Key Insights

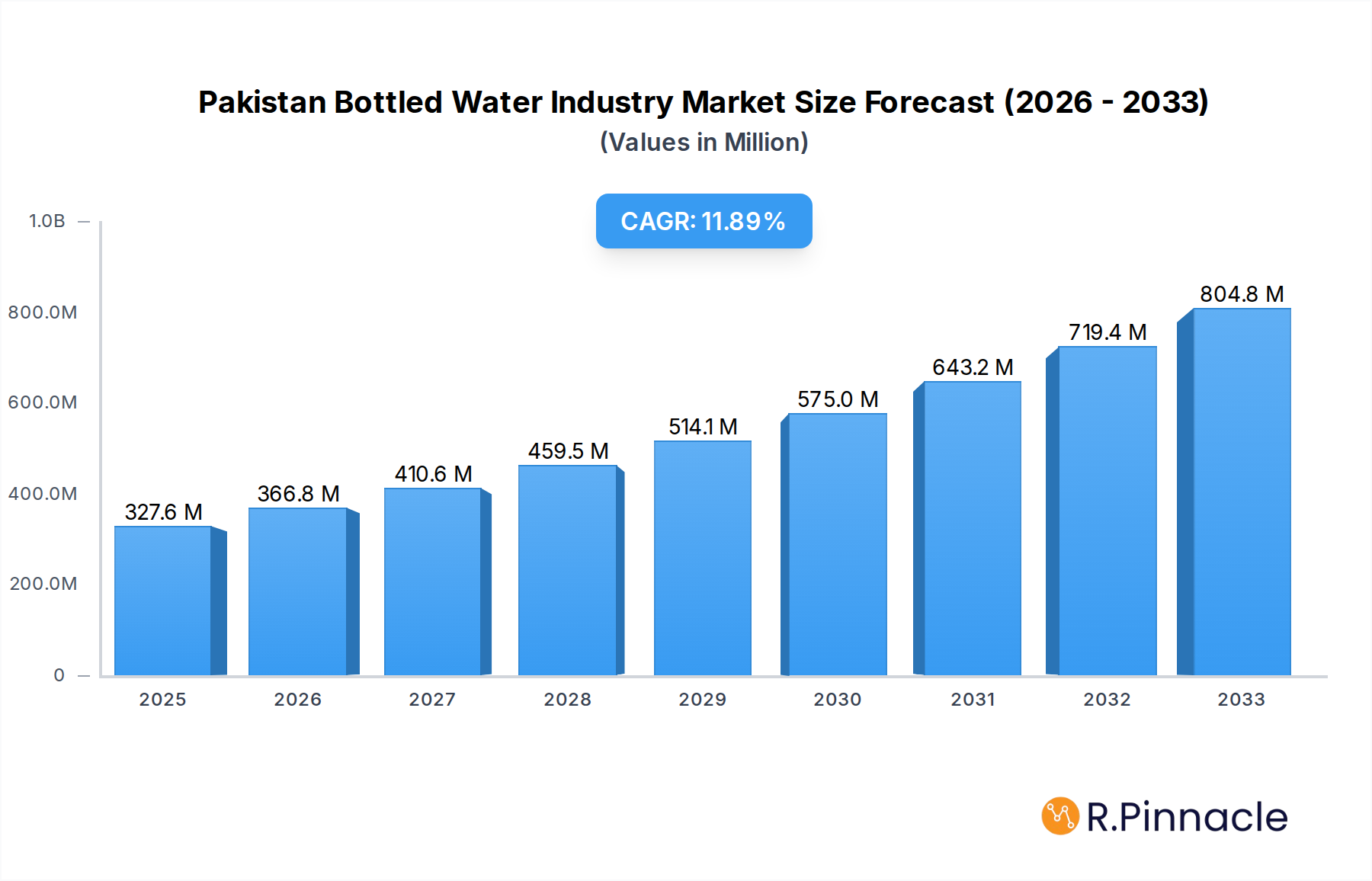

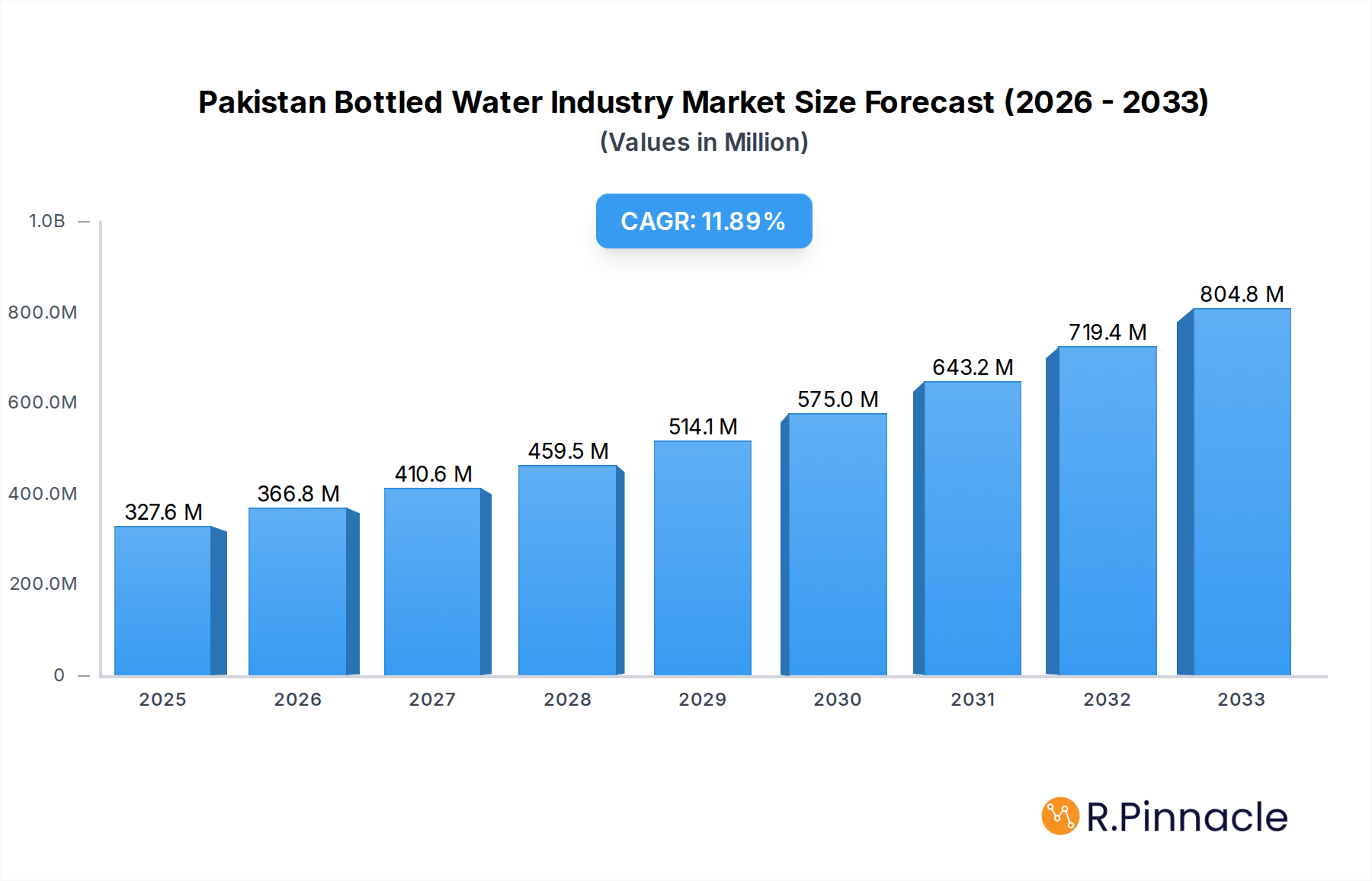

The Pakistan Bottled Water Industry is poised for substantial expansion, with a current market size of 327.61 Million and a projected Compound Annual Growth Rate (CAGR) of 11.96% over the forecast period of 2025-2033. This robust growth is fueled by several key drivers, including increasing urbanization, a rising disposable income, and growing consumer awareness regarding water quality and health. The convenience and perceived safety of bottled water, especially in a country where access to clean tap water can be inconsistent, make it an increasingly attractive option for households and individuals. Furthermore, the expanding modern retail infrastructure, encompassing supermarkets, hypermarkets, and online platforms, is enhancing product accessibility and driving sales. The Home and Office Delivery (HOD) segment is also witnessing significant traction as consumers prioritize convenience.

Pakistan Bottled Water Industry Market Size (In Million)

The market is broadly segmented into Still Water and Sparkling Water, with Still Water holding the dominant share due to established consumer preferences and affordability. However, Sparkling Water is anticipated to register a higher growth rate, driven by evolving consumer tastes and the introduction of flavored variants. Distribution channels are diverse, with Off-Trade channels, particularly supermarkets/hypermarkets and online retail stores, leading the market penetration. On-Trade channels also contribute, albeit to a lesser extent. Key players such as Nestle S.A., PepsiCo Inc., and The Coca-Cola Company are actively investing in expanding their production capacities, introducing innovative product lines, and strengthening their distribution networks to capitalize on the market's upward trajectory. Emerging companies are also entering the fray, intensifying competition and fostering product innovation.

Pakistan Bottled Water Industry Company Market Share

Here's an SEO-optimized, reader-centric report description for the Pakistan Bottled Water Industry, designed for engagement and search visibility:

Pakistan Bottled Water Industry Market Structure & Innovation Trends

The Pakistan bottled water industry, valued at over XX Million in 2025, presents a dynamic market structure with significant opportunities for growth. Market concentration is moderate, with key players like Nestlé S.A., PepsiCo Inc., and The Coca-Cola Company holding substantial shares, alongside robust local contenders such as Qarshi Industries (Pvt) Ltd and Sufi Group of Industries. Innovation is primarily driven by the demand for healthier beverage options, increased awareness of water quality, and the adoption of sustainable packaging solutions. Regulatory frameworks are evolving, with a growing emphasis on food safety standards and environmental compliance. Product substitutes, including tap water and other beverages, exert some pressure, but the convenience and perceived purity of bottled water continue to drive demand. End-user demographics are broad, encompassing urban populations seeking convenience, health-conscious individuals, and the hospitality sector. Merger and acquisition (M&A) activities, while not extensive, are indicative of strategic consolidation efforts, with recent deal values estimated in the range of XX Million.

- Market Concentration: Moderate, with a mix of multinational corporations and strong local players.

- Innovation Drivers: Health consciousness, water quality concerns, sustainable packaging.

- Regulatory Frameworks: Evolving focus on food safety and environmental sustainability.

- Product Substitutes: Tap water, other beverage categories.

- End-User Demographics: Urban consumers, health-conscious individuals, hospitality sector.

- M&A Activities: Strategic consolidation; estimated deal values XX Million.

Pakistan Bottled Water Industry Market Dynamics & Trends

The Pakistan bottled water industry is poised for substantial expansion, driven by a confluence of demographic, economic, and lifestyle shifts. The market's Compound Annual Growth Rate (CAGR) is projected to be robust, estimated at XX% between 2025 and 2033. This growth is underpinned by increasing urbanization, a rising disposable income, and a burgeoning middle class with a greater propensity to spend on convenient and perceived healthier hydration options. Technological advancements in water purification and bottling technologies are enabling manufacturers to produce higher quality products more efficiently, contributing to market penetration. Consumer preferences are increasingly leaning towards premiumized products, including flavored and functional waters, alongside a strong demand for still water. Competitive dynamics are characterized by intense brand advertising, promotional activities, and strategic distribution network expansions. The industry is also witnessing a growing emphasis on corporate social responsibility (CSR) initiatives related to water conservation and community access, which positively influences brand perception and market standing. The penetration of bottled water is steadily increasing, particularly in urban centers, as consumers prioritize safety and convenience over cost.

Dominant Regions & Segments in Pakistan Bottled Water Industry

The Pakistan bottled water industry exhibits distinct regional dominance and segment preferences, shaping its overall market landscape. Within Pakistan, the Punjab province consistently emerges as the leading region, driven by its high population density, extensive urbanization, and strong economic activity. The availability of robust infrastructure, including advanced distribution networks and significant retail penetration, further solidifies Punjab's position as the largest market for bottled water.

Among the product types, Still Water commands the largest market share. This dominance is attributed to its widespread appeal as a basic necessity, its suitability for everyday consumption, and the lower price point compared to sparkling or functional varieties. The increasing awareness of health and wellness also favors still water as a pure and unadulterated hydration source.

In terms of distribution channels, Off-Trade channels are the primary revenue generators. This segment is further broken down, with Supermarkets/Hypermarkets and Convenience Stores playing a pivotal role in catering to the daily hydration needs of consumers. The widespread presence of these retail outlets across urban and semi-urban areas ensures easy accessibility. Online Retail Stores are rapidly gaining traction, reflecting the growing e-commerce penetration in Pakistan and the consumer demand for convenient home delivery. Home and Office Delivery (HOD) services are also crucial, particularly for bulk purchases and regular replenishment, catering to both residential and corporate clients.

- Leading Region: Punjab, due to high population, urbanization, and economic activity.

- Key Drivers: Economic policies supporting consumer spending, well-developed retail infrastructure, extensive transportation networks.

- Dominant Product Type: Still Water, favored for its universal appeal and health perceptions.

- Key Drivers: Consumer preference for natural hydration, lower price point, widespread availability.

- Dominant Distribution Channel: Off-Trade, specifically Supermarkets/Hypermarkets and Convenience Stores.

- Key Drivers: High retail density, impulse purchase behavior, convenience-driven consumption.

- Growing Distribution Channel: Online Retail Stores and Home and Office Delivery (HOD), driven by e-commerce growth and demand for convenience.

Pakistan Bottled Water Industry Product Innovations

Product innovation in the Pakistan bottled water industry is increasingly focused on enhancing consumer appeal and meeting evolving lifestyle demands. Companies are actively developing flavored waters infused with natural fruit essences, catering to the growing preference for taste alongside hydration. Functional waters, enriched with vitamins, minerals, and electrolytes, are also gaining traction among health-conscious consumers seeking added health benefits. Furthermore, there's a significant push towards sustainable packaging solutions, with manufacturers exploring recyclable materials, lighter-weight bottles, and even plant-based alternatives to reduce environmental impact. These innovations offer distinct competitive advantages by differentiating brands, attracting niche consumer segments, and aligning with global sustainability trends.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Pakistan bottled water industry, segmenting the market by product type and distribution channel. The segmentation covers: Still Water and Sparkling Water under product type, and On Trade, Off-Trade (including Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, Home and Office Delivery (HOD), and Other Distribution Channels) under distribution channels.

For Still Water, projections indicate continued dominance with robust growth driven by its fundamental appeal as a healthy hydration choice. Sparkling Water, while a smaller segment, is expected to witness higher growth rates fueled by a growing consumer interest in premium and occasion-based beverages. In the distribution channels, Off-Trade segments, particularly Supermarkets/Hypermarkets and Convenience Stores, will maintain their leading positions due to accessibility. However, Online Retail Stores and Home and Office Delivery (HOD) are anticipated to experience the most significant growth, reflecting the digital transformation and evolving consumer convenience expectations.

Key Drivers of Pakistan Bottled Water Industry Growth

The Pakistan bottled water industry's growth is propelled by several key factors:

- Increasing Urbanization and Disposable Income: As more of the population moves to urban centers and disposable incomes rise, the demand for convenient and safe hydration options like bottled water escalates.

- Growing Health and Wellness Awareness: Consumers are increasingly conscious of their health and seek pure, safe drinking water, driving preference for bottled alternatives over potentially contaminated tap water.

- Expanding Retail Infrastructure: The proliferation of supermarkets, hypermarkets, and convenience stores across the country ensures wider accessibility and availability of bottled water.

- Technological Advancements: Improvements in purification technologies and efficient bottling processes contribute to the production of higher quality, safer, and more affordable bottled water.

- Corporate Social Responsibility (CSR) Initiatives: Companies' efforts in water conservation and providing clean water access enhance brand reputation and foster consumer trust.

Challenges in the Pakistan Bottled Water Industry Sector

Despite its growth potential, the Pakistan bottled water industry faces several challenges:

- Price Sensitivity and Affordability: A significant portion of the population remains price-sensitive, making affordability a key concern, especially for premium or specialized bottled water products.

- Regulatory Hurdles and Compliance Costs: Navigating evolving food safety regulations and environmental compliance standards can be complex and costly for manufacturers.

- Supply Chain Inefficiencies and Logistics: Ensuring consistent product availability across diverse geographical regions can be hampered by underdeveloped logistics and supply chain infrastructure.

- Environmental Concerns and Plastic Waste: Growing awareness and concern over plastic pollution pose a challenge, necessitating investment in sustainable packaging solutions and responsible waste management.

- Competition from Unorganized Sector: The presence of an unorganized sector offering lower-priced, often uncertified, bottled water creates competitive pressure and can impact market share for organized players.

Emerging Opportunities in Pakistan Bottled Water Industry

The Pakistan bottled water industry is ripe with emerging opportunities:

- Growth in Functional and Flavored Waters: Catering to the increasing consumer demand for enhanced health benefits and varied taste profiles presents a significant avenue for product differentiation and market expansion.

- Expansion into Tier-II and Tier-III Cities: Untapped potential exists in smaller cities and rural areas as incomes rise and awareness of water quality increases.

- E-commerce and Direct-to-Consumer (DTC) Models: Leveraging online platforms and establishing DTC channels can enhance reach, improve customer engagement, and offer personalized purchasing experiences.

- Sustainable Packaging Innovations: Investing in eco-friendly and recyclable packaging not only addresses environmental concerns but also resonates with a growing segment of environmentally conscious consumers.

- Strategic Partnerships and Collaborations: Collaborations with NGOs, government bodies, or other industries can help address water scarcity issues, enhance brand image, and explore new market segments.

Leading Players in the Pakistan Bottled Water Industry Market

- Qarshi Industries (Pvt) Ltd

- Nestle S A

- 3B Water Engineering & Services (Pvt) Ltd

- PepsiCo Inc

- PakTurk Bottlers

- Reignwood Investments UK Ltd (VOSS Water)

- Aqua Fujitenma Inc

- Danone S A

- Sufi Group of Industries

- The Coca-Cola Company

- Masafi LLC

Key Developments in Pakistan Bottled Water Industry Industry

- March 2022: PepsiCo collaborated with WaterAid to improve access to clean water for underserved urban communities in Pakistan, demonstrating a commitment to social impact and brand building.

- December 2021: Coca-Cola Beverages Pakistan Limited (CCI Pakistan) established a state-of-the-art water filtration plant in Haripur, Khyber Pakhtunkhwa, as part of its PAANI CSR project, highlighting a focus on community development and water accessibility.

Future Outlook for Pakistan Bottled Water Industry Market

The future outlook for the Pakistan bottled water industry is highly positive, driven by sustained economic growth, increasing consumer affluence, and a heightened focus on health and hygiene. The market is expected to witness continued expansion in both volume and value, with a growing emphasis on product diversification, including functional and premium offerings. Technological advancements in purification and sustainable packaging will play a crucial role in shaping the industry's trajectory. Furthermore, the growing penetration of online retail and direct-to-consumer models will revolutionize distribution strategies. Companies that prioritize product quality, environmental sustainability, and strong corporate social responsibility will be best positioned to capitalize on the abundant opportunities and achieve long-term success in this dynamic market.

Pakistan Bottled Water Industry Segmentation

-

1. Type

- 1.1. Still Water

- 1.2. Sparkling Water

-

2. Distribution Channel

- 2.1. On Trade

-

2.2. Off-Trade

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Convenience Stores

- 2.2.3. Online Retail Stores

- 2.2.4. Home and Office Delivery (HOD)

- 2.2.5. Other Distribution Channels

Pakistan Bottled Water Industry Segmentation By Geography

- 1. Pakistan

Pakistan Bottled Water Industry Regional Market Share

Geographic Coverage of Pakistan Bottled Water Industry

Pakistan Bottled Water Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Still Water

- 5.1.2. Sparkling Water

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On Trade

- 5.2.2. Off-Trade

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Convenience Stores

- 5.2.2.3. Online Retail Stores

- 5.2.2.4. Home and Office Delivery (HOD)

- 5.2.2.5. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Pakistan

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Pakistan Bottled Water Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Still Water

- 6.1.2. Sparkling Water

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On Trade

- 6.2.2. Off-Trade

- 6.2.2.1. Supermarkets/Hypermarkets

- 6.2.2.2. Convenience Stores

- 6.2.2.3. Online Retail Stores

- 6.2.2.4. Home and Office Delivery (HOD)

- 6.2.2.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Qarshi Industries (Pvt ) Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Nestle S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 3B Water Engineering & Services (Pvt) Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PepsiCo Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 PakTurk Bottlers

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Reignwood Investments UK Ltd (VOSS Water)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Aqua Fujitenma Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Danone S A

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sufi Group of Industries

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 The Coca-Cola Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Masafi LLC*List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Qarshi Industries (Pvt ) Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Pakistan Bottled Water Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Pakistan Bottled Water Industry Share (%) by Company 2025

List of Tables

- Table 1: Pakistan Bottled Water Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Pakistan Bottled Water Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Pakistan Bottled Water Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Pakistan Bottled Water Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Pakistan Bottled Water Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Pakistan Bottled Water Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pakistan Bottled Water Industry?

The projected CAGR is approximately 11.96%.

2. Which companies are prominent players in the Pakistan Bottled Water Industry?

Key companies in the market include Qarshi Industries (Pvt ) Ltd, Nestle S A, 3B Water Engineering & Services (Pvt) Ltd, PepsiCo Inc, PakTurk Bottlers, Reignwood Investments UK Ltd (VOSS Water), Aqua Fujitenma Inc, Danone S A, Sufi Group of Industries, The Coca-Cola Company, Masafi LLC*List Not Exhaustive.

3. What are the main segments of the Pakistan Bottled Water Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 327.61 Million as of 2022.

5. What are some drivers contributing to market growth?

Escalating Concern for Quality Drinking Water; Strategic Investment by the Key Players.

6. What are the notable trends driving market growth?

Escalating Concern for Quality Drinking Water.

7. Are there any restraints impacting market growth?

Need for Stringent Regulatory Landscape.

8. Can you provide examples of recent developments in the market?

March 2022: The global beverage and snack conglomerate PepsiCo collaborated with WaterAid in a bid to provide clean water to the masses of Pakistan. The company claimed that it is working to improve access to clean water for underserved urban communities in Pakistan.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pakistan Bottled Water Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pakistan Bottled Water Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pakistan Bottled Water Industry?

To stay informed about further developments, trends, and reports in the Pakistan Bottled Water Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence