Key Insights

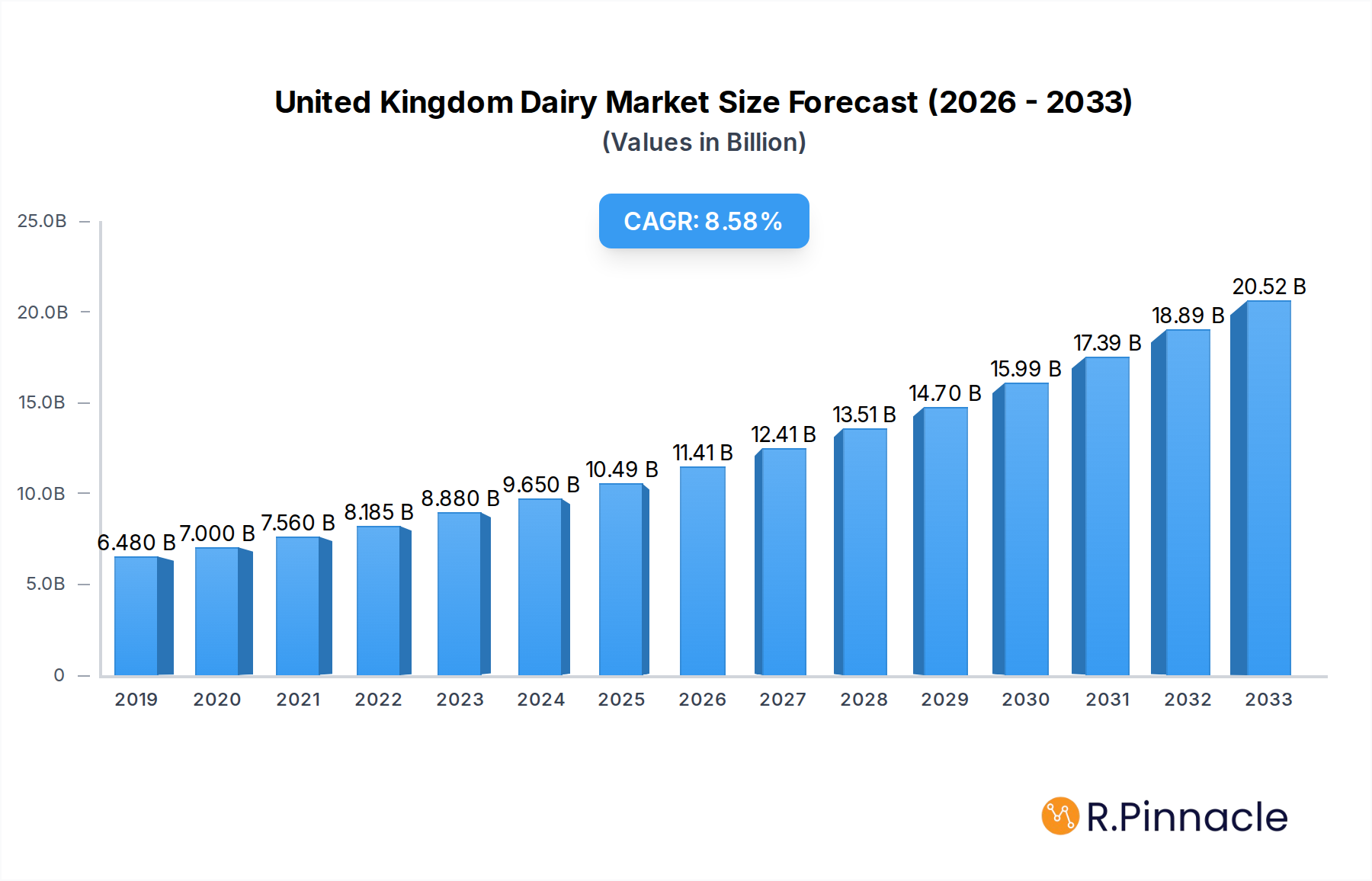

The United Kingdom dairy market is poised for significant expansion, projected to reach approximately USD 9.88 billion in 2024. Driven by a consistent Compound Annual Growth Rate (CAGR) of 9.62%, the market is anticipated to witness robust growth throughout the forecast period extending to 2033. This upward trajectory is largely fueled by evolving consumer preferences towards healthier and more convenient dairy products, coupled with an increasing demand for premium and specialized offerings. The market's dynamism is further underscored by the diverse segmentation, encompassing essential categories like milk, cheese, yogurt, butter, cream, and dairy desserts. Innovation within these segments, particularly in flavored milk, plant-based alternatives subtly integrated within dairy product portfolios, and artisanal cheese varieties, is a key catalyst. Furthermore, the expansion of online retail and convenience stores as primary distribution channels reflects changing shopping habits, contributing to market accessibility and growth.

United Kingdom Dairy Market Market Size (In Billion)

Several factors are shaping the UK dairy landscape. Key growth drivers include a rising awareness of dairy's nutritional benefits, particularly for protein and calcium intake, and a growing acceptance of functional dairy products incorporating probiotics or added vitamins. The influence of food trends, such as the demand for gut-healthy options like yogurts and fermented milk drinks, and the surge in interest for premium ice creams and cheesecakes, are significant contributors. While the market benefits from strong consumer demand and product innovation, it also faces certain restraints. These include the volatility of raw milk prices, increasing operational costs for dairy producers, and the persistent consumer shift towards plant-based alternatives, which, while not entirely replacing dairy, do present a competitive pressure. Despite these challenges, the UK dairy market's resilience and adaptability, supported by a well-established industry infrastructure and leading companies like Bel Group, Arla Foods, and Danone SA, are expected to ensure its continued prosperity.

United Kingdom Dairy Market Company Market Share

Uncover Growth & Innovation: United Kingdom Dairy Market Analysis (2019–2033)

Gain unparalleled insights into the dynamic United Kingdom dairy market with this comprehensive report. Spanning from 2019 to 2033, with a deep dive into the base and estimated year of 2025 and a detailed forecast period from 2025–2033, this analysis provides strategic intelligence for dairy producers, ingredient suppliers, retailers, and investors. Explore market structure, evolving consumer preferences, technological advancements, and dominant regional trends shaping the UK's multi-billion pound dairy industry.

United Kingdom Dairy Market Market Structure & Innovation Trends

The United Kingdom dairy market exhibits a moderate to high level of concentration, with several major international and domestic players dominating significant market share. Key companies like Arla Foods, Danone SA, and Unilever PLC command substantial portions of the consumer-facing dairy product categories, while specialized players like Bel Group and Ornua Co-Operative Limited hold strong positions in specific segments such as cheese. Innovation in the UK dairy sector is primarily driven by evolving consumer demands for healthier, more sustainable, and convenient products. This includes a growing interest in plant-based alternatives, lactose-free options, and products fortified with vitamins and minerals. Regulatory frameworks, including stringent food safety standards and evolving environmental legislation, also significantly influence market operations and product development. Product substitutes, such as plant-based beverages and yogurts, are increasingly impacting traditional dairy consumption. End-user demographics are shifting, with a growing emphasis on health-conscious millennials and an aging population seeking nutrient-dense foods. Mergers and acquisitions (M&A) activity, while not at peak levels, is strategic, focusing on acquiring innovative startups or expanding existing product portfolios. For instance, an M&A deal value of approximately USD 500 million was observed in 2022 for a dairy technology firm.

- Market Concentration: Dominated by a few large multinational corporations alongside a network of regional and specialized producers.

- Innovation Drivers: Health and wellness trends, sustainability concerns, demand for convenient formats, and premiumization.

- Regulatory Frameworks: Strict adherence to food safety (e.g., FSA), labeling, and emerging environmental regulations (e.g., plastic packaging reduction).

- Product Substitutes: Rising popularity of plant-based alternatives, impacting milk, yogurt, and cheese segments.

- End-User Demographics: Growing demand from health-conscious consumers, families, and an aging population seeking functional foods.

- M&A Activities: Strategic acquisitions to gain market access, enhance product offerings, and adopt new technologies.

United Kingdom Dairy Market Market Dynamics & Trends

The United Kingdom dairy market is propelled by a confluence of robust growth drivers, technological disruptions, evolving consumer preferences, and intense competitive dynamics, collectively shaping its trajectory throughout the forecast period. The market's overall value is estimated to reach over £30 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 3.5% from 2025 to 2033. A key driver of this growth is the persistent demand for dairy as a staple in British diets, particularly for milk and cheese. However, significant shifts are underway. Consumer preferences are increasingly leaning towards healthier options, driving demand for low-fat, high-protein, and lactose-free dairy products. This trend is further amplified by a growing awareness of the environmental impact of food production, spurring interest in sustainable farming practices and reduced carbon footprints within the dairy supply chain. Technological disruptions are playing a pivotal role, from advancements in processing and packaging that enhance shelf-life and convenience to the adoption of digital tools in farm management for improved efficiency and animal welfare. The rise of e-commerce and online grocery platforms has fundamentally altered distribution channels, enabling greater accessibility and direct-to-consumer models, thereby increasing market penetration for a wider range of dairy products. Competitive dynamics are characterized by intense brand loyalty in established categories, but also by aggressive innovation and marketing from both traditional players and new entrants, particularly in the burgeoning plant-based alternatives sector. Companies are investing heavily in R&D to develop novel dairy products, such as cultured dairy beverages with probiotic benefits and premium cheese varieties. The "on-trade" sector, encompassing hospitality and food service, continues to be a significant contributor, albeit with evolving consumer tastes influencing menu offerings. The "off-trade" segment, dominated by supermarkets and hypermarkets, remains the largest distribution channel, but online retail is experiencing rapid expansion. The market penetration of specialized dairy products, such as artisanal cheeses and functional yogurts, is steadily increasing, reflecting a consumer appetite for premium and differentiated offerings. The dairy industry's commitment to sustainability, including efforts to reduce methane emissions and improve land use, is also becoming a critical factor in consumer purchasing decisions and overall market perception. Furthermore, the integration of artificial intelligence in dairy farming for optimized feed management and predictive health monitoring is poised to enhance efficiency and profitability.

Dominant Regions & Segments in United Kingdom Dairy Market

The United Kingdom dairy market showcases distinct regional dominance and segment leadership, driven by diverse consumer behaviors, economic factors, and established infrastructure. England consistently emerges as the leading region, accounting for the largest share of dairy consumption and production due to its high population density and sophisticated retail network. Within England, the South East and London regions exhibit the highest per capita consumption of value-added dairy products, including premium cheeses and specialized yogurts, driven by higher disposable incomes and a cosmopolitan consumer base.

The Milk segment, particularly Fresh Milk and UHT Milk, remains the bedrock of the UK dairy market, representing a substantial market share by volume. However, growth in this segment is moderate, often influenced by price sensitivity and the increasing adoption of plant-based alternatives. The dominance of fresh milk is attributed to its daily necessity for households, while UHT milk's extended shelf-life makes it a crucial product for retail and food service.

The Cheese segment, encompassing both Natural Cheese and Processed Cheese, is a powerhouse of growth and innovation. Natural cheese, in particular, is experiencing robust expansion, driven by demand for a wider variety of artisanal, specialty, and continental cheeses. The UK's strong cheese-making heritage, coupled with increasing consumer interest in gourmet food experiences, fuels this dominance. Key drivers include the popularity of cheese boards, snacking culture, and its versatility in culinary applications.

Milk Segment Dominance:

- Key Drivers: Essential daily consumption, affordability, perceived nutritional value.

- Detailed Dominance Analysis: Fresh milk remains paramount for immediate consumption, supported by extensive retail availability. UHT milk offers convenience and extended shelf-life, making it a staple in pantries. Growth is moderated by the rise of dairy alternatives.

Cheese Segment Dominance:

- Key Drivers: Culinary versatility, premiumization, growing interest in artisanal and specialty varieties, snacking trends.

- Detailed Dominance Analysis: Natural cheese leads growth due to evolving consumer palates and exploration of diverse flavors and textures. Processed cheese maintains a strong presence in convenience foods and food service. The market is segmented by strong consumer preference for Cheddar, but with increasing demand for international and regional cheeses.

The Yogurt segment, with Flavored Yogurt leading in volume, is another significant contributor. Growth is driven by its appeal as a healthy breakfast option, snack, and dessert. The market is characterized by a continuous stream of new flavors, functional benefits (e.g., probiotics, added protein), and convenient packaging formats.

- Yogurt Segment Dominance:

- Key Drivers: Health and wellness perception, versatility as a snack or dessert, innovation in flavors and functional benefits.

- Detailed Dominance Analysis: Flavored yogurts capture a larger market share due to their broader appeal. Unflavored variants are gaining traction among health-conscious consumers seeking natural options or for use in cooking and baking.

The Cream segment, with Double Cream and Single Cream being the most popular, serves essential culinary and dessert applications. While not a high-growth segment, it maintains a steady demand, particularly within the food service industry and for premium home baking.

- Cream Segment Dominance:

- Key Drivers: Culinary applications, indulgence, use in desserts and baking.

- Detailed Dominance Analysis: Double and single creams are widely used in traditional British cuisine and baking. Whipping cream caters to dessert decoration and specific recipes.

Distribution channel dominance is firmly with the Off-Trade segment, primarily Supermarkets and Hypermarkets, which account for the largest share of dairy product sales. However, Online Retail is experiencing rapid and significant growth, driven by convenience and the expansion of online grocery platforms.

- Off-Trade Distribution Dominance:

- Key Drivers: Extensive reach, convenience, price competitiveness, wide product selection.

- Detailed Dominance Analysis: Supermarkets and hypermarkets are the primary conduits for dairy products due to their extensive customer base and prime locations. Convenience stores and specialist retailers cater to impulse buys and niche markets.

Industry Developments:

November 2022: Ornua Foods UK's investment of USD 3.77 million in state-of-the-art cutting and packing equipment at its Leek facility is a prime example of sector-specific investment aimed at enhancing production capacity and efficiency. The addition of a high-speed cheese-slicing line and expanded grating capabilities, projected to add 7,000 metric tons of capacity for a total exceeding 110,000 metric tons annually, directly addresses the growing demand for pre-packaged and ready-to-use cheese products. This development signifies a strategic move to capitalize on market trends favoring convenience and quality in the cheese sector.

September 2021: Bel UK's launch of flavored hot cheese bites under its Boursin brand exemplifies product innovation and market diversification. This initiative tapped into the growing consumer interest in novel snacking options and convenient, ready-to-heat food products. The expansion of an existing, well-established brand into a new product category demonstrates a keen understanding of evolving consumer lifestyles and a proactive approach to capturing new market segments.

November 2020: Dairy Farm's introduction of a Fixed Milk Price Contract for its 1,300 milk producers highlights a crucial development in addressing market volatility and ensuring farmer stability. By offering a guaranteed price for three years, this initiative provides essential financial security to milk producers, mitigating the risks associated with fluctuating commodity markets. This proactive measure can foster greater investment in farm infrastructure and sustainability practices, ultimately contributing to a more resilient and predictable dairy supply chain.

United Kingdom Dairy Market Product Innovations

Product innovations in the UK dairy market are increasingly focused on health, convenience, and sustainability. There's a surge in demand for lactose-free and reduced-lactose dairy options, catering to a significant portion of the population experiencing lactose intolerance. Plant-based alternatives, while technically not dairy, are a major disruptor and influence dairy innovation towards enriched and functional products. Companies are developing yogurts and milk drinks fortified with probiotics, vitamins (e.g., Vitamin D, B12), and minerals, aligning with the growing consumer focus on gut health and overall well-being. Premiumization is also a key trend, with the introduction of artisanal cheeses, single-origin dairy products, and luxury dairy desserts. Innovations in packaging, such as recyclable materials and convenient single-serving formats, further enhance product appeal and market fit.

Report Scope & Segmentation Analysis

This report meticulously analyzes the United Kingdom dairy market, segmented by product category and distribution channel. The product categories include Butter (Cultured Butter, Uncultured Butter), Cheese (Natural Cheese, Processed Cheese), Cream (Double Cream, Single Cream, Whipping Cream, Others), Dairy Desserts (Cheesecakes, Frozen Desserts, Ice Cream, Mousses), Milk (Condensed milk, Flavored Milk, Fresh Milk, Powdered Milk, UHT Milk), Sour Milk Drinks, and Yogurt (Flavored Yogurt, Unflavored Yogurt). Distribution channels are divided into Off-Trade (Convenience Stores, Online Retail, Specialist Retailers, Supermarkets and Hypermarkets, Others) and On-Trade. The market is projected to witness significant growth in the Cheese and Dairy Desserts segments, driven by premiumization and indulgent consumption trends. Online retail is expected to be the fastest-growing distribution channel.

Key Drivers of United Kingdom Dairy Market Growth

The growth of the United Kingdom dairy market is underpinned by several key drivers:

- Rising Health Consciousness: An increasing consumer focus on health and wellness fuels demand for fortified dairy products, low-fat options, and those with functional benefits like probiotics.

- Convenience and Ready-to-Eat Options: Busy lifestyles drive demand for convenient dairy formats, including pre-portioned yogurts, ready-to-cook cheese, and milk drinks.

- Premiumization and Indulgence: A growing consumer willingness to spend on higher-quality, artisanal, and specialty dairy products, particularly in the cheese and dessert segments.

- Technological Advancements: Innovations in processing, packaging, and farm management enhance efficiency, product quality, and sustainability.

- Growing Food Service Sector: The demand from restaurants, cafes, and hotels for diverse dairy ingredients and products continues to support market expansion.

Challenges in the United Kingdom Dairy Market Sector

Despite robust growth prospects, the UK dairy market faces several challenges:

- Intensifying Competition from Plant-Based Alternatives: The rapidly expanding market for plant-based milk, yogurt, and cheese poses a significant competitive threat to traditional dairy products.

- Price Volatility and Input Costs: Fluctuations in raw material prices, energy costs, and labor expenses can impact profit margins for dairy producers.

- Regulatory and Environmental Pressures: Increasing scrutiny on environmental impact, emissions, and packaging waste necessitates significant investment in sustainable practices.

- Supply Chain Disruptions: Geopolitical events and logistical challenges can lead to disruptions in the supply chain, affecting product availability and costs.

- Consumer Perception and Ethical Concerns: Public discourse around animal welfare and the environmental impact of dairy farming can influence consumer choices.

Emerging Opportunities in United Kingdom Dairy Market

Emerging opportunities within the UK dairy market are ripe for exploitation:

- Functional Dairy Products: Development of dairy items with enhanced health benefits, such as improved digestion, immune support, and bone health, appealing to a health-conscious consumer base.

- Sustainable Dairy Farming: Investments in and promotion of environmentally friendly farming practices, such as reduced methane emissions and improved land management, can attract eco-conscious consumers.

- Niche and Specialty Dairy: Expansion of the artisanal cheese market, unique dairy dessert flavors, and specialized milk types to cater to discerning palates.

- E-commerce and Direct-to-Consumer Models: Leveraging online platforms for wider reach, personalized offerings, and faster delivery of fresh dairy products.

- Value-Added Dairy Ingredients: Opportunities in supplying specialized dairy ingredients to the food manufacturing sector for use in processed foods, beverages, and supplements.

Leading Players in the United Kingdom Dairy Market Market

- Bel Group

- Arla Foods

- Unilever PLC

- Glanbia PLC

- Danone SA

- Dale Farm Cooperative Limited

- Muller Group

- Ornua Co-Operative Limited

- Kingcott Dairy

- Saputo Inc

Key Developments in United Kingdom Dairy Market Industry

- November 2022: Ornua Foods UK invested USD 3.77 million in state-of-the-art cutting and packing equipment at its Leek facility, enhancing cheese production capacity by an additional 7,000 metric tons.

- September 2021: Bel UK launched a range of flavored hot cheese bites under its Boursin brand, expanding its product portfolio in the convenience food segment.

- November 2020: Dairy Farm introduced a Fixed Milk Price Contract option for its 1,300 milk producers, offering price stability for three years to protect against market volatility.

Future Outlook for United Kingdom Dairy Market Market

The future outlook for the United Kingdom dairy market is characterized by sustained growth, driven by a blend of established demand and evolving consumer preferences. Innovation in health-focused and sustainable dairy products will continue to be paramount, alongside the increasing integration of technology across the value chain. The market is poised to benefit from a growing appreciation for premium and specialty dairy items, while the rapid expansion of online retail will reshape distribution strategies. Companies that prioritize sustainability, product differentiation, and adapting to the competitive landscape, particularly in relation to plant-based alternatives, will be best positioned for future success. The ongoing investment in production efficiency and capacity expansion by key players indicates confidence in the long-term viability and growth potential of the UK dairy sector.

United Kingdom Dairy Market Segmentation

-

1. Category

-

1.1. Butter

-

1.1.1. By Product Type

- 1.1.1.1. Cultured Butter

- 1.1.1.2. Uncultured Butter

-

1.1.1. By Product Type

-

1.2. Cheese

- 1.2.1. Natural Cheese

- 1.2.2. Processed Cheese

-

1.3. Cream

- 1.3.1. Double Cream

- 1.3.2. Single Cream

- 1.3.3. Whipping Cream

- 1.3.4. Others

-

1.4. Dairy Desserts

- 1.4.1. Cheesecakes

- 1.4.2. Frozen Desserts

- 1.4.3. Ice Cream

- 1.4.4. Mousses

-

1.5. Milk

- 1.5.1. Condensed milk

- 1.5.2. Flavored Milk

- 1.5.3. Fresh Milk

- 1.5.4. Powdered Milk

- 1.5.5. UHT Milk

- 1.6. Sour Milk Drinks

-

1.7. Yogurt

- 1.7.1. Flavored Yogurt

- 1.7.2. Unflavored Yogurt

-

1.1. Butter

-

2. Distribution Channel

-

2.1. Off-Trade

- 2.1.1. Convenience Stores

- 2.1.2. Online Retail

- 2.1.3. Specialist Retailers

- 2.1.4. Supermarkets and Hypermarkets

- 2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 2.2. On-Trade

-

2.1. Off-Trade

United Kingdom Dairy Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Dairy Market Regional Market Share

Geographic Coverage of United Kingdom Dairy Market

United Kingdom Dairy Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Butter

- 5.1.1.1. By Product Type

- 5.1.1.1.1. Cultured Butter

- 5.1.1.1.2. Uncultured Butter

- 5.1.1.1. By Product Type

- 5.1.2. Cheese

- 5.1.2.1. Natural Cheese

- 5.1.2.2. Processed Cheese

- 5.1.3. Cream

- 5.1.3.1. Double Cream

- 5.1.3.2. Single Cream

- 5.1.3.3. Whipping Cream

- 5.1.3.4. Others

- 5.1.4. Dairy Desserts

- 5.1.4.1. Cheesecakes

- 5.1.4.2. Frozen Desserts

- 5.1.4.3. Ice Cream

- 5.1.4.4. Mousses

- 5.1.5. Milk

- 5.1.5.1. Condensed milk

- 5.1.5.2. Flavored Milk

- 5.1.5.3. Fresh Milk

- 5.1.5.4. Powdered Milk

- 5.1.5.5. UHT Milk

- 5.1.6. Sour Milk Drinks

- 5.1.7. Yogurt

- 5.1.7.1. Flavored Yogurt

- 5.1.7.2. Unflavored Yogurt

- 5.1.1. Butter

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Off-Trade

- 5.2.1.1. Convenience Stores

- 5.2.1.2. Online Retail

- 5.2.1.3. Specialist Retailers

- 5.2.1.4. Supermarkets and Hypermarkets

- 5.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 5.2.2. On-Trade

- 5.2.1. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. United Kingdom Dairy Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Category

- 6.1.1. Butter

- 6.1.1.1. By Product Type

- 6.1.1.1.1. Cultured Butter

- 6.1.1.1.2. Uncultured Butter

- 6.1.1.1. By Product Type

- 6.1.2. Cheese

- 6.1.2.1. Natural Cheese

- 6.1.2.2. Processed Cheese

- 6.1.3. Cream

- 6.1.3.1. Double Cream

- 6.1.3.2. Single Cream

- 6.1.3.3. Whipping Cream

- 6.1.3.4. Others

- 6.1.4. Dairy Desserts

- 6.1.4.1. Cheesecakes

- 6.1.4.2. Frozen Desserts

- 6.1.4.3. Ice Cream

- 6.1.4.4. Mousses

- 6.1.5. Milk

- 6.1.5.1. Condensed milk

- 6.1.5.2. Flavored Milk

- 6.1.5.3. Fresh Milk

- 6.1.5.4. Powdered Milk

- 6.1.5.5. UHT Milk

- 6.1.6. Sour Milk Drinks

- 6.1.7. Yogurt

- 6.1.7.1. Flavored Yogurt

- 6.1.7.2. Unflavored Yogurt

- 6.1.1. Butter

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Off-Trade

- 6.2.1.1. Convenience Stores

- 6.2.1.2. Online Retail

- 6.2.1.3. Specialist Retailers

- 6.2.1.4. Supermarkets and Hypermarkets

- 6.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 6.2.2. On-Trade

- 6.2.1. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Category

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bel Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Arla Foods

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Unilever PL

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Glanbia PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Danone SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Dale Farm Cooperative Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Muller Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ornua Co-Operative Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Kingcott Dairy

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Saputo Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bel Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Dairy Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United Kingdom Dairy Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Dairy Market Revenue billion Forecast, by Category 2020 & 2033

- Table 2: United Kingdom Dairy Market Volume K Tons Forecast, by Category 2020 & 2033

- Table 3: United Kingdom Dairy Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: United Kingdom Dairy Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: United Kingdom Dairy Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United Kingdom Dairy Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: United Kingdom Dairy Market Revenue billion Forecast, by Category 2020 & 2033

- Table 8: United Kingdom Dairy Market Volume K Tons Forecast, by Category 2020 & 2033

- Table 9: United Kingdom Dairy Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: United Kingdom Dairy Market Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 11: United Kingdom Dairy Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Dairy Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Dairy Market?

The projected CAGR is approximately 9.62%.

2. Which companies are prominent players in the United Kingdom Dairy Market?

Key companies in the market include Bel Group, Arla Foods, Unilever PL, Glanbia PLC, Danone SA, Dale Farm Cooperative Limited, Muller Group, Ornua Co-Operative Limited, Kingcott Dairy, Saputo Inc.

3. What are the main segments of the United Kingdom Dairy Market?

The market segments include Category, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.88 billion as of 2022.

5. What are some drivers contributing to market growth?

Surge in Participation of Sports Activities; Functional and Processing Bnefits of Whey Protein.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Manufacturing Costs and Fluctuations in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

November 2022: Ornua Foods UK invested USD 3.77 million in state-of-the-art cutting and packing equipment at its Leek facility. The latest investment may see the installation of an additional high-speed cheese-slicing line and the further expansion of Ornua's cheese-grating capabilities. Overall, the new state-of-the-art equipment is expected to result in an additional 7,000 metric tons of capacity, bringing the total annual production to over 110,000 metric tons.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Dairy Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Dairy Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Dairy Market?

To stay informed about further developments, trends, and reports in the United Kingdom Dairy Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence