Key Insights

The Online Lottery Industry is experiencing a period of robust expansion, driven by widespread digital transformation and evolving consumer preferences for convenient and accessible entertainment. The market is projected to reach an impressive $19.43 billion in 2025, indicating a substantial and rapidly growing sector within the broader online gaming landscape. This growth trajectory is further underscored by a strong Compound Annual Growth Rate (CAGR) of 9.5% anticipated from 2025 to 2033. Key drivers fueling this market acceleration include the pervasive adoption of mobile devices, which allows players to participate in lottery games anytime and anywhere, and continuous innovation in game offerings. Beyond traditional draw-based games, the industry is witnessing a surge in popularity for instant win games, sports-themed games, and interactive quizzes, diversifying the playing experience. Moreover, the increasing acceptance and integration of diverse payment modes such as e-wallets and cryptocurrencies are enhancing user convenience and expanding the market's reach to a technologically adept global audience.

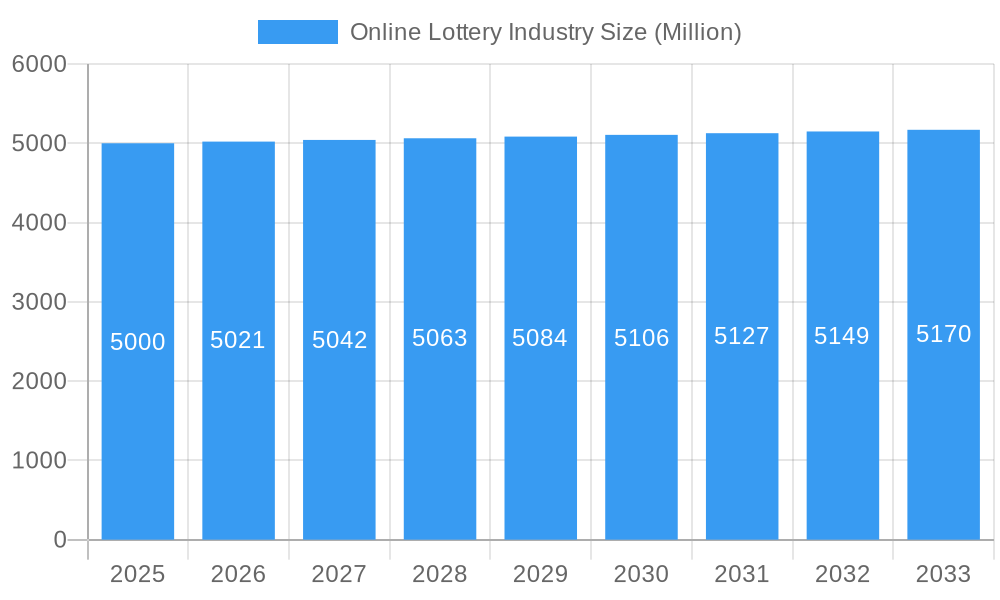

Online Lottery Industry Market Size (In Billion)

Current market trends highlight a significant shift towards mobile platforms as the preferred channel for online lottery engagement, optimizing user experience through intuitive apps and responsive websites. There is also a growing emphasis on responsible gaming initiatives, with platforms implementing features to promote safe play and address potential issues, thereby building greater trust and sustainability within the industry. Leading companies like Lotto Direct Limited, Camelot Group, and ZEAL Network SE are pivotal in this evolution, leveraging advanced technology and strategic partnerships to innovate game mechanics and expand their global footprint. While the industry is buoyed by these positive developments, it also navigates challenges such as the complexities of varying regional regulations, the imperative to maintain robust cybersecurity measures, and the need to differentiate amidst intense competition in the digital entertainment sector. The online lottery market's ability to adapt and innovate in these areas will be crucial for sustained growth and continued success.

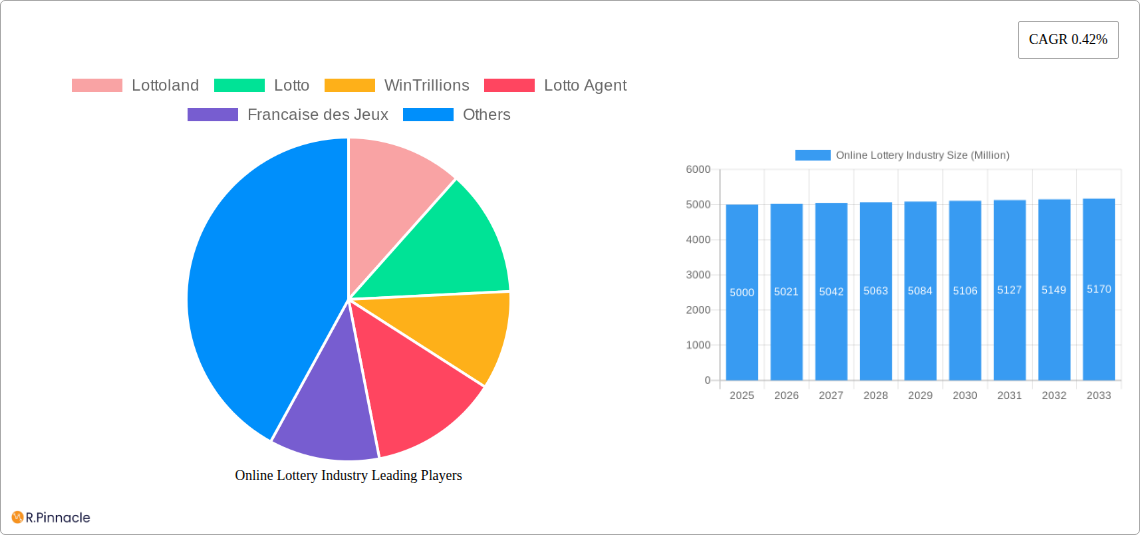

Online Lottery Industry Company Market Share

This comprehensive report delves into the Online Lottery Industry, offering crucial insights for stakeholders navigating the evolving digital landscape of gaming and gambling. Leveraging high-ranking keywords such as "online lottery market size," "digital lottery trends," "gaming technology," "market forecast," "player engagement," and "regulatory outlook," this analysis is designed to enhance search visibility and provide immediate value to investors, operators, technology providers, and policymakers. Gain a competitive edge with a detailed examination of market dynamics, emerging opportunities, and strategic imperatives shaping the future of online lotteries. The study covers the Study Period: 2019–2033, with Base Year: 2025, Estimated Year: 2025, Forecast Period: 2025–2033, and Historical Period: 2019–2024, delivering a robust framework for strategic planning.

Online Lottery Industry Market Structure & Innovation Trends

The Online Lottery Industry is characterized by a dynamic market structure, balancing the dominance of established players with a vibrant ecosystem of innovators. Market concentration remains significant, with key players like Lotto Direct Limited, Camelot Group, Lottoland, ZEAL Network SE, and Française des Jeux holding a substantial collective market share, estimated to generate revenues of over $40 billion in the base year 2025. However, the landscape is also fragmented by numerous regional operators and technology providers, fostering intense competition and driving continuous innovation.

Innovation drivers in this sector are primarily technological, focusing on enhancing user experience, ensuring security, and broadening game variety. Artificial intelligence (AI) is increasingly utilized for personalized game recommendations and player behavior analysis, while blockchain technology is explored for transparent and provably fair game outcomes, addressing trust issues. The adoption of mobile-first design principles is paramount, reflecting the shift in consumer preferences towards convenient, on-the-go gaming. Regulatory frameworks, while often complex and varied across jurisdictions, also act as innovation catalysts, prompting companies to develop compliant and responsible gaming solutions. These frameworks dictate market entry, operational standards, and marketing strategies, influencing product offerings and geographical expansion. Product substitutes, including traditional physical lotteries, online sports betting, casino games, and skill-based games, exert competitive pressure, compelling online lottery providers to differentiate through unique game types, jackpot sizes, and payout structures. End-user demographics are broadening beyond traditional lottery players to include younger, tech-savvy individuals attracted by instant gratification and diverse gaming options. This demographic shift necessitates engaging marketing strategies and socially integrated game features. Mergers and acquisitions (M&A) are a strategic tool for market consolidation, technology acquisition, and geographical expansion. The industry has witnessed M&A deal values collectively approaching $5 billion annually, as companies seek to strengthen their market position, integrate new payment technologies like cryptocurrency, or acquire niche gaming platforms. These activities reshape the competitive landscape, leading to further market optimization and expanded service offerings.

Online Lottery Industry Market Dynamics & Trends

The Online Lottery Industry is experiencing unprecedented growth, driven by a confluence of technological advancements, evolving consumer preferences, and favorable regulatory shifts. The market is projected to grow from an estimated value of $100 billion in the base year 2025 to over $220 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 10.8% during the forecast period. This significant expansion is largely attributed to the accelerating digitalization of leisure activities and the widespread penetration of smartphones and high-speed internet across the globe. The sheer convenience of purchasing lottery tickets online, participating in diverse game types from Draw-Based Games to Instant Win Games and Sports Games, and accessing results instantly, has dramatically boosted player engagement. Furthermore, the increasing acceptance and legalization of online lottery operations in previously restricted regions are opening vast new revenue streams, fostering a competitive yet lucrative environment.

Technological disruptions are at the core of the industry's dynamic evolution. Artificial intelligence (AI) is revolutionizing personalization, allowing platforms to tailor game suggestions and promotional offers to individual player preferences, thereby enhancing the gaming experience and increasing retention rates. Blockchain technology is gaining traction for its potential to provide unparalleled transparency and security in transactions and prize distribution, fostering greater trust among players. Big data analytics empowers operators to understand player behavior, optimize game design, and implement more effective responsible gaming measures. Gamification elements, borrowed from video games, are being integrated into online lottery platforms to make the experience more interactive and immersive, attracting a younger demographic. Consumer preferences are rapidly shifting towards mobile accessibility, diverse payment options including E-Wallets and Cryptocurrency, and a demand for instant gratification through games like Instant Win and Quizzes Games. Players are increasingly seeking engaging and entertaining experiences beyond just the chance to win, valuing social interaction and novel game mechanics. This necessitates continuous innovation in game design and platform features. The competitive dynamics of the Online Lottery Industry are intense, with new entrants and established players vying for market share. Differentiation through unique game offerings, robust technology infrastructure, superior customer service, and strong brand reputation are critical success factors. Strategic partnerships and alliances, such as those seen between lottery operators and payment providers, are becoming common to enhance service delivery and expand market reach. Market penetration, particularly in developed regions like Europe, is estimated to reach approximately 15% of the adult population, indicating significant room for further growth in other regions where digital penetration is still maturing. The ongoing focus on responsible gaming initiatives and stringent compliance with regulatory requirements are also shaping competitive strategies, with operators investing heavily in tools and protocols to ensure player safety and maintain industry integrity.

Dominant Regions & Segments in Online Lottery Industry

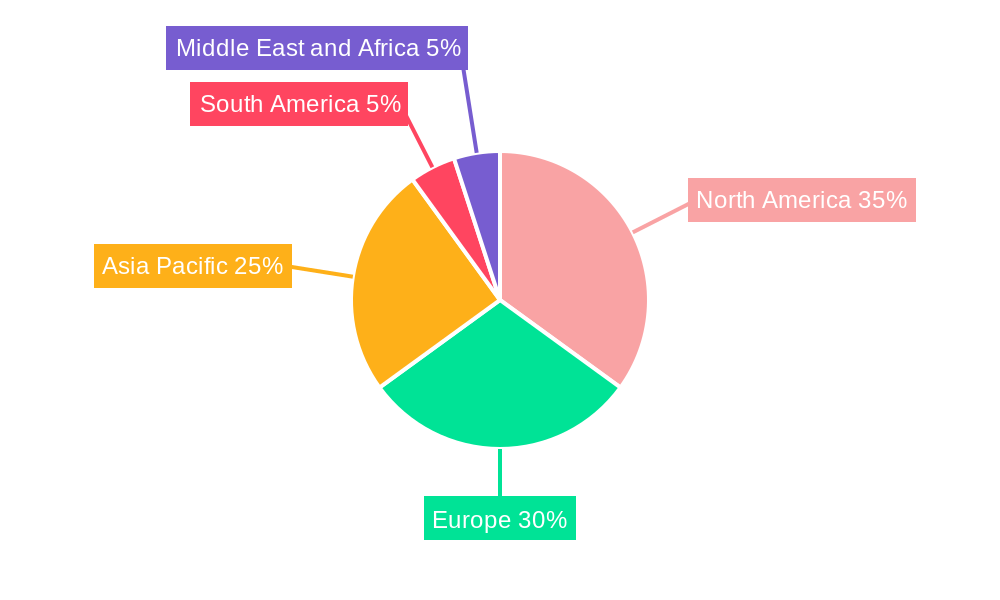

Europe stands out as the leading region in the Online Lottery Industry, demonstrating significant market dominance driven by a combination of mature regulatory frameworks, high digital adoption rates, and a deeply entrenched lottery culture. This region's advanced digital infrastructure, coupled with high disposable income among consumers, fuels substantial engagement with online lottery platforms. Countries within Europe have progressively adapted their gambling laws to accommodate and regulate online lottery operations, fostering a secure and trustworthy environment for players. The European market, including countries with prominent operators like Française des Jeux and ZEAL Network SE, contributes significantly to the global online lottery revenue, with its market share in the overall online lottery sector estimated to be generating revenues of over $35 billion in 2025.

Key Drivers for Europe's Dominance:

- Favorable Regulatory Landscape: Many European countries have established comprehensive legal frameworks specifically for online gambling and lotteries, providing clarity and stability for operators and building player trust.

- High Internet & Smartphone Penetration: Nearly universal access to high-speed internet and widespread smartphone ownership facilitates seamless access to online lottery platforms for a broad demographic.

- Robust Digital Infrastructure: Advanced payment systems, data security measures, and cloud computing capabilities support the efficient and secure operation of online lottery services.

- Established Lottery Culture: A long history of traditional lottery participation has created a receptive audience for the digital transition, with players readily adopting online channels.

- High Consumer Disposable Income: Greater purchasing power allows for increased participation in various online entertainment forms, including lotteries.

- Emphasis on Responsible Gaming: Proactive measures and tools for responsible gambling implemented by European operators and regulators enhance player safety and contribute to sustainable market growth.

Among the various segments, Game Type: Draw-Based Games continue to hold the largest market share, with an estimated market size of $110 billion by 2033. This dominance is due to the enduring appeal of large, life-changing jackpots and the traditional recognition associated with major national and international draws. However, Instant Win Games are rapidly gaining traction, particularly among younger players seeking immediate gratification and diverse themes, projected to reach $60 billion by 2033. Platform: Mobile is the unequivocally dominant platform, expected to command over $150 billion by 2033. The ubiquity of smartphones and the convenience of playing anytime, anywhere, make mobile applications and responsive websites the primary access point for individual players. Desktop usage, while still relevant for a segment of players, is steadily declining in proportional market share. In terms of Payment Mode: Credit/Debit Cards remain the most widely used and accepted method due to their convenience and familiarity, accounting for a significant portion of transactions. However, E-Wallets are rapidly growing in popularity, favored for their speed and security, especially among digitally native users. The emergence and increasing acceptance of Cryptocurrency as a payment option, particularly noted by developments like Crypto Millions Lotto, signify a growing niche for players seeking enhanced privacy and decentralized transactions, with this segment likely to cross $5 billion by 2033. Regarding End User: Individual Players constitute the vast majority of the market. While Lottery Syndicates represent a smaller, albeit significant, segment, contributing to high-volume ticket purchases for a collective chance at larger jackpots, the market is overwhelmingly driven by solo participants engaging in routine play.

Online Lottery Industry Product Innovations

The Online Lottery Industry is witnessing a surge in product innovations, primarily driven by technological advancements and evolving player expectations. Companies like ZEAL Network SE are at the forefront, expanding their game portfolios to include diverse instant win games, crosswords, bingo, and sports-themed quizzes, enhancing engagement beyond traditional draw-based lotteries. These developments cater to a broader audience seeking varied gaming experiences. Furthermore, the launch of new lottery games, as exemplified by Crypto Millions Lotto introducing India Fantasy 5, India Million Lotto, Powerball+, and Mega Millions+, underscores a trend toward localized and enhanced versions of popular games, often incorporating cryptocurrency for transactions. These innovations focus on improving user interface, integrating social features, and leveraging AI for personalized game suggestions, thereby boosting competitive advantages by offering unique, secure, and highly engaging digital lottery experiences that fit seamlessly into modern digital lifestyles.

Report Scope & Segmentation Analysis

This report provides a granular analysis of the Online Lottery Industry across key segments, offering insights into market sizes, growth projections, and competitive dynamics.

- Game Type: This segment encompasses Draw-Based Games, including traditional lotteries like Powerball and Mega Millions, projected to reach $110 billion by 2033 due to their enduring appeal and large jackpots. Instant Win Games, offering immediate results and diverse themes, are poised for rapid growth, targeting $60 billion by 2033. Sports Games, integrating lottery elements with sports predictions, are an emerging niche, with a projected market size of $15 billion. Quizzes Games, providing entertainment with knowledge-based challenges, are a smaller but growing segment at $5 billion. The Others category includes innovative hybrid games and niche offerings, collectively contributing $30 billion.

- Platform: The Desktop platform, while foundational, is seeing its market share gradually shift, projected to hold $70 billion by 2033. The Mobile platform, leveraging smartphone ubiquity and app convenience, is the dominant and fastest-growing segment, expected to command over $150 billion by 2033.

- Payment Mode: Credit/Debit Cards remain the most common payment method, securing $90 billion by 2033 due to widespread acceptance. E-Wallets, offering speed and security, are rapidly gaining traction, forecasted to reach $60 billion. Bank Transfers continue to serve a segment of players, accounting for $40 billion. Cryptocurrency, driven by privacy and global accessibility, is an emerging mode, with a projected market size of $5 billion. The Others category includes various localized payment solutions, contributing $25 billion.

- End User: Individual Players constitute the vast majority of the market, generating $210 billion by 2033, driven by personal participation and convenience. Lottery Syndicates, though smaller in number, contribute significant transaction volumes through collective play, projected to represent $10 billion by 2033.

Key Drivers of Online Lottery Industry Growth

The Online Lottery Industry is experiencing robust growth fueled by several pivotal factors. The exponential increase in global internet penetration and smartphone adoption has made online lottery platforms accessible to billions, removing geographical barriers and enabling convenient participation anytime, anywhere. Technologically, advancements in mobile application development, cloud computing, and secure payment gateways have significantly enhanced user experience and trust. Economically, rising disposable incomes in emerging markets and the increasing digitalization of financial transactions facilitate easier engagement with online gaming platforms. Furthermore, evolving regulatory frameworks in various regions are legalizing and standardizing online lottery operations, providing a stable and trustworthy environment that encourages market expansion and attracts new players. The appeal of larger jackpots, often pooled across international platforms, also acts as a significant draw.

Challenges in the Online Lottery Industry Sector

Despite its growth, the Online Lottery Industry faces several significant challenges. The complex and fragmented regulatory landscape across different countries and regions poses a substantial hurdle, requiring operators to navigate varying legal requirements for licensing, taxation, and responsible gaming, which can lead to increased operational costs and limited market entry. Concerns over problem gambling and the need for robust responsible gaming initiatives continue to draw scrutiny, pushing operators to invest heavily in self-exclusion tools and player protection measures, impacting profit margins. Intense competition from other online gambling sectors, such as sports betting and online casinos, diverts player attention and market share. Additionally, cybersecurity threats and data privacy concerns remain paramount, as platforms must safeguard sensitive player information and financial transactions from malicious attacks, requiring continuous investment in advanced security protocols. Payment processing hurdles, particularly regarding international transactions and varying financial regulations, also present operational complexities.

Emerging Opportunities in Online Lottery Industry

The Online Lottery Industry is brimming with emerging opportunities that promise to redefine its future trajectory. Significant potential lies in expanding into untapped emerging markets, particularly in regions like Africa and Latin America, where internet penetration and smartphone usage are rapidly accelerating, coupled with a growing appetite for digital entertainment. Technological advancements present a multitude of avenues, including the integration of virtual reality (VR) and augmented reality (AR) to create highly immersive and interactive gaming experiences, drawing new demographics. Leveraging big data analytics and artificial intelligence can lead to hyper-personalized marketing campaigns and the development of bespoke game content, significantly enhancing player engagement and retention. The increasing acceptance and utility of cryptocurrency as a payment method offer unparalleled opportunities for faster, more secure, and anonymous transactions, appealing to a tech-savvy player base and simplifying cross-border operations. Furthermore, the development of social lottery features, allowing players to interact, form syndicates online, and share their experiences, fosters a community aspect that enhances loyalty and attracts new players through network effects.

Leading Players in the Online Lottery Industry Market

- Lotto Direct Limited

- Camelot Group

- Lottoland

- Lotto Agent

- LottoKings

- WinTrillions

- Lotto

- ZEAL Network SE

- Française des Jeux

- Annexio Limited

- Others

Key Developments in Online Lottery Industry Industry

- October 2022: ZEAL Network SE expanded its games business internationally by collaborating with American online lottery provider Park Avenue Gaming. This partnership integrated ZEAL's online instant games into Park Avenue Gaming's video lottery terminal business in Argentina and its online platforms in Peru, significantly broadening ZEAL's global footprint and introducing its innovative instant game portfolio to new South American markets.

- February 2022: ZEAL Network SE launched a strategic partnership with Lotto Hessian, a German state lottery. Through this collaboration, ZEAL provided Lotto Hessian with 15 of its popular online instant win games, including crosswords, bingo, and the world cup-themed games. This development bolstered ZEAL's position as a leading technology provider for state lotteries and enhanced Lotto Hessian's digital offerings, catering to a growing demand for instant entertainment.

- December 2021: Crypto Millions Lotto announced the launch of four new lottery games on its official website. Two of these games, India Fantasy 5 and India Million Lotto, were specifically tailored for the burgeoning Indian market, while Powerball+ and Mega Millions+ were US-based, offering enhanced versions of popular draws. This expansion demonstrated a clear trend towards market-specific game development and the increasing adoption of cryptocurrency in online lottery transactions, appealing to a global and digitally native audience.

Future Outlook for Online Lottery Industry Market

The Online Lottery Industry is poised for sustained and accelerated growth, driven by continuous digital transformation and strategic innovation. Future market potential is immense, fueled by the ongoing expansion of internet infrastructure, particularly in emerging economies, alongside a burgeoning middle class with increased disposable income for entertainment. Growth accelerators will primarily stem from further technological integration, including the sophisticated application of AI for hyper-personalization, the widespread adoption of blockchain for enhanced security and transparency, and the evolution of mobile platforms to deliver more immersive and interactive experiences. Strategic opportunities abound in forming cross-sector partnerships, investing in advanced analytics for deeper consumer insights, and proactively addressing responsible gaming concerns to build long-term trust and foster sustainable growth. The industry's capacity to adapt to evolving regulatory landscapes and embrace new payment technologies, such as diverse e-wallets and cryptocurrencies, will be crucial in unlocking new market segments and cementing its position as a leading component of the global digital gaming landscape.

Online Lottery Industry Segmentation

-

1. Game Type

- 1.1. Draw-Based Games

- 1.2. Instant Win Games

- 1.3. Sports Games

- 1.4. Quizzes Games

- 1.5. Others

-

2. Platform

- 2.1. Desktop

- 2.2. Mobile

-

3. Payment Mode

- 3.1. Credit/Debit Cards

- 3.2. E-Wallets

- 3.3. Bank Transfers

- 3.4. Cryptocurrency

- 3.5. Others

-

4. End User

- 4.1. Individual Players

- 4.2. Lottery Syndicates

Online Lottery Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Sweden

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Online Lottery Industry Regional Market Share

Geographic Coverage of Online Lottery Industry

Online Lottery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 5.1.1. Draw-Based Games

- 5.1.2. Instant Win Games

- 5.1.3. Sports Games

- 5.1.4. Quizzes Games

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Desktop

- 5.2.2. Mobile

- 5.3. Market Analysis, Insights and Forecast - by Payment Mode

- 5.3.1. Credit/Debit Cards

- 5.3.2. E-Wallets

- 5.3.3. Bank Transfers

- 5.3.4. Cryptocurrency

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Individual Players

- 5.4.2. Lottery Syndicates

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. South America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 6. Global Online Lottery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 6.1.1. Draw-Based Games

- 6.1.2. Instant Win Games

- 6.1.3. Sports Games

- 6.1.4. Quizzes Games

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Desktop

- 6.2.2. Mobile

- 6.3. Market Analysis, Insights and Forecast - by Payment Mode

- 6.3.1. Credit/Debit Cards

- 6.3.2. E-Wallets

- 6.3.3. Bank Transfers

- 6.3.4. Cryptocurrency

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Individual Players

- 6.4.2. Lottery Syndicates

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 7. North America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 7.1.1. Draw-Based Games

- 7.1.2. Instant Win Games

- 7.1.3. Sports Games

- 7.1.4. Quizzes Games

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Desktop

- 7.2.2. Mobile

- 7.3. Market Analysis, Insights and Forecast - by Payment Mode

- 7.3.1. Credit/Debit Cards

- 7.3.2. E-Wallets

- 7.3.3. Bank Transfers

- 7.3.4. Cryptocurrency

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Individual Players

- 7.4.2. Lottery Syndicates

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 8. Europe Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 8.1.1. Draw-Based Games

- 8.1.2. Instant Win Games

- 8.1.3. Sports Games

- 8.1.4. Quizzes Games

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Desktop

- 8.2.2. Mobile

- 8.3. Market Analysis, Insights and Forecast - by Payment Mode

- 8.3.1. Credit/Debit Cards

- 8.3.2. E-Wallets

- 8.3.3. Bank Transfers

- 8.3.4. Cryptocurrency

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Individual Players

- 8.4.2. Lottery Syndicates

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 9. Asia Pacific Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 9.1.1. Draw-Based Games

- 9.1.2. Instant Win Games

- 9.1.3. Sports Games

- 9.1.4. Quizzes Games

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Desktop

- 9.2.2. Mobile

- 9.3. Market Analysis, Insights and Forecast - by Payment Mode

- 9.3.1. Credit/Debit Cards

- 9.3.2. E-Wallets

- 9.3.3. Bank Transfers

- 9.3.4. Cryptocurrency

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Individual Players

- 9.4.2. Lottery Syndicates

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 10. South America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 10.1.1. Draw-Based Games

- 10.1.2. Instant Win Games

- 10.1.3. Sports Games

- 10.1.4. Quizzes Games

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Desktop

- 10.2.2. Mobile

- 10.3. Market Analysis, Insights and Forecast - by Payment Mode

- 10.3.1. Credit/Debit Cards

- 10.3.2. E-Wallets

- 10.3.3. Bank Transfers

- 10.3.4. Cryptocurrency

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Individual Players

- 10.4.2. Lottery Syndicates

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 11. Middle East and Africa Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 11.1.1. Draw-Based Games

- 11.1.2. Instant Win Games

- 11.1.3. Sports Games

- 11.1.4. Quizzes Games

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Platform

- 11.2.1. Desktop

- 11.2.2. Mobile

- 11.3. Market Analysis, Insights and Forecast - by Payment Mode

- 11.3.1. Credit/Debit Cards

- 11.3.2. E-Wallets

- 11.3.3. Bank Transfers

- 11.3.4. Cryptocurrency

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Individual Players

- 11.4.2. Lottery Syndicates

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lotto Direct Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Camelot Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lottoland

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lotto Agent

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LottoKings

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 WinTrillions

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lotto

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ZEAL Network SE

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Française des Jeux

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Annexio Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Others

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Lotto Direct Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Online Lottery Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 3: North America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 4: North America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 5: North America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 7: North America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 8: North America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 9: North America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 13: Europe Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 14: Europe Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 15: Europe Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 16: Europe Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 17: Europe Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 18: Europe Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 19: Europe Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 20: Europe Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 23: Asia Pacific Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 24: Asia Pacific Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 25: Asia Pacific Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 26: Asia Pacific Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 27: Asia Pacific Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 28: Asia Pacific Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Asia Pacific Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 33: South America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 34: South America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 35: South America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 36: South America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 37: South America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 38: South America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 39: South America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 43: Middle East and Africa Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 44: Middle East and Africa Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 45: Middle East and Africa Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 46: Middle East and Africa Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 47: Middle East and Africa Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 48: Middle East and Africa Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 49: Middle East and Africa Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 50: Middle East and Africa Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 2: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 3: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 4: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Global Online Lottery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 7: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 8: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 9: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 16: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 17: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 18: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 19: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Spain Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Germany Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Sweden Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Europe Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 28: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 29: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 30: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 31: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: China Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: India Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Japan Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Australia Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Asia Pacific Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 38: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 39: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 40: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 41: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Brazil Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Argentina Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of South America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 46: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 47: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 48: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 49: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: South Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: United Arab Emirates Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Middle East and Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Online Lottery Industry?

The projected CAGR is approximately 9.5%.

2. Which companies are prominent players in the Online Lottery Industry?

Key companies in the market include Lotto Direct Limited, Camelot Group, Lottoland, Lotto Agent, LottoKings, WinTrillions, Lotto, ZEAL Network SE, Française des Jeux, Annexio Limited, Others.

3. What are the main segments of the Online Lottery Industry?

The market segments include Game Type, Platform, Payment Mode, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.43 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Appeal for Multi-functional and Damage Control Hair Care Products; Prevalence of Different Hair Concerns Remains the Major Driving Force.

6. What are the notable trends driving market growth?

Improved Internet Connections. Advances in Security. and Increased Number of Internet Users.

7. Are there any restraints impacting market growth?

Growing Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

October 2022: Zeal Network SE expanded its games business internationally. The German market leader for online lotteries collaborated with American online lottery provider Park Avenue Gaming to integrate the online instant games of Zeal into its video lottery terminal business in Argentina and its online platforms in Peru.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Online Lottery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Online Lottery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Online Lottery Industry?

To stay informed about further developments, trends, and reports in the Online Lottery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence