Key Insights

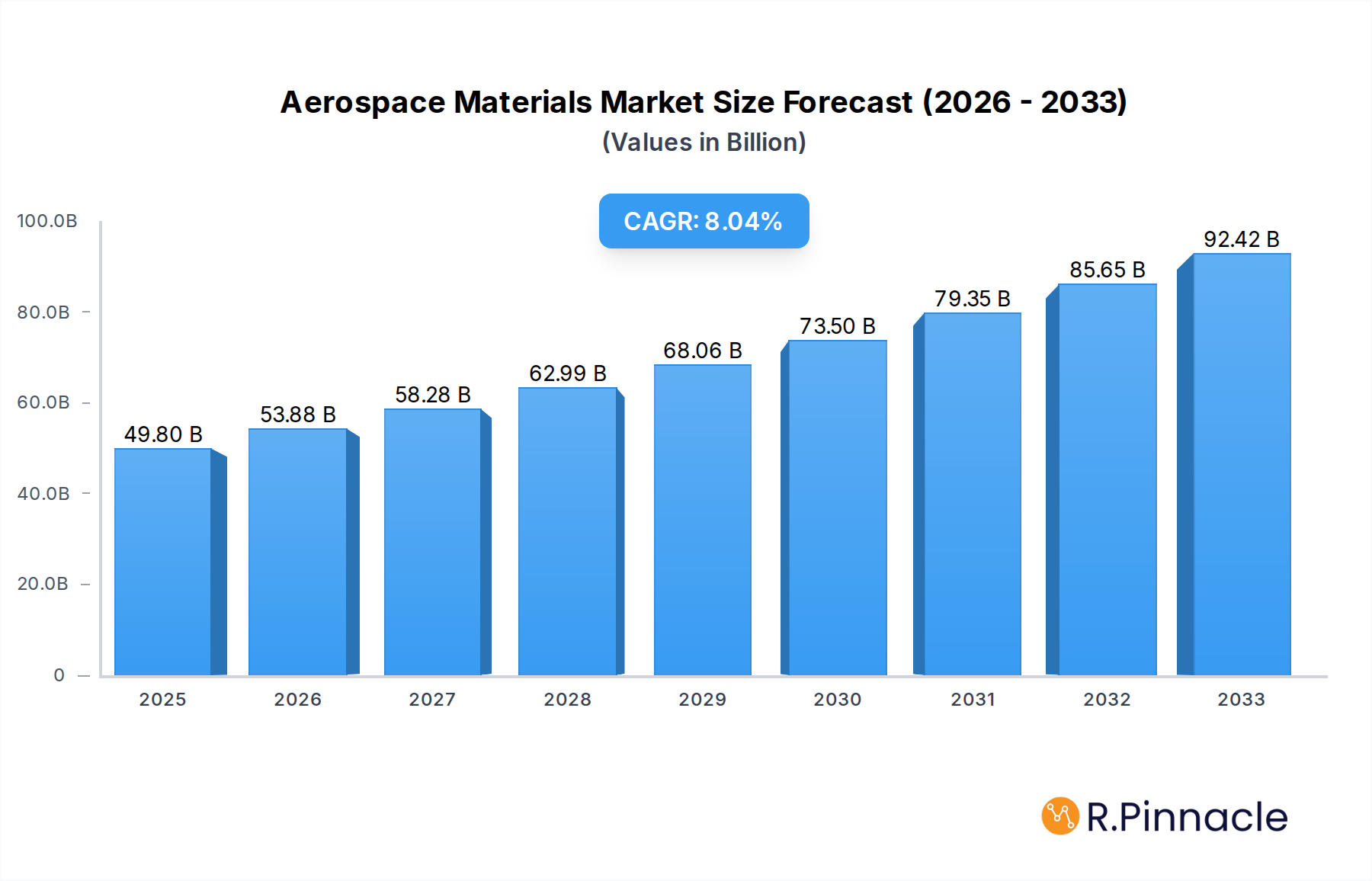

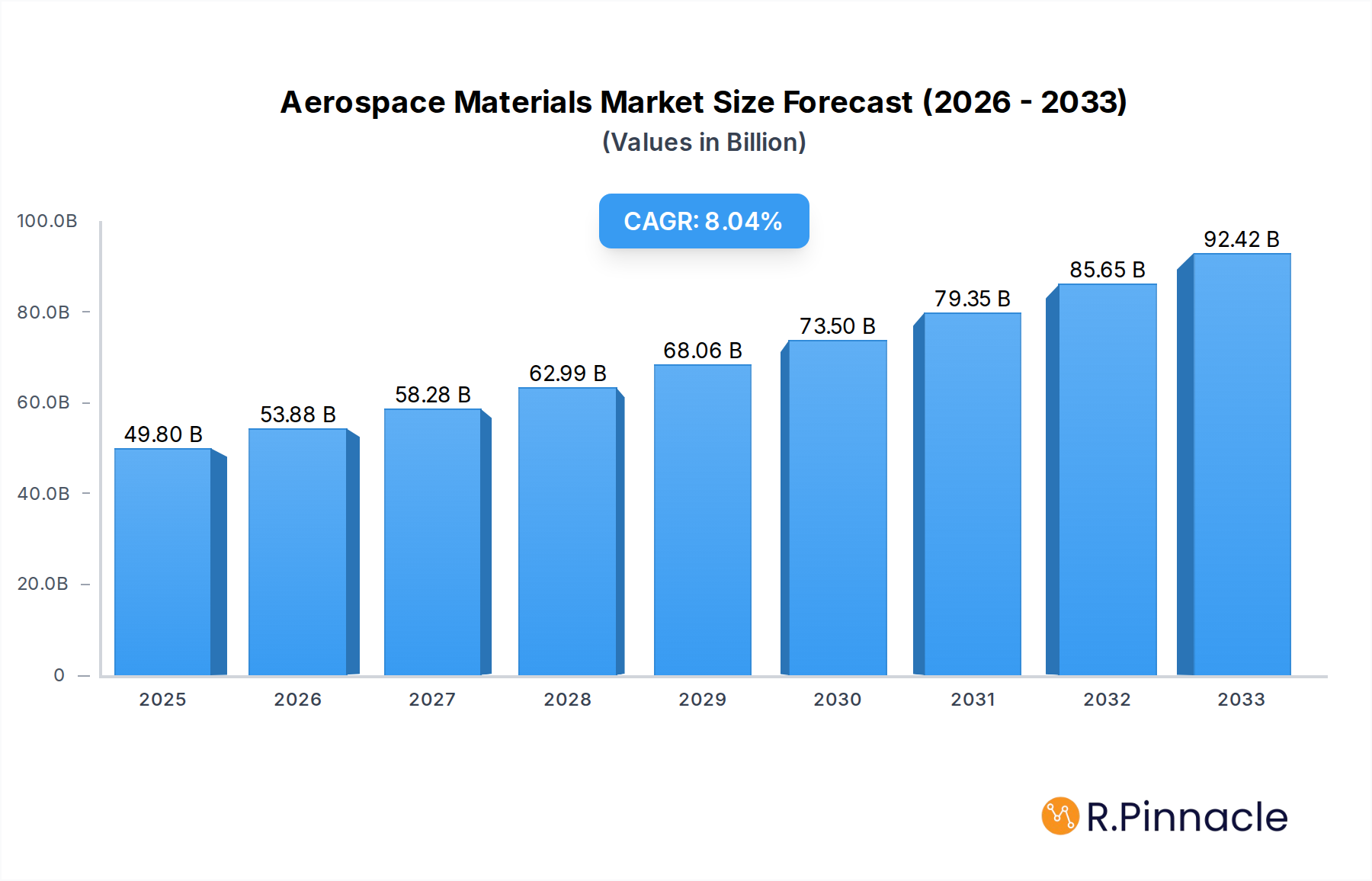

The global Aerospace Materials Market is poised for significant expansion, projected to reach $49.8 billion in 2025 and grow at a robust CAGR of 8.3% throughout the forecast period of 2025-2033. This substantial growth is propelled by a confluence of factors, primarily driven by the escalating demand for lighter, stronger, and more durable materials across commercial aviation, military and defense, and space exploration sectors. Advancements in composite materials, including carbon fiber and glass fiber, are central to this upward trajectory, enabling manufacturers to design more fuel-efficient aircraft and spacecraft with enhanced performance capabilities. The increasing production rates of commercial aircraft, coupled with the modernization of military fleets and ambitious space programs, are creating sustained demand for a wide array of aerospace materials, from high-performance alloys like titanium and aluminum to specialized coatings, adhesives, and sealants. The continuous push for innovation and the development of next-generation materials with superior properties are also significant catalysts for market growth.

Aerospace Materials Market Market Size (In Billion)

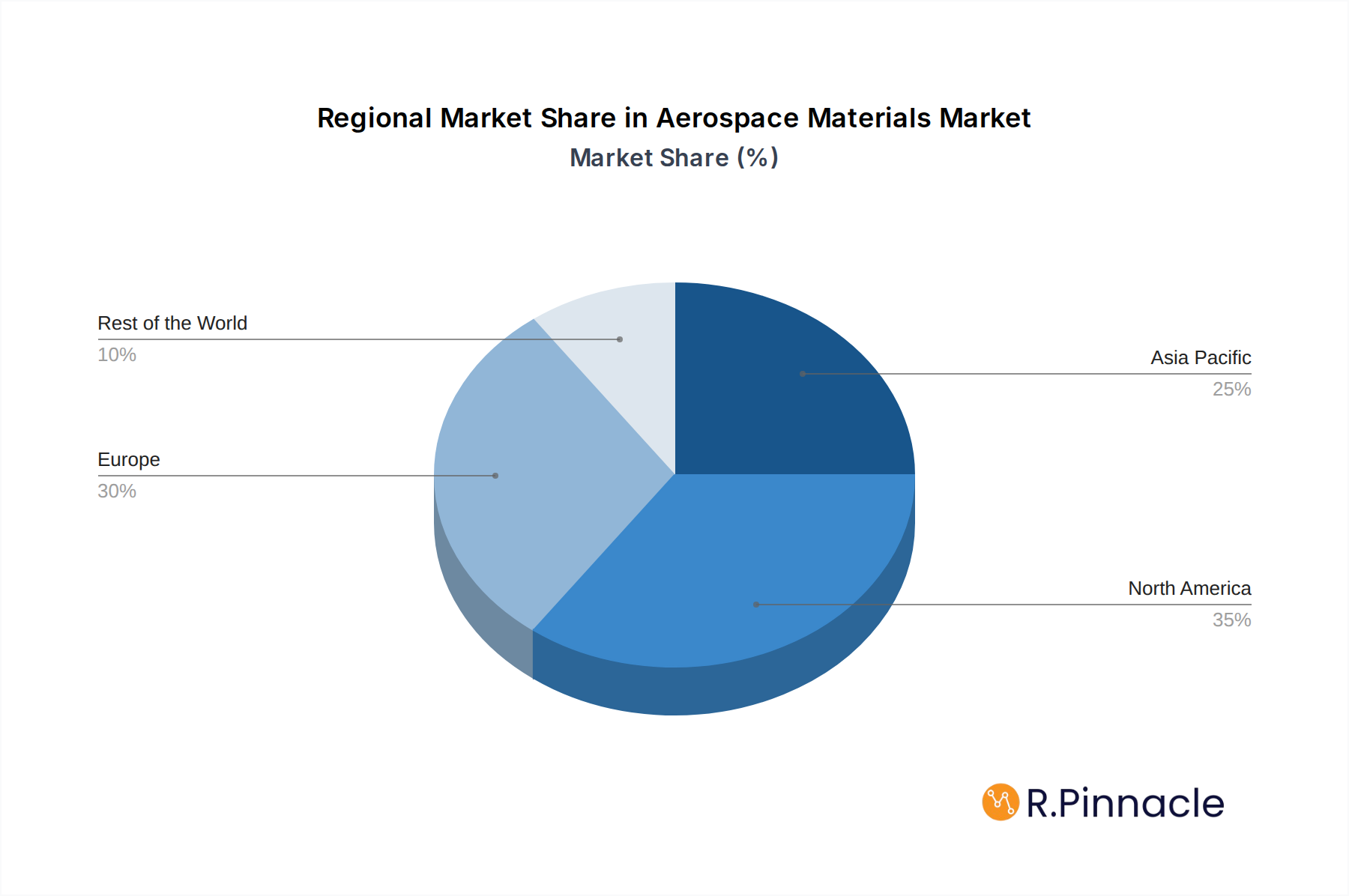

However, the market is not without its challenges. The high cost of advanced materials, coupled with stringent regulatory requirements and complex supply chains, can pose significant restraints. Geopolitical factors and their impact on global trade and manufacturing can also influence material availability and pricing. Nevertheless, the market's inherent growth drivers, including the ongoing need for improved safety, performance, and sustainability in aerospace applications, are expected to outweigh these constraints. The market’s segmentation reveals a strong focus on structural materials, with composites and advanced alloys taking center stage, followed by non-structural components like coatings and adhesives. Geographically, North America and Europe currently dominate the market due to the presence of major aerospace manufacturers and R&D hubs, but the Asia Pacific region is rapidly emerging as a key growth area, driven by increasing investments in domestic aerospace industries and expanding manufacturing capabilities.

Aerospace Materials Market Company Market Share

Unlock critical insights into the dynamic global Aerospace Materials market with this in-depth report. Covering the period from 2019 to 2033, with a base year of 2025, this analysis provides a detailed examination of market structure, drivers, segmentation, and future outlook. Discover the latest innovations, key growth opportunities, and strategic developments shaping the future of aerospace material applications across structural and non-structural components for commercial, military, and space vehicles. This report is essential for stakeholders seeking to navigate the evolving landscape, from raw material suppliers to aircraft manufacturers and investors.

Aerospace Materials Market Market Structure & Innovation Trends

The global Aerospace Materials market exhibits a moderately consolidated structure, characterized by the presence of established global players and specialized regional manufacturers. Innovation is a key driver, with significant R&D investments focused on developing lighter, stronger, and more sustainable materials like advanced composites, high-performance alloys, and novel adhesives. Regulatory frameworks, such as stringent safety and performance standards set by aviation authorities, play a crucial role in shaping product development and market entry. Product substitutes, while evolving, primarily involve the gradual replacement of traditional metals with advanced composites and engineered plastics for weight reduction and improved fuel efficiency. End-user demographics are increasingly diverse, encompassing major aircraft manufacturers, defense contractors, satellite and space exploration companies, and the burgeoning general aviation sector. Mergers and acquisitions (M&A) are strategic tools for market expansion and technology acquisition. Recent M&A activities have focused on consolidating composite manufacturing capabilities and acquiring niche technology providers. For instance, the acquisition of Gurit Holding AG's Aviation and Aerospace business unit by ISOVOLTA AG in April 2022 underscores this trend, expanding ISOVOLTA's offerings in advanced composite materials and manufacturing.

Aerospace Materials Market Market Dynamics & Trends

The Aerospace Materials market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. This expansion is primarily fueled by the sustained demand for new commercial aircraft, driven by increasing global air travel and fleet modernization initiatives. The defense sector's continuous need for advanced materials for next-generation aircraft, unmanned aerial vehicles (UAVs), and spacecraft further bolsters market growth. Technological disruptions are at the forefront, with significant advancements in composite materials such as carbon fiber, glass fiber, and aramid fiber, offering superior strength-to-weight ratios compared to traditional metals. The development of high-temperature alloys, including titanium and superalloys, is critical for engine components and other demanding applications. Consumer preferences, while indirectly influencing the materials market through aircraft design and efficiency demands, are primarily dictated by airline operational costs and passenger experience, both of which are positively impacted by lighter and more fuel-efficient aircraft enabled by advanced materials. Competitive dynamics are characterized by intense innovation, strategic partnerships, and a focus on supply chain resilience. Companies are investing heavily in research and development to create materials that offer enhanced performance, reduced environmental impact, and cost-effectiveness. Market penetration of advanced composites is steadily increasing, replacing traditional aluminum alloys in airframes and other structural components. The trend towards sustainability is also gaining traction, with a growing interest in recyclable and bio-based aerospace materials. The market penetration for advanced composites is expected to reach over 60% in new commercial aircraft production by 2030. The projected market size for Aerospace Materials is expected to reach approximately $55 billion by 2028, with continued upward trajectory.

Dominant Regions & Segments in Aerospace Materials Market

North America currently dominates the Aerospace Materials market, driven by the presence of major aircraft manufacturers like Boeing, a robust defense industry, and significant investment in space exploration. The United States, in particular, leads in research, development, and production of advanced aerospace materials. Key drivers for this dominance include substantial government spending on defense and space programs, favorable economic policies supporting aerospace manufacturing, and a highly developed technological infrastructure.

Leading Segments by Type:

Structural Materials: This segment holds the largest market share.

- Composites:

- Carbon Fiber: The leading composite material, crucial for its exceptional strength-to-weight ratio, widely used in primary and secondary aircraft structures.

- Glass Fiber: Offers good electrical insulation properties and cost-effectiveness, used in secondary structures and interiors.

- Aramid Fiber: Known for its high impact resistance and toughness, utilized in ballistic protection and specialized components.

- Other Composites: Including ceramic matrix composites (CMCs) for high-temperature applications.

- Plastics: Used in interior components, insulation, and some structural elements where weight savings are paramount.

- Alloys:

- Titanium: Essential for high-strength, lightweight applications, particularly in airframes and engine components due to its corrosion resistance and high-temperature performance.

- Aluminum: Remains a significant material for airframes, offering a balance of strength, weight, and cost.

- Steel: Used in high-stress and high-load bearing components.

- Superalloys: Critical for turbine blades and other engine parts operating at extreme temperatures.

- Magnesium: Offers the lowest density among structural metals, used for specific lightweight components.

- Composites:

Non-structural Materials:

- Coatings: Provide protection against corrosion, wear, and extreme environmental conditions.

- Adhesives and Sealants: Crucial for bonding composite structures, sealing gaps, and preventing leaks, with epoxy, polyurethane, and silicone being prominent types.

- Foams: Used for insulation, sound dampening, and lightweight structural cores.

- Seals: Essential for maintaining cabin pressure and preventing fluid leaks.

Leading Segments by Aircraft Type:

- General and Commercial: This segment is the largest contributor to market revenue due to the high volume of aircraft production and fleet maintenance requirements. The demand for fuel-efficient and sustainable aircraft drives innovation in this area.

- Military and Defense: A significant and growing segment, fueled by the need for advanced materials in fighter jets, transport aircraft, helicopters, and unmanned aerial vehicles (UAVs).

- Space Vehicles: A niche but rapidly expanding segment, demanding materials that can withstand extreme temperatures, radiation, and vacuum conditions for satellites, rockets, and spacecraft.

Aerospace Materials Market Product Innovations

Recent product innovations in the Aerospace Materials market focus on enhancing performance, reducing weight, and improving sustainability. Advancements in composite technologies, such as the development of advanced carbon fiber prepregs for critical wing structures, as demonstrated by Hexcel's partnership with Dassault for the Falcon 10X program, are crucial. The integration of functional properties into materials, like advanced next-generation aerospace materials with enhanced capabilities, is a key trend, exemplified by Toray Composite Materials America's partnership with SpecialityMaterials. Furthermore, the development of high-temperature resistant materials and advanced coatings is enabling more efficient and durable aircraft designs. These innovations provide a competitive advantage by meeting the stringent demands for lighter, stronger, and more resilient aerospace components.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Aerospace Materials market segmented by Type and Aircraft Type. The Type segmentation includes Structural materials like Composites (Glass Fiber, Carbon Fiber, Aramid Fiber, Other Composites), Plastics, and Alloys (Titanium, Aluminium, Steel, Superalloys, Magnesium, Other Alloys). Non-structural materials comprise Coatings, Adhesives and Sealants (Epoxy, Polyurethane, Silicone, Other Adhesives and Sealants), Foams (Polyethylene, Other Foams), and Seals. The Aircraft Type segmentation covers General and Commercial, Military and Defense, and Space Vehicles. Growth projections are driven by increased air travel, defense spending, and space exploration initiatives. Market sizes are estimated to reach billions of dollars for each major segment. Competitive dynamics within these segments are intense, with companies focusing on specialized material development and supply chain integration.

Key Drivers of Aerospace Materials Market Growth

Several key drivers are propelling the growth of the Aerospace Materials market. Technological advancements in composite materials, such as carbon fiber and advanced alloys, are paramount, enabling lighter and more fuel-efficient aircraft. Increasing global air travel and the subsequent demand for new commercial aircraft and fleet modernization directly fuels the need for these materials. Government investments in defense and space exploration projects, particularly in emerging economies and established aerospace hubs, create significant demand for high-performance materials. Furthermore, stringent environmental regulations are pushing manufacturers to adopt lighter and more sustainable materials to reduce carbon emissions. The forecast for the market indicates a substantial growth trajectory, driven by these multifaceted factors.

Challenges in the Aerospace Materials Market Sector

Despite robust growth, the Aerospace Materials market faces several challenges. High research and development costs associated with novel material innovation can be a significant barrier. Stringent regulatory hurdles and lengthy certification processes for new materials can delay market entry and increase development timelines. Supply chain volatility and raw material price fluctuations, particularly for rare earth elements and specialized alloys, can impact production costs and availability. The need for specialized manufacturing processes and skilled labor for advanced materials adds another layer of complexity. Furthermore, the competitive pressure from established material providers and the emergence of new players necessitates continuous innovation and cost optimization. These factors collectively shape the competitive landscape and influence market dynamics. The market is expected to reach approximately $60 billion by 2030, but these challenges could temper the pace of growth if not effectively managed.

Emerging Opportunities in Aerospace Materials Market

Emerging opportunities in the Aerospace Materials market lie in the growing demand for sustainable and recyclable materials, driven by increasing environmental consciousness and regulatory pressures. The expansion of the space tourism sector and the rise of commercial space exploration present new avenues for advanced material applications. The development of smart materials with integrated sensing capabilities for structural health monitoring offers significant potential. Furthermore, additive manufacturing (3D printing) of aerospace components using advanced materials is an evolving opportunity, enabling complex designs and on-demand production. The increasing adoption of electric and hybrid-electric aircraft will also create demand for lightweight and high-performance battery enclosure materials and other specialized components. These emerging trends are poised to redefine the future of aerospace material utilization.

Leading Players in the Aerospace Materials Market Market

- ISOVOLTA AG

- Precision Castparts Corp

- SGL Carbon

- Henkel AG & Co KGaA

- HYOSUNG

- Arkema

- Beacon Adhesives Inc

- The Sherwin-Williams Company

- Jiangsu Hengshen Co Ltd

- Reliance Industries Ltd

- Solvay

- Mitsubishi Chemical Corporation

- Akzo Nobel NV

- Aluminum Corporation of China Limited (Chalco)

- Rogers Corporation

- Evonik Industries AG

- 3M

- PPG Industries Inc

- ATI

- Corporation VSMPO-AVISMA

- BASF SE

- Socomore

- Huntsman International LLC

- Axalta Coating Systems

- Howmet Aerospace

- Toray Industries Inc

- Mankiewicz Gebr & Co

- Greiner AG

- Hexcel Corporation

- Carpenter Technology Corporation

- NIPPON STEEL CORPORATION

- DELO Industrie Klebstoffe GmbH & Co KGaA

- Tata Steel (Corus)

- Acerinox SA (VDM Metals)

- Nanjing Yunhai Special Metal Co Ltd

- Hentzen Coatings Inc

Key Developments in Aerospace Materials Market Industry

- October 2022: Toray Composite Materials America partnered with SpecialityMaterials, a boron fiber manufacturer, to develop advanced next-generation aerospace materials with functional properties, strengthening Toray's position in the aerospace materials market.

- July 2022: Hexcel announced its partnership with Dassault to supply carbon fiber prepreg for the Falcon 10X program, incorporating high-performance advanced carbon fiber composites in manufacturing its aircraft wings.

- April 2022: ISOVOLTA AG acquired the Aviation and Aerospace business unit from Gurit Holding AG, enabling the company to expand its business to produce advanced composite materials, composite manufacturing equipment, and core kitting services for the aerospace industry.

Future Outlook for Aerospace Materials Market Market

The future outlook for the Aerospace Materials market is exceptionally strong, driven by sustained demand for air travel, escalating defense modernization, and the burgeoning space economy. The market is poised for continued significant growth, with innovations in lightweight composites, high-temperature alloys, and sustainable materials taking center stage. Strategic partnerships and acquisitions will remain crucial for companies to expand their technological capabilities and market reach. The increasing focus on fuel efficiency and reduced environmental impact will accelerate the adoption of advanced materials in both commercial and military aviation. Furthermore, the rapid advancements in additive manufacturing and the development of smart materials will open up new frontiers for material application and performance optimization. The market is projected to witness consistent expansion, with an estimated valuation exceeding $70 billion by 2033, presenting lucrative opportunities for stakeholders committed to innovation and sustainable growth.

Aerospace Materials Market Segmentation

-

1. Type

-

1.1. Structural

-

1.1.1. Composites

- 1.1.1.1. Glass Fiber

- 1.1.1.2. Carbon Fiber

- 1.1.1.3. Aramid Fiber

- 1.1.1.4. Other Composites

- 1.1.2. Plastics

-

1.1.3. Alloys

- 1.1.3.1. Titanium

- 1.1.3.2. Aluminium

- 1.1.3.3. Steel

- 1.1.3.4. Super

- 1.1.3.5. Magnesium

- 1.1.3.6. Other Alloys

-

1.1.1. Composites

-

1.2. Non-structural

- 1.2.1. Coatings

-

1.2.2. Adhesives and Sealants

- 1.2.2.1. Epoxy

- 1.2.2.2. Polyurethane

- 1.2.2.3. Silicone

- 1.2.2.4. Other Adhesives and Sealants

-

1.2.3. Foams

- 1.2.3.1. Polyethylene

- 1.2.3.2. Other Foams

- 1.2.4. Seals

-

1.1. Structural

-

2. Aircraft Type

- 2.1. General and Commercial

- 2.2. Military and Defense

- 2.3. Space Vehicles

Aerospace Materials Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Aerospace Materials Market Regional Market Share

Geographic Coverage of Aerospace Materials Market

Aerospace Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Structural

- 5.1.1.1. Composites

- 5.1.1.1.1. Glass Fiber

- 5.1.1.1.2. Carbon Fiber

- 5.1.1.1.3. Aramid Fiber

- 5.1.1.1.4. Other Composites

- 5.1.1.2. Plastics

- 5.1.1.3. Alloys

- 5.1.1.3.1. Titanium

- 5.1.1.3.2. Aluminium

- 5.1.1.3.3. Steel

- 5.1.1.3.4. Super

- 5.1.1.3.5. Magnesium

- 5.1.1.3.6. Other Alloys

- 5.1.1.1. Composites

- 5.1.2. Non-structural

- 5.1.2.1. Coatings

- 5.1.2.2. Adhesives and Sealants

- 5.1.2.2.1. Epoxy

- 5.1.2.2.2. Polyurethane

- 5.1.2.2.3. Silicone

- 5.1.2.2.4. Other Adhesives and Sealants

- 5.1.2.3. Foams

- 5.1.2.3.1. Polyethylene

- 5.1.2.3.2. Other Foams

- 5.1.2.4. Seals

- 5.1.1. Structural

- 5.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.2.1. General and Commercial

- 5.2.2. Military and Defense

- 5.2.3. Space Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Aerospace Materials Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Structural

- 6.1.1.1. Composites

- 6.1.1.1.1. Glass Fiber

- 6.1.1.1.2. Carbon Fiber

- 6.1.1.1.3. Aramid Fiber

- 6.1.1.1.4. Other Composites

- 6.1.1.2. Plastics

- 6.1.1.3. Alloys

- 6.1.1.3.1. Titanium

- 6.1.1.3.2. Aluminium

- 6.1.1.3.3. Steel

- 6.1.1.3.4. Super

- 6.1.1.3.5. Magnesium

- 6.1.1.3.6. Other Alloys

- 6.1.1.1. Composites

- 6.1.2. Non-structural

- 6.1.2.1. Coatings

- 6.1.2.2. Adhesives and Sealants

- 6.1.2.2.1. Epoxy

- 6.1.2.2.2. Polyurethane

- 6.1.2.2.3. Silicone

- 6.1.2.2.4. Other Adhesives and Sealants

- 6.1.2.3. Foams

- 6.1.2.3.1. Polyethylene

- 6.1.2.3.2. Other Foams

- 6.1.2.4. Seals

- 6.1.1. Structural

- 6.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.2.1. General and Commercial

- 6.2.2. Military and Defense

- 6.2.3. Space Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Structural

- 7.1.1.1. Composites

- 7.1.1.1.1. Glass Fiber

- 7.1.1.1.2. Carbon Fiber

- 7.1.1.1.3. Aramid Fiber

- 7.1.1.1.4. Other Composites

- 7.1.1.2. Plastics

- 7.1.1.3. Alloys

- 7.1.1.3.1. Titanium

- 7.1.1.3.2. Aluminium

- 7.1.1.3.3. Steel

- 7.1.1.3.4. Super

- 7.1.1.3.5. Magnesium

- 7.1.1.3.6. Other Alloys

- 7.1.1.1. Composites

- 7.1.2. Non-structural

- 7.1.2.1. Coatings

- 7.1.2.2. Adhesives and Sealants

- 7.1.2.2.1. Epoxy

- 7.1.2.2.2. Polyurethane

- 7.1.2.2.3. Silicone

- 7.1.2.2.4. Other Adhesives and Sealants

- 7.1.2.3. Foams

- 7.1.2.3.1. Polyethylene

- 7.1.2.3.2. Other Foams

- 7.1.2.4. Seals

- 7.1.1. Structural

- 7.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.2.1. General and Commercial

- 7.2.2. Military and Defense

- 7.2.3. Space Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Structural

- 8.1.1.1. Composites

- 8.1.1.1.1. Glass Fiber

- 8.1.1.1.2. Carbon Fiber

- 8.1.1.1.3. Aramid Fiber

- 8.1.1.1.4. Other Composites

- 8.1.1.2. Plastics

- 8.1.1.3. Alloys

- 8.1.1.3.1. Titanium

- 8.1.1.3.2. Aluminium

- 8.1.1.3.3. Steel

- 8.1.1.3.4. Super

- 8.1.1.3.5. Magnesium

- 8.1.1.3.6. Other Alloys

- 8.1.1.1. Composites

- 8.1.2. Non-structural

- 8.1.2.1. Coatings

- 8.1.2.2. Adhesives and Sealants

- 8.1.2.2.1. Epoxy

- 8.1.2.2.2. Polyurethane

- 8.1.2.2.3. Silicone

- 8.1.2.2.4. Other Adhesives and Sealants

- 8.1.2.3. Foams

- 8.1.2.3.1. Polyethylene

- 8.1.2.3.2. Other Foams

- 8.1.2.4. Seals

- 8.1.1. Structural

- 8.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.2.1. General and Commercial

- 8.2.2. Military and Defense

- 8.2.3. Space Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Structural

- 9.1.1.1. Composites

- 9.1.1.1.1. Glass Fiber

- 9.1.1.1.2. Carbon Fiber

- 9.1.1.1.3. Aramid Fiber

- 9.1.1.1.4. Other Composites

- 9.1.1.2. Plastics

- 9.1.1.3. Alloys

- 9.1.1.3.1. Titanium

- 9.1.1.3.2. Aluminium

- 9.1.1.3.3. Steel

- 9.1.1.3.4. Super

- 9.1.1.3.5. Magnesium

- 9.1.1.3.6. Other Alloys

- 9.1.1.1. Composites

- 9.1.2. Non-structural

- 9.1.2.1. Coatings

- 9.1.2.2. Adhesives and Sealants

- 9.1.2.2.1. Epoxy

- 9.1.2.2.2. Polyurethane

- 9.1.2.2.3. Silicone

- 9.1.2.2.4. Other Adhesives and Sealants

- 9.1.2.3. Foams

- 9.1.2.3.1. Polyethylene

- 9.1.2.3.2. Other Foams

- 9.1.2.4. Seals

- 9.1.1. Structural

- 9.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.2.1. General and Commercial

- 9.2.2. Military and Defense

- 9.2.3. Space Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Structural

- 10.1.1.1. Composites

- 10.1.1.1.1. Glass Fiber

- 10.1.1.1.2. Carbon Fiber

- 10.1.1.1.3. Aramid Fiber

- 10.1.1.1.4. Other Composites

- 10.1.1.2. Plastics

- 10.1.1.3. Alloys

- 10.1.1.3.1. Titanium

- 10.1.1.3.2. Aluminium

- 10.1.1.3.3. Steel

- 10.1.1.3.4. Super

- 10.1.1.3.5. Magnesium

- 10.1.1.3.6. Other Alloys

- 10.1.1.1. Composites

- 10.1.2. Non-structural

- 10.1.2.1. Coatings

- 10.1.2.2. Adhesives and Sealants

- 10.1.2.2.1. Epoxy

- 10.1.2.2.2. Polyurethane

- 10.1.2.2.3. Silicone

- 10.1.2.2.4. Other Adhesives and Sealants

- 10.1.2.3. Foams

- 10.1.2.3.1. Polyethylene

- 10.1.2.3.2. Other Foams

- 10.1.2.4. Seals

- 10.1.1. Structural

- 10.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.2.1. General and Commercial

- 10.2.2. Military and Defense

- 10.2.3. Space Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 ISOVOLTA AG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Precision Castparts Corp

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 SGL Carbon

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Henkel AG & Co KGaA

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 HYOSUNG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Arkema

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Beacon Adhesives Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 The Sherwin-Williams Company

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Jiangsu Hengshen Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Reliance Industries Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Solvay

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Mitsubishi Chemical Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Akzo Nobel NV

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Aluminum Corporation of China Limited (Chalco)

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 Rogers Corporation

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.16 Evonik Industries AG

- 11.1.16.1. Company Overview

- 11.1.16.2. Products

- 11.1.16.3. Company Financials

- 11.1.16.4. SWOT Analysis

- 11.1.17 3M

- 11.1.17.1. Company Overview

- 11.1.17.2. Products

- 11.1.17.3. Company Financials

- 11.1.17.4. SWOT Analysis

- 11.1.18 PPG Industries Inc

- 11.1.18.1. Company Overview

- 11.1.18.2. Products

- 11.1.18.3. Company Financials

- 11.1.18.4. SWOT Analysis

- 11.1.19 ATI

- 11.1.19.1. Company Overview

- 11.1.19.2. Products

- 11.1.19.3. Company Financials

- 11.1.19.4. SWOT Analysis

- 11.1.20 Corporation VSMPO-AVISMA

- 11.1.20.1. Company Overview

- 11.1.20.2. Products

- 11.1.20.3. Company Financials

- 11.1.20.4. SWOT Analysis

- 11.1.21 BASF SE

- 11.1.21.1. Company Overview

- 11.1.21.2. Products

- 11.1.21.3. Company Financials

- 11.1.21.4. SWOT Analysis

- 11.1.22 Socomore

- 11.1.22.1. Company Overview

- 11.1.22.2. Products

- 11.1.22.3. Company Financials

- 11.1.22.4. SWOT Analysis

- 11.1.23 Huntsman International LLC

- 11.1.23.1. Company Overview

- 11.1.23.2. Products

- 11.1.23.3. Company Financials

- 11.1.23.4. SWOT Analysis

- 11.1.24 Axalta Coating Systems

- 11.1.24.1. Company Overview

- 11.1.24.2. Products

- 11.1.24.3. Company Financials

- 11.1.24.4. SWOT Analysis

- 11.1.25 Howmet Aerospace

- 11.1.25.1. Company Overview

- 11.1.25.2. Products

- 11.1.25.3. Company Financials

- 11.1.25.4. SWOT Analysis

- 11.1.26 Toray Industries Inc *List Not Exhaustive

- 11.1.26.1. Company Overview

- 11.1.26.2. Products

- 11.1.26.3. Company Financials

- 11.1.26.4. SWOT Analysis

- 11.1.27 Mankiewicz Gebr & Co

- 11.1.27.1. Company Overview

- 11.1.27.2. Products

- 11.1.27.3. Company Financials

- 11.1.27.4. SWOT Analysis

- 11.1.28 Greiner AG

- 11.1.28.1. Company Overview

- 11.1.28.2. Products

- 11.1.28.3. Company Financials

- 11.1.28.4. SWOT Analysis

- 11.1.29 Hexcel Corporation

- 11.1.29.1. Company Overview

- 11.1.29.2. Products

- 11.1.29.3. Company Financials

- 11.1.29.4. SWOT Analysis

- 11.1.30 Carpenter Technology Corporation

- 11.1.30.1. Company Overview

- 11.1.30.2. Products

- 11.1.30.3. Company Financials

- 11.1.30.4. SWOT Analysis

- 11.1.31 NIPPON STEEL CORPORATION

- 11.1.31.1. Company Overview

- 11.1.31.2. Products

- 11.1.31.3. Company Financials

- 11.1.31.4. SWOT Analysis

- 11.1.32 DELO Industrie Klebstoffe GmbH & Co KGaA

- 11.1.32.1. Company Overview

- 11.1.32.2. Products

- 11.1.32.3. Company Financials

- 11.1.32.4. SWOT Analysis

- 11.1.33 Tata Steel (Corus)

- 11.1.33.1. Company Overview

- 11.1.33.2. Products

- 11.1.33.3. Company Financials

- 11.1.33.4. SWOT Analysis

- 11.1.34 Acerinox SA (VDM Metals)

- 11.1.34.1. Company Overview

- 11.1.34.2. Products

- 11.1.34.3. Company Financials

- 11.1.34.4. SWOT Analysis

- 11.1.35 Nanjing Yunhai Special Metal Co Ltd

- 11.1.35.1. Company Overview

- 11.1.35.2. Products

- 11.1.35.3. Company Financials

- 11.1.35.4. SWOT Analysis

- 11.1.36 Hentzen Coatings Inc

- 11.1.36.1. Company Overview

- 11.1.36.2. Products

- 11.1.36.3. Company Financials

- 11.1.36.4. SWOT Analysis

- 11.1.1 ISOVOLTA AG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Aerospace Materials Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Aerospace Materials Market Revenue (billion), by Type 2025 & 2033

- Figure 3: Asia Pacific Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Aerospace Materials Market Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 5: Asia Pacific Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 6: Asia Pacific Aerospace Materials Market Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Aerospace Materials Market Revenue (billion), by Type 2025 & 2033

- Figure 9: North America Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Aerospace Materials Market Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 11: North America Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: North America Aerospace Materials Market Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace Materials Market Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Aerospace Materials Market Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 17: Europe Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 18: Europe Aerospace Materials Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Aerospace Materials Market Revenue (billion), by Type 2025 & 2033

- Figure 21: Rest of the World Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Rest of the World Aerospace Materials Market Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 23: Rest of the World Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 24: Rest of the World Aerospace Materials Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Materials Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Aerospace Materials Market Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 3: Global Aerospace Materials Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace Materials Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Aerospace Materials Market Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 6: Global Aerospace Materials Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Aerospace Materials Market Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Aerospace Materials Market Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 14: Global Aerospace Materials Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Aerospace Materials Market Revenue billion Forecast, by Type 2020 & 2033

- Table 19: Global Aerospace Materials Market Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 20: Global Aerospace Materials Market Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Spain Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Russia Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Materials Market Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global Aerospace Materials Market Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 30: Global Aerospace Materials Market Revenue billion Forecast, by Country 2020 & 2033

- Table 31: South America Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Middle East and Africa Aerospace Materials Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Materials Market?

The projected CAGR is approximately 8.4%.

2. Which companies are prominent players in the Aerospace Materials Market?

Key companies in the market include ISOVOLTA AG, Precision Castparts Corp, SGL Carbon, Henkel AG & Co KGaA, HYOSUNG, Arkema, Beacon Adhesives Inc, The Sherwin-Williams Company, Jiangsu Hengshen Co Ltd, Reliance Industries Ltd, Solvay, Mitsubishi Chemical Corporation, Akzo Nobel NV, Aluminum Corporation of China Limited (Chalco), Rogers Corporation, Evonik Industries AG, 3M, PPG Industries Inc, ATI, Corporation VSMPO-AVISMA, BASF SE, Socomore, Huntsman International LLC, Axalta Coating Systems, Howmet Aerospace, Toray Industries Inc *List Not Exhaustive, Mankiewicz Gebr & Co, Greiner AG, Hexcel Corporation, Carpenter Technology Corporation, NIPPON STEEL CORPORATION, DELO Industrie Klebstoffe GmbH & Co KGaA, Tata Steel (Corus), Acerinox SA (VDM Metals), Nanjing Yunhai Special Metal Co Ltd, Hentzen Coatings Inc.

3. What are the main segments of the Aerospace Materials Market?

The market segments include Type, Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 41.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Use of Composites in Aircraft Manufacturing; Growing Space Industry; Increasing Government Spending on Defense in the United States and European Countries.

6. What are the notable trends driving market growth?

Increasing Demand for General and Commercial Aircraft.

7. Are there any restraints impacting market growth?

High Manufacturing Cost of Carbon Fibers; Declining Usage of Alloys.

8. Can you provide examples of recent developments in the market?

In October 2022, Toray Composite Materials America partnered with SpecialityMaterials, a boron fiber manufacturer, to develop advanced next-generation aerospace materials with functional properties. This move will strengthen Toray's position in the aerospace materials market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Materials Market?

To stay informed about further developments, trends, and reports in the Aerospace Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence