Key Insights

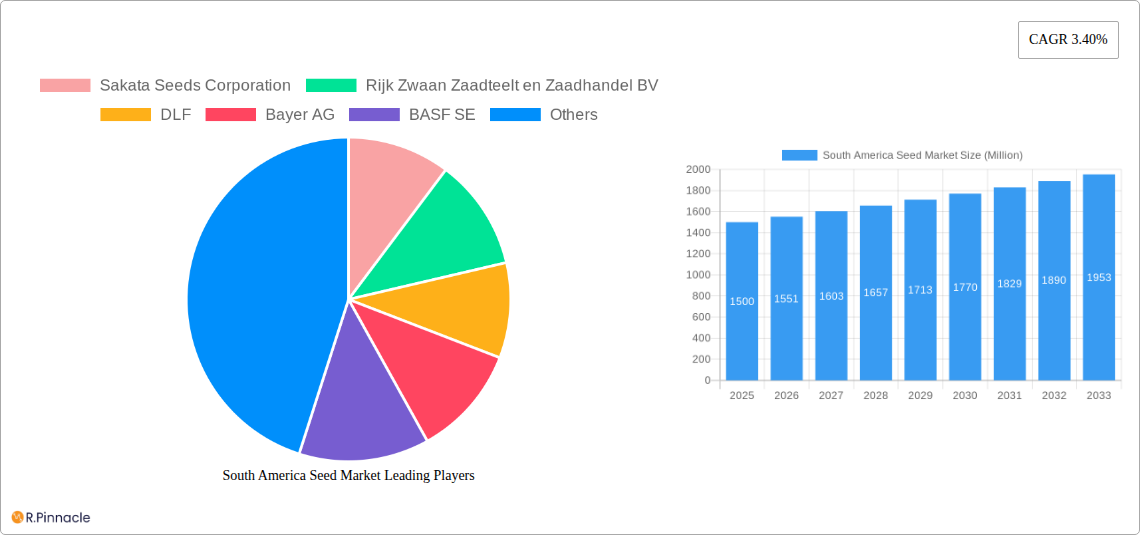

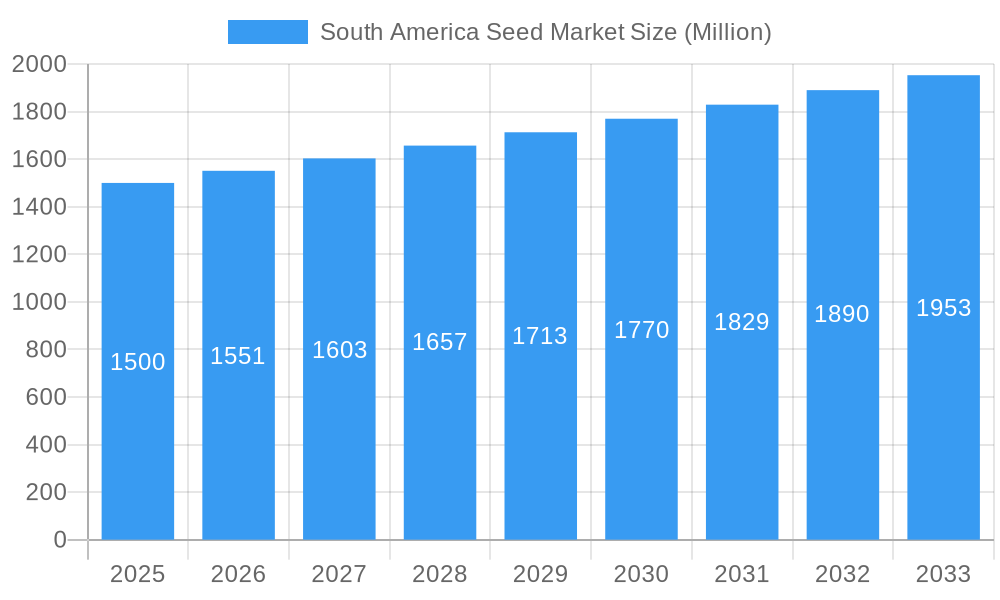

The South American seed market, valued at approximately $X million in 2025 (estimated based on provided CAGR and market size), is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 3.40% from 2025 to 2033. This expansion is driven by several key factors. Firstly, the increasing demand for high-yielding and disease-resistant crop varieties, particularly in row crops and pulses, fuels the need for advanced seed technologies. Secondly, the growing adoption of protected cultivation techniques in regions like Brazil and Argentina is boosting market demand for specialized seeds optimized for these environments. Thirdly, the increasing investment in agricultural research and development within South America is fostering innovation in breeding technologies, leading to the development of hybrid seeds with enhanced productivity and resilience. This growth, however, faces constraints such as climate change impacts on crop yields and fluctuating commodity prices, potentially impacting farmer investment in high-quality seeds. The market is segmented by cultivation mechanism (open field vs. protected cultivation), pulse and vegetable types, and country (Brazil, Argentina, and Rest of South America). Leading players, including Sakata Seeds Corporation, Rijk Zwaan, and Bayer AG, are competing through product innovation and strategic partnerships to capture market share within this expanding sector.

South America Seed Market Market Size (In Billion)

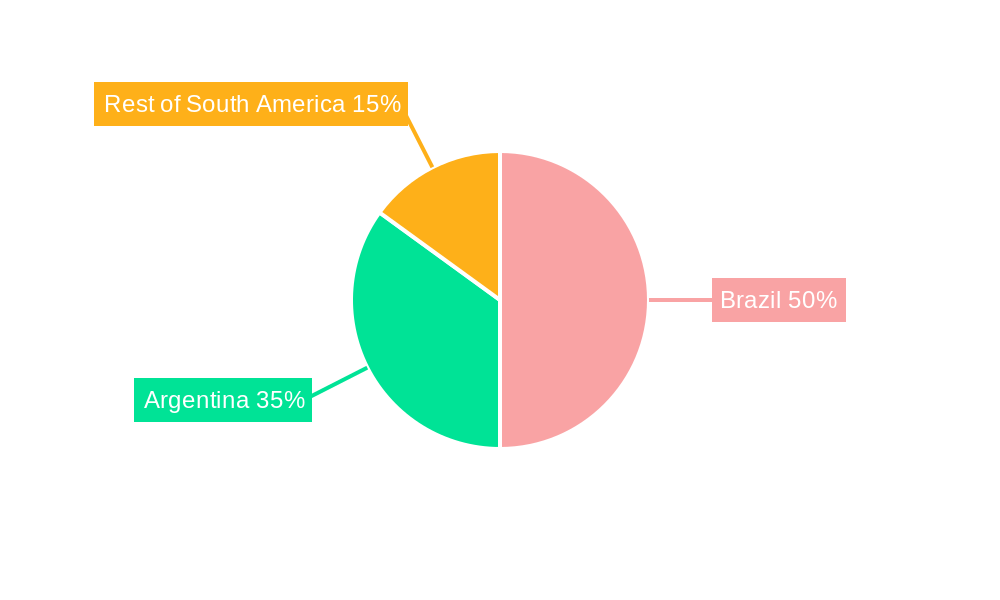

The market segmentation reveals Brazil and Argentina as dominant players within the South American seed market, driven by their large agricultural sectors and adoption of modern farming practices. The 'Rest of South America' segment presents an opportunity for future growth, albeit with potential challenges related to infrastructure and market access. The preference for hybrid seeds is expected to continue to rise, driven by the improved yields and other benefits these seeds offer, though the market will also continue to see demand for open-pollinated varieties. Overall, the South American seed market's future trajectory appears promising, contingent on overcoming challenges related to climate change and economic volatility, requiring companies to invest in resilient seed varieties and sustainable agricultural practices.

South America Seed Market Company Market Share

South America Seed Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the South America seed market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The report covers the period from 2019 to 2033, with a focus on the estimated year 2025. It leverages extensive market research to provide actionable intelligence on market size, growth drivers, challenges, and future opportunities. The total market value in 2025 is estimated at $XX Million.

South America Seed Market Structure & Innovation Trends

This section analyzes the competitive landscape of the South America seed market, including market concentration, innovation drivers, regulatory frameworks, and M&A activities. The market is moderately concentrated, with key players such as Sakata Seeds Corporation, Rijk Zwaan, DLF, Bayer AG, BASF SE, Groupe Limagrain, KWS SAAT, Advanta Seeds - UPL, Syngenta Group, and Corteva Agriscience holding significant market share. However, the presence of numerous smaller players indicates a dynamic competitive environment.

- Market Concentration: The top 5 players hold an estimated xx% market share in 2025.

- Innovation Drivers: Technological advancements in breeding technologies (hybrids, GMOs), precision agriculture, and improved seed treatments are driving market innovation. Government initiatives promoting sustainable agriculture also play a significant role.

- Regulatory Framework: Varying regulatory frameworks across South American countries influence seed adoption and market access. Compliance with biosafety regulations is crucial.

- Product Substitutes: Limited viable substitutes exist for high-quality seeds. However, organic and heirloom seeds represent a growing niche market.

- End-User Demographics: The primary end-users are commercial farmers, followed by smallholder farmers. Market penetration varies significantly across regions and crop types.

- M&A Activities: Recent years have witnessed a moderate level of M&A activity, with deal values ranging from $XX Million to $XX Million. Consolidation amongst players is expected to continue.

South America Seed Market Dynamics & Trends

The South America seed market is experiencing robust growth, driven by several factors. Increasing demand for food and feed, favorable government policies supporting agricultural development, and expanding arable land are major contributors. Technological disruptions, such as the adoption of precision agriculture techniques and improved breeding technologies, are further fueling market expansion. Consumer preferences are shifting towards high-yielding, disease-resistant, and climate-resilient seed varieties.

The market is projected to witness a CAGR of xx% during the forecast period (2025-2033). Market penetration of advanced seed technologies, such as hybrids, is expected to increase significantly, especially in key markets like Brazil and Argentina. Competitive dynamics are characterized by intense rivalry among multinational corporations and regional players. The market also experiences seasonal fluctuations due to planting cycles.

Dominant Regions & Segments in South America Seed Market

Brazil and Argentina stand as the titans of the South American seed market, projected to collectively account for a significant portion of the total market value by 2025. This regional leadership is underpinned by extensive agricultural landscapes, favorable climatic conditions conducive to diverse crop cultivation, and robust government support aimed at bolstering the agricultural sector's productivity and sustainability. Open field cultivation continues to be the prevailing method, highlighting its cost-effectiveness and scalability for large-scale agricultural operations. Within the market segments, the vegetable sector is experiencing a surge in demand, fueled by evolving consumer preferences for fresh, nutritious produce and the burgeoning processed food industry. Furthermore, hybrid breeding technology has secured a dominant share, a testament to its proven ability to deliver superior yields, enhanced nutritional content, and improved performance characteristics compared to conventional breeding methods.

- Key Drivers for Brazil: Comprehensive government incentives, vast expanses of arable land, well-developed agricultural infrastructure, and a skilled and abundant agricultural workforce are instrumental in Brazil's market dominance.

- Key Drivers for Argentina: The consistently favorable climate, deeply entrenched and advanced agricultural practices, and a strategic focus on export-oriented production contribute significantly to Argentina's strong market presence.

- Key Drivers for Open Field Cultivation: Its inherent cost-effectiveness and proven suitability for large-scale, efficient farming operations make it the preferred cultivation method.

- Key Drivers for Vegetable Segment: Rapid urbanization leading to increased demand for convenient and readily available food, evolving dietary habits favoring healthier options, and the escalating consumption of processed and convenience foods are fueling growth.

- Key Drivers for Hybrid Breeding Technology: The ability to deliver significantly improved crop yields, enhanced resistance to a wide spectrum of diseases, and superior adaptability to diverse and challenging environmental conditions are key advantages.

South America Seed Market Product Innovations

The South American seed market is a hotbed of continuous innovation, driven by an unrelenting pursuit of enhanced crop yields, superior disease resistance, and greater tolerance to environmental stressors. Market players are intensely focused on developing cutting-edge hybrid seeds endowed with advanced genetic traits and sophisticated seed treatments designed to optimize plant performance, bolster pest and disease control, and improve overall crop resilience. A significant trend is the development of seed varieties meticulously adapted to specific regional agro-climatic conditions and the increasing impacts of climate change. This forward-thinking approach encompasses the creation of seeds engineered for drought resistance, herbicide tolerance, and improved nutrient utilization efficiency. These innovations are not only directly addressing the critical needs of farmers but also making substantial contributions to the broader goal of establishing more sustainable and environmentally responsible agricultural practices across the continent.

Report Scope & Segmentation Analysis

This report segments the South America seed market based on Cultivation Mechanism (Open Field, Protected Cultivation), Pulses, Vegetables, Other Unclassified Vegetables, Country (Argentina, Brazil, Rest of South America), Crop Type (Row Crops), and Breeding Technology (Hybrids). Each segment's market size, growth projections, and competitive dynamics are thoroughly analyzed. For example, the open-field segment is expected to dominate in terms of market size but show slower growth than the protected cultivation segment which projects high growth rates due to increasing adoption of greenhouse technologies. The report projects substantial growth in all segments across the forecast period, with variation dependent on specific country-crop combinations.

Key Drivers of South America Seed Market Growth

The South America seed market is fueled by several key growth drivers: rising food demand driven by population growth and increasing incomes; favorable government policies promoting agricultural development and investment; advancements in seed technology, including the development of hybrids and genetically modified (GM) seeds; and the increasing adoption of precision farming techniques. These factors combine to create a market environment primed for significant expansion.

Challenges in the South America Seed Market Sector

Several challenges hinder the growth of the South America seed market. These include the high cost of advanced seed technologies, which can limit access for smallholder farmers; the prevalence of counterfeit seeds, which undermines market integrity; fluctuating commodity prices, impacting farmer investments; and climate change, posing increased risks to crop yields and profitability. These factors collectively impact overall market expansion and profitability of various market players.

Emerging Opportunities in South America Seed Market

The South America seed market presents several significant opportunities. The increasing demand for organic and non-GMO seeds creates a niche market segment for growth. Advances in biotechnological innovations such as gene editing, the development of disease-resistant varieties, and drought tolerance are important growth areas. Furthermore, growing awareness of sustainable agricultural practices presents an opportunity for seed companies to offer innovative solutions for enhancing agricultural output in an ecologically responsible manner.

Leading Players in the South America Seed Market Market

Key Developments in South America Seed Market Industry

- July 2023: BASF significantly bolstered its Xitavo soybean seed offering by introducing 11 novel, high-yielding varieties for the 2024 growing season, prominently featuring the advanced Enlist E3 technology. This strategic expansion reinforces BASF's competitive standing in the soybean market by providing farmers with enhanced weed management solutions.

- May 2023: Advanta Seeds forged a key partnership with Embrapa, a renowned Brazilian agricultural research corporation, with the explicit goal of developing hybrid canola seeds possessing superior nematode management capabilities. This collaborative endeavor aims to tackle a persistent challenge faced by canola growers in Brazil, potentially catalyzing a substantial increase in canola cultivation across the region.

- April 2023: Syngenta Seeds entered into a strategic collaboration with Ginkgo Bioworks, a leading synthetic biology company, to pioneer the development of novel traits for next-generation seed technology. This partnership underscores the growing pivotal role of biotechnology in advancing seed development and holds significant promise for creating more resilient and productive crop varieties.

Future Outlook for South America Seed Market Market

The South American seed market is projected to embark on a trajectory of sustained and robust growth, propelled by a confluence of factors including the imperative to enhance agricultural productivity, the continued implementation of supportive government policies, and the relentless pace of technological advancements. The increasing integration of precision agriculture technologies, harmonized with the ongoing development of climate-resilient seed varieties, is set to significantly accelerate market expansion. For companies aiming to thrive and maintain a competitive edge within this dynamic and rapidly evolving landscape, strategic partnerships and substantial investments in research and development will be absolutely paramount. The persistent and growing demand for seeds that offer high yields and exceptional disease resistance will continue to be the primary engine driving this market's expansion.

South America Seed Market Segmentation

-

1. Breeding Technology

-

1.1. Hybrids

- 1.1.1. Non-Transgenic Hybrids

- 1.1.2. Herbicide Tolerant Hybrids

- 1.1.3. Insect Resistant Hybrids

- 1.1.4. Other Traits

- 1.2. Open Pollinated Varieties & Hybrid Derivatives

-

1.1. Hybrids

-

2. Cultivation Mechanism

- 2.1. Open Field

- 2.2. Protected Cultivation

-

3. Crop Type

-

3.1. Row Crops

-

3.1.1. Fiber Crops

- 3.1.1.1. Cotton

- 3.1.1.2. Other Fiber Crops

-

3.1.2. Forage Crops

- 3.1.2.1. Alfalfa

- 3.1.2.2. Forage Corn

- 3.1.2.3. Forage Sorghum

- 3.1.2.4. Other Forage Crops

-

3.1.3. Grains & Cereals

- 3.1.3.1. Rice

- 3.1.3.2. Wheat

- 3.1.3.3. Other Grains & Cereals

-

3.1.4. Oilseeds

- 3.1.4.1. Canola, Rapeseed & Mustard

- 3.1.4.2. Soybean

- 3.1.4.3. Sunflower

- 3.1.4.4. Other Oilseeds

- 3.1.5. Pulses

-

3.1.1. Fiber Crops

-

3.2. Vegetables

-

3.2.1. Brassicas

- 3.2.1.1. Cabbage

- 3.2.1.2. Carrot

- 3.2.1.3. Cauliflower & Broccoli

- 3.2.1.4. Other Brassicas

-

3.2.2. Cucurbits

- 3.2.2.1. Cucumber & Gherkin

- 3.2.2.2. Pumpkin & Squash

- 3.2.2.3. Other Cucurbits

-

3.2.3. Roots & Bulbs

- 3.2.3.1. Garlic

- 3.2.3.2. Onion

- 3.2.3.3. Potato

- 3.2.3.4. Other Roots & Bulbs

-

3.2.4. Solanaceae

- 3.2.4.1. Chilli

- 3.2.4.2. Eggplant

- 3.2.4.3. Tomato

- 3.2.4.4. Other Solanaceae

-

3.2.5. Unclassified Vegetables

- 3.2.5.1. Asparagus

- 3.2.5.2. Lettuce

- 3.2.5.3. Okra

- 3.2.5.4. Peas

- 3.2.5.5. Spinach

- 3.2.5.6. Other Unclassified Vegetables

-

3.2.1. Brassicas

-

3.1. Row Crops

-

4. Breeding Technology

-

4.1. Hybrids

- 4.1.1. Non-Transgenic Hybrids

- 4.1.2. Herbicide Tolerant Hybrids

- 4.1.3. Insect Resistant Hybrids

- 4.1.4. Other Traits

- 4.2. Open Pollinated Varieties & Hybrid Derivatives

-

4.1. Hybrids

-

5. Cultivation Mechanism

- 5.1. Open Field

- 5.2. Protected Cultivation

-

6. Crop Type

-

6.1. Row Crops

-

6.1.1. Fiber Crops

- 6.1.1.1. Cotton

- 6.1.1.2. Other Fiber Crops

-

6.1.2. Forage Crops

- 6.1.2.1. Alfalfa

- 6.1.2.2. Forage Corn

- 6.1.2.3. Forage Sorghum

- 6.1.2.4. Other Forage Crops

-

6.1.3. Grains & Cereals

- 6.1.3.1. Rice

- 6.1.3.2. Wheat

- 6.1.3.3. Other Grains & Cereals

-

6.1.4. Oilseeds

- 6.1.4.1. Canola, Rapeseed & Mustard

- 6.1.4.2. Soybean

- 6.1.4.3. Sunflower

- 6.1.4.4. Other Oilseeds

- 6.1.5. Pulses

-

6.1.1. Fiber Crops

-

6.2. Vegetables

-

6.2.1. Brassicas

- 6.2.1.1. Cabbage

- 6.2.1.2. Carrot

- 6.2.1.3. Cauliflower & Broccoli

- 6.2.1.4. Other Brassicas

-

6.2.2. Cucurbits

- 6.2.2.1. Cucumber & Gherkin

- 6.2.2.2. Pumpkin & Squash

- 6.2.2.3. Other Cucurbits

-

6.2.3. Roots & Bulbs

- 6.2.3.1. Garlic

- 6.2.3.2. Onion

- 6.2.3.3. Potato

- 6.2.3.4. Other Roots & Bulbs

-

6.2.4. Solanaceae

- 6.2.4.1. Chilli

- 6.2.4.2. Eggplant

- 6.2.4.3. Tomato

- 6.2.4.4. Other Solanaceae

-

6.2.5. Unclassified Vegetables

- 6.2.5.1. Asparagus

- 6.2.5.2. Lettuce

- 6.2.5.3. Okra

- 6.2.5.4. Peas

- 6.2.5.5. Spinach

- 6.2.5.6. Other Unclassified Vegetables

-

6.2.1. Brassicas

-

6.1. Row Crops

South America Seed Market Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Peru

- 1.6. Venezuela

- 1.7. Ecuador

- 1.8. Bolivia

- 1.9. Paraguay

- 1.10. Uruguay

South America Seed Market Regional Market Share

Geographic Coverage of South America Seed Market

South America Seed Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.1.1. Hybrids

- 5.1.1.1. Non-Transgenic Hybrids

- 5.1.1.2. Herbicide Tolerant Hybrids

- 5.1.1.3. Insect Resistant Hybrids

- 5.1.1.4. Other Traits

- 5.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1. Hybrids

- 5.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.2.1. Open Field

- 5.2.2. Protected Cultivation

- 5.3. Market Analysis, Insights and Forecast - by Crop Type

- 5.3.1. Row Crops

- 5.3.1.1. Fiber Crops

- 5.3.1.1.1. Cotton

- 5.3.1.1.2. Other Fiber Crops

- 5.3.1.2. Forage Crops

- 5.3.1.2.1. Alfalfa

- 5.3.1.2.2. Forage Corn

- 5.3.1.2.3. Forage Sorghum

- 5.3.1.2.4. Other Forage Crops

- 5.3.1.3. Grains & Cereals

- 5.3.1.3.1. Rice

- 5.3.1.3.2. Wheat

- 5.3.1.3.3. Other Grains & Cereals

- 5.3.1.4. Oilseeds

- 5.3.1.4.1. Canola, Rapeseed & Mustard

- 5.3.1.4.2. Soybean

- 5.3.1.4.3. Sunflower

- 5.3.1.4.4. Other Oilseeds

- 5.3.1.5. Pulses

- 5.3.1.1. Fiber Crops

- 5.3.2. Vegetables

- 5.3.2.1. Brassicas

- 5.3.2.1.1. Cabbage

- 5.3.2.1.2. Carrot

- 5.3.2.1.3. Cauliflower & Broccoli

- 5.3.2.1.4. Other Brassicas

- 5.3.2.2. Cucurbits

- 5.3.2.2.1. Cucumber & Gherkin

- 5.3.2.2.2. Pumpkin & Squash

- 5.3.2.2.3. Other Cucurbits

- 5.3.2.3. Roots & Bulbs

- 5.3.2.3.1. Garlic

- 5.3.2.3.2. Onion

- 5.3.2.3.3. Potato

- 5.3.2.3.4. Other Roots & Bulbs

- 5.3.2.4. Solanaceae

- 5.3.2.4.1. Chilli

- 5.3.2.4.2. Eggplant

- 5.3.2.4.3. Tomato

- 5.3.2.4.4. Other Solanaceae

- 5.3.2.5. Unclassified Vegetables

- 5.3.2.5.1. Asparagus

- 5.3.2.5.2. Lettuce

- 5.3.2.5.3. Okra

- 5.3.2.5.4. Peas

- 5.3.2.5.5. Spinach

- 5.3.2.5.6. Other Unclassified Vegetables

- 5.3.2.1. Brassicas

- 5.3.1. Row Crops

- 5.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.4.1. Hybrids

- 5.4.1.1. Non-Transgenic Hybrids

- 5.4.1.2. Herbicide Tolerant Hybrids

- 5.4.1.3. Insect Resistant Hybrids

- 5.4.1.4. Other Traits

- 5.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.4.1. Hybrids

- 5.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.5.1. Open Field

- 5.5.2. Protected Cultivation

- 5.6. Market Analysis, Insights and Forecast - by Crop Type

- 5.6.1. Row Crops

- 5.6.1.1. Fiber Crops

- 5.6.1.1.1. Cotton

- 5.6.1.1.2. Other Fiber Crops

- 5.6.1.2. Forage Crops

- 5.6.1.2.1. Alfalfa

- 5.6.1.2.2. Forage Corn

- 5.6.1.2.3. Forage Sorghum

- 5.6.1.2.4. Other Forage Crops

- 5.6.1.3. Grains & Cereals

- 5.6.1.3.1. Rice

- 5.6.1.3.2. Wheat

- 5.6.1.3.3. Other Grains & Cereals

- 5.6.1.4. Oilseeds

- 5.6.1.4.1. Canola, Rapeseed & Mustard

- 5.6.1.4.2. Soybean

- 5.6.1.4.3. Sunflower

- 5.6.1.4.4. Other Oilseeds

- 5.6.1.5. Pulses

- 5.6.1.1. Fiber Crops

- 5.6.2. Vegetables

- 5.6.2.1. Brassicas

- 5.6.2.1.1. Cabbage

- 5.6.2.1.2. Carrot

- 5.6.2.1.3. Cauliflower & Broccoli

- 5.6.2.1.4. Other Brassicas

- 5.6.2.2. Cucurbits

- 5.6.2.2.1. Cucumber & Gherkin

- 5.6.2.2.2. Pumpkin & Squash

- 5.6.2.2.3. Other Cucurbits

- 5.6.2.3. Roots & Bulbs

- 5.6.2.3.1. Garlic

- 5.6.2.3.2. Onion

- 5.6.2.3.3. Potato

- 5.6.2.3.4. Other Roots & Bulbs

- 5.6.2.4. Solanaceae

- 5.6.2.4.1. Chilli

- 5.6.2.4.2. Eggplant

- 5.6.2.4.3. Tomato

- 5.6.2.4.4. Other Solanaceae

- 5.6.2.5. Unclassified Vegetables

- 5.6.2.5.1. Asparagus

- 5.6.2.5.2. Lettuce

- 5.6.2.5.3. Okra

- 5.6.2.5.4. Peas

- 5.6.2.5.5. Spinach

- 5.6.2.5.6. Other Unclassified Vegetables

- 5.6.2.1. Brassicas

- 5.6.1. Row Crops

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. South America

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6. South America Seed Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.1.1. Hybrids

- 6.1.1.1. Non-Transgenic Hybrids

- 6.1.1.2. Herbicide Tolerant Hybrids

- 6.1.1.3. Insect Resistant Hybrids

- 6.1.1.4. Other Traits

- 6.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.1.1. Hybrids

- 6.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.2.1. Open Field

- 6.2.2. Protected Cultivation

- 6.3. Market Analysis, Insights and Forecast - by Crop Type

- 6.3.1. Row Crops

- 6.3.1.1. Fiber Crops

- 6.3.1.1.1. Cotton

- 6.3.1.1.2. Other Fiber Crops

- 6.3.1.2. Forage Crops

- 6.3.1.2.1. Alfalfa

- 6.3.1.2.2. Forage Corn

- 6.3.1.2.3. Forage Sorghum

- 6.3.1.2.4. Other Forage Crops

- 6.3.1.3. Grains & Cereals

- 6.3.1.3.1. Rice

- 6.3.1.3.2. Wheat

- 6.3.1.3.3. Other Grains & Cereals

- 6.3.1.4. Oilseeds

- 6.3.1.4.1. Canola, Rapeseed & Mustard

- 6.3.1.4.2. Soybean

- 6.3.1.4.3. Sunflower

- 6.3.1.4.4. Other Oilseeds

- 6.3.1.5. Pulses

- 6.3.1.1. Fiber Crops

- 6.3.2. Vegetables

- 6.3.2.1. Brassicas

- 6.3.2.1.1. Cabbage

- 6.3.2.1.2. Carrot

- 6.3.2.1.3. Cauliflower & Broccoli

- 6.3.2.1.4. Other Brassicas

- 6.3.2.2. Cucurbits

- 6.3.2.2.1. Cucumber & Gherkin

- 6.3.2.2.2. Pumpkin & Squash

- 6.3.2.2.3. Other Cucurbits

- 6.3.2.3. Roots & Bulbs

- 6.3.2.3.1. Garlic

- 6.3.2.3.2. Onion

- 6.3.2.3.3. Potato

- 6.3.2.3.4. Other Roots & Bulbs

- 6.3.2.4. Solanaceae

- 6.3.2.4.1. Chilli

- 6.3.2.4.2. Eggplant

- 6.3.2.4.3. Tomato

- 6.3.2.4.4. Other Solanaceae

- 6.3.2.5. Unclassified Vegetables

- 6.3.2.5.1. Asparagus

- 6.3.2.5.2. Lettuce

- 6.3.2.5.3. Okra

- 6.3.2.5.4. Peas

- 6.3.2.5.5. Spinach

- 6.3.2.5.6. Other Unclassified Vegetables

- 6.3.2.1. Brassicas

- 6.3.1. Row Crops

- 6.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.4.1. Hybrids

- 6.4.1.1. Non-Transgenic Hybrids

- 6.4.1.2. Herbicide Tolerant Hybrids

- 6.4.1.3. Insect Resistant Hybrids

- 6.4.1.4. Other Traits

- 6.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.4.1. Hybrids

- 6.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.5.1. Open Field

- 6.5.2. Protected Cultivation

- 6.6. Market Analysis, Insights and Forecast - by Crop Type

- 6.6.1. Row Crops

- 6.6.1.1. Fiber Crops

- 6.6.1.1.1. Cotton

- 6.6.1.1.2. Other Fiber Crops

- 6.6.1.2. Forage Crops

- 6.6.1.2.1. Alfalfa

- 6.6.1.2.2. Forage Corn

- 6.6.1.2.3. Forage Sorghum

- 6.6.1.2.4. Other Forage Crops

- 6.6.1.3. Grains & Cereals

- 6.6.1.3.1. Rice

- 6.6.1.3.2. Wheat

- 6.6.1.3.3. Other Grains & Cereals

- 6.6.1.4. Oilseeds

- 6.6.1.4.1. Canola, Rapeseed & Mustard

- 6.6.1.4.2. Soybean

- 6.6.1.4.3. Sunflower

- 6.6.1.4.4. Other Oilseeds

- 6.6.1.5. Pulses

- 6.6.1.1. Fiber Crops

- 6.6.2. Vegetables

- 6.6.2.1. Brassicas

- 6.6.2.1.1. Cabbage

- 6.6.2.1.2. Carrot

- 6.6.2.1.3. Cauliflower & Broccoli

- 6.6.2.1.4. Other Brassicas

- 6.6.2.2. Cucurbits

- 6.6.2.2.1. Cucumber & Gherkin

- 6.6.2.2.2. Pumpkin & Squash

- 6.6.2.2.3. Other Cucurbits

- 6.6.2.3. Roots & Bulbs

- 6.6.2.3.1. Garlic

- 6.6.2.3.2. Onion

- 6.6.2.3.3. Potato

- 6.6.2.3.4. Other Roots & Bulbs

- 6.6.2.4. Solanaceae

- 6.6.2.4.1. Chilli

- 6.6.2.4.2. Eggplant

- 6.6.2.4.3. Tomato

- 6.6.2.4.4. Other Solanaceae

- 6.6.2.5. Unclassified Vegetables

- 6.6.2.5.1. Asparagus

- 6.6.2.5.2. Lettuce

- 6.6.2.5.3. Okra

- 6.6.2.5.4. Peas

- 6.6.2.5.5. Spinach

- 6.6.2.5.6. Other Unclassified Vegetables

- 6.6.2.1. Brassicas

- 6.6.1. Row Crops

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sakata Seeds Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DLF

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bayer AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BASF SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Groupe Limagrain

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 KWS SAAT SE & Co KGaA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Advanta Seeds - UPL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Syngenta Grou

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Corteva Agriscience

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Sakata Seeds Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Seed Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South America Seed Market Share (%) by Company 2025

List of Tables

- Table 1: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 2: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 3: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 4: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 5: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 6: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 7: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 8: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 9: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 10: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 11: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 12: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 13: South America Seed Market Revenue Million Forecast, by Region 2020 & 2033

- Table 14: South America Seed Market Volume Kiloton Forecast, by Region 2020 & 2033

- Table 15: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 16: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 17: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 18: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 19: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 20: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 21: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 22: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 23: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 24: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 25: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 26: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 27: South America Seed Market Revenue Million Forecast, by Country 2020 & 2033

- Table 28: South America Seed Market Volume Kiloton Forecast, by Country 2020 & 2033

- Table 29: Brazil South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Brazil South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 31: Argentina South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Argentina South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 33: Chile South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Chile South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 35: Colombia South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Colombia South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 37: Peru South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Peru South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 39: Venezuela South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Venezuela South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 41: Ecuador South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Ecuador South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 43: Bolivia South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Bolivia South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 45: Paraguay South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Paraguay South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 47: Uruguay South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Uruguay South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Seed Market?

The projected CAGR is approximately 3.40%.

2. Which companies are prominent players in the South America Seed Market?

Key companies in the market include Sakata Seeds Corporation, Rijk Zwaan Zaadteelt en Zaadhandel BV, DLF, Bayer AG, BASF SE, Groupe Limagrain, KWS SAAT SE & Co KGaA, Advanta Seeds - UPL, Syngenta Grou, Corteva Agriscience.

3. What are the main segments of the South America Seed Market?

The market segments include Breeding Technology, Cultivation Mechanism, Crop Type, Breeding Technology, Cultivation Mechanism, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Seed Treatment As A Solution To Enhance Yield; Growing Awareness For Seed Treatment Among The Farmers; Rising Trend Of Organic Farming.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Limitations Across Farm-Level Seed Treatment; Rising Environmental Concerns.

8. Can you provide examples of recent developments in the market?

July 2023: BASF expanded its Xitavo soybean seed portfolio with the addition of its 11 new high-yielding varieties for the 2024 growing season, featuring the Enlist E3 technology to combat difficult weeds.May 2023: Advanta Seeds made an agreement with Embrapa (Brazilian Agricultural Research Corporation) to develop hybrid canola seeds with nematode management potential.April 2023: Syngenta Seeds and Ginkgo Bioworks collaborated to develop new traits for the next generation of seed technology to produce healthier and more resilient crops.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Seed Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Seed Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Seed Market?

To stay informed about further developments, trends, and reports in the South America Seed Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence