD) configurations steadily gaining traction due to their superior performance. The competitive landscape is dynamic, featuring prominent players such as Mahindra & Mahindra Ltd., Escorts Ltd., Tractors and Farm Equipment Limited (TAFE), Deere & Company, and Kubota Corp., all of whom are actively innovating with advanced features, strengthening extensive dealer networks, and providing comprehensive after-sales services to meet the diverse requirements of farmers across India.

India Agricultural Tractor Market Company Market Share

Description: Navigate the dynamic landscape of the India agricultural tractor market with our comprehensive, SEO-optimized report. This essential guide provides in-depth analysis for industry professionals, investors, and policymakers seeking to understand market size, growth drivers, and strategic opportunities. Leveraging high-ranking keywords such as "farm mechanization India," "tractor sales India," "agriculture technology trends," and "rural economy impact," this report offers unparalleled insights into a sector vital to India's economic growth. From the robust demand for utility tractors to the burgeoning potential of electric tractors, we meticulously examine market segments, competitive strategies, and future projections. The study period spans 2019–2033, with 2025 as the base and estimated year, and a forecast extending to 2033, providing a detailed historical context (2019–2024) and forward-looking analysis. Discover how leading players like Mahindra & Mahindra Ltd., Escorts Ltd., and TAFE are shaping the industry through innovation and strategic investments. Uncover critical market dynamics, emerging technologies, and policy impacts that will define the next decade of agricultural mechanization in India.

India Agricultural Tractor Market Market Structure & Innovation Trends

The India agricultural tractor market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, yet also accommodating numerous smaller and regional manufacturers contributing to a competitive landscape. Market concentration is particularly evident in the higher horsepower segments, while the compact and utility tractor categories see a broader array of competition. Leading companies like Mahindra & Mahindra Ltd., Escorts Ltd., and Tractors and Farm Equipment Limited (TAFE) consistently command a substantial portion of the market, with their combined market share often exceeding xx% to xx% of total sales volume. This dominance is sustained through extensive dealer networks, strong brand loyalty, and continuous product innovation tailored to diverse Indian farming conditions.

Innovation drivers are multifaceted, propelled by a combination of necessity and opportunity. The pressing need for increased agricultural productivity amidst a shrinking labor force and rising labor costs is a primary catalyst. This drives demand for more efficient, versatile, and automated tractors. Furthermore, government initiatives promoting farm mechanization, such as subsidies and loan schemes, significantly encourage the adoption of advanced machinery. Regulatory frameworks, including emission standards and safety regulations, also steer innovation, prompting manufacturers to invest in greener technologies and enhanced safety features. For instance, the push towards Bharat Stage (Trem IV/V) emission norms for non-road diesel engines is compelling companies to develop more fuel-efficient and environmentally friendly engines. Product substitutes, while present in the form of power tillers or animal-drawn implements, increasingly struggle to compete with the efficiency and labor-saving benefits offered by modern tractors, especially as farm sizes consolidate and income levels rise.

End-user demographics play a crucial role in shaping market demand. Small and marginal farmers, who constitute the majority of Indian agriculturists, primarily drive demand for compact and utility tractors in the Less Than 40 HP and 40 HP to 75 HP ranges. Conversely, larger commercial farms, particularly in states like Punjab, Haryana, and Uttar Pradesh, often opt for higher horsepower tractors (75 HP to 150 HP and above) to handle extensive acreage and demanding tasks. The rising awareness about precision farming and advanced farm management systems is also influencing purchasing decisions, particularly among younger, technologically adept farmers.

Mergers and acquisitions (M&A) activities, though not as frequent as in some other sectors, are strategically important. These activities often involve global players acquiring or forming joint ventures with Indian companies to gain market access or expand their product portfolios. While specific recent M&A deal values in the Indian agricultural tractor sector are proprietary, the trend often involves technology transfer and capacity expansion. For example, a global player might acquire a stake in an Indian firm to leverage its manufacturing capabilities and distribution network, or an Indian major might acquire a smaller competitor to consolidate market share or gain access to a niche technology. These strategic alliances and acquisitions, valued potentially in the range of hundreds of Million USD, are instrumental in driving market consolidation and introducing new technologies, contributing to a more robust and innovative industry structure.

India Agricultural Tractor Market Market Dynamics & Trends

The India agricultural tractor market is experiencing robust dynamics, propelled by a confluence of strong growth drivers and transformative technological disruptions, while simultaneously adapting to evolving consumer preferences and intense competitive pressures. A significant market growth driver is the sustained government support for agriculture through various schemes like the Pradhan Mantri Krishi Sinchai Yojana (PMKSY), Sub-Mission on Agricultural Mechanization (SMAM), and farmer income support programs like PM-KISAN. These initiatives boost farmer purchasing power and encourage the adoption of modern farming equipment, directly impacting tractor sales. Furthermore, the increasing scarcity of farm labor and rising labor wages across rural India necessitate mechanization to maintain productivity, making tractors an indispensable asset for farmers. The rising disposable income of farmers, driven by better crop prices and government procurement, also fuels demand for new and advanced tractors. Urbanization and the migration of rural youth to cities are further intensifying the labor crunch, making mechanization not just an option, but a necessity for sustainable farming.

Technological disruptions are fundamentally reshaping the market. The integration of advanced features such as GPS-enabled auto-steer, telematics for remote monitoring, and IoT-based predictive maintenance is transforming traditional tractors into smart farming solutions. Electric tractors, while still in their nascent stages, represent a significant disruption, offering the promise of reduced operating costs, lower emissions, and quieter operations. Companies like Tractors and Farm Equipment Limited (TAFE) are at the forefront, introducing electric models equipped with farm management systems. The adoption of precision agriculture techniques, enabled by these smart tractors, allows farmers to optimize resource utilization, leading to higher yields and reduced input costs. The development of AI-driven implements that can adapt to varying soil and crop conditions further exemplifies the technological leap occurring in the sector. These innovations are not just improving efficiency but also enhancing the overall farming experience, making it less laborious and more profitable.

Consumer preferences are rapidly evolving, shifting towards tractors that offer greater fuel efficiency, versatility for multiple applications, and enhanced comfort for operators. There is a growing demand for tractors with advanced hydraulics, power steering, and comfortable cabins, reflecting farmers' desire for a more ergonomic and productive working environment. Affordability remains a critical factor, particularly for small and marginal farmers, leading manufacturers to innovate in developing cost-effective yet feature-rich models. The demand for 4 Wheel Drive tractors is also steadily increasing, especially in regions with challenging terrains or those requiring heavier implements, although 2 Wheel Drive models still dominate due to their lower initial cost and suitability for most Indian conditions. The increasing awareness about environmental sustainability is also influencing choices, with a gradual but discernible preference for cleaner and more energy-efficient machines, setting the stage for electric and alternative fuel tractors.

The competitive dynamics within the India agricultural tractor market are characterized by intense competition across all segments. Major players engage in robust product development, aggressive marketing campaigns, and expansion of their sales and service networks. Pricing strategies are highly competitive, with companies constantly balancing affordability with feature enrichment. After-sales service and spare parts availability are crucial differentiators, as farmers rely heavily on prompt support to minimize downtime. Companies are also focusing on financial schemes and partnerships with banks and non-banking financial companies (NBFCs) to offer easier credit access to farmers, thereby facilitating tractor purchases. The market is expected to grow at a Compound Annual Growth Rate (CAGR) of approximately xx% from 2025 to 2033, driven by these dynamics. Market penetration, particularly in regions with lower mechanization rates, offers significant untapped potential, estimated to increase from its current xx% to xx% over the forecast period as awareness and accessibility improve.

Dominant Regions & Segments in India Agricultural Tractor Market

The Indian agricultural tractor market exhibits distinct regional and segmental dominance, driven by varied agricultural practices, economic conditions, and farmer preferences. Among the various segments, Utility Tractors in the 40 HP to 150 HP range, predominantly with 2 Wheel Drive and utilizing ICE (Internal Combustion Engine) propulsion, currently hold the most significant market share. This dominance is largely attributable to their versatility, suitability for a wide array of farming tasks, and optimal balance between power and fuel efficiency for the typical Indian farm size.

- Key Drivers for Dominance of Utility Tractors (40-150 HP, 2WD, ICE):

- Economic Policies and Government Support: Government subsidies and schemes often target the purchase of utility tractors, making them more accessible and affordable for a broad spectrum of farmers. Policies encouraging farm mechanization, coupled with easy financing options, have significantly boosted sales in this category.

- Versatility and Applicability: Utility tractors in this HP range are highly versatile, capable of performing diverse tasks from plowing and tilling to hauling and operating various implements like rotavators, cultivators, and seed drills. This multi-purpose utility makes them an attractive investment for farmers who need a single machine for multiple applications.

- Farm Size and Cropping Patterns: The majority of Indian farms are small to medium-sized. Tractors in the 40 HP to 150 HP range are ideally suited for these farm sizes, offering sufficient power without being oversized or excessively expensive. Regions with intensive cultivation of crops like wheat, rice, sugarcane, and cotton heavily rely on these tractors.

- Infrastructure and Road Conditions: While 4 Wheel Drive (4WD) offers superior traction, the existing rural road infrastructure and the nature of most field operations in India mean that 2 Wheel Drive (2WD) tractors are often sufficient and more cost-effective. Their lighter weight and simpler mechanics also contribute to easier maintenance and lower initial purchase costs.

- Cost-Effectiveness and Fuel Efficiency: ICE tractors have a long-established presence, offering proven reliability, ease of repair, and readily available fuel (diesel). While electric propulsion is emerging, ICE models still dominate due to their lower initial cost and widespread service infrastructure. Tractors in this HP range are also increasingly designed for better fuel efficiency, appealing to cost-conscious farmers.

- Farmer Familiarity and Training: Farmers have a high degree of familiarity with operating and maintaining ICE 2WD utility tractors. The widespread availability of skilled mechanics and spare parts further reinforces their dominance.

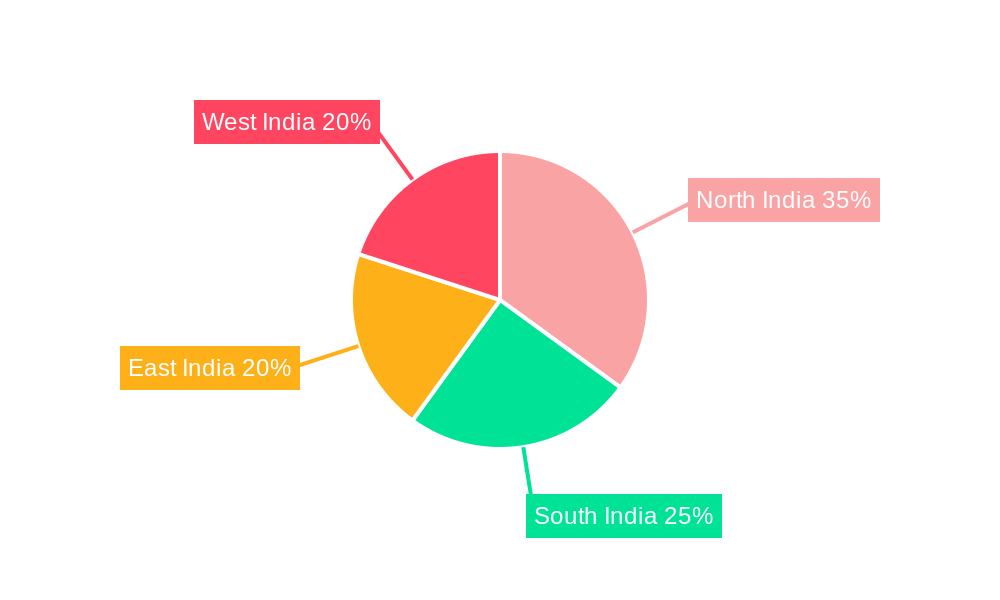

Geographically, states within North India (e.g., Uttar Pradesh, Punjab, Haryana) and Central India (e.g., Madhya Pradesh, Rajasthan) typically represent the largest markets for agricultural tractors. Uttar Pradesh, for instance, with its vast agricultural land and diverse cropping patterns, consistently leads in tractor sales volume. This regional dominance is driven by high agricultural productivity, larger landholdings compared to some southern states, and a strong culture of mechanization. States like Punjab and Haryana, being the 'grain bowls' of India, have high mechanization rates and a demand for more powerful tractors.

The Authorized Dealers and Distributors channel remains the primary sales route, underpinning the market's reach. This network ensures product availability, essential after-sales service, and critical farmer financing support, which are vital for widespread adoption across diverse geographical regions. While direct sales exist for specific large-scale buyers, the intricate network of dealers provides localized support, crucial for a product like tractors that require continuous maintenance and parts availability. This traditional channel's dominance is unlikely to be significantly challenged in the short to medium term due to its deep penetration and trust among the farming community.

India Agricultural Tractor Market Product Innovations

The India agricultural tractor market is witnessing a wave of product innovations, driven by the need for enhanced efficiency, sustainability, and connectivity. Manufacturers are focusing on developing tractors that are not only powerful and robust but also smart and eco-friendly. Recent developments include the introduction of electric tractors, such as those unveiled by Tractors and Farm Equipment Limited (TAFE), featuring advanced auto-steer capabilities and integrated farm management systems. These innovations promise reduced operational costs and lower environmental impact, aligning with global sustainability goals. Furthermore, advancements in ICE technology are leading to more fuel-efficient engines that comply with stricter emission norms, offering competitive advantages through lower running costs. The integration of precision farming technologies like GPS-guided steering, telematics, and IoT sensors is also becoming more prevalent, enabling farmers to optimize resource use and boost productivity. These technological trends are focused on creating a better market fit by addressing challenges like labor scarcity and the demand for data-driven farming, ultimately aiming to make farming more profitable and less strenuous for the Indian farmer.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the India agricultural tractor market to provide granular insights into its multifaceted structure. The market is segmented by Type, including Compact Tractors, Utility Tractors, Row Crop Tractors, Orchard Tractors, and Specialty Tractors. Utility tractors are anticipated to remain the largest segment, valued at xx Million in 2025, driven by their versatility and suitability for a wide range of farm sizes, with a projected CAGR of xx%. The Horsepower (HP) segment is categorized into Less Than 40 HP, 40 HP to 150 HP, 151 HP to 250 HP, 251 HP to 350 HP, and More Than 350 HP. The 40 HP to 150 HP segment dominates, accounting for a market size of xx Million in 2025, fueled by high demand from small and medium farmers. In terms of Drive Type, the market is split into 2 Wheel Drive and 4 Wheel Drive, with 2 Wheel Drive tractors holding a substantial share, valued at xx Million in 2025, due to their cost-effectiveness and applicability in most Indian farming conditions. The Propulsion segment covers Electric and ICE (Internal Combustion Engine), where ICE tractors currently hold the lion's share, estimated at xx Million in 2025, but electric tractors are projected to exhibit the highest growth rate at xx% CAGR. Finally, by Sales Channel, the market is divided into Direct Sales and Authorized Dealers and Distributors, with the latter being the predominant channel, valued at xx Million in 2025, owing to its extensive reach and crucial after-sales support.

Key Drivers of India Agricultural Tractor Market Growth

The India agricultural tractor market is propelled by several robust growth drivers, fundamentally transforming the agricultural landscape.

- Government Support & Subsidies: Proactive government policies like the Sub-Mission on Agricultural Mechanization (SMAM) and various loan schemes significantly reduce the financial burden on farmers, encouraging tractor purchases. This is a critical factor driving demand, especially for small and marginal farmers.

- Labor Scarcity & Rising Wages: The increasing migration of rural populations to urban areas, coupled with rising agricultural labor wages, creates a pressing need for mechanization to maintain farm productivity and profitability. Tractors emerge as an indispensable solution to overcome this labor deficit.

- Increasing Farm Income & Crop Prices: Better minimum support prices (MSPs) for crops, improved irrigation facilities, and overall growth in agricultural output contribute to higher farm incomes, enabling farmers to invest in advanced machinery like tractors.

- Technological Advancements: The introduction of smart tractors equipped with GPS, telematics, and automation features enhances efficiency, reduces operational costs, and attracts younger, tech-savvy farmers. Electric tractors, though nascent, represent a future growth frontier, promising lower running costs and environmental benefits.

- Expansion of Farm Credit: Easier access to credit facilities from banks and financial institutions tailored for agricultural machinery purchases, often supported by government schemes, facilitates higher tractor sales.

Challenges in the India Agricultural Tractor Market Sector

Despite robust growth, the India agricultural tractor market faces several challenges that could impede its full potential.

- Fragmented Landholdings: The prevalence of small and fragmented landholdings in India often makes large-scale tractor ownership economically unviable for many farmers, limiting the market for higher HP tractors and efficient utilization. This can impact sales volume in specific segments by an estimated xx%.

- High Initial Investment: The initial capital outlay for purchasing a new tractor can be substantial, posing a significant barrier for financially constrained small and marginal farmers, even with subsidies. This financial hurdle can defer purchases by up to xx% in some regions.

- Fluctuating Agricultural Income: Variability in monsoon patterns, unpredictable crop yields, and fluctuating market prices for agricultural produce directly impact farmers' disposable income, making them hesitant to make large investments in machinery during lean periods.

- Lack of Access to Finance: While government schemes exist, a significant portion of the farming community still struggles with limited access to formal credit channels, pushing them towards informal, high-interest loans that make tractor ownership difficult.

- Intense Competition & Pricing Pressures: The market is highly competitive with numerous domestic and international players, leading to pricing pressures that can impact profit margins for manufacturers and make it challenging for smaller players to thrive.

Emerging Opportunities in India Agricultural Tractor Market

The India agricultural tractor market is ripe with emerging opportunities that promise to drive future growth and innovation.

- Growth of Tractor Rental Services: The rise of organized tractor rental services (e.g., through digital platforms) presents a significant opportunity. This model makes mechanization accessible to small and marginal farmers who cannot afford outright ownership, thereby expanding the user base for tractors.

- Electrification of Tractors: The increasing focus on sustainable agriculture and government push for electric vehicles opens a substantial opportunity for electric tractors. As battery technology improves and charging infrastructure develops, electric tractors are poised for exponential growth, offering lower operating costs and environmental benefits.

- Precision Agriculture Integration: The adoption of precision farming technologies, including GPS-enabled guidance systems, telematics, and IoT integration, offers a niche but rapidly growing market. Tractors equipped with these features can optimize resource use, reduce waste, and improve yields, appealing to progressive farmers.

- Focus on Specialty Tractors: Growing demand for specialized tractors for specific applications like orchard farming, vineyard management, and sugarcane cultivation presents a significant opportunity for manufacturers to innovate and cater to niche segments, particularly as crop diversification increases.

- Export Potential: Indian tractor manufacturers, with their cost-effective production capabilities and robust designs suitable for challenging conditions, have an opportunity to expand their export footprint to developing markets in Africa, Southeast Asia, and Latin America.

Leading Players in the India Agricultural Tractor Market Market

- Escorts Ltd.

- Tractors and Farm Equipment Limited

- Mahindra & Mahindra Ltd.

- Deere & Company

- AGCO Corp.

- Iseki & Co. Ltd.

- Claas KGaA mbH

- Massey Ferguson

- New Holland

- Qilu Machinery

- Case IH

- International Tractors Ltd

- CNH Industrial N.V.

- Kubota Corp.

- Yanmar Co., Ltd.

- Others

Key Developments in India Agricultural Tractor Market Industry

- April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, featured MS Dhoni's signature as a symbol of gratitude to the customers, boosting brand visibility and customer engagement, particularly among rural consumers who connect with the cricketing legend.

- March 2024: Sonalika Tractors invested USD 157.4 Million for two new plants in Punjab. The company allocated USD 121.1 Million to a new tractor assembly plant and USD 36.3 Million to a high-pressure foundry. This significant investment aims to enhance production capacity, improve manufacturing efficiency, and strengthen the company's position in the highly competitive tractor market.

- January 2024: Tractors and Farm Equipment Limited (TAFE) introduced electric tractors at the Tamil Nadu Global Investors Meet (TN GIM) 2024. These tractors are equipped with auto steer and a farm management system, marking a pivotal step towards sustainable farm mechanization and catering to the evolving needs for advanced, eco-friendly farming solutions in India.

Future Outlook for India Agricultural Tractor Market Market

The future outlook for the India agricultural tractor market remains overwhelmingly positive, driven by persistent growth accelerators. Continued government emphasis on farm mechanization through enhanced subsidies and credit availability will significantly bolster purchasing power among farmers. The ongoing shift towards precision agriculture, integrating advanced technologies like AI, IoT, and telematics into tractors, will create demand for high-value, feature-rich models, appealing to a tech-savvy generation of farmers. The nascent but promising segment of electric tractors is expected to gain momentum, fueled by environmental concerns, rising fuel costs, and supportive policy frameworks, potentially reshaping the market dynamics over the long term. Furthermore, the growth of rental and leasing models will expand market access to a wider base of small and marginal farmers, ensuring sustained demand. Strategic partnerships between domestic and international players, coupled with continuous product innovation focused on fuel efficiency, versatility, and operator comfort, will define the future competitive landscape, paving the way for substantial market potential and strategic opportunities for industry participants.

India Agricultural Tractor Market Segmentation

-

1. Type

- 1.1. Compact Tractors

- 1.2. Utility Tractors

- 1.3. Row Crop Tractors

- 1.4. Orchard Tractors

- 1.5. Specialty Tractors

-

2. Horse power

- 2.1. Less Than 40 HP

- 2.2. 40 HP to 150 HP

- 2.3. 151 HP to 250 HP

- 2.4. 251 HP to 350 HP

- 2.5. More Than 350 HP

-

3. Drive Type

- 3.1. 2 Wheel Drive

- 3.2. 4 Wheel Drive

-

4. Propulsion

- 4.1. Electric

- 4.2. ICE

-

5. Sales Channel

- 5.1. Direct Sales

- 5.2. Authorized Dealers and Distributors

India Agricultural Tractor Market Segmentation By Geography

- 1. India

India Agricultural Tractor Market Regional Market Share

Geographic Coverage of India Agricultural Tractor Market

India Agricultural Tractor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Compact Tractors

- 5.1.2. Utility Tractors

- 5.1.3. Row Crop Tractors

- 5.1.4. Orchard Tractors

- 5.1.5. Specialty Tractors

- 5.2. Market Analysis, Insights and Forecast - by Horse power

- 5.2.1. Less Than 40 HP

- 5.2.2. 40 HP to 150 HP

- 5.2.3. 151 HP to 250 HP

- 5.2.4. 251 HP to 350 HP

- 5.2.5. More Than 350 HP

- 5.3. Market Analysis, Insights and Forecast - by Drive Type

- 5.3.1. 2 Wheel Drive

- 5.3.2. 4 Wheel Drive

- 5.4. Market Analysis, Insights and Forecast - by Propulsion

- 5.4.1. Electric

- 5.4.2. ICE

- 5.5. Market Analysis, Insights and Forecast - by Sales Channel

- 5.5.1. Direct Sales

- 5.5.2. Authorized Dealers and Distributors

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Agricultural Tractor Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Compact Tractors

- 6.1.2. Utility Tractors

- 6.1.3. Row Crop Tractors

- 6.1.4. Orchard Tractors

- 6.1.5. Specialty Tractors

- 6.2. Market Analysis, Insights and Forecast - by Horse power

- 6.2.1. Less Than 40 HP

- 6.2.2. 40 HP to 150 HP

- 6.2.3. 151 HP to 250 HP

- 6.2.4. 251 HP to 350 HP

- 6.2.5. More Than 350 HP

- 6.3. Market Analysis, Insights and Forecast - by Drive Type

- 6.3.1. 2 Wheel Drive

- 6.3.2. 4 Wheel Drive

- 6.4. Market Analysis, Insights and Forecast - by Propulsion

- 6.4.1. Electric

- 6.4.2. ICE

- 6.5. Market Analysis, Insights and Forecast - by Sales Channel

- 6.5.1. Direct Sales

- 6.5.2. Authorized Dealers and Distributors

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Escorts Ltd.

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tractors and Farm Equipment Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mahindra & Mahindra Ltd.

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Deere & Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AGCO Corp.

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Iseki & Co. Ltd.

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Claas KGaA mbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Massey Ferguson

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 New Holland

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Qilu Machinery

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Case IH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 International Tractors Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 CNH Industrial N.V.

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Kubota Corp.

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Yanmar Co. Ltd.

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Others

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.1 Escorts Ltd.

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Agricultural Tractor Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Agricultural Tractor Market Share (%) by Company 2025

List of Tables

- Table 1: India Agricultural Tractor Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: India Agricultural Tractor Market Revenue Million Forecast, by Horse power 2020 & 2033

- Table 3: India Agricultural Tractor Market Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 4: India Agricultural Tractor Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 5: India Agricultural Tractor Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 6: India Agricultural Tractor Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: India Agricultural Tractor Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: India Agricultural Tractor Market Revenue Million Forecast, by Horse power 2020 & 2033

- Table 9: India Agricultural Tractor Market Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 10: India Agricultural Tractor Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 11: India Agricultural Tractor Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 12: India Agricultural Tractor Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Agricultural Tractor Market?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the India Agricultural Tractor Market?

Key companies in the market include Escorts Ltd., Tractors and Farm Equipment Limited, Mahindra & Mahindra Ltd., Deere & Company, AGCO Corp., Iseki & Co. Ltd., Claas KGaA mbH, Massey Ferguson, New Holland, Qilu Machinery, Case IH, International Tractors Ltd, CNH Industrial N.V., Kubota Corp., Yanmar Co., Ltd., Others.

3. What are the main segments of the India Agricultural Tractor Market?

The market segments include Type, Horse power, Drive Type, Propulsion, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.42 Million as of 2022.

5. What are some drivers contributing to market growth?

Mechanization Trend in Agriculture Sector; Trend of Custom Hiring of Tractors.

6. What are the notable trends driving market growth?

30-50 HP Tractors Are Widely Preferred.

7. Are there any restraints impacting market growth?

Lack of Awareness and Skilled Manpower; Poor Economic Condition of Farmers.

8. Can you provide examples of recent developments in the market?

April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, has MS Dhoni's signature as a symbol of gratitude to the customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Agricultural Tractor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Agricultural Tractor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Agricultural Tractor Market?

To stay informed about further developments, trends, and reports in the India Agricultural Tractor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence