Key Insights

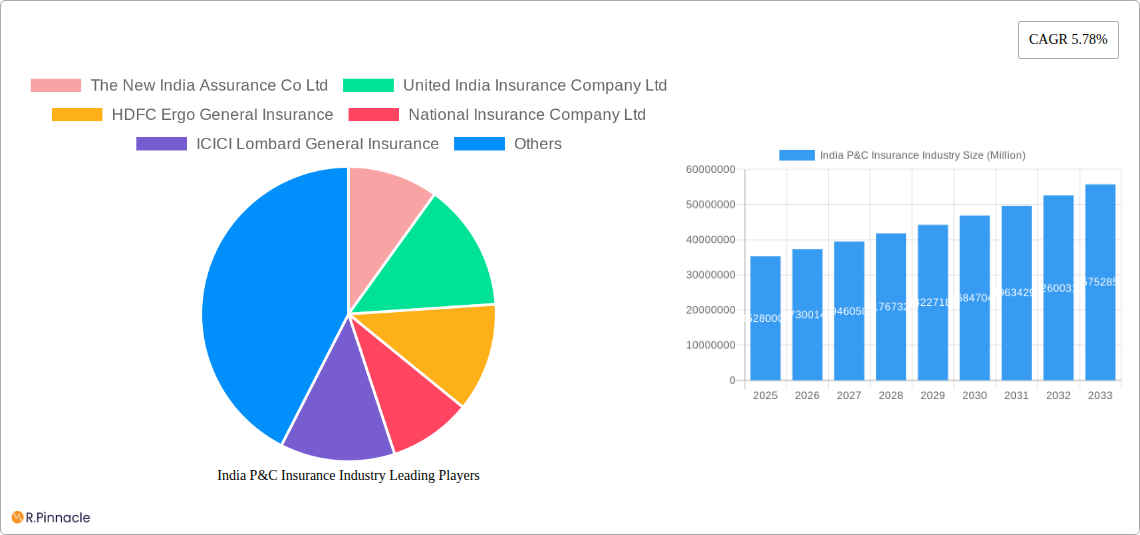

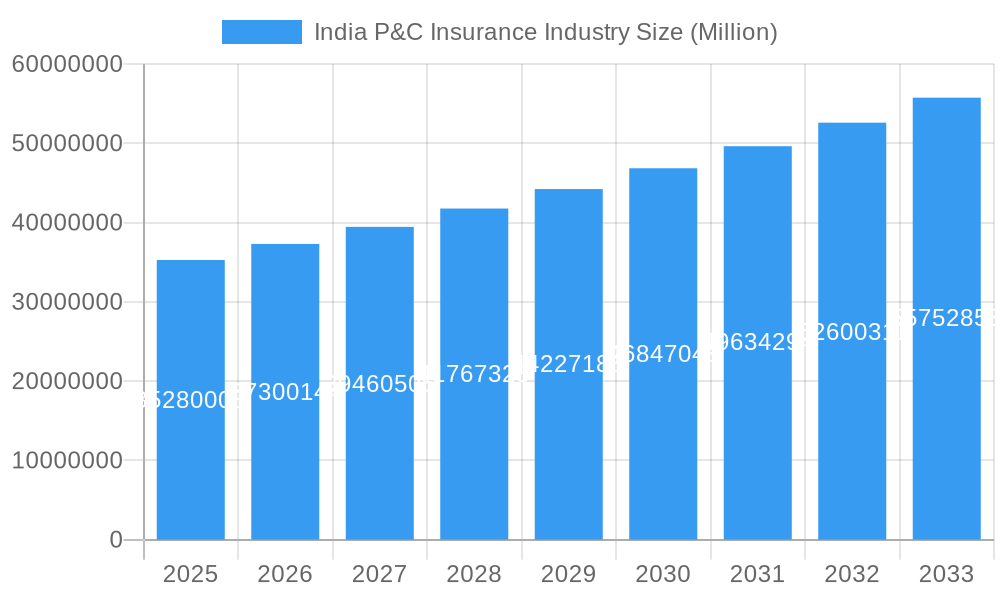

The Indian P&C (Property and Casualty) Insurance industry is poised for robust growth, projected to reach a market size of approximately USD 35.28 million by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 5.78% through 2033. This expansion is underpinned by a confluence of critical drivers, including increasing disposable incomes, growing awareness of insurance as a vital financial security tool, and a burgeoning middle class that seeks to protect its assets. The nation's rapid economic development, coupled with government initiatives promoting financial inclusion and insurance penetration, are further fueling this upward trajectory. Specifically, the motor insurance segment is expected to remain a dominant force, driven by rising vehicle ownership and stringent regulatory mandates. Simultaneously, the fire and engineering insurance sectors are witnessing accelerated demand due to increased infrastructure development and industrialization across the country. The shift towards digital platforms and enhanced customer engagement strategies by insurers are also playing a pivotal role in driving adoption and expanding the market reach.

India P&C Insurance Industry Market Size (In Million)

Further analysis reveals that the distribution landscape of the Indian P&C insurance market is dynamic and diversified. While traditional channels like agents and brokers continue to hold significant sway, there's a discernible and accelerating trend towards direct-to-consumer (DTC) models, propelled by digital insurance platforms and InsurTech innovations. Banks, acting as bancassurance partners, also represent a substantial distribution avenue, leveraging their extensive customer base. Micro-insurance agents are crucial in tapping into the rural and underserved populations, enhancing financial inclusion. The market is characterized by intense competition among established public sector insurers and agile private players, with companies like The New India Assurance, HDFC Ergo, and ICICI Lombard actively innovating to capture market share. Emerging trends also include a greater focus on personalized insurance products, data analytics for risk assessment, and the integration of IoT devices for proactive risk management, particularly in motor and engineering insurance segments. Challenges such as low insurance penetration in certain segments and the need for enhanced public awareness about the benefits of comprehensive P&C coverage remain areas of focus for sustained growth.

India P&C Insurance Industry Company Market Share

India P&C Insurance Industry: Market Analysis, Trends, and Forecast 2019-2033

This comprehensive report provides an in-depth analysis of the India P&C insurance industry, a rapidly evolving sector poised for significant growth. Leveraging advanced market research methodologies and incorporating high-ranking keywords such as "general insurance India," "non-life insurance market," "motor insurance India," "fire insurance India," and "insurtech India," this report is designed to equip industry professionals, investors, and stakeholders with actionable insights. We delve into the market structure, dynamics, segmentation, innovation trends, and future outlook, covering the period from 2019 to 2033, with a base year of 2025.

India P&C Insurance Industry Market Structure & Innovation Trends

The India P&C insurance industry exhibits a dynamic market structure characterized by both established public sector undertakings and a growing number of private players. Market concentration is moderate, with key players commanding significant market share. Innovation drivers are primarily centered around digital transformation, product customization, and enhanced customer experience, fueled by the proliferation of insurtech solutions. The regulatory framework, overseen by the Insurance Regulatory and Development Authority of India (IRDAI), plays a crucial role in shaping market conduct and solvency. Product substitutes are emerging with the growth of alternative risk management tools, while evolving end-user demographics, particularly a growing middle class and increasing digital literacy, are shaping demand. Merger and acquisition (M&A) activities are anticipated to increase as companies seek to expand their market reach and capabilities. For instance, in the historical period, M&A deals within the insurance sector are estimated to have seen transaction values in the hundreds of millions to billions of USD, aiming to consolidate market positions and acquire innovative technologies. The market is also witnessing strategic investments and partnerships aimed at enhancing operational efficiency and customer reach.

India P&C Insurance Industry Market Dynamics & Trends

The India P&C insurance market is projected to experience robust growth, driven by a confluence of economic, demographic, and technological factors. The CAGR (Compound Annual Growth Rate) of the market is estimated to be in the range of 12-15% during the forecast period. Market penetration, currently around 0.9-1.1% of GDP, is expected to rise significantly as insurance awareness and affordability increase. Key growth drivers include a burgeoning middle class with rising disposable incomes, increased awareness of risk management, and a growing need for protection against natural calamities and unforeseen events. The digital revolution is a paramount trend, with insurtech startups and established insurers investing heavily in digital platforms for sales, claims processing, and customer service. This technological disruption is leading to personalized products, faster claim settlements, and improved customer engagement. Consumer preferences are shifting towards simpler, more transparent, and digitally accessible insurance solutions. The competitive dynamics are intensifying, with both domestic and international players vying for market share. The increasing adoption of usage-based insurance and on-demand insurance models is further reshaping the competitive landscape, forcing insurers to be more agile and customer-centric. The penetration of motor insurance and health insurance remains high, while significant growth is expected in commercial insurance lines like engineering insurance and liability insurance due to increased industrialization and regulatory mandates. The market is also witnessing a surge in demand for specialized insurance products catering to emerging risks such as cyber threats and climate-related events.

Dominant Regions & Segments in India P&C Insurance Industry

The India P&C insurance industry is characterized by strong regional dynamics and segment dominance.

Dominant Region: While the entire nation presents significant opportunities, the Western and Southern regions of India currently lead in terms of premium collections and market penetration. This dominance is attributed to higher economic activity, greater urbanization, stronger financial literacy, and a more robust insurance distribution network in these areas. The presence of major industrial hubs and a higher concentration of affluent households contribute to the demand for a wide range of P&C insurance products.

Dominant Product Types:

- Motor Insurance: This segment consistently holds the largest market share due to mandatory third-party liability cover and the ever-increasing number of vehicles on Indian roads. The rising disposable incomes and growing preference for private vehicle ownership fuel its sustained dominance. Growth in electric vehicles is also creating new opportunities and challenges for this segment.

- Fire Insurance: Driven by the growth in the manufacturing sector, infrastructure development, and a heightened awareness of property protection against fire hazards, fire insurance remains a crucial segment. Government initiatives promoting industrial growth and disaster management also contribute to its importance.

- Other Product Types: This broad category encompasses significant growth potential from Engineering Insurance (tied to infrastructure development and industrial projects), Marine Insurance (boosted by India's extensive coastline and international trade), and Liability Insurance (as businesses become more aware of their legal obligations and risks).

Dominant Distribution Channels:

- Agents: Traditionally, the agency channel has been the backbone of insurance distribution in India, leveraging personal relationships and trust to reach a wider customer base, especially in semi-urban and rural areas.

- Banks (Bancassurance): Banks have emerged as a powerful distribution channel, offering insurance products alongside financial services. This channel benefits from the vast customer base and trust associated with banking institutions.

- Direct Businesses & Brokers: With increasing digitalization, direct online sales are gaining traction. Brokers play a vital role in the corporate segment, providing specialized advice and solutions. The growth of micro-insurance agents is crucial for increasing insurance penetration in the underserved segments of the population.

India P&C Insurance Industry Product Innovations

Product innovation in the India P&C insurance industry is increasingly driven by technological advancements and a deeper understanding of evolving customer needs. Insurers are developing more personalized and modular products, offering flexibility in coverage and premium. The integration of IoT devices is enabling innovative usage-based insurance models, particularly in motor and property insurance, rewarding safe behavior. Furthermore, the development of parametric insurance products, which pay out based on predefined triggers (e.g., weather events), is gaining traction for addressing specific risks like crop failure or natural disasters. Insurtech platforms are facilitating the creation of bundled products and simplifying the policy issuance and claims process, thereby enhancing competitive advantage by offering greater convenience and cost-effectiveness.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the India P&C Insurance Industry, segmented across key areas to offer granular insights.

- Product Type: The market is analyzed based on Fire Insurance, Marine Insurance, Aviation Insurance, Engineering Insurance, Motor Insurance, Liability Insurance, and Other Product Types. Each segment's growth projections and market sizes are detailed, with Motor Insurance expected to maintain its lead, followed by significant growth in Engineering Insurance and Liability Insurance due to economic expansion.

- Distribution Channel: The report examines the dominance and growth of Direct Businesses, Agents, Banks, Brokers, and Micro-Insurance Agents. The Bank and Direct Business channels are anticipated to show the highest growth rates, driven by digitalization and convenience. Agents will remain crucial for reach, while Micro-Insurance Agents are vital for financial inclusion.

Key Drivers of India P&C Insurance Industry Growth

The growth of the India P&C insurance industry is propelled by several factors. Economically, rising GDP, increasing disposable incomes, and robust industrial growth are fueling demand for protection. Technologically, the adoption of insurtech, AI, and data analytics is enhancing operational efficiency, enabling product innovation, and improving customer experience. Regulatory initiatives aimed at increasing insurance penetration and solvency also play a pivotal role. For instance, government policies promoting infrastructure development indirectly drive demand for engineering insurance, while mandatory regulations for vehicles boost motor insurance. A growing middle class with increasing awareness of risk management further contributes to market expansion.

Challenges in the India P&C Insurance Industry Sector

Despite its growth potential, the India P&C insurance industry faces several challenges. Regulatory hurdles, including evolving compliance requirements and pricing controls, can impact profitability. Distribution complexities, especially in reaching remote and underserved populations, remain a significant barrier. Intense competition from both established players and new entrants, including insurtechs, puts pressure on margins. Furthermore, rising claims from increasingly frequent extreme weather events and economic volatility pose underwriting and financial risks. The low level of insurance penetration in certain segments and segments like Aviation Insurance also represents a challenge, requiring concerted efforts in awareness and product development. Supply chain disruptions and economic slowdowns can directly impact premium collections, particularly for commercial lines of insurance.

Emerging Opportunities in India P&C Insurance Industry

Emerging opportunities in the India P&C insurance industry are diverse and significant. The rapid growth of the digital economy presents substantial opportunities for insurtech innovation, leading to the development of personalized, on-demand, and parametric insurance products. The increasing focus on sustainability and climate change is creating demand for specialized products like climate risk insurance and renewable energy insurance. The expansion of the gig economy and the rise of SMEs also present untapped markets for tailored insurance solutions. Furthermore, government initiatives promoting financial inclusion and digital adoption create fertile ground for innovative distribution models and products catering to previously underserved segments. The burgeoning Electric Vehicle (EV) market is opening up new avenues for specialized motor insurance products.

Leading Players in the India P&C Insurance Industry Market

The following companies are prominent players in the India P&C Insurance Industry Market:

- The New India Assurance Co Ltd

- United India Insurance Company Ltd

- HDFC Ergo General Insurance

- National Insurance Company Ltd

- ICICI Lombard General Insurance

- Bajaj Allianz General Insurance

- The Oriental Insurance Co Ltd

- Cholamandalam MS General Insurance Co Ltd

- IFFCO Tokio General Insurance Co Ltd

- Reliance General Insurance Co Ltd

- SBI General Insurance Co Ltd

Key Developments in India P&C Insurance Industry Industry

- March 2024: ICICI Lombard General Insurance acquired a 0.7% stake in Kotak Mahindra Bank for USD 2.92 billion. Concurrently, the company issued equity shares under its ICICI Lombard Employees Stock Option Scheme-2005, indicating confidence in its growth prospects.

- August 2023: HDFC ERGO partnered with Duck Creek Technologies to enhance its presence in the Indian insurance market. The collaboration involves implementing cloud-based SaaS solutions and employing a local workforce of approximately 1,000 people. This initiative aligns with Duck Creek's global market strategy and targets India's insurance industry, which is projected to reach USD 200 billion by 2027. Duck Creek established a new data center in India to support this expansion.

Future Outlook for India P&C Insurance Industry Market

The future outlook for the India P&C insurance industry is exceptionally positive, driven by sustained economic growth, increasing insurance penetration, and rapid digital adoption. The market is expected to continue its upward trajectory, fueled by a young demographic, rising incomes, and a greater awareness of risk management. Insurtech will play an increasingly pivotal role, driving innovation in product development, distribution, and claims management. Strategic collaborations, mergers, and acquisitions are likely to reshape the competitive landscape, leading to greater consolidation and specialization. The industry is well-positioned to capitalize on emerging trends such as climate resilience, cyber security, and the growth of the informal economy, offering significant strategic opportunities for market leaders and new entrants alike. The projected market size is expected to reach USD 150-200 billion by 2030, presenting a substantial opportunity for all stakeholders.

India P&C Insurance Industry Segmentation

-

1. Product Type

- 1.1. Fire Insurance

- 1.2. Marine Insurance

- 1.3. Aviation Insurance

- 1.4. Engineering Insurance

- 1.5. Motor Insurance

- 1.6. Liability Insurance

- 1.7. Other Product Types

-

2. Distribution Channel

- 2.1. Direct Businesses

- 2.2. Agents

- 2.3. Banks

- 2.4. Brokers

- 2.5. Micro-Insurance Agents

- 2.6. Other Distribution Channel

India P&C Insurance Industry Segmentation By Geography

- 1. India

India P&C Insurance Industry Regional Market Share

Geographic Coverage of India P&C Insurance Industry

India P&C Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Fire Insurance

- 5.1.2. Marine Insurance

- 5.1.3. Aviation Insurance

- 5.1.4. Engineering Insurance

- 5.1.5. Motor Insurance

- 5.1.6. Liability Insurance

- 5.1.7. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct Businesses

- 5.2.2. Agents

- 5.2.3. Banks

- 5.2.4. Brokers

- 5.2.5. Micro-Insurance Agents

- 5.2.6. Other Distribution Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. India P&C Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Fire Insurance

- 6.1.2. Marine Insurance

- 6.1.3. Aviation Insurance

- 6.1.4. Engineering Insurance

- 6.1.5. Motor Insurance

- 6.1.6. Liability Insurance

- 6.1.7. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct Businesses

- 6.2.2. Agents

- 6.2.3. Banks

- 6.2.4. Brokers

- 6.2.5. Micro-Insurance Agents

- 6.2.6. Other Distribution Channel

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 The New India Assurance Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 United India Insurance Company Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 HDFC Ergo General Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 National Insurance Company Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ICICI Lombard General Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bajaj Allianz General Insurance

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 The Oriental Insurance Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cholamandalam MS General Insurance Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 IFFCO Tokio General Insurance Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Reliance General Insurance Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SBI General Insurance Co Ltd**List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 The New India Assurance Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India P&C Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India P&C Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: India P&C Insurance Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: India P&C Insurance Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 3: India P&C Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: India P&C Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: India P&C Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: India P&C Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: India P&C Insurance Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: India P&C Insurance Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 9: India P&C Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: India P&C Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: India P&C Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: India P&C Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India P&C Insurance Industry?

The projected CAGR is approximately 5.78%.

2. Which companies are prominent players in the India P&C Insurance Industry?

Key companies in the market include The New India Assurance Co Ltd, United India Insurance Company Ltd, HDFC Ergo General Insurance, National Insurance Company Ltd, ICICI Lombard General Insurance, Bajaj Allianz General Insurance, The Oriental Insurance Co Ltd, Cholamandalam MS General Insurance Co Ltd, IFFCO Tokio General Insurance Co Ltd, Reliance General Insurance Co Ltd, SBI General Insurance Co Ltd**List Not Exhaustive.

3. What are the main segments of the India P&C Insurance Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.28 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Awareness of Insurance Benefits; Increased Asset Ownership is Expected to Drive Market Growth.

6. What are the notable trends driving market growth?

Growing Awareness of Insurance Products and Services is Driving the Market.

7. Are there any restraints impacting market growth?

Rising Awareness of Insurance Benefits; Increased Asset Ownership is Expected to Drive Market Growth.

8. Can you provide examples of recent developments in the market?

March 2024: ICICI Lombard General Insurance acquired a 0.7% stake in Kotak Mahindra Bank for USD 2.92 billion. Concurrently, the company issued equity shares under its ICICI Lombard Employees Stock Option Scheme-2005, indicating confidence in its growth prospects.August 2023: HDFC ERGO partnered with Duck Creek Technologies to enhance its presence in the Indian insurance market. The collaboration involves implementing cloud-based SaaS solutions and employing a local workforce of approximately 1,000 people. This initiative aligns with Duck Creek's global market strategy and targets India's insurance industry, which is projected to reach USD 200 billion by 2027. Duck Creek established a new data center in India to support this expansion.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India P&C Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India P&C Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India P&C Insurance Industry?

To stay informed about further developments, trends, and reports in the India P&C Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence