Key Insights

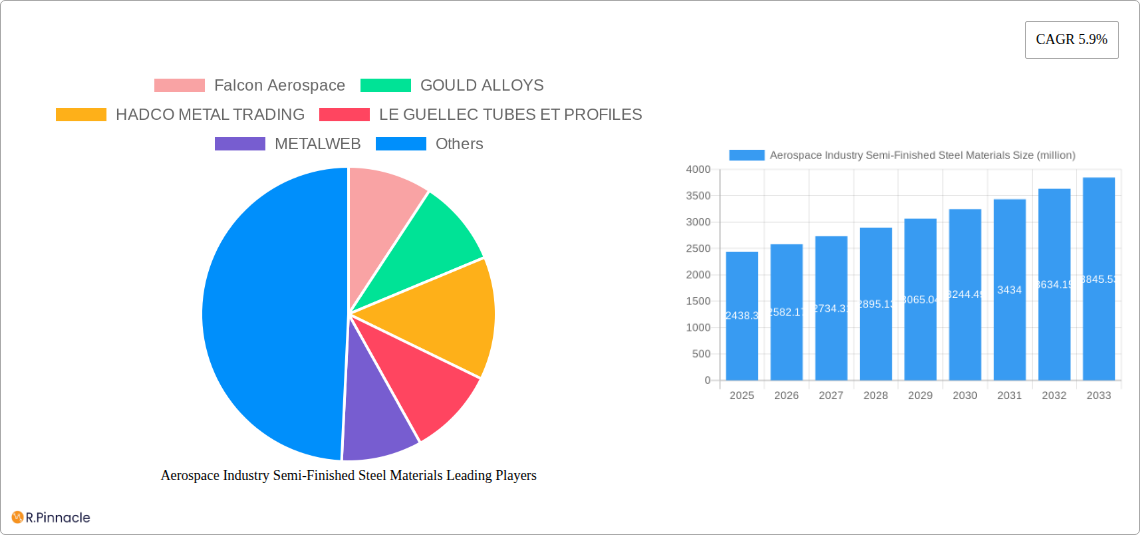

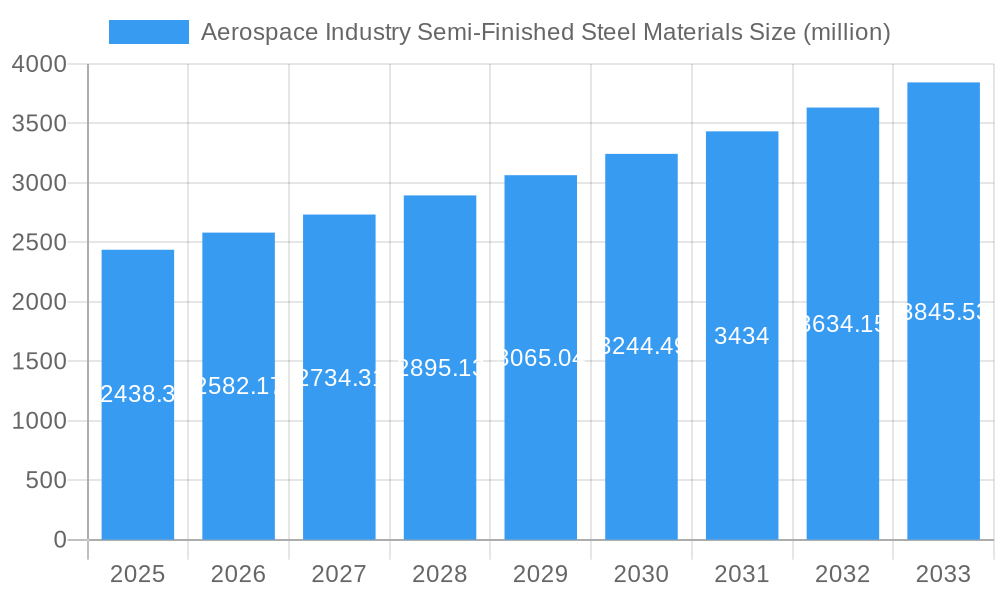

The global market for Aerospace Industry Semi-Finished Steel Materials is poised for significant expansion, driven by robust growth in the aviation and space sectors. Valued at $2438.3 million in 2025, the market is projected to witness a Compound Annual Growth Rate (CAGR) of 5.9% during the forecast period of 2025-2033. This sustained growth is primarily fueled by the increasing demand for lightweight, high-strength steel components in aircraft manufacturing, guided missiles, and space vehicles. The continuous innovation in aerospace technology, leading to the development of advanced aircraft with enhanced fuel efficiency and performance, directly translates to a higher consumption of specialized semi-finished steel products like rods, sheets, and plates. Furthermore, the burgeoning space exploration initiatives and the rapid growth of the commercial satellite market are creating new avenues for market expansion. Key drivers include the expansion of global air travel, increased defense spending, and the development of next-generation aerospace platforms.

Aerospace Industry Semi-Finished Steel Materials Market Size (In Billion)

The market's trajectory is further shaped by key trends such as the growing adoption of advanced high-strength steels (AHSS) and specialized alloys that offer superior performance characteristics. These materials are crucial for meeting stringent safety regulations and performance requirements in the aerospace industry. While the market is experiencing robust growth, certain factors may present challenges. These include the fluctuating raw material prices, particularly for critical alloying elements, and the complex and stringent regulatory landscape governing aerospace material production and certification. The competitive landscape is characterized by the presence of several prominent players, including Falcon Aerospace, GOULD ALLOYS, HADCO METAL TRADING, and SANDVIK MATERIALS TECHNOLOGY, who are continuously investing in research and development to offer innovative solutions and expand their market reach. The market is segmented by application into Aircraft, Guided Missiles, Space Vehicles, and Others, with Aircraft forming the largest segment. By type, Rod, Sheet, Plate, Tube, and Others represent the key product categories. Geographically, North America and Europe currently hold significant market shares, driven by established aerospace manufacturing hubs, while the Asia Pacific region is emerging as a high-growth market due to expanding manufacturing capabilities and increasing air travel demand.

Aerospace Industry Semi-Finished Steel Materials Company Market Share

Unlock the Future of Aerospace with Our Definitive Report on Semi-Finished Steel Materials

This comprehensive report provides an in-depth analysis of the Aerospace Industry Semi-Finished Steel Materials Market, a critical sector driving innovation in aviation, defense, and space exploration. Spanning from 2019 to 2033, this study offers unparalleled insights into market dynamics, competitive landscapes, and future growth trajectories. Leverage our expert analysis to make informed strategic decisions and stay ahead of the curve.

Aerospace Industry Semi-Finished Steel Materials Market Structure & Innovation Trends

The Aerospace Industry Semi-Finished Steel Materials Market exhibits a moderately concentrated structure, with key players like Tata Steel, Sandvik Materials Technology, and Reliance Steel and Aluminum holding significant market share, estimated at over 40% collectively by value in the base year of 2025. Innovation is primarily driven by the relentless demand for lighter, stronger, and more heat-resistant materials to improve aircraft fuel efficiency and performance in extreme aerospace environments. Regulatory frameworks, such as stringent aerospace material certifications and international trade agreements, play a crucial role in shaping market entry and product development. While direct product substitutes for high-performance semi-finished steel in critical aerospace applications are limited, advancements in composite materials and titanium alloys present indirect competitive pressures. End-user demographics are dominated by major aircraft manufacturers, defense contractors, and space agencies, whose evolving requirements dictate material specifications. Mergers and acquisitions are sporadic but strategic, with notable deals in the historical period amounting to over $500 million, aimed at consolidating market position and expanding technological capabilities.

Aerospace Industry Semi-Finished Steel Materials Market Dynamics & Trends

The Aerospace Industry Semi-Finished Steel Materials Market is poised for robust growth, driven by several interconnected factors throughout the forecast period of 2025–2033. A primary growth accelerator is the continuous expansion of global air travel, leading to increased demand for new commercial aircraft, which in turn fuels the need for sophisticated semi-finished steel components. The burgeoning defense sector, with its emphasis on advanced fighter jets, drones, and missile systems, also contributes significantly to market expansion. Furthermore, the growing investments in space exploration and commercial space ventures by both governmental agencies and private entities are creating novel demand for specialized high-strength, lightweight steel alloys. Technological disruptions are continuously pushing the boundaries of material science. Advancements in steel alloying, heat treatment processes, and additive manufacturing techniques are enabling the creation of materials with superior mechanical properties, such as enhanced tensile strength, improved fatigue resistance, and exceptional corrosion resistance. These innovations are crucial for meeting the ever-increasing performance demands of modern aerospace applications, where weight reduction and operational lifespan are paramount. Consumer preferences, while largely dictated by the stringent requirements of aerospace engineers and regulatory bodies, are leaning towards materials that offer a better balance of performance, cost-effectiveness, and sustainability. Manufacturers are increasingly seeking materials that are easier to process and fabricate, while also adhering to environmental regulations and promoting a circular economy. Competitive dynamics within the market are characterized by intense innovation and strategic partnerships. Companies are investing heavily in research and development to introduce next-generation steel grades and to optimize their manufacturing processes. The market penetration of advanced alloys is expected to increase, driven by their ability to meet the demanding specifications of next-generation aircraft and spacecraft. The overall market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period, reaching an estimated market size of over $35,000 million by 2033. This growth is underpinned by the persistent need for reliable, high-performance materials in an industry that is constantly striving for greater efficiency, safety, and capability.

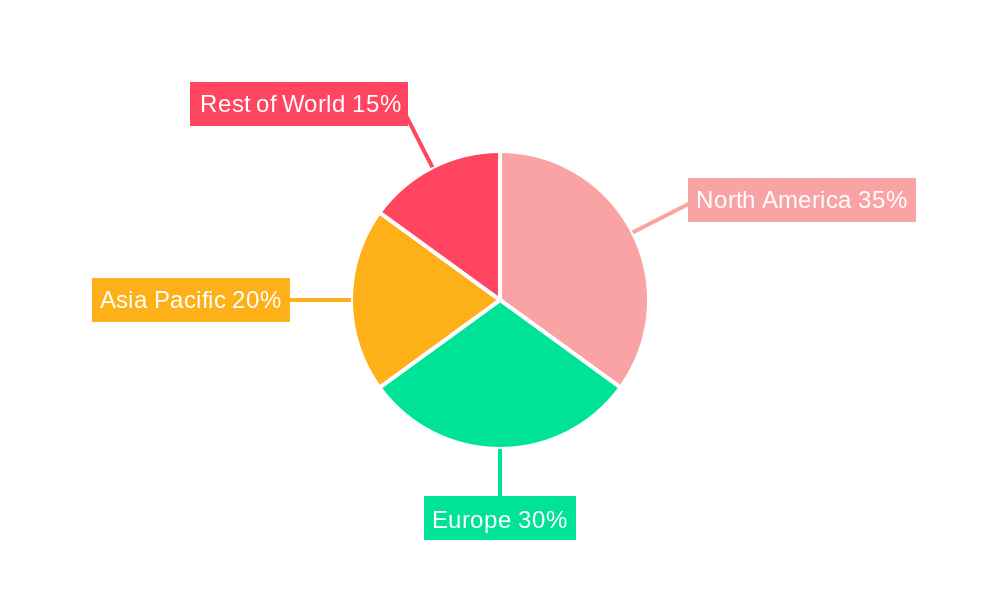

Dominant Regions & Segments in Aerospace Industry Semi-Finished Steel Materials

North America, particularly the United States, is the dominant region in the Aerospace Industry Semi-Finished Steel Materials Market. This leadership is attributed to the presence of the world's largest aerospace manufacturers, significant defense spending, and a well-established research and development ecosystem. Key economic policies supporting the defense and aerospace sectors, coupled with substantial investments in space exploration initiatives, further solidify its leading position. Countries like Germany, France, and the United Kingdom in Europe also hold substantial market share due to their strong aerospace manufacturing bases and innovation capabilities.

Within the Application segment, Aircraft applications represent the largest and most influential segment, accounting for an estimated 65% of the market value in 2025. The continuous demand for commercial airliners, business jets, and military aircraft, driven by global passenger traffic growth and defense modernization efforts, ensures sustained demand for semi-finished steel materials. The Guided Missiles segment is also a significant contributor, with its growth tied to geopolitical stability and defense spending, projected to grow at a CAGR of 6.0% during the forecast period. Space Vehicles, though currently a smaller segment, is experiencing rapid expansion due to increased private investment in space exploration and satellite technology, with an estimated market size of over $3,000 million by 2033.

In terms of Types, Plate and Sheet materials collectively constitute the largest share of the market, estimated at over 50% in 2025. These forms are indispensable for structural components, fuselage sections, wings, and internal frameworks of aircraft and spacecraft. The Tube segment is also critical, particularly for hydraulic systems, fuel lines, and exhaust components, projected to witness a steady growth of 5.2% CAGR. Rod applications, while smaller, are essential for fasteners, fittings, and various smaller machined parts.

Aerospace Industry Semi-Finished Steel Materials Product Innovations

Product innovations in Aerospace Industry Semi-Finished Steel Materials are centered on enhancing material properties for critical applications. Developments include advanced high-strength steel (AHSS) alloys with improved yield strength and fracture toughness, alongside specialized stainless steels and nickel-based superalloys designed for extreme temperature resistance and corrosion prevention in jet engines and spacecraft. Applications range from structural airframe components to critical engine parts and landing gear. Competitive advantages are derived from superior performance metrics, reduced weight, increased durability, and cost-effectiveness in the long run, directly addressing the aerospace industry’s drive for greater efficiency and safety.

Report Scope & Segmentation Analysis

This report meticulously segments the Aerospace Industry Semi-Finished Steel Materials Market by Application and Type.

Aircraft: This segment, projected to reach over $20,000 million by 2033, encompasses all civilian and military aircraft. Growth is propelled by fleet expansion and replacement cycles, with manufacturers focusing on lightweight, high-strength steel for optimal performance and fuel efficiency.

Guided Missiles: This segment, valued at over $5,000 million in 2025, includes materials for various missile systems. Demand is driven by defense budgets and technological advancements in missile capabilities, requiring materials that can withstand extreme conditions.

Space Vehicles: Expected to grow at a CAGR of 7.0%, this segment, estimated at over $3,000 million by 2033, covers satellites, rockets, and probes. Innovation in materials is crucial for space missions' success, focusing on light weight, radiation resistance, and thermal stability.

Others: This segment includes materials for auxiliary aerospace components and ground support equipment, contributing an estimated $2,000 million to the market.

Rod: This segment, with an estimated market size of over $4,000 million by 2033, is vital for fasteners, fittings, and specialized machined parts, characterized by consistent demand and technological refinements for precision applications.

Sheet: Valued at over $10,000 million in 2025, sheets are fundamental for airframes, fuselage panels, and internal structures, with continuous innovation in gauge and alloy composition for weight optimization.

Plate: This segment, expected to reach over $12,000 million by 2033, is essential for heavier structural components, bulkheads, and wing spars, benefiting from advancements in high-strength alloy development.

Tube: With an estimated market size of over $6,000 million by 2033, tubes are critical for hydraulic, fuel, and environmental control systems, focusing on pressure resistance and durability.

Others: This segment includes specialized forms and custom profiles, contributing an estimated $1,000 million to the market.

Key Drivers of Aerospace Industry Semi-Finished Steel Materials Growth

The growth of the Aerospace Industry Semi-Finished Steel Materials Market is propelled by several key drivers. The escalating global demand for air travel, leading to increased aircraft production, is a primary economic driver. Technological advancements in metallurgy are yielding advanced steel alloys with superior strength-to-weight ratios and enhanced performance in extreme conditions, crucial for next-generation aircraft and space vehicles. Government investments in defense modernization and space exploration programs worldwide provide significant impetus. Furthermore, a growing emphasis on sustainability is driving the demand for recyclable and energy-efficient material solutions. Regulatory mandates for enhanced safety and performance standards also necessitate the adoption of cutting-edge materials.

Challenges in the Aerospace Industry Semi-Finished Steel Materials Sector

The Aerospace Industry Semi-Finished Steel Materials Sector faces several significant challenges. Stringent regulatory compliance and the lengthy certification processes for new materials can impede market entry and slow down innovation adoption. The high cost of raw materials and advanced processing techniques contributes to higher product prices, impacting affordability. Supply chain disruptions, as witnessed in recent global events, can lead to material shortages and price volatility, affecting production schedules. Intense competition from alternative materials like advanced composites and titanium alloys, which offer similar or superior performance in certain applications, presents a continuous threat. Moreover, the skilled labor shortage in specialized manufacturing and metallurgical expertise can hinder production capacity and innovation.

Emerging Opportunities in Aerospace Industry Semi-Finished Steel Materials

Emerging opportunities in the Aerospace Industry Semi-Finished Steel Materials Market are diverse and promising. The rapid growth of the commercial space industry, including satellite constellations and space tourism, presents a significant new market for specialized steel alloys. The ongoing development of sustainable aviation fuels and electric aircraft is creating a demand for lighter, more efficient materials. Advancements in additive manufacturing (3D printing) for aerospace components open new avenues for customized steel parts with complex geometries, reducing waste and improving efficiency. The increasing focus on MRO (Maintenance, Repair, and Overhaul) activities also generates demand for high-quality semi-finished steel for component refurbishment and replacement. Furthermore, the development of "smart" materials with integrated sensing capabilities for structural health monitoring in aircraft is an emerging frontier.

Leading Players in the Aerospace Industry Semi-Finished Steel Materials Market

- Falcon Aerospace

- GOULD ALLOYS

- HADCO METAL TRADING

- LE GUELLEC TUBES ET PROFILES

- METALWEB

- MILTECH INTERNATIONAL

- Paris Saint-Denis Aero

- Brookfield Wire

- CASTLE METALS

- CMK

- DEVILLE RECTIFICATION

- DYNAMIC METALS

- QuesTek Innovations

- RELIANCE STEEL AND ALUMINUM

- SAMUEL, SON & CO.

- SANDVIK MATERIALS TECHNOLOGY

- Smith Metal Centres

- Tata Steel

- PLYMOUTH TUBE

- BRALCO METALS

- Titanium Industries

- Aerocom Metals

- ATI

- BOHLER BLECHE

Key Developments in Aerospace Industry Semi-Finished Steel Materials Industry

- 2023 January: Tata Steel announces a breakthrough in developing a new generation of ultra-high-strength steel for next-generation fighter jets.

- 2023 March: Sandvik Materials Technology unveils an advanced alloy for aerospace engine components, offering enhanced high-temperature resistance.

- 2023 May: Reliance Steel and Aluminum acquires a specialized aerospace metal distributor, expanding its reach in the North American market.

- 2023 August: ATI introduces a novel manufacturing process for aerospace-grade steel plates, improving structural integrity and reducing lead times.

- 2023 October: The European Union implements new regulations for aerospace material traceability and sustainability, impacting supply chain practices.

- 2024 February: A major aerospace manufacturer partners with CMK to develop lightweight steel alloys for commercial aircraft interiors.

- 2024 April: Plymouth Tube secures a significant contract to supply specialized steel tubes for a new satellite launch vehicle program.

- 2024 June: QuesTek Innovations collaborates with a leading aerospace firm to develop AI-driven material design solutions for future aircraft.

Future Outlook for Aerospace Industry Semi-Finished Steel Materials Market

The future outlook for the Aerospace Industry Semi-Finished Steel Materials Market is exceptionally positive, driven by sustained innovation and expanding application areas. The continued growth in air travel and the burgeoning commercial space sector will be primary growth accelerators. Advances in additive manufacturing and intelligent material design will enable the creation of highly customized, performance-optimized steel components, reducing waste and lead times. The increasing focus on environmental sustainability will drive the development of recyclable and energy-efficient steel grades. Strategic collaborations between material suppliers and aerospace manufacturers will be crucial for co-developing solutions that meet the ever-evolving demands for lighter, stronger, and more resilient materials, ensuring a robust and dynamic market trajectory for years to come.

Aerospace Industry Semi-Finished Steel Materials Segmentation

-

1. Application

- 1.1. Aircraft

- 1.2. Guided Missiles

- 1.3. Space Vehicles

- 1.4. Others

-

2. Types

- 2.1. Rod

- 2.2. Sheet

- 2.3. Plate

- 2.4. Tube

- 2.5. Others

Aerospace Industry Semi-Finished Steel Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aerospace Industry Semi-Finished Steel Materials Regional Market Share

Geographic Coverage of Aerospace Industry Semi-Finished Steel Materials

Aerospace Industry Semi-Finished Steel Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aircraft

- 5.1.2. Guided Missiles

- 5.1.3. Space Vehicles

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Rod

- 5.2.2. Sheet

- 5.2.3. Plate

- 5.2.4. Tube

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aircraft

- 6.1.2. Guided Missiles

- 6.1.3. Space Vehicles

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Rod

- 6.2.2. Sheet

- 6.2.3. Plate

- 6.2.4. Tube

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aircraft

- 7.1.2. Guided Missiles

- 7.1.3. Space Vehicles

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Rod

- 7.2.2. Sheet

- 7.2.3. Plate

- 7.2.4. Tube

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aircraft

- 8.1.2. Guided Missiles

- 8.1.3. Space Vehicles

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Rod

- 8.2.2. Sheet

- 8.2.3. Plate

- 8.2.4. Tube

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aircraft

- 9.1.2. Guided Missiles

- 9.1.3. Space Vehicles

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Rod

- 9.2.2. Sheet

- 9.2.3. Plate

- 9.2.4. Tube

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aircraft

- 10.1.2. Guided Missiles

- 10.1.3. Space Vehicles

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Rod

- 10.2.2. Sheet

- 10.2.3. Plate

- 10.2.4. Tube

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Aerospace Industry Semi-Finished Steel Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Aircraft

- 11.1.2. Guided Missiles

- 11.1.3. Space Vehicles

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Rod

- 11.2.2. Sheet

- 11.2.3. Plate

- 11.2.4. Tube

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Falcon Aerospace

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 GOULD ALLOYS

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HADCO METAL TRADING

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 LE GUELLEC TUBES ET PROFILES

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 METALWEB

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 MILTECH INTERNATIONAL

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Paris Saint-Denis Aero

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Brookfield Wire

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 CASTLE METALS

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CMK

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 DEVILLE RECTIFICATION

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 DYNAMIC METALS

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 QuesTek Innovations

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 RELIANCE STEEL AND ALUMINUM

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 SAMUEL

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 SON & CO.

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 SANDVIK MATERIALS TECHNOLOGY

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Smith Metal Centres

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Tata Steel

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 PLYMOUTH TUBE

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 BRALCO METALS

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Titanium Industries

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Aerocom Metals

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 ATI

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 BOHLER BLECHE

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.1 Falcon Aerospace

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aerospace Industry Semi-Finished Steel Materials Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Application 2025 & 2033

- Figure 3: North America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Types 2025 & 2033

- Figure 5: North America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Country 2025 & 2033

- Figure 7: North America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Application 2025 & 2033

- Figure 9: South America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Types 2025 & 2033

- Figure 11: South America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Country 2025 & 2033

- Figure 13: South America Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Aerospace Industry Semi-Finished Steel Materials Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aerospace Industry Semi-Finished Steel Materials Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Industry Semi-Finished Steel Materials?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the Aerospace Industry Semi-Finished Steel Materials?

Key companies in the market include Falcon Aerospace, GOULD ALLOYS, HADCO METAL TRADING, LE GUELLEC TUBES ET PROFILES, METALWEB, MILTECH INTERNATIONAL, Paris Saint-Denis Aero, Brookfield Wire, CASTLE METALS, CMK, DEVILLE RECTIFICATION, DYNAMIC METALS, QuesTek Innovations, RELIANCE STEEL AND ALUMINUM, SAMUEL, SON & CO., SANDVIK MATERIALS TECHNOLOGY, Smith Metal Centres, Tata Steel, PLYMOUTH TUBE, BRALCO METALS, Titanium Industries, Aerocom Metals, ATI, BOHLER BLECHE.

3. What are the main segments of the Aerospace Industry Semi-Finished Steel Materials?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2438.3 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Industry Semi-Finished Steel Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Industry Semi-Finished Steel Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Industry Semi-Finished Steel Materials?

To stay informed about further developments, trends, and reports in the Aerospace Industry Semi-Finished Steel Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence