Key Insights

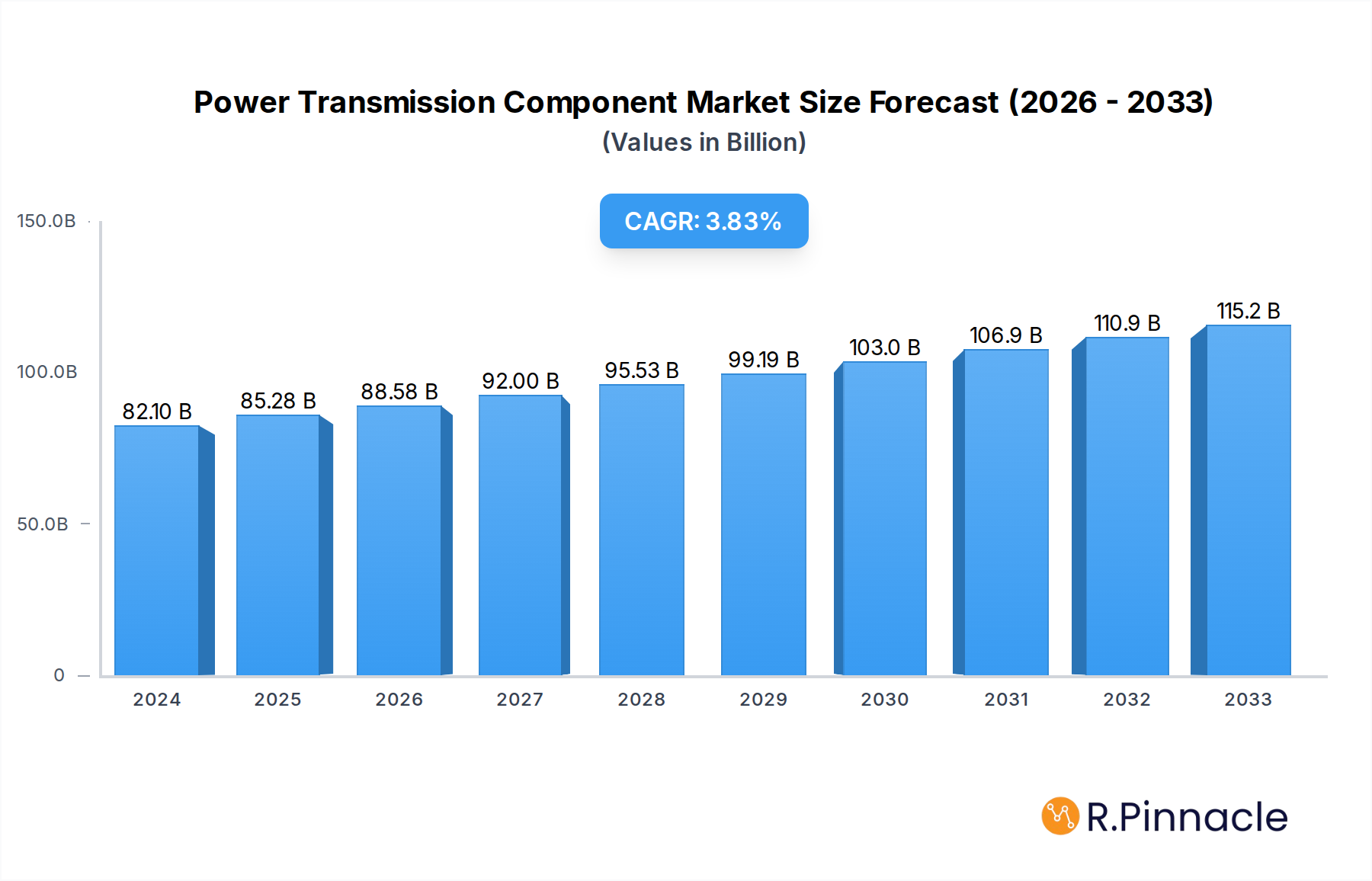

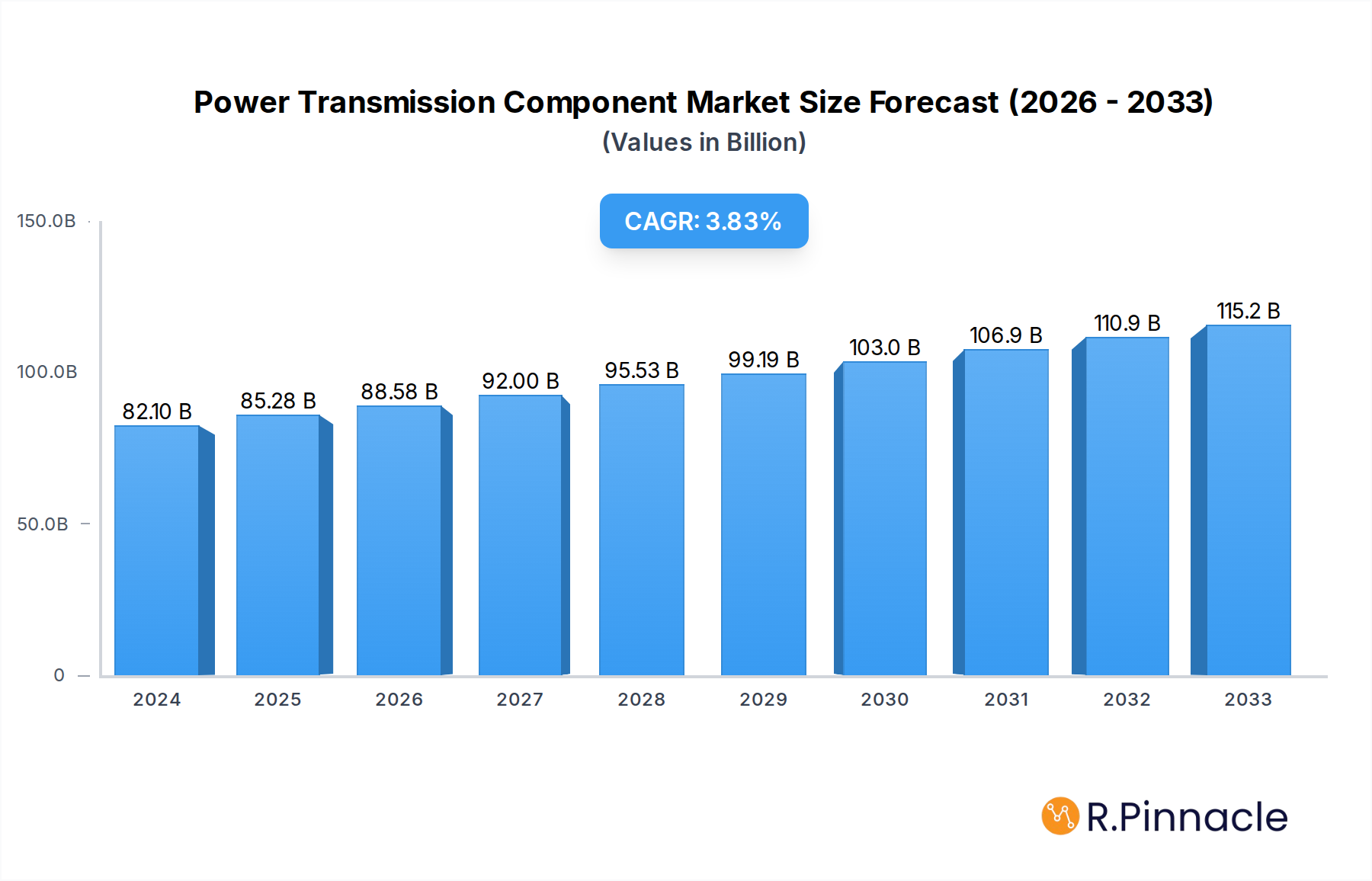

The global Power Transmission Component market is poised for significant expansion, projected to reach USD 82.1 billion in 2024 and demonstrating a healthy Compound Annual Growth Rate (CAGR) of 3.9% through 2033. This robust growth is primarily fueled by the escalating demand for reliable and efficient power transmission solutions across a multitude of sectors. Key drivers include the ongoing global investment in infrastructure development, particularly in renewable energy projects and the modernization of existing power grids. The increasing adoption of electric vehicles (EVs) and the subsequent need for enhanced charging infrastructure also contribute substantially to market expansion. Furthermore, industrial automation and the burgeoning demand for high-performance components in manufacturing, mining, and oil & gas operations are creating sustained market momentum. The market's trajectory is further bolstered by technological advancements, leading to the development of more durable, energy-efficient, and intelligent power transmission components.

Power Transmission Component Market Size (In Billion)

The Power Transmission Component market is characterized by a dynamic landscape shaped by evolving industry needs and technological innovation. While the market benefits from strong demand, it also faces certain restraints. Increasing raw material costs for critical components like metals and specialized plastics can impact profit margins. Additionally, stringent regulatory frameworks and the need for continuous upgrades to comply with evolving safety and environmental standards present challenges for manufacturers. Despite these hurdles, the market is actively addressing them through strategic initiatives. Companies are investing in research and development to optimize material usage and explore sustainable alternatives. The development of smart grid technologies, including advanced sensors and control systems, is another significant trend, enabling better monitoring, fault detection, and energy management. The competitive environment is intense, with major players like ABB, Siemens, and General Electric continuously innovating to offer advanced solutions and expand their global reach, particularly in emerging economies that represent significant untapped potential for power transmission infrastructure.

Power Transmission Component Company Market Share

Here is an SEO-optimized, reader-centric report description for the Power Transmission Component market, incorporating your specified details and structure:

Power Transmission Component Market Structure & Innovation Trends

The global Power Transmission Component market is characterized by a moderately concentrated structure, with leading players like ABB, Toshiba, EATON, Siemens, Crompton Greaves, General Electric, Hitachi, Schneider Electric, Mitsubishi, Hyundai, BHEL, Emerson, SKF, Freudenberg Sealing Technologies, Trelleborg, and Parker Hannifin holding significant market share. This report delves into the intricate market concentration, identifying the top-tier contributors and their respective shares, projected to be in the billions. Innovation is a primary driver, fueled by advancements in materials science, miniaturization, and energy efficiency. Regulatory frameworks, though evolving, aim to standardize safety and performance, influencing product development and market entry. The threat of product substitutes, while present in niche applications, is largely mitigated by the critical nature of reliable power transmission. End-user demographics are increasingly diverse, spanning industrial automation, renewable energy, electric vehicles, and aerospace, each with distinct performance requirements. Mergers and acquisitions (M&A) activity is a notable trend, with an estimated market value of over a billion in recent transactions, indicative of strategic consolidation and expansion efforts by key industry giants seeking to broaden their portfolios and technological capabilities.

Power Transmission Component Market Dynamics & Trends

The Power Transmission Component market is poised for robust expansion, driven by an escalating global demand for efficient and reliable power delivery across diverse sectors. The Compound Annual Growth Rate (CAGR) is estimated to be between 5.5% and 7.0%, signaling substantial market penetration in the coming years. Key growth drivers include the burgeoning renewable energy sector, requiring sophisticated transmission components for grid integration and distributed power generation. The rapid adoption of electric vehicles (EVs) necessitates high-performance, compact, and durable power transmission systems. Industrial automation, with its emphasis on enhanced productivity and reduced downtime, is another significant catalyst. Technological disruptions are at the forefront, with innovations in power electronics, smart grids, and advanced materials like composites and high-strength alloys shaping the future of transmission components. Consumer preferences are shifting towards energy-efficient, low-maintenance, and digitally integrated solutions, demanding components that offer real-time monitoring and predictive maintenance capabilities. The competitive dynamics are intensifying, with established players continuously investing in R&D to maintain their edge, while emerging companies are carving out niches through specialized product offerings and disruptive technologies. The market penetration for advanced power transmission components is projected to exceed 60% by 2033, reflecting a significant industry-wide shift. The total market value is anticipated to reach over one trillion by 2033.

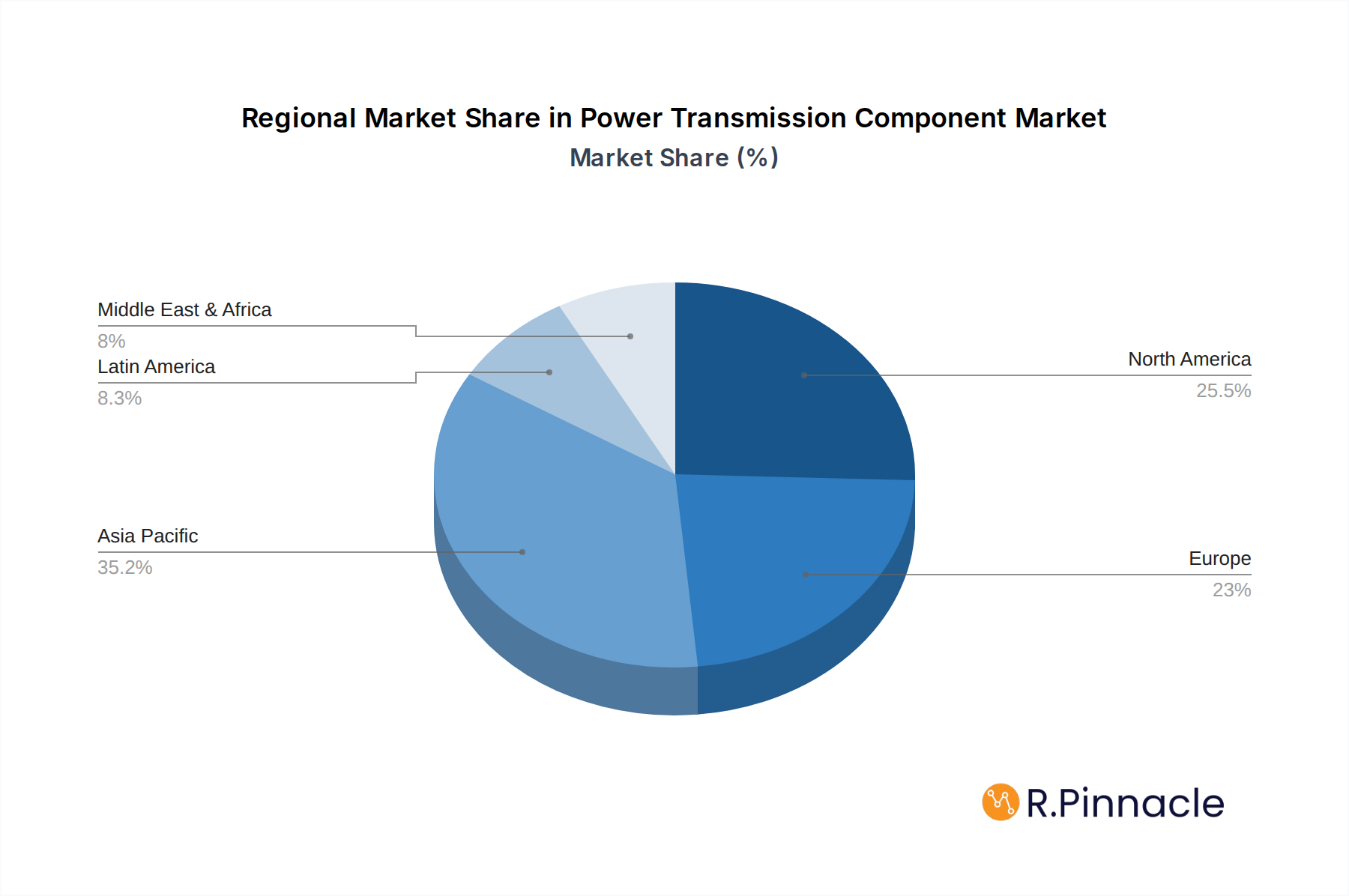

Dominant Regions & Segments in Power Transmission Component

North America and Europe currently dominate the global Power Transmission Component market, with a combined market share projected to be over 50% of the total market value, which is expected to exceed one trillion by 2033. This dominance is attributed to robust industrial infrastructure, significant investments in renewable energy projects, and stringent quality and performance standards. Within North America, the United States leads due to its advanced manufacturing capabilities and strong demand from the aerospace and automotive sectors, particularly in the electric vehicle segment. Economic policies promoting industrial modernization and grid upgrades further bolster this region's position. In Europe, Germany, France, and the UK are key contributors, driven by a strong focus on sustainable energy and advanced manufacturing technologies.

The Application: segment is largely dominated by the Industrial Automation sector, accounting for an estimated 35% of the market. This is driven by the increasing need for precise and reliable power transmission in manufacturing processes, robotics, and material handling systems. Key drivers include the Industry 4.0 revolution, emphasizing automation and connectivity. The Electric Vehicle application segment is experiencing exponential growth, projected to reach over 20% of the market by 2033. This surge is fueled by government mandates for EV adoption, advancements in battery technology, and consumer demand for sustainable transportation.

In terms of Type:, Electric Motors and Power Transmission Gearboxes collectively represent the largest share, estimated at over 40% of the market. Electric motors are fundamental to countless industrial and automotive applications, while gearboxes are crucial for efficient torque and speed management. The demand for high-efficiency motors and compact, robust gearboxes is a significant driver. The Couplings and Clutches segment is also substantial, estimated at over 15%, essential for connecting and controlling power flow. Growth in this segment is driven by the need for vibration dampening and overload protection.

Power Transmission Component Product Innovations

Recent product innovations in the Power Transmission Component market are centered on enhancing efficiency, durability, and intelligent integration. Developments include lightweight and high-strength composite materials for reduced energy consumption and improved performance, particularly in aerospace and automotive applications. Smart components with integrated sensors for predictive maintenance and real-time performance monitoring are gaining traction. The miniaturization of power transmission systems is also a key trend, enabling more compact and powerful designs for electric vehicles and portable industrial equipment. These innovations offer significant competitive advantages by reducing operational costs, increasing reliability, and enabling advanced functionalities.

Report Scope & Segmentation Analysis

This comprehensive report offers an in-depth analysis of the global Power Transmission Component market from 2019 to 2033. The market is meticulously segmented by Application:, including Industrial Automation, Electric Vehicles, Renewable Energy, Aerospace, and Others. The Industrial Automation segment is expected to maintain its leading position throughout the forecast period, driven by widespread adoption of automated processes. The Electric Vehicle segment is projected for the highest growth rate, fueled by global EV adoption trends.

Further segmentation by Type: encompasses Electric Motors, Power Transmission Gearboxes, Couplings and Clutches, Bearings, and Others. The Electric Motors and Gearboxes segments are anticipated to hold the largest market share. Growth in the Bearings segment is driven by demand for high-precision and long-life solutions across various industries. Market sizes for each segment are projected in billions, with detailed growth forecasts and competitive analyses provided.

Key Drivers of Power Transmission Component Growth

The Power Transmission Component market is propelled by several powerful growth drivers. Technologically, the relentless pursuit of energy efficiency across all sectors is paramount, leading to demand for advanced motors, gearboxes, and control systems. The global push for renewable energy integration necessitates robust and adaptable transmission components for efficient power distribution. Economically, increasing industrialization and infrastructure development in emerging economies are creating significant demand. Furthermore, the rapid expansion of the electric vehicle (EV) market is a major catalyst, requiring specialized and high-performance power transmission solutions. Government initiatives and supportive policies aimed at promoting green energy and advanced manufacturing also play a crucial role in driving market growth.

Challenges in the Power Transmission Component Sector

Despite robust growth, the Power Transmission Component sector faces several significant challenges. Intensifying global competition among established players and emerging manufacturers exerts downward pressure on pricing. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production timelines and costs, with potential impacts in the billions. Stringent regulatory compliances related to safety, emissions, and energy efficiency require continuous investment in R&D and product modifications. The high initial investment cost for advanced power transmission systems can be a barrier for smaller enterprises, limiting market penetration in certain segments. Furthermore, the pace of technological obsolescence necessitates constant innovation and product upgrades to remain competitive.

Emerging Opportunities in Power Transmission Component

The Power Transmission Component market is ripe with emerging opportunities, driven by technological advancements and evolving market needs. The burgeoning smart grid infrastructure presents a significant opportunity for components that support advanced grid management and energy storage solutions. The continued growth of electrified transportation, including not only passenger vehicles but also commercial trucks and industrial machinery, offers substantial expansion potential. Innovations in advanced materials, such as lightweight composites and self-healing materials, can lead to the development of more durable and efficient components. The increasing focus on Industry 5.0, emphasizing human-robot collaboration and customization, will drive demand for highly adaptable and intelligent power transmission systems. Furthermore, the development of sustainable and recyclable power transmission components aligns with global environmental consciousness and presents a growing market niche.

Leading Players in the Power Transmission Component Market

- ABB

- Toshiba

- EATON

- Siemens

- Crompton Greaves

- General Electric

- Hitachi

- Schneider Electric

- Mitsubishi

- Hyundai

- BHEL

- Emerson

- SKF

- Freudenberg Sealing Technologies

- Trelleborg

- Parker Hannifin

Key Developments in Power Transmission Component Industry

- 2023/09: Siemens announced the acquisition of a leading provider of advanced automation software, bolstering its industrial digital solutions portfolio, valued at approximately $1.5 billion.

- 2023/07: ABB launched a new generation of high-efficiency electric motors designed for industrial applications, targeting a significant reduction in energy consumption and operational costs.

- 2023/05: EATON unveiled its latest range of power distribution units for electric vehicles, enhancing charging speed and grid integration capabilities, with an estimated market impact of hundreds of millions.

- 2022/11: Schneider Electric expanded its smart grid offerings with the introduction of new intelligent transmission components, facilitating enhanced grid resilience and remote monitoring.

- 2022/08: General Electric announced significant investments in R&D for advanced materials in turbine components, aiming to improve efficiency and lifespan.

- 2022/04: Hyundai Heavy Industries unveiled a new series of electric powertrains for commercial vehicles, signaling a strong commitment to the growing EV market.

Future Outlook for Power Transmission Component Market

The future outlook for the Power Transmission Component market is exceptionally promising, driven by a confluence of technological advancements, sustainability mandates, and burgeoning global demand. The ongoing transition towards electrification across multiple sectors, from transportation to industrial processes, will continue to be a primary growth accelerator. Investments in smart grid technologies and renewable energy infrastructure are expected to surge, requiring sophisticated and reliable power transmission solutions. The demand for highly efficient, intelligent, and durable components will escalate, pushing innovation in areas like advanced materials, IoT integration for predictive maintenance, and miniaturization. Strategic opportunities lie in addressing the unique requirements of emerging markets and developing customized solutions for nascent applications, ensuring the market's continued expansion into the trillions.

Power Transmission Component Segmentation

-

1. Application

- 1.1. undefined

-

2. Type

- 2.1. undefined

Power Transmission Component Segmentation By Geography

- 1. undefined

- 2. undefined

- 3. undefined

- 4. undefined

- 5. undefined

Power Transmission Component Regional Market Share

Geographic Coverage of Power Transmission Component

Power Transmission Component REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1.

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1.

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1.

- 5.3.2.

- 5.3.3.

- 5.3.4.

- 5.3.5.

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. undefined Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1.

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1.

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. undefined Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1.

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1.

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. undefined Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1.

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1.

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. undefined Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1.

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1.

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. undefined Power Transmission Component Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1.

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1.

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ABB

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Toshiba

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 EATON

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Siemens

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Crompton Greaves

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 General Electric

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hitachi

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Schneider Electric

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Mitsubishi

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Hyundai

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BHEL

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Emerson

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 SKF

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Freudenberg Sealing Technologies

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Trelleborg

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Parker Hannifin

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 ABB

List of Figures

- Figure 1: Global Power Transmission Component Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Power Transmission Component Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: undefined Power Transmission Component Revenue (billion), by Application 2025 & 2033

- Figure 4: undefined Power Transmission Component Volume (K), by Application 2025 & 2033

- Figure 5: undefined Power Transmission Component Revenue Share (%), by Application 2025 & 2033

- Figure 6: undefined Power Transmission Component Volume Share (%), by Application 2025 & 2033

- Figure 7: undefined Power Transmission Component Revenue (billion), by Type 2025 & 2033

- Figure 8: undefined Power Transmission Component Volume (K), by Type 2025 & 2033

- Figure 9: undefined Power Transmission Component Revenue Share (%), by Type 2025 & 2033

- Figure 10: undefined Power Transmission Component Volume Share (%), by Type 2025 & 2033

- Figure 11: undefined Power Transmission Component Revenue (billion), by Country 2025 & 2033

- Figure 12: undefined Power Transmission Component Volume (K), by Country 2025 & 2033

- Figure 13: undefined Power Transmission Component Revenue Share (%), by Country 2025 & 2033

- Figure 14: undefined Power Transmission Component Volume Share (%), by Country 2025 & 2033

- Figure 15: undefined Power Transmission Component Revenue (billion), by Application 2025 & 2033

- Figure 16: undefined Power Transmission Component Volume (K), by Application 2025 & 2033

- Figure 17: undefined Power Transmission Component Revenue Share (%), by Application 2025 & 2033

- Figure 18: undefined Power Transmission Component Volume Share (%), by Application 2025 & 2033

- Figure 19: undefined Power Transmission Component Revenue (billion), by Type 2025 & 2033

- Figure 20: undefined Power Transmission Component Volume (K), by Type 2025 & 2033

- Figure 21: undefined Power Transmission Component Revenue Share (%), by Type 2025 & 2033

- Figure 22: undefined Power Transmission Component Volume Share (%), by Type 2025 & 2033

- Figure 23: undefined Power Transmission Component Revenue (billion), by Country 2025 & 2033

- Figure 24: undefined Power Transmission Component Volume (K), by Country 2025 & 2033

- Figure 25: undefined Power Transmission Component Revenue Share (%), by Country 2025 & 2033

- Figure 26: undefined Power Transmission Component Volume Share (%), by Country 2025 & 2033

- Figure 27: undefined Power Transmission Component Revenue (billion), by Application 2025 & 2033

- Figure 28: undefined Power Transmission Component Volume (K), by Application 2025 & 2033

- Figure 29: undefined Power Transmission Component Revenue Share (%), by Application 2025 & 2033

- Figure 30: undefined Power Transmission Component Volume Share (%), by Application 2025 & 2033

- Figure 31: undefined Power Transmission Component Revenue (billion), by Type 2025 & 2033

- Figure 32: undefined Power Transmission Component Volume (K), by Type 2025 & 2033

- Figure 33: undefined Power Transmission Component Revenue Share (%), by Type 2025 & 2033

- Figure 34: undefined Power Transmission Component Volume Share (%), by Type 2025 & 2033

- Figure 35: undefined Power Transmission Component Revenue (billion), by Country 2025 & 2033

- Figure 36: undefined Power Transmission Component Volume (K), by Country 2025 & 2033

- Figure 37: undefined Power Transmission Component Revenue Share (%), by Country 2025 & 2033

- Figure 38: undefined Power Transmission Component Volume Share (%), by Country 2025 & 2033

- Figure 39: undefined Power Transmission Component Revenue (billion), by Application 2025 & 2033

- Figure 40: undefined Power Transmission Component Volume (K), by Application 2025 & 2033

- Figure 41: undefined Power Transmission Component Revenue Share (%), by Application 2025 & 2033

- Figure 42: undefined Power Transmission Component Volume Share (%), by Application 2025 & 2033

- Figure 43: undefined Power Transmission Component Revenue (billion), by Type 2025 & 2033

- Figure 44: undefined Power Transmission Component Volume (K), by Type 2025 & 2033

- Figure 45: undefined Power Transmission Component Revenue Share (%), by Type 2025 & 2033

- Figure 46: undefined Power Transmission Component Volume Share (%), by Type 2025 & 2033

- Figure 47: undefined Power Transmission Component Revenue (billion), by Country 2025 & 2033

- Figure 48: undefined Power Transmission Component Volume (K), by Country 2025 & 2033

- Figure 49: undefined Power Transmission Component Revenue Share (%), by Country 2025 & 2033

- Figure 50: undefined Power Transmission Component Volume Share (%), by Country 2025 & 2033

- Figure 51: undefined Power Transmission Component Revenue (billion), by Application 2025 & 2033

- Figure 52: undefined Power Transmission Component Volume (K), by Application 2025 & 2033

- Figure 53: undefined Power Transmission Component Revenue Share (%), by Application 2025 & 2033

- Figure 54: undefined Power Transmission Component Volume Share (%), by Application 2025 & 2033

- Figure 55: undefined Power Transmission Component Revenue (billion), by Type 2025 & 2033

- Figure 56: undefined Power Transmission Component Volume (K), by Type 2025 & 2033

- Figure 57: undefined Power Transmission Component Revenue Share (%), by Type 2025 & 2033

- Figure 58: undefined Power Transmission Component Volume Share (%), by Type 2025 & 2033

- Figure 59: undefined Power Transmission Component Revenue (billion), by Country 2025 & 2033

- Figure 60: undefined Power Transmission Component Volume (K), by Country 2025 & 2033

- Figure 61: undefined Power Transmission Component Revenue Share (%), by Country 2025 & 2033

- Figure 62: undefined Power Transmission Component Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Power Transmission Component Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Power Transmission Component Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Power Transmission Component Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Power Transmission Component Volume K Forecast, by Country 2020 & 2033

- Table 13: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 15: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 16: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 17: Global Power Transmission Component Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Power Transmission Component Volume K Forecast, by Country 2020 & 2033

- Table 19: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Power Transmission Component Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Power Transmission Component Volume K Forecast, by Country 2020 & 2033

- Table 25: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 26: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 27: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 28: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 29: Global Power Transmission Component Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Power Transmission Component Volume K Forecast, by Country 2020 & 2033

- Table 31: Global Power Transmission Component Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Power Transmission Component Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Power Transmission Component Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Power Transmission Component Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Power Transmission Component Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Power Transmission Component Volume K Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Power Transmission Component?

The projected CAGR is approximately 3.9%.

2. Which companies are prominent players in the Power Transmission Component?

Key companies in the market include ABB, Toshiba, EATON, Siemens, Crompton Greaves, General Electric, Hitachi, Schneider Electric, Mitsubishi, Hyundai, BHEL, Emerson, SKF, Freudenberg Sealing Technologies, Trelleborg, Parker Hannifin.

3. What are the main segments of the Power Transmission Component?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 82.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Power Transmission Component," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Power Transmission Component report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Power Transmission Component?

To stay informed about further developments, trends, and reports in the Power Transmission Component, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence