Key Insights

The Asia Pacific luxury goods industry is poised for robust expansion, with a current market size of 141,820 Million USD and a projected Compound Annual Growth Rate (CAGR) of 4.06% through 2033. This growth is fueled by a confluence of factors, including the burgeoning middle and affluent classes in key markets like China and India, a rising demand for premium and personalized experiences, and the increasing influence of digital channels in luxury consumption. The apparel and footwear segments are expected to lead the charge, driven by evolving fashion trends and a strong desire for high-quality, branded products. Similarly, the jewelry and watches segments will benefit from their status as aspirational purchases and investment vehicles. The strategic expansion of online retail channels, coupled with the enduring appeal of exclusive single-branded stores, will shape the distribution landscape, catering to diverse consumer preferences.

Asia Pacific Luxury Goods Industry Market Size (In Billion)

The market's trajectory is further influenced by significant trends such as the growing importance of sustainability and ethical sourcing, which are increasingly influencing purchasing decisions among luxury consumers. Furthermore, the rise of experiential luxury, encompassing travel, dining, and exclusive events, is complementing traditional product purchases. While rapid urbanization and increasing disposable incomes act as key growth drivers, potential restraints include heightened competition, evolving regulatory landscapes in certain regions, and the impact of global economic uncertainties. Nevertheless, the dominance of China as a major market, alongside the emerging potential of India and other Southeast Asian nations, underscores the Asia Pacific's pivotal role in shaping the future of the global luxury goods sector. Companies like LVMH, Hermes, and Kering are strategically positioned to capitalize on these dynamics, with a focus on innovation, digital transformation, and cultivating strong brand loyalty.

Asia Pacific Luxury Goods Industry Company Market Share

Unlocking the Asia Pacific Luxury Goods Industry: Market Insights & Growth Strategies (2019–2033)

This comprehensive report delves into the dynamic and rapidly evolving Asia Pacific Luxury Goods Industry. Covering a study period from 2019–2033, with 2025 as the base and estimated year, and a forecast period of 2025–2033, this analysis provides deep insights into market structure, dynamics, and future potential. We examine key players, product innovations, dominant regions, and strategic opportunities to guide industry professionals and investors in navigating this lucrative market.

Asia Pacific Luxury Goods Industry Market Structure & Innovation Trends

The Asia Pacific luxury goods market exhibits a moderately concentrated structure, with a few major conglomerates like LVMH Moet Hennessy, Compagnie Financiere Richemont SA, and Kering SA holding significant market share, estimated to be upwards of 65 Million in total market capitalization. Innovation is primarily driven by brand heritage, craftsmanship, and increasingly, digital integration and sustainability initiatives. Regulatory frameworks vary across countries, impacting import duties and consumer protection, with an estimated 2% influence on market entry. Product substitutes, while present in premium segments, rarely offer the same aspirational value or perceived quality as established luxury brands. End-user demographics are shifting towards a younger, affluent, and digitally-savvy consumer base, with a projected 30% increase in Gen Z luxury spending by 2028. Mergers and acquisitions (M&A) activity, while not as frenzied as in other sectors, remains strategic, with deal values for niche luxury acquisitions often exceeding 10 Million.

- Market Concentration: Dominated by global luxury powerhouses, with a focus on brand equity.

- Innovation Drivers: Digital transformation, sustainable practices, unique experiences, and hyper-personalization.

- Regulatory Frameworks: Impacting pricing, distribution, and brand communication across diverse national landscapes.

- Product Substitutes: Limited impact due to strong brand loyalty and intangible brand value.

- End-User Demographics: Growing influence of younger consumers and the rise of HENRYs (High Earners, Not Rich Yet).

- M&A Activities: Strategic acquisitions of emerging luxury brands and technology providers.

Asia Pacific Luxury Goods Industry Market Dynamics & Trends

The Asia Pacific luxury goods market is experiencing robust growth, fueled by several key dynamics and evolving trends. The Compound Annual Growth Rate (CAGR) for the forecast period is projected to be a healthy 7.5%, indicating sustained expansion. A primary growth driver is the burgeoning affluent class in emerging economies, particularly in Southeast Asia and India, who are increasingly seeking to express their status and success through luxury purchases. China continues to be the largest contributor, accounting for an estimated 45% of the regional market share, driven by a strong domestic consumption base and a growing appetite for high-end fashion, accessories, and experiences.

Technological disruptions are playing a transformative role. The increasing adoption of e-commerce and omnichannel strategies by luxury brands is enhancing accessibility and customer engagement. Virtual try-ons, personalized online consultations, and seamless integration between online and offline retail channels are becoming standard. The metaverse and NFTs are also emerging as new frontiers, with select brands experimenting with digital collectibles and virtual storefronts, opening up new revenue streams and engagement models.

Consumer preferences are undergoing a significant shift. There is a growing demand for sustainable and ethically produced luxury goods. Consumers are increasingly conscious of the environmental and social impact of their purchases, leading brands to focus on transparent sourcing, ethical manufacturing, and circular economy initiatives. Furthermore, the desire for unique and personalized experiences is paramount. This includes bespoke product customization, exclusive events, and highly tailored customer service. Authenticity and heritage also remain crucial, with consumers valuing brands that can authentically connect with their values and aspirations.

Competitive dynamics are intensifying. While established global players maintain their dominance, there is a rise of agile, digitally native luxury brands and a growing influence of local designers and artisans who tap into regional aesthetics and cultural nuances. Strategic partnerships, collaborations with influencers, and a focus on building strong online communities are key to capturing market share. The report estimates a market penetration of luxury goods reaching 20% within the affluent demographic by 2028.

Dominant Regions & Segments in Asia Pacific Luxury Goods Industry

The Asia Pacific luxury goods industry is characterized by regional and segmental dominance, driven by distinct economic, cultural, and demographic factors. China stands out as the undisputed leader, commanding an estimated 45% of the regional market share. This dominance is attributed to its massive, rapidly growing affluent population, increasing disposable incomes, and a strong consumer desire for premium and aspirational products. Government policies promoting domestic consumption and the development of sophisticated retail infrastructure further bolster its position.

Within product categories, Clothing and Apparel and Bags are consistently the top-performing segments, each accounting for approximately 25% of the total market value. This reflects the strong fashion-conscious culture prevalent across many Asian countries and the enduring appeal of iconic luxury handbags as status symbols.

- Key Drivers for China's Dominance:

- Large and growing affluent consumer base.

- High disposable incomes and strong consumption power.

- Government support for luxury consumption and retail development.

- Influence of social media and KOLs (Key Opinion Leaders).

The Distribution Channel landscape is evolving, with Single-branded Stores still holding a significant share due to the brand control and immersive customer experience they offer. However, Online Stores are rapidly gaining traction, projected to capture over 30% of the market share by 2028, driven by the increasing adoption of e-commerce and the convenience it offers.

- Dominant Segments Breakdown:

- Type: Clothing and Apparel (25%), Bags (25%), Jewelry (18%), Watches (15%), Footwear (10%), Other Types (7%).

- Distribution Channel: Single-branded Stores (40%), Online Stores (30%), Multi-brand Stores (25%), Other Distribution Channels (5%).

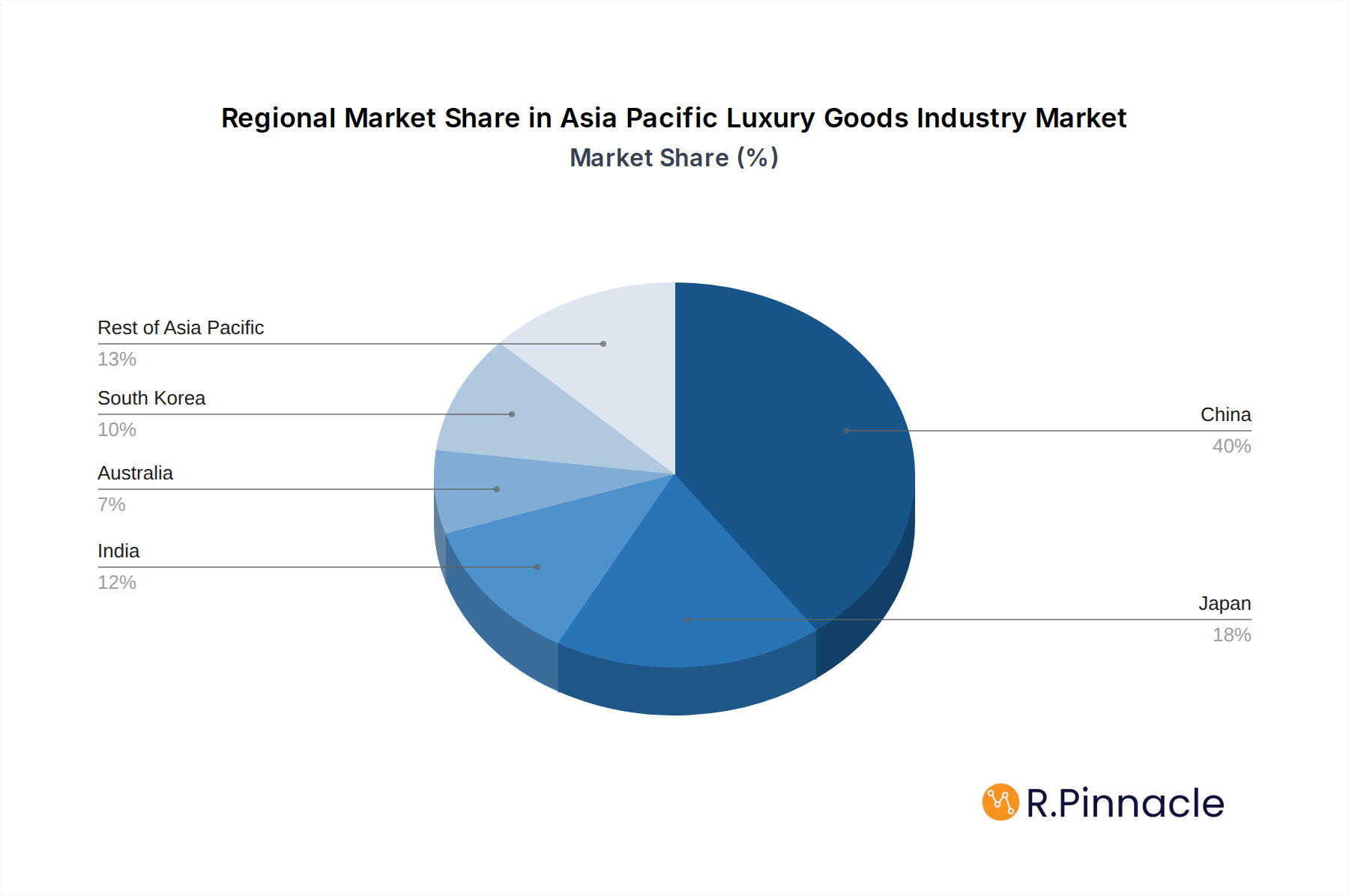

- Geography: China (45%), Japan (15%), South Korea (10%), India (8%), Australia (5%), Rest of Asia-Pacific (17%).

Japan remains a mature yet significant market, characterized by a discerning consumer base that values craftsmanship, quality, and understated elegance. South Korea is a dynamic market with a strong influence of K-fashion and K-beauty trends, driving demand for innovative and trendsetting luxury items. The Rest of Asia-Pacific, encompassing emerging economies like Vietnam, Thailand, and Indonesia, presents substantial growth potential due to rising disposable incomes and an expanding middle class.

Asia Pacific Luxury Goods Industry Product Innovations

Product innovation in the Asia Pacific luxury goods industry is characterized by a blend of heritage craftsmanship and cutting-edge technology. Brands are increasingly focusing on incorporating sustainable materials and ethical sourcing practices, appealing to environmentally conscious consumers. For instance, the use of recycled gold in jewelry and organic fabrics in apparel is gaining prominence. Furthermore, personalization and customization are key competitive advantages. Technology enables intricate monogramming, bespoke design services, and made-to-measure options, creating unique products tailored to individual preferences. The integration of smart technology into traditional luxury items, such as smartwatches with enhanced functionalities and luxury apparel with embedded tech, is also a growing trend. These innovations not only enhance product appeal but also create distinct market positioning and a competitive edge.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Asia Pacific Luxury Goods Industry, segmented across key categories. The Type segmentation includes Clothing and Apparel, Footwear, Bags, Jewelry, Watches, and Other Types, each analyzed for market size and growth projections. The Distribution Channel segmentation covers Single-branded Stores, Multi-brand Stores, Online Stores, and Other Distribution Channels, offering insights into consumer purchasing habits and brand strategies. Geographically, the report meticulously examines China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific, detailing their unique market dynamics, growth potential, and competitive landscapes. Growth projections for each segment are estimated with a CAGR of approximately 7% over the forecast period, with significant variations based on regional economic development and consumer trends.

Key Drivers of Asia Pacific Luxury Goods Industry Growth

The growth of the Asia Pacific luxury goods industry is propelled by several key factors. The escalating disposable income among the growing affluent and ultra-high-net-worth individuals across the region is a primary driver. Technological advancements, particularly the widespread adoption of e-commerce and digital marketing, have democratized access to luxury goods, expanding the consumer base beyond traditional brick-and-mortar stores. Furthermore, increasing urbanization and exposure to global trends through social media and travel have heightened consumer aspirations. Government initiatives aimed at boosting domestic consumption and supporting the luxury retail sector in key markets also contribute significantly.

Challenges in the Asia Pacific Luxury Goods Industry Sector

Despite its robust growth, the Asia Pacific luxury goods industry faces several challenges. Intense competition from both established global brands and emerging local players necessitates continuous innovation and strong brand differentiation. Navigating diverse regulatory landscapes, including varying import duties, taxes, and intellectual property protection laws across different countries, presents operational complexities. Supply chain disruptions, exacerbated by geopolitical events and logistical challenges, can impact product availability and lead times. Additionally, the increasing demand for sustainability and ethical sourcing requires significant investment and operational overhauls from brands. Counterfeiting remains a persistent threat, eroding brand value and consumer trust, with an estimated 10 Million lost annually due to the sale of counterfeit luxury goods.

Emerging Opportunities in Asia Pacific Luxury Goods Industry

Emerging opportunities in the Asia Pacific luxury goods industry lie in tapping into the burgeoning Gen Z and millennial consumer base, who prioritize experiences, personalization, and digital engagement. The growing demand for sustainable and ethically produced luxury items presents a significant avenue for brands that can demonstrate genuine commitment to these principles. Expansion into less saturated, high-growth emerging markets within Southeast Asia and India offers substantial untapped potential. The continued development of e-commerce and the exploration of new digital frontiers like the metaverse and NFTs provide innovative channels for customer engagement and direct-to-consumer sales, with an estimated 15 Million projected revenue increase from digital channels by 2027.

Leading Players in the Asia Pacific Luxury Goods Industry Market

- LVMH Moet Hennessy

- Hermes International SA

- Kering SA

- Compagnie Financiere Richemont SA

- The Estee Lauder Company

- Prada SpA

- L'Oreal SA

- Chanel SA

- The Swatch Group

- Rolex SA

Key Developments in Asia Pacific Luxury Goods Industry Industry

- June 2022: Estée Lauder's Luxury debuted its Fragrance Collection in Southeast Asia. This marked Southeast Asia's first travel retail launch of the Estée Lauder Luxury Fragrance Collection, partnering with King Power Duty-Free in Thailand. This initiative significantly expanded Estée Lauder's regional travel retail footprint.

- December 2021: Luxury Swiss watch brand Roger Dubuis launched its first standalone store in Australia, located in Sydney. The brand featured 28 exclusive timepieces for the Sydney store, indicating a strategic focus on the Australian market and its affluent clientele.

- May 2021: The Los Angeles-based Aaron Kirman Group launched a new Asia-Pacific division. This move was aimed at better tapping into the growing market of luxury buyers from Asia, recognizing the increasing demand for high-end real estate and lifestyle products from this demographic.

Future Outlook for Asia Pacific Luxury Goods Industry Market

The future outlook for the Asia Pacific luxury goods industry remains exceptionally bright, with sustained growth anticipated throughout the forecast period. Key growth accelerators include the continued economic development of emerging markets, leading to an expanding base of affluent consumers eager to embrace luxury. The increasing digital native population will drive further innovation in e-commerce, personalized digital experiences, and the exploration of virtual worlds. Brands that successfully integrate sustainability into their core operations and product offerings will gain a significant competitive advantage. Strategic expansion into underserved regions and a focus on catering to evolving consumer preferences for authenticity, craftsmanship, and unique experiences will be crucial for long-term success. The industry is projected to see an overall market value exceeding 150 Million by 2033, with a CAGR of approximately 7.5%.

Asia Pacific Luxury Goods Industry Segmentation

-

1. Type

- 1.1. Clothing and Apparel

- 1.2. Footwear

- 1.3. Bags

- 1.4. Jewelry

- 1.5. Watches

- 1.6. Other Types

-

2. Distribution Channel

- 2.1. Single-branded Stores

- 2.2. Multi-brand Stores

- 2.3. Online Stores

- 2.4. Other Distribution Channels

-

3. Geography

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia-Pacific

Asia Pacific Luxury Goods Industry Segmentation By Geography

- 1. China

- 2. Japan

- 3. India

- 4. Australia

- 5. South Korea

- 6. Rest of Asia Pacific

Asia Pacific Luxury Goods Industry Regional Market Share

Geographic Coverage of Asia Pacific Luxury Goods Industry

Asia Pacific Luxury Goods Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Clothing and Apparel

- 5.1.2. Footwear

- 5.1.3. Bags

- 5.1.4. Jewelry

- 5.1.5. Watches

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Single-branded Stores

- 5.2.2. Multi-brand Stores

- 5.2.3. Online Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. Japan

- 5.3.3. India

- 5.3.4. Australia

- 5.3.5. South Korea

- 5.3.6. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. Japan

- 5.4.3. India

- 5.4.4. Australia

- 5.4.5. South Korea

- 5.4.6. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Clothing and Apparel

- 6.1.2. Footwear

- 6.1.3. Bags

- 6.1.4. Jewelry

- 6.1.5. Watches

- 6.1.6. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Single-branded Stores

- 6.2.2. Multi-brand Stores

- 6.2.3. Online Stores

- 6.2.4. Other Distribution Channels

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. Japan

- 6.3.3. India

- 6.3.4. Australia

- 6.3.5. South Korea

- 6.3.6. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. China Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Clothing and Apparel

- 7.1.2. Footwear

- 7.1.3. Bags

- 7.1.4. Jewelry

- 7.1.5. Watches

- 7.1.6. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Single-branded Stores

- 7.2.2. Multi-brand Stores

- 7.2.3. Online Stores

- 7.2.4. Other Distribution Channels

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. Japan

- 7.3.3. India

- 7.3.4. Australia

- 7.3.5. South Korea

- 7.3.6. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Japan Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Clothing and Apparel

- 8.1.2. Footwear

- 8.1.3. Bags

- 8.1.4. Jewelry

- 8.1.5. Watches

- 8.1.6. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Single-branded Stores

- 8.2.2. Multi-brand Stores

- 8.2.3. Online Stores

- 8.2.4. Other Distribution Channels

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. Japan

- 8.3.3. India

- 8.3.4. Australia

- 8.3.5. South Korea

- 8.3.6. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. India Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Clothing and Apparel

- 9.1.2. Footwear

- 9.1.3. Bags

- 9.1.4. Jewelry

- 9.1.5. Watches

- 9.1.6. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Single-branded Stores

- 9.2.2. Multi-brand Stores

- 9.2.3. Online Stores

- 9.2.4. Other Distribution Channels

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. Japan

- 9.3.3. India

- 9.3.4. Australia

- 9.3.5. South Korea

- 9.3.6. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Clothing and Apparel

- 10.1.2. Footwear

- 10.1.3. Bags

- 10.1.4. Jewelry

- 10.1.5. Watches

- 10.1.6. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Single-branded Stores

- 10.2.2. Multi-brand Stores

- 10.2.3. Online Stores

- 10.2.4. Other Distribution Channels

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. Japan

- 10.3.3. India

- 10.3.4. Australia

- 10.3.5. South Korea

- 10.3.6. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South Korea Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Clothing and Apparel

- 11.1.2. Footwear

- 11.1.3. Bags

- 11.1.4. Jewelry

- 11.1.5. Watches

- 11.1.6. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Single-branded Stores

- 11.2.2. Multi-brand Stores

- 11.2.3. Online Stores

- 11.2.4. Other Distribution Channels

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. Japan

- 11.3.3. India

- 11.3.4. Australia

- 11.3.5. South Korea

- 11.3.6. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Asia Pacific Asia Pacific Luxury Goods Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Clothing and Apparel

- 12.1.2. Footwear

- 12.1.3. Bags

- 12.1.4. Jewelry

- 12.1.5. Watches

- 12.1.6. Other Types

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Single-branded Stores

- 12.2.2. Multi-brand Stores

- 12.2.3. Online Stores

- 12.2.4. Other Distribution Channels

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. China

- 12.3.2. Japan

- 12.3.3. India

- 12.3.4. Australia

- 12.3.5. South Korea

- 12.3.6. Rest of Asia-Pacific

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 LVMH Moet Hennessy

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Hermes International SA

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Kering SA

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Compagnie Financiere Richemont SA

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 The Estee Lauder Company

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Prada SpA

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 L'Oreal SA

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Chanel SA

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 The Swatch Group*List Not Exhaustive

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Rolex SA

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 LVMH Moet Hennessy

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Asia Pacific Luxury Goods Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Luxury Goods Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 3: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 5: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 7: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 9: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 11: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 12: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 13: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 15: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 17: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 18: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 19: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 20: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 21: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 23: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 26: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 27: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 28: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 29: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 30: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 31: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 33: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 35: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 36: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 37: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 38: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 39: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 41: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 42: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 43: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 44: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 45: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 46: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 47: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 49: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 50: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 51: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 52: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Distribution Channel 2020 & 2033

- Table 53: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 54: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Geography 2020 & 2033

- Table 55: Asia Pacific Luxury Goods Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Asia Pacific Luxury Goods Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Luxury Goods Industry?

The projected CAGR is approximately 4.06%.

2. Which companies are prominent players in the Asia Pacific Luxury Goods Industry?

Key companies in the market include LVMH Moet Hennessy, Hermes International SA, Kering SA, Compagnie Financiere Richemont SA, The Estee Lauder Company, Prada SpA, L'Oreal SA, Chanel SA, The Swatch Group*List Not Exhaustive, Rolex SA.

3. What are the main segments of the Asia Pacific Luxury Goods Industry?

The market segments include Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 141.82 Million as of 2022.

5. What are some drivers contributing to market growth?

Product Innovations to Drive Demand for Watches; Rising Demand for Premium Fashion Items.

6. What are the notable trends driving market growth?

Rising Trend of Personalization and Customization of Goods.

7. Are there any restraints impacting market growth?

Presence of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

June 2022: Estée Lauder's Luxury debuted its Fragrance Collection in Southeast Asia. This is Southeast Asia's first travel retail launch of the Estée Lauder Luxury Fragrance Collection. Estée Lauder has partnered with King Power Duty-Free [part of the King Power International Group] for the exclusive launch of the Luxury Fragrance Collection in Thailand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Luxury Goods Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Luxury Goods Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Luxury Goods Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Luxury Goods Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence