Key Insights

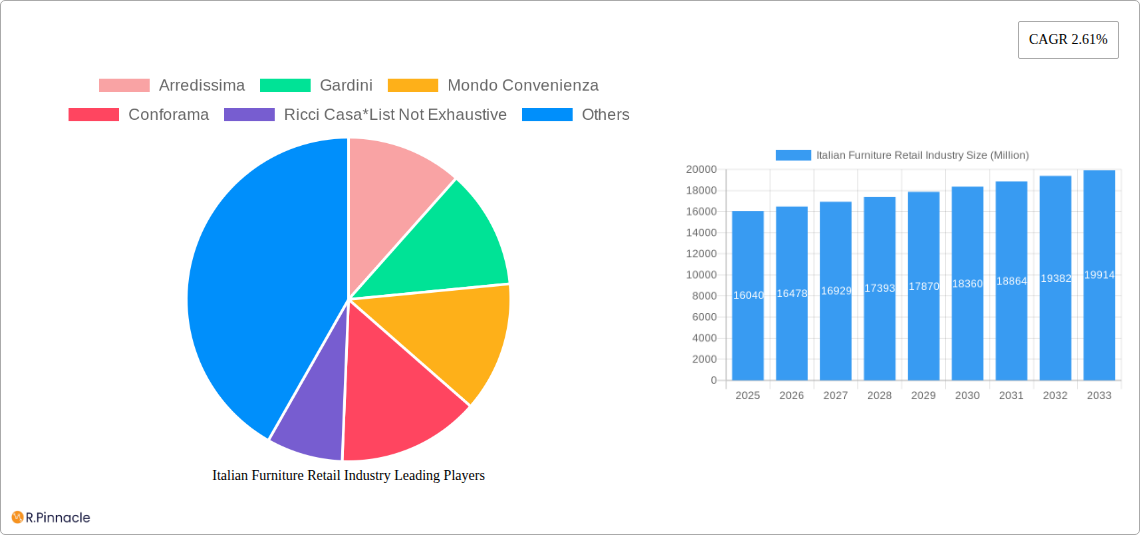

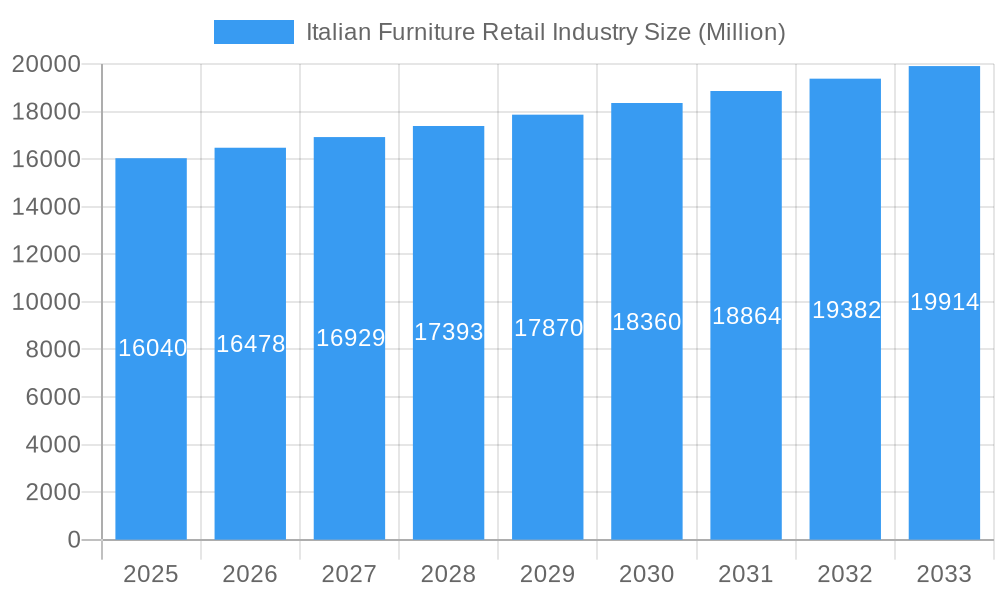

The Italian furniture retail industry, valued at €16.04 billion in 2025, is projected to experience steady growth, driven by a combination of factors. Rising disposable incomes, particularly amongst younger demographics, fuel demand for stylish and functional furniture. A growing preference for home improvement and renovation projects, spurred by increased remote work and a focus on creating comfortable living spaces, further contributes to market expansion. The industry is segmented across various furniture types, with bedroom, kitchen, and living room furniture dominating. Online distribution channels are rapidly gaining traction, challenging the established offline retail landscape. While the organized sector holds a significant share, the unorganized sector remains a considerable player, reflecting the diverse nature of the Italian market. Key players like IKEA, Mondo Convenienza, and Poltronesofa compete intensely, focusing on design innovation, competitive pricing, and effective marketing strategies to capture market share. The industry faces challenges including fluctuating raw material costs and evolving consumer preferences, necessitating agile adaptation and diversification.

Italian Furniture Retail Industry Market Size (In Billion)

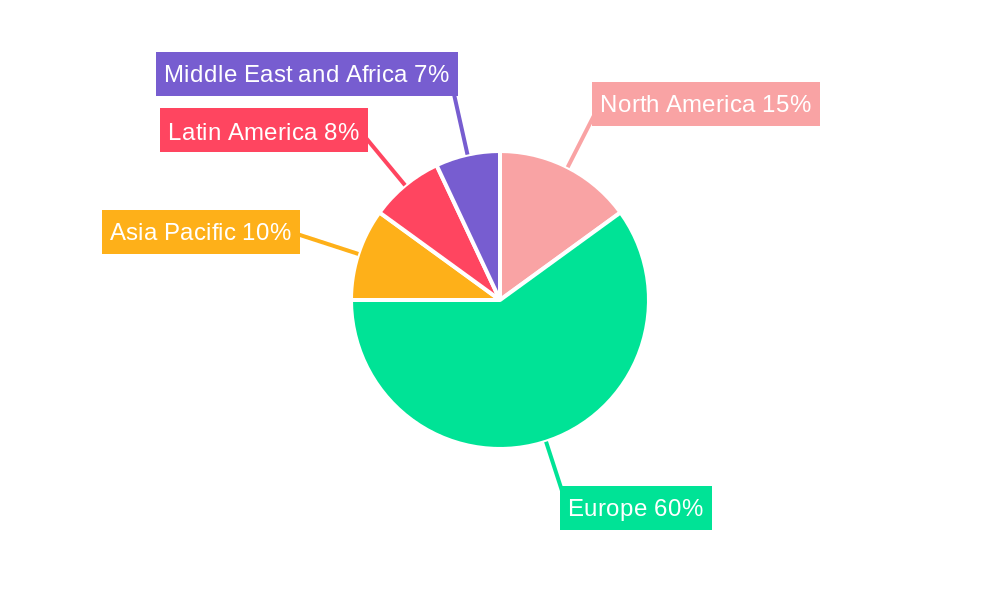

The forecast period (2025-2033) anticipates a continuation of moderate growth, with the CAGR of 2.61% suggesting a steady expansion. However, geopolitical uncertainties and potential economic downturns pose risks. To maintain growth, companies are likely to explore strategic partnerships, expand their online presence, and personalize their offerings to cater to niche customer segments. Growth will likely be driven by the continued rise in e-commerce adoption, increasing urbanization, and the introduction of innovative furniture designs integrating technology and sustainability. Regional variations exist; while Europe remains the largest market, Asia Pacific shows promising potential for future growth, fuelled by rising middle classes and increased awareness of Italian design. The industry's success hinges on balancing affordability with design appeal, catering to evolving consumer preferences, and adopting sustainable manufacturing practices to address growing environmental concerns.

Italian Furniture Retail Industry Company Market Share

Italian Furniture Retail Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Italian furniture retail industry, offering invaluable insights for industry professionals, investors, and strategic planners. With a study period spanning 2019-2033, a base year of 2025, and an estimated and forecast period of 2025-2033, this report leverages historical data (2019-2024) to project future market trends and opportunities. The Italian furniture market, valued at xx Million in 2024, is poised for significant growth, driven by factors detailed within this report.

Italian Furniture Retail Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape of the Italian furniture retail market, examining market concentration, innovation drivers, regulatory frameworks, and market dynamics. We explore the impact of product substitutes and end-user demographics on market growth, and delve into significant M&A activities within the sector.

Market Concentration: The Italian furniture market exhibits a mix of large multinational players like IKEA and JYSK, alongside established domestic brands such as Arredissima, Gardini, Mondo Convenienza, Conforama, and Ricci Casa. The market share distribution among these players is dynamic, with xx Million representing the approximate market value controlled by the top 5 players in 2024. Smaller, independent retailers also constitute a significant portion of the market.

Innovation Drivers: Innovation is driven by consumer demand for sustainable, technologically advanced, and customizable furniture. The integration of smart home technology and e-commerce platforms is transforming the industry, requiring retailers to adapt their strategies.

Regulatory Frameworks: EU regulations on product safety and environmental standards significantly impact the industry, influencing manufacturing processes and product design.

M&A Activity: While precise figures for M&A deal values are unavailable (xx Million estimated total for 2019-2024), activity has been moderate, driven primarily by consolidation within the sector and expansion into new markets.

Italian Furniture Retail Industry Market Dynamics & Trends

This section delves into the key dynamics shaping the Italian furniture retail market's growth trajectory. We analyze market growth drivers, technological disruptions, shifting consumer preferences, and the competitive landscape.

The Italian furniture retail market experienced a CAGR of xx% during the historical period (2019-2024). Key growth drivers include rising disposable incomes, urbanization, and a growing preference for aesthetically pleasing and functional home furnishings. Technological advancements, particularly in e-commerce and digital marketing, are reshaping the distribution landscape. Consumer preferences are shifting towards sustainable, ethically sourced products, and personalized design options. Intense competition necessitates strategic innovation and efficient operations for retailers to thrive. Market penetration of online channels is increasing steadily, though offline stores remain significant.

Dominant Regions & Segments in Italian Furniture Retail Industry

This section identifies the leading regions and segments within the Italian furniture retail market. Analysis considers geographic distribution, room furniture types, distribution channels, and market organization (organized vs. unorganized).

Dominant Regions: Northern Italy, particularly regions like Lombardy and Veneto, holds a significant share of the market due to established manufacturing clusters and high consumer spending.

Dominant Room Furniture Types: Living room and bedroom furniture represent the largest segments, followed by kitchen furniture. The outdoor furniture segment is experiencing growth, driven by increased demand for outdoor living spaces.

Dominant Distribution Channels: Although online sales are growing rapidly, offline channels, particularly large-format stores and specialized showrooms, still dominate the market.

Dominant Market Type: The organized sector, characterized by large retailers and established brands, holds a significant market share. However, the unorganized sector, comprising smaller, independent retailers, remains substantial.

Key Drivers:

- Strong domestic demand

- Tourism-related sales

- High concentration of manufacturers in certain regions

- Government incentives and support for the furniture industry.

Italian Furniture Retail Industry Product Innovations

The Italian furniture retail industry showcases ongoing innovation, with a focus on smart home integration, sustainable materials, and customizable designs. Technologically advanced furniture, including smart speakers integrated into furniture pieces (as seen with the IKEA and Sonos collaboration), is gaining traction. These innovations enhance user experience and offer unique selling propositions. The market is increasingly demanding eco-friendly materials and manufacturing processes, reflecting a growing awareness of environmental concerns.

Report Scope & Segmentation Analysis

This report segments the Italian furniture retail market by room furniture type (bedroom, kitchen, living/dining room, outdoor, and other), distribution channel (online and offline), and market type (organized and unorganized). Each segment’s growth projections, market size, and competitive dynamics are analyzed, providing a granular understanding of market opportunities. The market size for each segment is estimated at xx Million for 2025, with varying growth projections across segments.

Key Drivers of Italian Furniture Retail Industry Growth

Several factors contribute to the growth of the Italian furniture retail industry. Rising disposable incomes and urbanization are driving increased demand for home furnishings. Technological advancements such as e-commerce and improved logistics are streamlining distribution and enhancing customer experience. Government initiatives and support for the furniture industry further contribute to market expansion.

Challenges in the Italian Furniture Retail Industry Sector

The Italian furniture retail industry faces challenges such as intense competition, supply chain disruptions, and rising raw material costs. These factors impact profitability and necessitate efficient management of operations. Fluctuations in the global economy also impact consumer spending and market stability. The predicted impact on revenue in 2025 is a loss of approximately xx Million due to these challenges.

Emerging Opportunities in Italian Furniture Retail Industry

The Italian furniture retail industry presents significant opportunities. Expansion into new export markets, leveraging e-commerce for enhanced reach, and capitalizing on the growing demand for sustainable and personalized furniture designs offer lucrative avenues for growth. The incorporation of smart home technologies and innovative design elements opens new possibilities for market penetration.

Leading Players in the Italian Furniture Retail Industry Market

- Arredissima

- Gardini

- Mondo Convenienza

- Conforama

- Ricci Casa

- IKEA

- Canfalone

- Dotolo Mobili

- Poltronesofa

- JYSK

Key Developments in Italian Furniture Retail Industry

- April 2021: PayGlobe and Ingenico partner to enhance payment solutions for Mondo Convenienza, improving customer experience and operational efficiency.

- September 2021: IKEA and Sonos launch an updated version of their SYMFONISK table lamp speaker, showcasing innovation in smart home furniture.

Future Outlook for Italian Furniture Retail Industry Market

The Italian furniture retail market is expected to experience continued growth in the forecast period (2025-2033), driven by increasing consumer spending, technological advancements, and expanding e-commerce channels. Strategic investments in innovation, sustainable practices, and omnichannel strategies will be crucial for success. The market is projected to reach a value of xx Million by 2033.

Italian Furniture Retail Industry Segmentation

-

1. Room Furniture Type

- 1.1. Bedroom Furniture

- 1.2. Kitchen Furniture

- 1.3. Living Room and Dining Room Furniture

- 1.4. Outdoor Furniture and Other Furniture

-

2. Distribution Channel

- 2.1. Online

- 2.2. Offline

-

3. Type of Market

- 3.1. Organized

- 3.2. Unorganized

Italian Furniture Retail Industry Segmentation By Geography

- 1. Italia

Italian Furniture Retail Industry Regional Market Share

Geographic Coverage of Italian Furniture Retail Industry

Italian Furniture Retail Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.61% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Room Furniture Type

- 5.1.1. Bedroom Furniture

- 5.1.2. Kitchen Furniture

- 5.1.3. Living Room and Dining Room Furniture

- 5.1.4. Outdoor Furniture and Other Furniture

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Online

- 5.2.2. Offline

- 5.3. Market Analysis, Insights and Forecast - by Type of Market

- 5.3.1. Organized

- 5.3.2. Unorganized

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Italia

- 5.1. Market Analysis, Insights and Forecast - by Room Furniture Type

- 6. Italian Furniture Retail Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Room Furniture Type

- 6.1.1. Bedroom Furniture

- 6.1.2. Kitchen Furniture

- 6.1.3. Living Room and Dining Room Furniture

- 6.1.4. Outdoor Furniture and Other Furniture

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Online

- 6.2.2. Offline

- 6.3. Market Analysis, Insights and Forecast - by Type of Market

- 6.3.1. Organized

- 6.3.2. Unorganized

- 6.1. Market Analysis, Insights and Forecast - by Room Furniture Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Arredissima

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Gardini

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mondo Convenienza

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Conforama

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ricci Casa*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 IKEA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Canfalone

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Dotolo Mobili

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Poltronesofa

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 JYSK

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Arredissima

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italian Furniture Retail Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Italian Furniture Retail Industry Share (%) by Company 2025

List of Tables

- Table 1: Italian Furniture Retail Industry Revenue Million Forecast, by Room Furniture Type 2020 & 2033

- Table 2: Italian Furniture Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Italian Furniture Retail Industry Revenue Million Forecast, by Type of Market 2020 & 2033

- Table 4: Italian Furniture Retail Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Italian Furniture Retail Industry Revenue Million Forecast, by Room Furniture Type 2020 & 2033

- Table 6: Italian Furniture Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 7: Italian Furniture Retail Industry Revenue Million Forecast, by Type of Market 2020 & 2033

- Table 8: Italian Furniture Retail Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italian Furniture Retail Industry?

The projected CAGR is approximately 2.61%.

2. Which companies are prominent players in the Italian Furniture Retail Industry?

Key companies in the market include Arredissima, Gardini, Mondo Convenienza, Conforama, Ricci Casa*List Not Exhaustive, IKEA, Canfalone, Dotolo Mobili, Poltronesofa, JYSK.

3. What are the main segments of the Italian Furniture Retail Industry?

The market segments include Room Furniture Type, Distribution Channel, Type of Market.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.04 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Urbanization and Housing Sector; Home Improvement and Renovation Project.

6. What are the notable trends driving market growth?

Growing E-commerce Penetration is Driving the Market..

7. Are there any restraints impacting market growth?

High Competitive Market; Fluctuating Raw Material Cost.

8. Can you provide examples of recent developments in the market?

September 2021- IKEA and Sonos are launching a new version of the SYMFONISK table lamp speaker, with a better sound experience and updated, customizable designs. The original SYMFONISK table lamp speaker debuted in 2019, marking the first product developed by IKEA and Sonos.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italian Furniture Retail Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italian Furniture Retail Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italian Furniture Retail Industry?

To stay informed about further developments, trends, and reports in the Italian Furniture Retail Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence