Key Insights

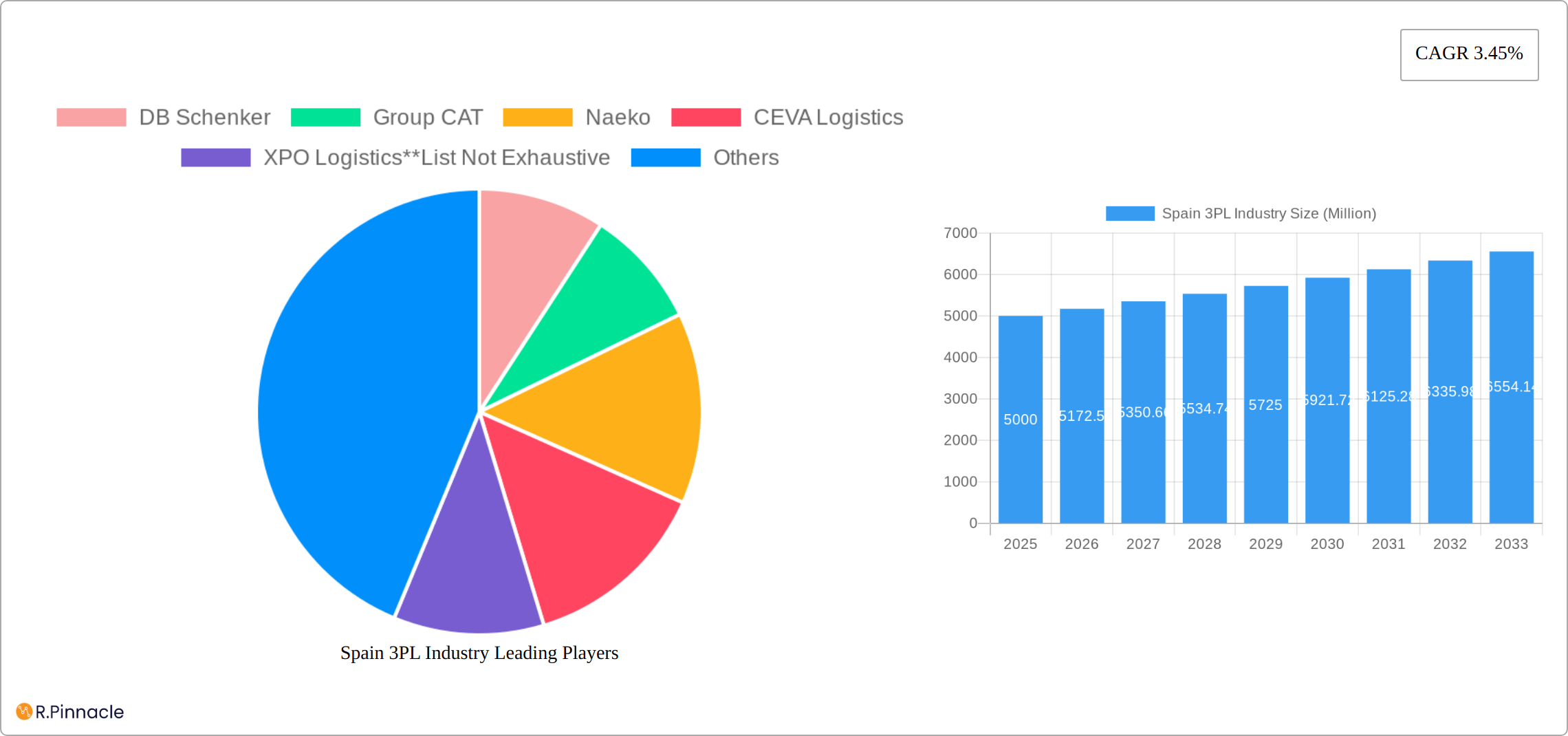

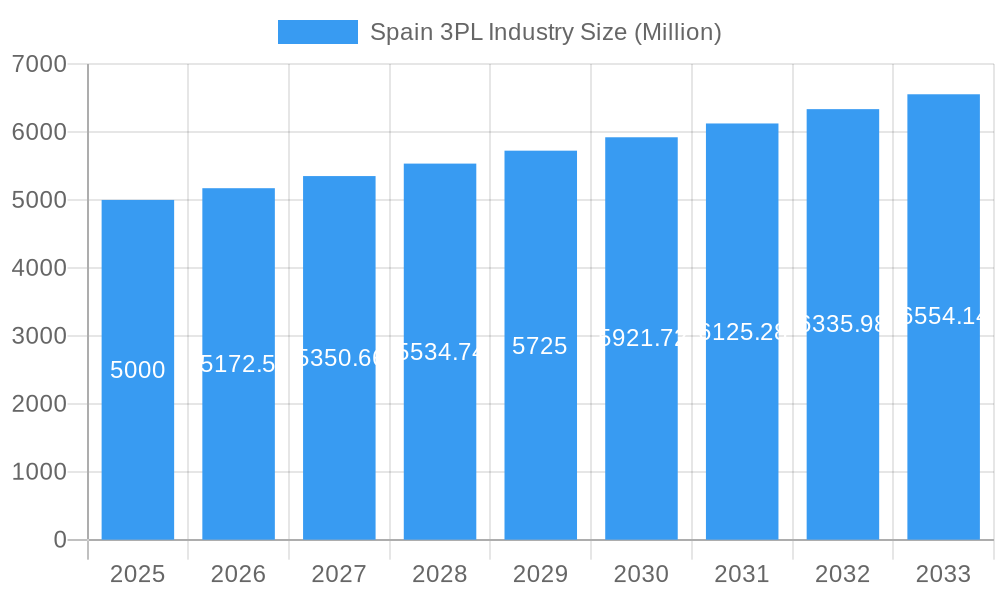

The Spanish Third-Party Logistics (3PL) market, valued at $14.46 billion in 2025, is forecast to expand at a Compound Annual Growth Rate (CAGR) of 4.03% from 2025 to 2033. This growth is propelled by the rapidly expanding e-commerce sector, which demands sophisticated warehousing and distribution. Key industries like manufacturing, automotive, oil & gas, and chemicals are increasingly outsourcing logistics to 3PL providers to optimize supply chains and reduce operational costs. The growing demand for value-added services, including specialized warehousing and inventory management, further fuels market expansion.

Spain 3PL Industry Market Size (In Billion)

Market growth may face headwinds from fluctuating fuel prices, economic uncertainties, and persistent challenges in driver and skilled labor availability. However, the widespread adoption of advanced technologies, such as automation and data analytics, is expected to mitigate these challenges. These technological integrations will enhance efficiency and supply chain visibility, reinforcing the long-term growth trajectory of the Spanish 3PL market. The competitive landscape features prominent players like DB Schenker, XPO Logistics, and DSV, alongside specialized niche providers. Domestic transportation management remains a significant segment, underscoring the strength of the local market.

Spain 3PL Industry Company Market Share

Spain 3PL Industry Market Analysis: 2019-2033

This comprehensive report delivers an in-depth analysis of the Spain 3PL industry, covering market size, growth drivers, competitive dynamics, and future projections. The study period encompasses 2019-2033, with 2025 as the base year and 2025-2033 as the forecast period. Leveraging extensive data analysis and industry expertise, this report provides actionable insights for industry professionals, investors, and stakeholders seeking to understand the strategic importance and dynamics of the Spanish 3PL market.

Spain 3PL Industry Market Structure & Innovation Trends

The Spanish 3PL market exhibits a moderately consolidated structure, with key players like DB Schenker, CEVA Logistics, XPO Logistics, and others holding significant market share. However, numerous smaller, specialized 3PL providers also contribute substantially. Market concentration is estimated at xx%, with the top five players commanding approximately xx% of the market in 2025. Innovation is driven by e-commerce growth, increasing demand for value-added services, and technological advancements in automation and data analytics. The regulatory framework, while generally supportive, presents challenges related to compliance and data privacy. Product substitutes include in-house logistics solutions and direct-to-consumer shipping models. M&A activity has been moderate, with deals typically focused on expanding service offerings and geographical reach. Recent M&A deal values have averaged approximately xx Million. End-user demographics are diverse, with a significant focus on manufacturing, automotive, and retail sectors.

Spain 3PL Industry Market Dynamics & Trends

The Spain 3PL market is experiencing robust growth, driven by factors such as increasing e-commerce penetration, the expansion of global supply chains, and rising demand for efficient and cost-effective logistics solutions. Technological disruptions, such as the adoption of AI, blockchain, and automation, are reshaping the industry landscape, creating both opportunities and challenges. Consumer preferences are shifting towards faster delivery times, greater transparency, and enhanced supply chain visibility. The competitive dynamics are characterized by intense rivalry, price competition, and a constant drive for innovation. The CAGR for the forecast period (2025-2033) is projected at xx%, with market penetration expected to reach xx% by 2033.

Dominant Regions & Segments in Spain 3PL Industry

Dominant Regions: While precise regional data is unavailable, the Madrid and Barcelona regions are expected to be the dominant areas, due to their high population density, developed infrastructure, and proximity to major ports and airports. Key drivers include favorable economic policies, robust infrastructure, and a large concentration of manufacturing and distribution hubs.

Dominant Segments:

- By Service: Value-added warehousing and distribution is a high-growth segment, fueled by e-commerce and the need for specialized services like packaging, labeling, and inventory management. International transportation management also shows strong growth potential, driven by increasing cross-border trade.

- By End User: The manufacturing & automotive sector, distributive trade (including e-commerce), and pharma & healthcare segments are the leading end-users, due to high logistics intensity and specialized requirements. These sectors account for over xx% of the total market value.

Spain 3PL Industry Product Innovations

The Spanish 3PL sector is experiencing a wave of innovation driven by the need for greater efficiency, transparency, and resilience. Recent product advancements center around automation, enhanced visibility, and data-driven optimization. This includes a significant uptake of automated storage and retrieval systems (AS/RS), sophisticated warehouse management systems (WMS), and advanced transportation management systems (TMS). The integration of artificial intelligence (AI) and machine learning (ML) is transforming operations, enabling predictive analytics for inventory management, optimized route planning, and proactive risk mitigation. Furthermore, the implementation of blockchain technology is enhancing supply chain transparency and traceability, bolstering trust and accountability. These technological advancements provide significant competitive advantages by enhancing speed, accuracy, cost-effectiveness, and overall supply chain resilience.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation of the Spain 3PL market by service type (Domestic Transportation Management, International Transportation Management, Value-added Warehousing and Distribution) and by end-user (Manufacturing & Automotive, Oil & Gas and Chemicals, Distributive Trade, Pharma & Healthcare, Construction, Other End Users). Each segment’s analysis includes growth projections, market size estimates, and an assessment of competitive dynamics. The market size for each segment is estimated for the historical period (2019-2024) and projected for the forecast period (2025-2033). Competitive dynamics are analyzed, highlighting key players and their strategies within each segment.

Key Drivers of Spain 3PL Industry Growth

Robust growth in the Spanish 3PL market is fueled by several key factors. The explosive expansion of e-commerce continues to drive demand for efficient and scalable logistics solutions. Increasing globalization and the complexity of modern supply chains necessitate the expertise and capabilities offered by 3PL providers. Government initiatives focused on modernizing logistics infrastructure and fostering digital transformation are creating a supportive environment for industry expansion. The rise of omnichannel retailing, demanding flexible and responsive logistics, further fuels demand. Finally, a growing emphasis on sustainability is pushing 3PLs to adopt eco-friendly practices, creating new market opportunities.

Challenges in the Spain 3PL Industry Sector

Despite the significant growth, the Spanish 3PL industry faces several challenges. Rising labor costs and intense competition put pressure on profit margins. Fluctuations in fuel prices and the ongoing impact of global supply chain disruptions present ongoing operational hurdles. Strict regulatory compliance adds another layer of complexity. Moreover, attracting and retaining skilled labor remains a critical challenge, demanding investment in training and development programs. Addressing these challenges requires ongoing innovation, strategic partnerships, and a commitment to operational excellence.

Emerging Opportunities in Spain 3PL Industry

The Spanish 3PL sector presents compelling opportunities for growth and innovation. The increasing demand for specialized services, such as cold chain logistics for pharmaceuticals and temperature-sensitive goods, offers a significant avenue for expansion. The growing focus on sustainable logistics practices, including the use of alternative fuels and eco-friendly packaging, is creating new market segments. The adoption of cutting-edge technologies, such as AI-powered predictive maintenance and blockchain for improved traceability, presents significant opportunities for enhancing efficiency and competitiveness. The continued expansion of e-commerce into rural areas also opens up new markets for 3PL providers offering robust last-mile delivery solutions.

Leading Players in the Spain 3PL Industry Market

- DB Schenker

- Group CAT

- Naeko

- CEVA Logistics

- XPO Logistics

- OIA Global

- Carcaba

- TIBA

- Rhenus Logistics

- DSV

- Decal FM Logistics

Key Developments in Spain 3PL Industry

- June 2023: Factor 5 implements a Dematic AutoStore™ system for enhanced order processing of perfumes and cosmetics, boosting competitiveness.

- April 2023: CEVA Logistics acquires full control of its BERGÉ GEFCO joint venture, expanding its finished vehicle logistics (FVL) services.

Future Outlook for Spain 3PL Industry Market

The Spain 3PL market is poised for continued growth, driven by ongoing technological advancements, increasing e-commerce penetration, and favorable government policies. Strategic opportunities exist for 3PL providers to leverage automation, data analytics, and sustainable logistics practices to gain a competitive edge. The market’s future potential is significant, presenting ample opportunities for both established players and new entrants.

Spain 3PL Industry Segmentation

-

1. Service

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End User

- 2.1. Manufacturing & Automotive

- 2.2. Oil & Gas and Chemicals

- 2.3. Distribu

- 2.4. Pharma & Healthcare

- 2.5. Construction

- 2.6. Other End Users

Spain 3PL Industry Segmentation By Geography

- 1. Spain

Spain 3PL Industry Regional Market Share

Geographic Coverage of Spain 3PL Industry

Spain 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.03% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing & Automotive

- 5.2.2. Oil & Gas and Chemicals

- 5.2.3. Distribu

- 5.2.4. Pharma & Healthcare

- 5.2.5. Construction

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Spain 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing & Automotive

- 6.2.2. Oil & Gas and Chemicals

- 6.2.3. Distribu

- 6.2.4. Pharma & Healthcare

- 6.2.5. Construction

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Group CAT

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Naeko

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CEVA Logistics

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 XPO Logistics**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 OIA Global

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Carcaba

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 TIBA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rhenus Logistics

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 DSV

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Decal FM Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain 3PL Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Spain 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Spain 3PL Industry Revenue billion Forecast, by Service 2020 & 2033

- Table 2: Spain 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Spain 3PL Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Spain 3PL Industry Revenue billion Forecast, by Service 2020 & 2033

- Table 5: Spain 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Spain 3PL Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain 3PL Industry?

The projected CAGR is approximately 4.03%.

2. Which companies are prominent players in the Spain 3PL Industry?

Key companies in the market include DB Schenker, Group CAT, Naeko, CEVA Logistics, XPO Logistics**List Not Exhaustive, OIA Global, Carcaba, TIBA, Rhenus Logistics, DSV, Decal FM Logistics.

3. What are the main segments of the Spain 3PL Industry?

The market segments include Service, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.46 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Global Trade and Export-Oriented Economy boosting the market4.; Investment in Robotics and Automation.

6. What are the notable trends driving market growth?

Growth in Refrigerated Logistics.

7. Are there any restraints impacting market growth?

4.; South Korea's logistics infrastructure. while generally well-developed. can experience congestion in key areas. such as ports and highways4.; Like many other countries. South Korea faced issues related to labor shortages in the logistics sector..

8. Can you provide examples of recent developments in the market?

June 2023: Third-party logistics operator Factor 5 recently commissioned a goods-to-person solution featuring an AutoStore™ automated storage and picking system provided by intelligent automation solution provider Dematic. The solution enhances its order process for perfumes and cosmetics products with the aim of boosting sales and strengthening its ability to compete in the long term. The solution went live in March at Factor 5’s Alovera site northeast of Madrid.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain 3PL Industry?

To stay informed about further developments, trends, and reports in the Spain 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence