Key Insights

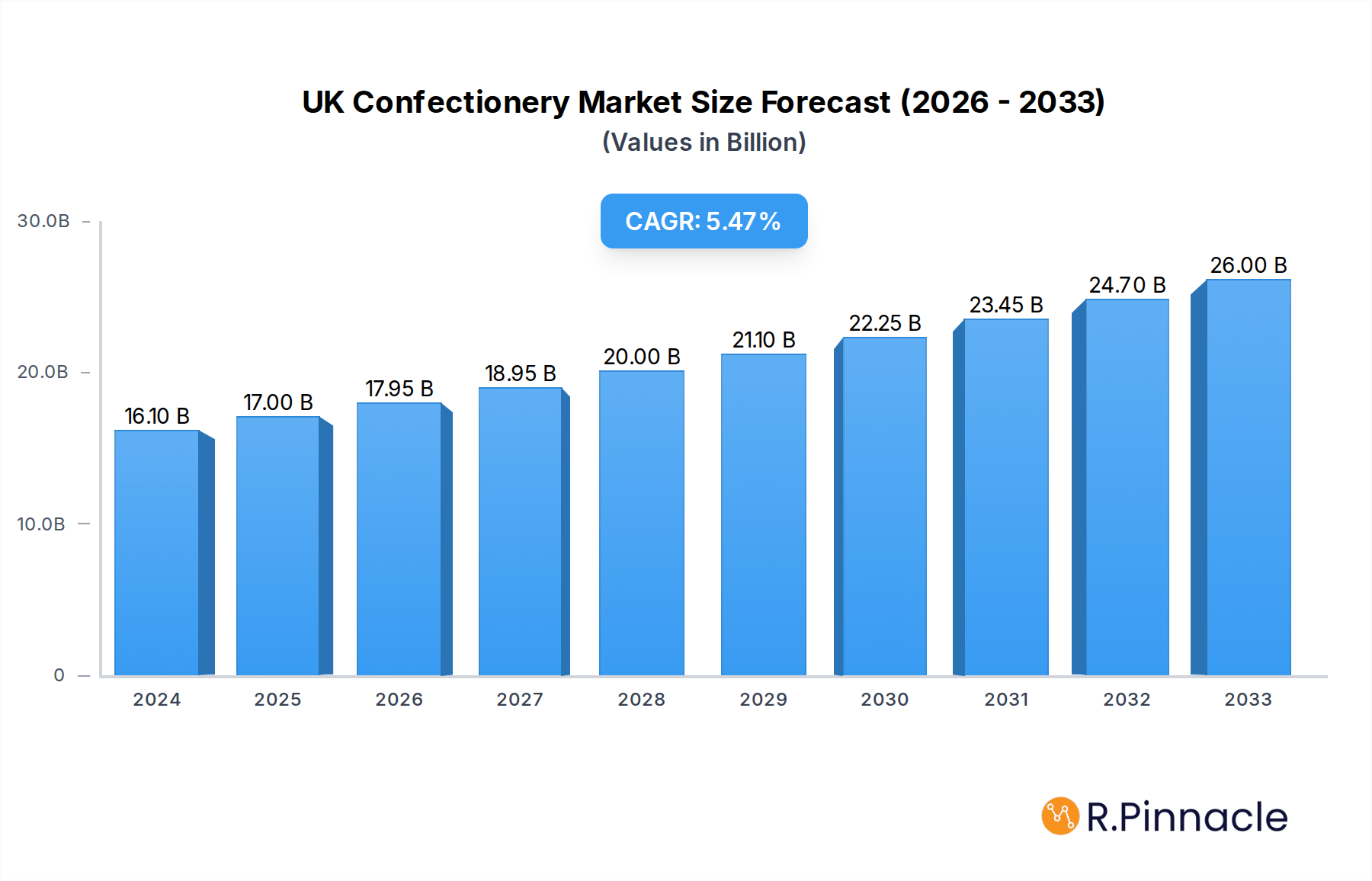

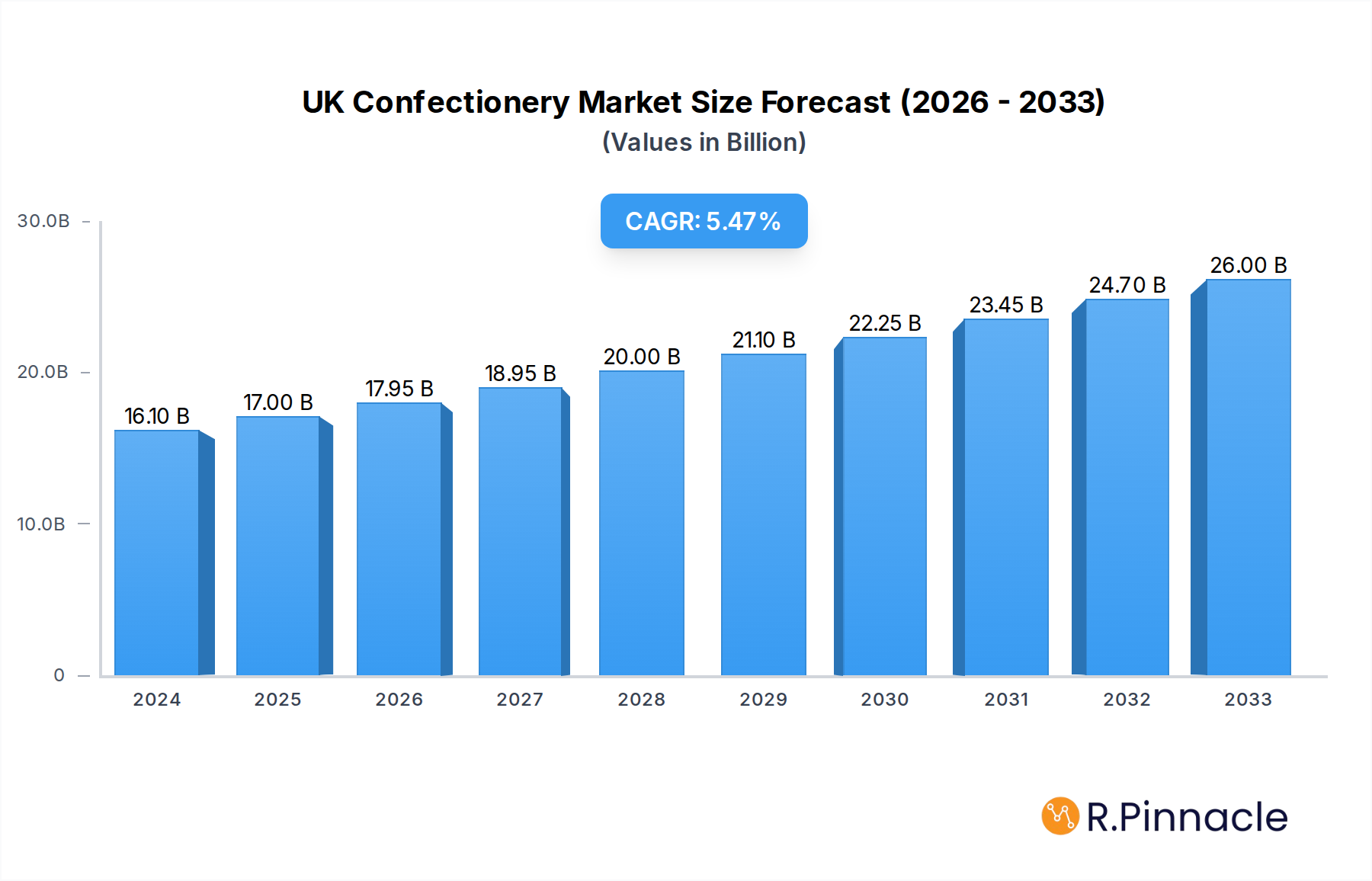

The UK confectionery market is poised for robust expansion, with a projected market size of £16.1 billion in 2024 and an anticipated CAGR of 5.4% through 2033. This dynamic growth is fueled by several key drivers, including increasing consumer demand for premium and artisanal chocolate products, a rising preference for healthier snack options like cereal and protein bars, and the continued innovation in sugar-free and low-sugar confectionery. The convenience and accessibility offered by online retail and supermarket channels further bolster market penetration, making a wide array of confections readily available to consumers. The market's resilience is also evident in its ability to adapt to evolving consumer preferences, with a growing emphasis on ethical sourcing, sustainable packaging, and unique flavor profiles.

UK Confectionery Market Market Size (In Billion)

The UK confectionery landscape is characterized by diverse segments, ranging from traditional chocolate and sugar confectionery to burgeoning snack bar categories. While established players like Nestlé SA, Mondelēz International Inc., and Mars Incorporated continue to dominate, smaller, niche brands are gaining traction by focusing on specialized offerings and direct-to-consumer models. Restraints such as fluctuating raw material costs and increasing health consciousness among certain demographics are being navigated through product reformulations and the development of functional confectionery. The market's future trajectory is heavily influenced by the ongoing interplay between indulgence and health, with companies strategically positioning themselves to cater to both desires. The ongoing expansion in regions like Asia Pacific, while not the primary focus here, signals a global trend that also influences innovation and supply chains impacting the UK market.

UK Confectionery Market Company Market Share

Unwrapping the Future: UK Confectionery Market Report 2025-2033

This comprehensive report delves deep into the dynamic UK confectionery market, offering unparalleled insights for industry professionals. Spanning the study period of 2019–2033, with a focus on the base year 2025, this analysis provides critical data and strategic recommendations. Explore the evolving landscape of chocolate, gums, snack bars, and sugar confectionery, alongside distribution channel shifts and emerging market trends. With a projected market value reaching hundreds of billions, this report is your essential guide to navigating growth, innovation, and competition in one of Europe's most significant confectionery markets.

UK Confectionery Market Market Structure & Innovation Trends

The UK confectionery market exhibits a moderately concentrated structure, with key players like Nestlé SA, Mars Incorporated, and Mondelēz International Inc. holding substantial market share, estimated in the tens of billions. Innovation is a primary driver, focusing on premiumization, healthier options, and novel flavor profiles. Regulatory frameworks, particularly concerning sugar content and marketing to children, continue to shape product development. Substitutes for traditional confectionery, such as healthier snack options and functional foods, are gaining traction, particularly among health-conscious demographics. Mergers and acquisitions remain a strategic avenue for consolidation and expansion, with recent deal values estimated in the hundreds of millions. End-user demographics are increasingly diverse, with a growing demand for bespoke and ethically sourced products.

- Market Concentration: Dominated by a few multinational corporations, with significant presence of specialized artisanal brands.

- Innovation Drivers: Health & wellness trends, premium ingredients, sustainable sourcing, novel flavor combinations, and experiential consumption.

- Regulatory Frameworks: Strict guidelines on sugar, artificial ingredients, and responsible marketing.

- Product Substitutes: Growing influence of functional snacks, fruit-based treats, and plant-based alternatives.

- End-User Demographics: Shifting preferences towards healthier indulgence, transparency, and ethical consumption.

- M&A Activities: Strategic acquisitions and partnerships to expand product portfolios and market reach, with deal values in the hundreds of millions.

UK Confectionery Market Market Dynamics & Trends

The UK confectionery market is poised for robust growth, driven by an increasing disposable income and a persistent consumer demand for indulgent treats. The estimated CAGR for the forecast period 2025–2033 is expected to be in the mid-single digits, with the market penetration continuing to deepen across all segments. Technological disruptions are reshaping the industry, from advanced manufacturing processes enabling customization to the rise of e-commerce platforms revolutionizing distribution. Consumer preferences are evolving rapidly, with a notable shift towards products offering perceived health benefits, such as reduced sugar, added vitamins, or plant-based ingredients. This trend is particularly evident in the growing demand for dark chocolate and sugar-free gum variants. Competitive dynamics are intensifying, with both established giants and agile startups vying for market share. The market penetration for premium and artisanal confectionery is on the rise, reflecting a consumer willingness to pay more for unique flavors and high-quality ingredients. The influence of social media and celebrity endorsements continues to play a significant role in shaping purchasing decisions, driving trends in product novelty and appeal. Furthermore, the growing emphasis on sustainability and ethical sourcing is becoming a key differentiator for brands, impacting consumer loyalty and market positioning. The increasing availability of international confectionery brands also contributes to a more diverse and competitive market.

Dominant Regions & Segments in UK Confectionery Market

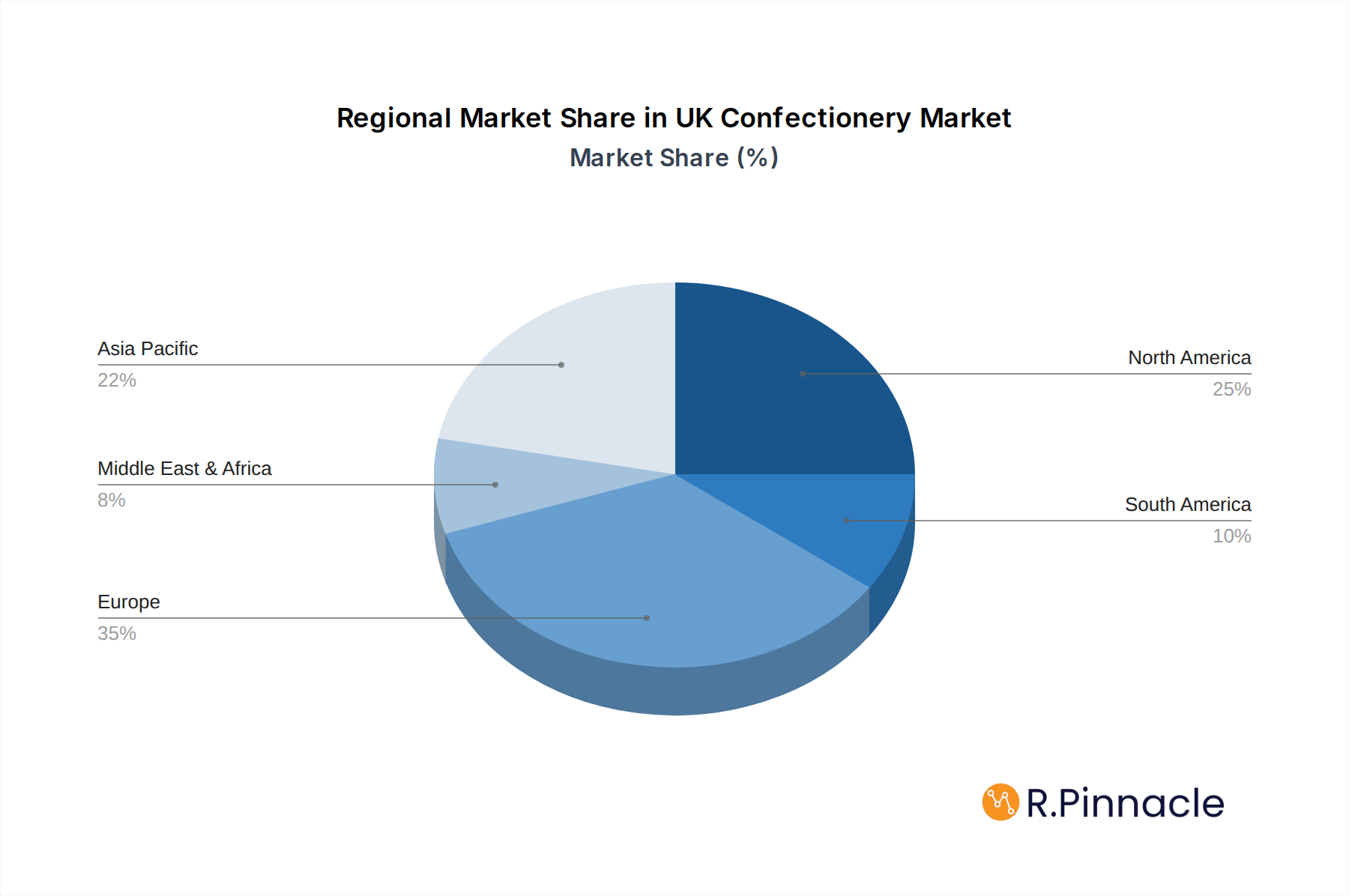

The United Kingdom’s confectionery market is characterized by its dynamic regional performance and the diverse dominance across its segments. While specific regional data is proprietary, England consistently represents the largest market by value and volume, driven by its dense population and robust retail infrastructure. Within the broader Confections segment, Chocolate commands the largest share, with Milk Chocolate being the perennial favorite, accounting for billions in annual sales. However, Dark Chocolate is witnessing significant growth, fueled by health-conscious consumers seeking perceived benefits and richer taste profiles.

The Gums segment, while smaller than chocolate, demonstrates consistent demand. Chewing Gum, particularly Sugar-free Chewing Gum, continues to be a strong performer due to its convenience and perceived oral health benefits. Sugar Confectionery remains a staple, with Hard Candy and Gummies and Jellies holding substantial market shares. The rise of "better-for-you" options within this segment, such as reduced-sugar gummies, is a notable trend.

Distribution channels reveal a strong reliance on Supermarkets/Hypermarkets, which handle a significant portion of confectionery sales, estimated in the tens of billions. However, Online Retail Stores are rapidly gaining ground, facilitated by convenience and wider product selection, with projected growth rates surpassing traditional channels. Convenience Stores also play a crucial role, particularly for impulse purchases, contributing billions to the overall market.

- Leading Region: England, due to its large population and well-developed retail network.

- Dominant Confectionery Segment: Chocolate, with Milk Chocolate as the largest sub-segment, followed by Dark Chocolate experiencing significant growth.

- Growing Confectionery Segment: Dark Chocolate, driven by health and premiumization trends.

- Key Gum Segment: Sugar-free Chewing Gum, due to its convenience and perceived health benefits.

- Leading Sugar Confectionery Sub-segments: Hard Candy and Gummies and Jellies.

- Emerging Trend in Sugar Confectionery: Reduced-sugar and healthier variants of gummies.

- Dominant Distribution Channel: Supermarkets/Hypermarkets, facilitating bulk purchases and wide availability.

- Rapidly Growing Distribution Channel: Online Retail Stores, driven by convenience and expanding reach.

- Impulse Purchase Hub: Convenience Stores, essential for immediate consumption needs.

UK Confectionery Market Product Innovations

Recent product developments in the UK confectionery market underscore a strong trend towards health-conscious indulgence and novel flavor experiences. The Hershey Company's launch of the ONE Peanut Butter & Jelly Flavored Protein Bar, packed with 20g of protein and minimal sugar, exemplifies the fusion of nutritional benefits with popular flavor profiles. Nestlé’s introduction of fused flavor chocolate bars, like the Purple One and Green Triangle, demonstrates a move towards exciting and unexpected taste combinations. Swizzels Sweets’ collaboration with Applied Nutrition to create sports nutrition products in iconic sweet flavors showcases an innovative approach to tapping into the wellness market. These innovations offer competitive advantages by catering to evolving consumer demands for both enjoyment and functional benefits, ensuring market relevance and appeal.

Report Scope & Segmentation Analysis

This report encompasses a granular analysis of the UK confectionery market, segmented across key categories to provide comprehensive insights. Confections are explored with detailed breakdowns including Chocolate (Dark Chocolate, Milk and White Chocolate), Gums (Bubble Gum, Chewing Gum – further segmented by Sugar Content into Sugar Chewing Gum and Sugar-free Chewing Gum), Snack Bars (Cereal Bar, Fruit & Nut Bar, Protein Bar), and Sugar Confectionery (Hard Candy, Lollipops, Mints, Pastilles, Gummies and Jellies, Toffees and Nougats, Others). Distribution Channels are also thoroughly analyzed, covering Convenience Stores, Online Retail Stores, Supermarkets/Hypermarkets, and Others. Growth projections for each segment range from low-single digits to double-digit percentages, with specific market sizes detailed within the report. Competitive dynamics within each segment are examined, highlighting key players and their strategies.

Key Drivers of UK Confectionery Market Growth

The UK confectionery market's growth is propelled by several interconnected factors. Increasing disposable incomes and a rising consumer propensity for affordable luxury fuel demand for indulgent treats. Innovation in product development, particularly the focus on healthier options like reduced-sugar and natural ingredient confectionery, caters to evolving consumer preferences and expands market reach. The growing influence of e-commerce and online retail channels provides greater accessibility and convenience, driving sales. Furthermore, strategic partnerships and collaborations, such as those seen between confectionery brands and sports nutrition companies, unlock new market segments and revenue streams, contributing significantly to overall market expansion.

Challenges in the UK Confectionery Market Sector

Despite its growth trajectory, the UK confectionery market faces significant challenges. Stringent government regulations concerning sugar content, labeling, and marketing to children necessitate ongoing product reformulation and marketing strategy adjustments, impacting production costs. Supply chain disruptions, exacerbated by global events, can lead to increased raw material costs and availability issues. Intense competition from both domestic and international players, including the growing threat from healthier snack alternatives, puts pressure on pricing and market share. Furthermore, negative public perception surrounding the health implications of excessive sugar consumption can influence consumer purchasing behavior, posing a restraint on certain product categories.

Emerging Opportunities in UK Confectionery Market

The UK confectionery market presents a wealth of emerging opportunities. The increasing demand for premium and artisanal confectionery, characterized by unique flavors, high-quality ingredients, and sustainable sourcing, offers premiumization potential. The expanding market for plant-based and vegan confectionery aligns with growing ethical consumerism. Innovations in functional confectionery, incorporating benefits like added vitamins, probiotics, or stress-relief properties, can tap into the burgeoning health and wellness trend. The continued growth of online retail and direct-to-consumer models presents opportunities for personalized product offerings and niche market penetration. Furthermore, exploring novel flavor combinations and limited-edition releases can drive consumer engagement and repeat purchases.

Leading Players in the UK Confectionery Market Market

Pimlico Confectioneries Ltd Nestlé SA Chocoladefabriken Lindt & Sprüngli AG Swizzels Matlow Ltd Polo del Gusto SRL August Storck KG Ferrero International SA Mars Incorporated Barry Callebaut AG Arcor S A I C HARIBO Holding GmbH & Co KG The Hershey Company Mondelēz International Inc Alfred Ritter GmbH & Co KG Confiserie Leonidas SA

Key Developments in UK Confectionery Market Industry

- April 2023: Swizzels Sweets partnered with Applied Nutrition to launch a range of sports nutrition products in several of Swizzels’ well-known flavors. The sports brand Applied Nutrition announced Drumstick flavor lollies of both its bestselling hydration drink, BodyFuel, and a 60 ml shot variant of its popular pre-workout, A.B.E.

- April 2023: Under the ONE brand, The Hershey Company launched the Peanut Butter & Jelly Flavored Protein Bar. The ONE Limited Edition Peanut Butter & Jelly flavored bars are packed with 20 g of protein, 1 g of sugar, and the familiar taste of peanut butter and strawberry jelly flavors.

- March 2023: Nestlé launched a new chocolate bar fused with two flavors, i.e., the Purple One and Green Triangle. These chocolate bars are available in supermarkets across the United Kingdom.

Future Outlook for UK Confectionery Market Market

The future outlook for the UK confectionery market remains positive, driven by sustained consumer demand for indulgence and a growing appetite for innovation. The market is expected to witness continued growth fueled by a combination of premiumization, healthier alternatives, and an expansion of e-commerce channels. Strategic investments in product development, focusing on novel flavors, plant-based options, and functional benefits, will be crucial for sustained success. Furthermore, brands that prioritize sustainability and ethical sourcing will likely resonate more strongly with an increasingly conscious consumer base. The interplay between traditional retail and digital platforms will continue to shape market dynamics, offering both challenges and significant opportunities for market leaders and emerging players alike.

UK Confectionery Market Segmentation

-

1. Confections

-

1.1. Chocolate

-

1.1.1. By Confectionery Variant

- 1.1.1.1. Dark Chocolate

- 1.1.1.2. Milk and White Chocolate

-

1.1.1. By Confectionery Variant

-

1.2. Gums

- 1.2.1. Bubble Gum

-

1.2.2. Chewing Gum

-

1.2.2.1. By Sugar Content

- 1.2.2.1.1. Sugar Chewing Gum

- 1.2.2.1.2. Sugar-free Chewing Gum

-

1.2.2.1. By Sugar Content

-

1.3. Snack Bar

- 1.3.1. Cereal Bar

- 1.3.2. Fruit & Nut Bar

- 1.3.3. Protein Bar

-

1.4. Sugar Confectionery

- 1.4.1. Hard Candy

- 1.4.2. Lollipops

- 1.4.3. Mints

- 1.4.4. Pastilles, Gummies, and Jellies

- 1.4.5. Toffees and Nougats

- 1.4.6. Others

-

1.1. Chocolate

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

UK Confectionery Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK Confectionery Market Regional Market Share

Geographic Coverage of UK Confectionery Market

UK Confectionery Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 5.1.1. Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.1.1.1. Dark Chocolate

- 5.1.1.1.2. Milk and White Chocolate

- 5.1.1.1. By Confectionery Variant

- 5.1.2. Gums

- 5.1.2.1. Bubble Gum

- 5.1.2.2. Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.2.2.1.1. Sugar Chewing Gum

- 5.1.2.2.1.2. Sugar-free Chewing Gum

- 5.1.2.2.1. By Sugar Content

- 5.1.3. Snack Bar

- 5.1.3.1. Cereal Bar

- 5.1.3.2. Fruit & Nut Bar

- 5.1.3.3. Protein Bar

- 5.1.4. Sugar Confectionery

- 5.1.4.1. Hard Candy

- 5.1.4.2. Lollipops

- 5.1.4.3. Mints

- 5.1.4.4. Pastilles, Gummies, and Jellies

- 5.1.4.5. Toffees and Nougats

- 5.1.4.6. Others

- 5.1.1. Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Confections

- 6. Global UK Confectionery Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Confections

- 6.1.1. Chocolate

- 6.1.1.1. By Confectionery Variant

- 6.1.1.1.1. Dark Chocolate

- 6.1.1.1.2. Milk and White Chocolate

- 6.1.1.1. By Confectionery Variant

- 6.1.2. Gums

- 6.1.2.1. Bubble Gum

- 6.1.2.2. Chewing Gum

- 6.1.2.2.1. By Sugar Content

- 6.1.2.2.1.1. Sugar Chewing Gum

- 6.1.2.2.1.2. Sugar-free Chewing Gum

- 6.1.2.2.1. By Sugar Content

- 6.1.3. Snack Bar

- 6.1.3.1. Cereal Bar

- 6.1.3.2. Fruit & Nut Bar

- 6.1.3.3. Protein Bar

- 6.1.4. Sugar Confectionery

- 6.1.4.1. Hard Candy

- 6.1.4.2. Lollipops

- 6.1.4.3. Mints

- 6.1.4.4. Pastilles, Gummies, and Jellies

- 6.1.4.5. Toffees and Nougats

- 6.1.4.6. Others

- 6.1.1. Chocolate

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Convenience Store

- 6.2.2. Online Retail Store

- 6.2.3. Supermarket/Hypermarket

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Confections

- 7. North America UK Confectionery Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Confections

- 7.1.1. Chocolate

- 7.1.1.1. By Confectionery Variant

- 7.1.1.1.1. Dark Chocolate

- 7.1.1.1.2. Milk and White Chocolate

- 7.1.1.1. By Confectionery Variant

- 7.1.2. Gums

- 7.1.2.1. Bubble Gum

- 7.1.2.2. Chewing Gum

- 7.1.2.2.1. By Sugar Content

- 7.1.2.2.1.1. Sugar Chewing Gum

- 7.1.2.2.1.2. Sugar-free Chewing Gum

- 7.1.2.2.1. By Sugar Content

- 7.1.3. Snack Bar

- 7.1.3.1. Cereal Bar

- 7.1.3.2. Fruit & Nut Bar

- 7.1.3.3. Protein Bar

- 7.1.4. Sugar Confectionery

- 7.1.4.1. Hard Candy

- 7.1.4.2. Lollipops

- 7.1.4.3. Mints

- 7.1.4.4. Pastilles, Gummies, and Jellies

- 7.1.4.5. Toffees and Nougats

- 7.1.4.6. Others

- 7.1.1. Chocolate

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Convenience Store

- 7.2.2. Online Retail Store

- 7.2.3. Supermarket/Hypermarket

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Confections

- 8. South America UK Confectionery Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Confections

- 8.1.1. Chocolate

- 8.1.1.1. By Confectionery Variant

- 8.1.1.1.1. Dark Chocolate

- 8.1.1.1.2. Milk and White Chocolate

- 8.1.1.1. By Confectionery Variant

- 8.1.2. Gums

- 8.1.2.1. Bubble Gum

- 8.1.2.2. Chewing Gum

- 8.1.2.2.1. By Sugar Content

- 8.1.2.2.1.1. Sugar Chewing Gum

- 8.1.2.2.1.2. Sugar-free Chewing Gum

- 8.1.2.2.1. By Sugar Content

- 8.1.3. Snack Bar

- 8.1.3.1. Cereal Bar

- 8.1.3.2. Fruit & Nut Bar

- 8.1.3.3. Protein Bar

- 8.1.4. Sugar Confectionery

- 8.1.4.1. Hard Candy

- 8.1.4.2. Lollipops

- 8.1.4.3. Mints

- 8.1.4.4. Pastilles, Gummies, and Jellies

- 8.1.4.5. Toffees and Nougats

- 8.1.4.6. Others

- 8.1.1. Chocolate

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Convenience Store

- 8.2.2. Online Retail Store

- 8.2.3. Supermarket/Hypermarket

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Confections

- 9. Europe UK Confectionery Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Confections

- 9.1.1. Chocolate

- 9.1.1.1. By Confectionery Variant

- 9.1.1.1.1. Dark Chocolate

- 9.1.1.1.2. Milk and White Chocolate

- 9.1.1.1. By Confectionery Variant

- 9.1.2. Gums

- 9.1.2.1. Bubble Gum

- 9.1.2.2. Chewing Gum

- 9.1.2.2.1. By Sugar Content

- 9.1.2.2.1.1. Sugar Chewing Gum

- 9.1.2.2.1.2. Sugar-free Chewing Gum

- 9.1.2.2.1. By Sugar Content

- 9.1.3. Snack Bar

- 9.1.3.1. Cereal Bar

- 9.1.3.2. Fruit & Nut Bar

- 9.1.3.3. Protein Bar

- 9.1.4. Sugar Confectionery

- 9.1.4.1. Hard Candy

- 9.1.4.2. Lollipops

- 9.1.4.3. Mints

- 9.1.4.4. Pastilles, Gummies, and Jellies

- 9.1.4.5. Toffees and Nougats

- 9.1.4.6. Others

- 9.1.1. Chocolate

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Convenience Store

- 9.2.2. Online Retail Store

- 9.2.3. Supermarket/Hypermarket

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Confections

- 10. Middle East & Africa UK Confectionery Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Confections

- 10.1.1. Chocolate

- 10.1.1.1. By Confectionery Variant

- 10.1.1.1.1. Dark Chocolate

- 10.1.1.1.2. Milk and White Chocolate

- 10.1.1.1. By Confectionery Variant

- 10.1.2. Gums

- 10.1.2.1. Bubble Gum

- 10.1.2.2. Chewing Gum

- 10.1.2.2.1. By Sugar Content

- 10.1.2.2.1.1. Sugar Chewing Gum

- 10.1.2.2.1.2. Sugar-free Chewing Gum

- 10.1.2.2.1. By Sugar Content

- 10.1.3. Snack Bar

- 10.1.3.1. Cereal Bar

- 10.1.3.2. Fruit & Nut Bar

- 10.1.3.3. Protein Bar

- 10.1.4. Sugar Confectionery

- 10.1.4.1. Hard Candy

- 10.1.4.2. Lollipops

- 10.1.4.3. Mints

- 10.1.4.4. Pastilles, Gummies, and Jellies

- 10.1.4.5. Toffees and Nougats

- 10.1.4.6. Others

- 10.1.1. Chocolate

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Convenience Store

- 10.2.2. Online Retail Store

- 10.2.3. Supermarket/Hypermarket

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Confections

- 11. Asia Pacific UK Confectionery Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Confections

- 11.1.1. Chocolate

- 11.1.1.1. By Confectionery Variant

- 11.1.1.1.1. Dark Chocolate

- 11.1.1.1.2. Milk and White Chocolate

- 11.1.1.1. By Confectionery Variant

- 11.1.2. Gums

- 11.1.2.1. Bubble Gum

- 11.1.2.2. Chewing Gum

- 11.1.2.2.1. By Sugar Content

- 11.1.2.2.1.1. Sugar Chewing Gum

- 11.1.2.2.1.2. Sugar-free Chewing Gum

- 11.1.2.2.1. By Sugar Content

- 11.1.3. Snack Bar

- 11.1.3.1. Cereal Bar

- 11.1.3.2. Fruit & Nut Bar

- 11.1.3.3. Protein Bar

- 11.1.4. Sugar Confectionery

- 11.1.4.1. Hard Candy

- 11.1.4.2. Lollipops

- 11.1.4.3. Mints

- 11.1.4.4. Pastilles, Gummies, and Jellies

- 11.1.4.5. Toffees and Nougats

- 11.1.4.6. Others

- 11.1.1. Chocolate

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Convenience Store

- 11.2.2. Online Retail Store

- 11.2.3. Supermarket/Hypermarket

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Confections

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pimlico Confectioneries Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nestlé SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Chocoladefabriken Lindt & Sprüngli AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Swizzels Matlow Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Polo del Gusto SRL

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 August Storck KG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ferrero International SA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mars Incorporated

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Barry Callebaut AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Arcor S A I C

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 HARIBO Holding GmbH & Co KG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 The Hershey Compan

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Mondelēz International Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Alfred Ritter GmbH & Co KG

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Confiserie Leonidas SA

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Pimlico Confectioneries Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Confectionery Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global UK Confectionery Market Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: North America UK Confectionery Market Revenue (billion), by Confections 2025 & 2033

- Figure 4: North America UK Confectionery Market Volume (K Tons), by Confections 2025 & 2033

- Figure 5: North America UK Confectionery Market Revenue Share (%), by Confections 2025 & 2033

- Figure 6: North America UK Confectionery Market Volume Share (%), by Confections 2025 & 2033

- Figure 7: North America UK Confectionery Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 8: North America UK Confectionery Market Volume (K Tons), by Distribution Channel 2025 & 2033

- Figure 9: North America UK Confectionery Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America UK Confectionery Market Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America UK Confectionery Market Revenue (billion), by Country 2025 & 2033

- Figure 12: North America UK Confectionery Market Volume (K Tons), by Country 2025 & 2033

- Figure 13: North America UK Confectionery Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America UK Confectionery Market Volume Share (%), by Country 2025 & 2033

- Figure 15: South America UK Confectionery Market Revenue (billion), by Confections 2025 & 2033

- Figure 16: South America UK Confectionery Market Volume (K Tons), by Confections 2025 & 2033

- Figure 17: South America UK Confectionery Market Revenue Share (%), by Confections 2025 & 2033

- Figure 18: South America UK Confectionery Market Volume Share (%), by Confections 2025 & 2033

- Figure 19: South America UK Confectionery Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 20: South America UK Confectionery Market Volume (K Tons), by Distribution Channel 2025 & 2033

- Figure 21: South America UK Confectionery Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: South America UK Confectionery Market Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: South America UK Confectionery Market Revenue (billion), by Country 2025 & 2033

- Figure 24: South America UK Confectionery Market Volume (K Tons), by Country 2025 & 2033

- Figure 25: South America UK Confectionery Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America UK Confectionery Market Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe UK Confectionery Market Revenue (billion), by Confections 2025 & 2033

- Figure 28: Europe UK Confectionery Market Volume (K Tons), by Confections 2025 & 2033

- Figure 29: Europe UK Confectionery Market Revenue Share (%), by Confections 2025 & 2033

- Figure 30: Europe UK Confectionery Market Volume Share (%), by Confections 2025 & 2033

- Figure 31: Europe UK Confectionery Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 32: Europe UK Confectionery Market Volume (K Tons), by Distribution Channel 2025 & 2033

- Figure 33: Europe UK Confectionery Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Europe UK Confectionery Market Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Europe UK Confectionery Market Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe UK Confectionery Market Volume (K Tons), by Country 2025 & 2033

- Figure 37: Europe UK Confectionery Market Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe UK Confectionery Market Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa UK Confectionery Market Revenue (billion), by Confections 2025 & 2033

- Figure 40: Middle East & Africa UK Confectionery Market Volume (K Tons), by Confections 2025 & 2033

- Figure 41: Middle East & Africa UK Confectionery Market Revenue Share (%), by Confections 2025 & 2033

- Figure 42: Middle East & Africa UK Confectionery Market Volume Share (%), by Confections 2025 & 2033

- Figure 43: Middle East & Africa UK Confectionery Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 44: Middle East & Africa UK Confectionery Market Volume (K Tons), by Distribution Channel 2025 & 2033

- Figure 45: Middle East & Africa UK Confectionery Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East & Africa UK Confectionery Market Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Middle East & Africa UK Confectionery Market Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa UK Confectionery Market Volume (K Tons), by Country 2025 & 2033

- Figure 49: Middle East & Africa UK Confectionery Market Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa UK Confectionery Market Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific UK Confectionery Market Revenue (billion), by Confections 2025 & 2033

- Figure 52: Asia Pacific UK Confectionery Market Volume (K Tons), by Confections 2025 & 2033

- Figure 53: Asia Pacific UK Confectionery Market Revenue Share (%), by Confections 2025 & 2033

- Figure 54: Asia Pacific UK Confectionery Market Volume Share (%), by Confections 2025 & 2033

- Figure 55: Asia Pacific UK Confectionery Market Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 56: Asia Pacific UK Confectionery Market Volume (K Tons), by Distribution Channel 2025 & 2033

- Figure 57: Asia Pacific UK Confectionery Market Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Asia Pacific UK Confectionery Market Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Asia Pacific UK Confectionery Market Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific UK Confectionery Market Volume (K Tons), by Country 2025 & 2033

- Figure 61: Asia Pacific UK Confectionery Market Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific UK Confectionery Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 2: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 3: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global UK Confectionery Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global UK Confectionery Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 8: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 9: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global UK Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global UK Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: United States UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Canada UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Mexico UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 20: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 21: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global UK Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global UK Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: Brazil UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Argentina UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 32: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 33: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 34: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global UK Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global UK Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 37: United Kingdom UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 39: Germany UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 41: France UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: Italy UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: Spain UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: Russia UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Benelux UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Nordics UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 55: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 56: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 57: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 58: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 59: Global UK Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global UK Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 61: Turkey UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 63: Israel UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 65: GCC UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 67: North Africa UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 69: South Africa UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 73: Global UK Confectionery Market Revenue billion Forecast, by Confections 2020 & 2033

- Table 74: Global UK Confectionery Market Volume K Tons Forecast, by Confections 2020 & 2033

- Table 75: Global UK Confectionery Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 76: Global UK Confectionery Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 77: Global UK Confectionery Market Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global UK Confectionery Market Volume K Tons Forecast, by Country 2020 & 2033

- Table 79: China UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 81: India UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 83: Japan UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 85: South Korea UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 87: ASEAN UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 89: Oceania UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific UK Confectionery Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific UK Confectionery Market Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Confectionery Market?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the UK Confectionery Market?

Key companies in the market include Pimlico Confectioneries Ltd, Nestlé SA, Chocoladefabriken Lindt & Sprüngli AG, Swizzels Matlow Ltd, Polo del Gusto SRL, August Storck KG, Ferrero International SA, Mars Incorporated, Barry Callebaut AG, Arcor S A I C, HARIBO Holding GmbH & Co KG, The Hershey Compan, Mondelēz International Inc, Alfred Ritter GmbH & Co KG, Confiserie Leonidas SA.

3. What are the main segments of the UK Confectionery Market?

The market segments include Confections, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Escalating Demand for Processed Poultry Products; Favorable Government Initiatives to Boost Production.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Rising Vegan Trend among Young Consumers; Deeper Penetration of Red Meat Across Saudi Arabia.

8. Can you provide examples of recent developments in the market?

April 2023: Swizzels Sweets has partnered with Applied Nutrition to launch a range of sports nutrition products in several of Swizzels’ well-known flavors. The sports brand Applied Nutrition announced Drumstick flavor lollies of both its bestselling hydration drink, BodyFuel, and a 60 ml shot variant of its popular pre-workout, A.B.E.April 2023: Under the ONE brand, The Hershey Company launched the Peanut Butter & Jelly Flavored Protein Bar. The ONE Limited Edition Peanut Butter & Jelly flavored bars are packed with 20 g of protein, 1 g of sugar, and the familiar taste of peanut butter and strawberry jelly flavors.March 2023: Nestlé launched a new chocolate bar fused with two flavors, i.e., the Purple One and Green Triangle. These chocolate bars are available in supermarkets across the United Kingdom.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Confectionery Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Confectionery Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Confectionery Market?

To stay informed about further developments, trends, and reports in the UK Confectionery Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence