Key Insights

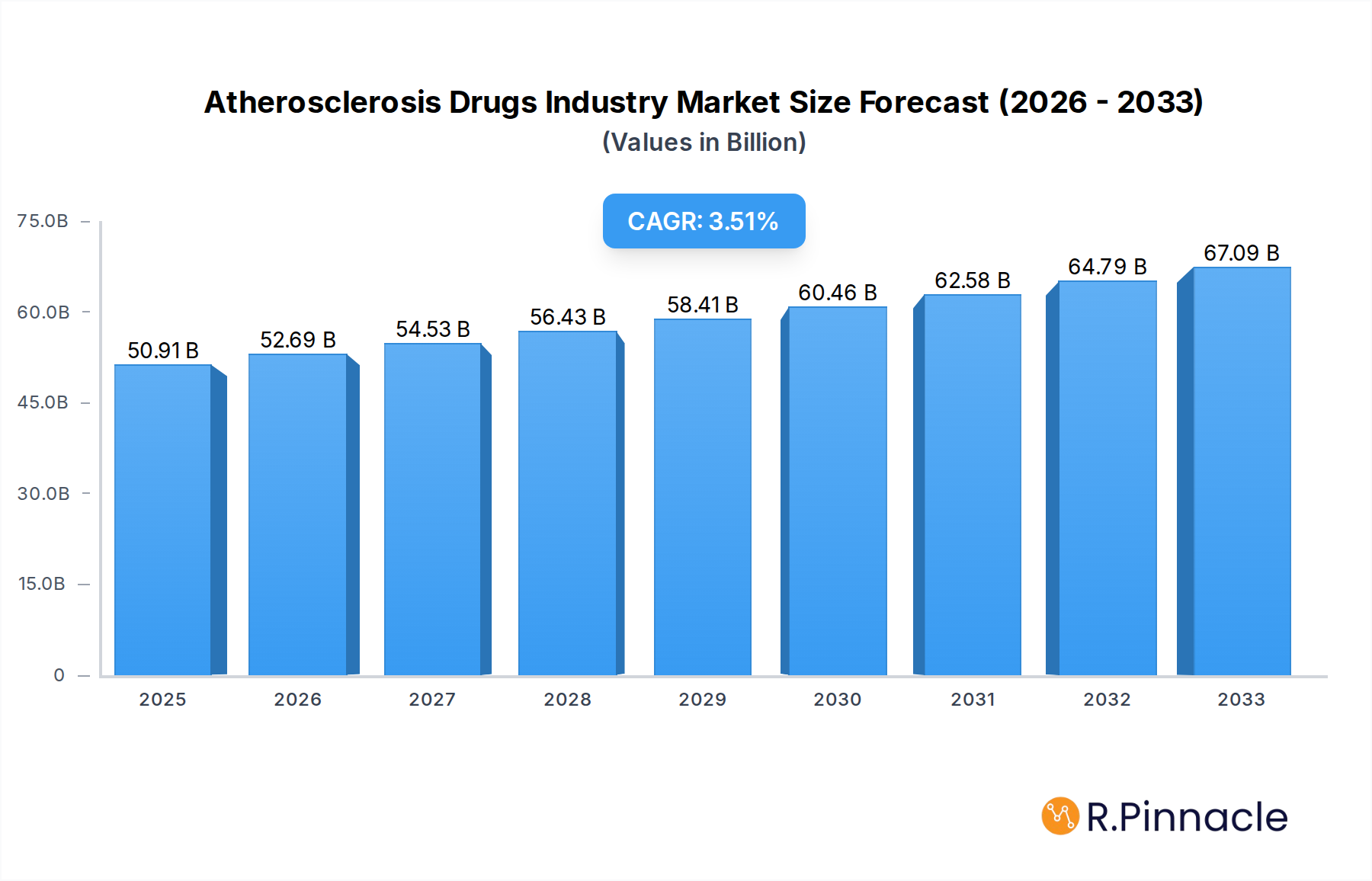

The Atherosclerosis Drugs market is poised for significant growth, with a projected market size of USD 50.91 billion in 2025. Driven by an increasing prevalence of cardiovascular diseases globally, advancements in drug development, and a growing awareness of preventative healthcare, the market is expected to expand at a Compound Annual Growth Rate (CAGR) of 3.5% from 2025 to 2033. Key therapeutic segments like Anti-platelet Medications and Cholesterol Lowering Medications are expected to lead this expansion, owing to their established efficacy in managing the risk factors associated with atherosclerosis. Furthermore, the growing adoption of novel drug classes and the increasing accessibility of treatments through various distribution channels, including online pharmacies, are contributing to this positive market trajectory. The rising global burden of chronic diseases, coupled with an aging population, fuels the sustained demand for effective atherosclerosis treatments, making this a critical area of pharmaceutical focus.

Atherosclerosis Drugs Industry Market Size (In Billion)

The market is characterized by a competitive landscape with major pharmaceutical giants such as Regeneron Pharmaceuticals Inc, Bayer AG, and Novartis AG at the forefront, actively investing in research and development to introduce innovative therapies. Emerging trends include the focus on personalized medicine and combination therapies to address the complex nature of atherosclerosis. However, challenges such as stringent regulatory approvals for new drugs and the high cost of some advanced treatments could act as restraints. Geographically, North America and Europe are anticipated to remain dominant markets due to high healthcare spending and advanced medical infrastructure, while the Asia Pacific region presents substantial growth opportunities driven by its large population, increasing disposable incomes, and a rising incidence of lifestyle-related diseases. The strategic initiatives by key players, including mergers, acquisitions, and partnerships, will further shape the market dynamics and innovation in the coming years.

Atherosclerosis Drugs Industry Company Market Share

Gain unparalleled insights into the burgeoning Atherosclerosis Drugs industry with this definitive market report. Spanning a comprehensive study period from 2019 to 2033, with a base year of 2025, this analysis delves deep into market dynamics, innovation trends, regional dominance, and future growth trajectories. We dissect the market through the lens of key drug classes, distribution channels, and groundbreaking industry developments, providing actionable intelligence for stakeholders. This report leverages high-ranking keywords and a reader-centric approach to offer a detailed, up-to-the-minute overview of a critical segment of the global healthcare market, projected to reach billions in value.

Atherosclerosis Drugs Industry Market Structure & Innovation Trends

The Atherosclerosis Drugs industry exhibits a moderately concentrated market structure, driven by significant R&D investments and stringent regulatory approvals. Innovation is a paramount driver, with companies continuously pursuing novel therapeutic targets and drug delivery mechanisms to address the complex nature of atherosclerosis. Key innovation drivers include advancements in genetic research, personalized medicine, and the development of targeted therapies. Regulatory frameworks, including those set by the FDA and EMA, play a crucial role in shaping market entry and product lifecycles. While generic competition exists for established treatments, patent protection for novel drugs creates temporary monopolies. Product substitutes include lifestyle modifications and interventional procedures, though pharmacological interventions remain central to long-term management. End-user demographics are predominantly aging populations and individuals with high-risk factors such as hypertension, diabetes, and hyperlipidemia. Mergers and acquisition (M&A) activities are prevalent, with deal values often reaching hundreds of millions to billions of dollars, as larger pharmaceutical companies seek to bolster their pipelines and expand market reach. For instance, a significant M&A deal in the cardiovascular space could involve a value exceeding $5 billion, reflecting the strategic importance of this therapeutic area. Market share dynamics are influenced by the efficacy, safety profile, and cost-effectiveness of approved therapies, with key players holding substantial portions of the market.

Atherosclerosis Drugs Industry Market Dynamics & Trends

The Atherosclerosis Drugs industry is propelled by a confluence of robust growth drivers, technological disruptions, evolving consumer preferences, and intense competitive dynamics. A primary growth driver is the escalating global prevalence of atherosclerosis, directly linked to the rising incidence of lifestyle-related diseases such as obesity, diabetes, and sedentary living. This surge in patient populations necessitates effective pharmacological interventions, creating sustained demand for advanced treatments. Technological disruptions are at the forefront of market evolution. The advent of novel drug classes, such as PCSK9 inhibitors and small interfering RNA (siRNA) therapies, represents a paradigm shift in managing cholesterol levels and reducing cardiovascular risk. These innovations offer significantly improved efficacy and novel mechanisms of action compared to traditional statins. Furthermore, advancements in diagnostic technologies, including genetic testing and advanced imaging, enable earlier and more precise diagnosis of atherosclerosis, thereby expanding the addressable market for therapeutic solutions. Consumer preferences are increasingly leaning towards treatments that offer convenience, better safety profiles, and a reduced pill burden. This is driving the demand for long-acting formulations and therapies with fewer side effects. The shift towards preventative healthcare is also influencing patient choices, with individuals actively seeking treatments that can mitigate future cardiovascular events. Competitive dynamics within the Atherosclerosis Drugs market are characterized by intense R&D efforts, strategic collaborations, and aggressive marketing strategies. Pharmaceutical giants are heavily invested in developing next-generation therapies, while smaller biotechs focus on niche therapeutic areas or innovative drug delivery systems. The market penetration of new drugs is often facilitated by strong clinical trial data, favorable reimbursement policies, and strategic partnerships with healthcare providers. The compound annual growth rate (CAGR) for the Atherosclerosis Drugs market is projected to be in the xx% range over the forecast period, indicating a healthy and expanding market. The increasing awareness of cardiovascular disease prevention and management strategies further fuels this growth, making Atherosclerosis Drugs a critical and dynamic sector within the pharmaceutical landscape. The total market value is expected to reach over $70 billion by 2033, driven by these multifaceted dynamics.

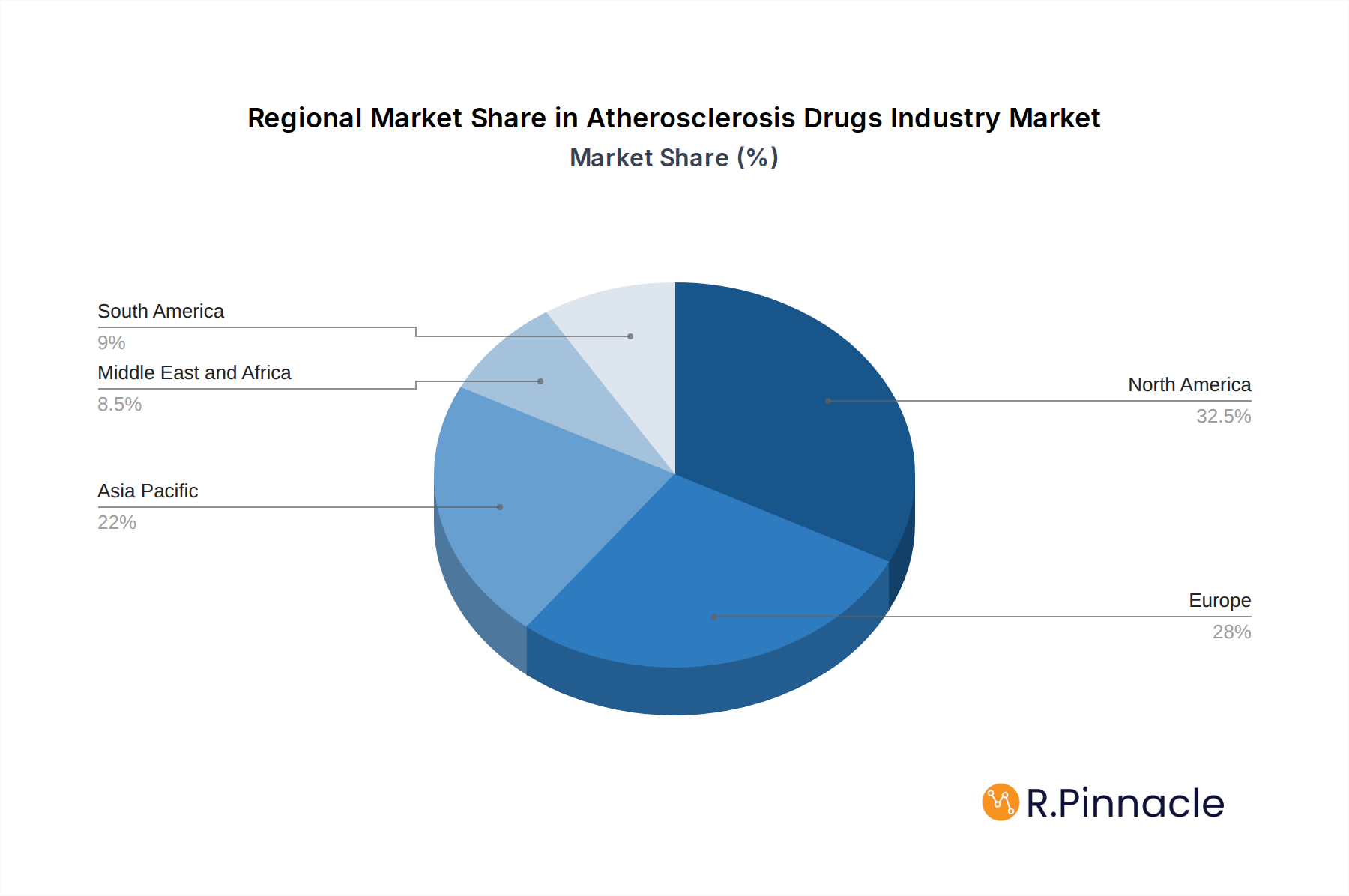

Dominant Regions & Segments in Atherosclerosis Drugs Industry

North America, particularly the United States, stands as the dominant region in the Atherosclerosis Drugs industry. This dominance is underpinned by several key drivers.

- Economic Policies: Robust healthcare spending, favorable reimbursement policies for advanced therapies, and a well-established network of research institutions contribute significantly to market growth. The presence of major pharmaceutical companies with substantial R&D budgets further solidifies its leading position.

- Infrastructure: Advanced healthcare infrastructure, including a high density of hospitals and specialized cardiovascular centers, ensures efficient patient access to innovative treatments. The strong emphasis on preventative healthcare and early diagnosis also plays a crucial role.

Within the drug class segmentation, Cholesterol Lowering Medications constitute the largest and most influential segment. This dominance stems from the widespread understanding of hyperlipidemia as a primary risk factor for atherosclerosis and the long-standing efficacy of statins, coupled with the recent introduction of highly effective novel agents like PCSK9 inhibitors. The market for cholesterol-lowering medications is projected to exceed $30 billion by 2025.

- Key Drivers for Cholesterol Lowering Medications:

- High prevalence of dyslipidemia and cardiovascular disease risk factors.

- Extensive clinical evidence supporting the efficacy of cholesterol reduction in preventing cardiovascular events.

- Continuous innovation leading to new drug classes with superior efficacy and improved patient adherence.

In terms of distribution channels, Retail Pharmacies currently hold the largest share. This is attributed to the high volume of prescription refills for chronic conditions like atherosclerosis, where long-term medication is essential. However, the influence of Hospital Pharmacies is growing, particularly for newly approved, high-cost specialty drugs that require specialized administration and monitoring. Online pharmacies are emerging as a significant channel, offering convenience and potentially competitive pricing, especially for generic medications.

- Market Size and Growth Projections for Key Segments (Estimated 2025):

- Cholesterol Lowering Medications: $30 billion+, with a projected CAGR of xx%.

- Anti-platelet Medications: $15 billion+, with a projected CAGR of xx%.

- Fibric Acid and Omega-3 Fatty Acid Derivatives: $5 billion+, with a projected CAGR of xx%.

- Beta Blockers: $10 billion+, with a projected CAGR of xx%.

- Others (including PCSK9 inhibitors, siRNA therapies): $10 billion+, with a projected CAGR of xx% (driven by rapid innovation).

The Asia-Pacific region is emerging as a high-growth market, driven by increasing healthcare expenditure, rising awareness, and a large patient pool suffering from lifestyle-related diseases. Key countries like China and India are witnessing substantial market expansion in Atherosclerosis Drugs.

Atherosclerosis Drugs Industry Product Innovations

Product innovations in the Atherosclerosis Drugs industry are characterized by a focus on enhanced efficacy, improved safety profiles, and novel mechanisms of action. The development of siRNA therapies, exemplified by Novartis' Leqvio, marks a significant advancement in lowering LDL cholesterol with infrequent dosing. PCSK9 inhibitors continue to offer potent lipid-lowering benefits for patients unresponsive to statins. Furthermore, research into anti-inflammatory agents targeting the underlying inflammatory processes of atherosclerosis shows promise. These innovations provide distinct competitive advantages by addressing unmet clinical needs and offering superior patient outcomes, fitting well within the evolving landscape of precision medicine and chronic disease management.

Report Scope & Segmentation Analysis

This report encompasses a comprehensive segmentation of the Atherosclerosis Drugs market, providing detailed analysis across key categories.

- Drug Class: The market is analyzed across Anti-platelet Medications, crucial for preventing clot formation; Cholesterol Lowering Medications, including statins, PCSK9 inhibitors, and novel agents for managing lipid profiles; Fibric Acid and Omega-3 Fatty Acid Derivatives, used for triglyceride management; Beta Blockers, impacting heart rate and blood pressure; and Others, encompassing emerging and investigational therapies.

- Distribution Channel: Segmentation includes Retail Pharmacies, serving a broad patient base; Hospital Pharmacies, crucial for in-patient treatment and specialty drugs; and Online Pharmacies, offering convenience and accessibility.

Each segment is analyzed for its current market size, projected growth rates, and competitive dynamics, with Cholesterol Lowering Medications expected to lead in market value, followed by Anti-platelet Medications.

Key Drivers of Atherosclerosis Drugs Industry Growth

The growth of the Atherosclerosis Drugs industry is propelled by several critical factors.

- Increasing Prevalence of Cardiovascular Diseases: Rising rates of obesity, diabetes, and hypertension globally directly correlate with a growing patient pool requiring atherosclerosis management.

- Technological Advancements in Drug Development: Innovations in genomics, molecular biology, and drug delivery systems are enabling the creation of more effective and targeted therapies.

- Aging Global Population: The demographic shift towards an older population inherently increases the incidence of chronic diseases, including atherosclerosis.

- Growing Awareness and Diagnosis Rates: Enhanced public health campaigns and improved diagnostic tools lead to earlier detection and treatment initiation.

- Favorable Reimbursement Policies: Supportive insurance coverage and government healthcare initiatives in key markets facilitate patient access to essential medications.

Challenges in the Atherosclerosis Drugs Industry Sector

Despite its growth, the Atherosclerosis Drugs industry faces several challenges.

- High Research and Development Costs: Developing novel drugs is an expensive and time-consuming process with a high rate of failure, impacting profitability.

- Stringent Regulatory Hurdles: Obtaining regulatory approval for new atherosclerosis drugs involves rigorous clinical trials and can lead to significant delays.

- Generic Competition: The expiration of patents for older, blockbuster drugs leads to market erosion by lower-cost generic alternatives.

- Pricing Pressures and Reimbursement Issues: Payers are increasingly scrutinizing the cost-effectiveness of new, high-priced therapies, leading to pricing challenges and potential access restrictions.

- Patient Adherence to Long-Term Treatment: Ensuring patients consistently take their prescribed medications for chronic conditions remains a persistent challenge.

Emerging Opportunities in Atherosclerosis Drugs Industry

The Atherosclerosis Drugs industry is ripe with emerging opportunities.

- Personalized Medicine: Advances in genetic profiling allow for the development of tailored therapies for specific patient subgroups, optimizing treatment efficacy.

- Novel Drug Delivery Systems: Innovations such as sustained-release formulations and implantable devices can improve patient compliance and therapeutic outcomes.

- Focus on Early Intervention and Prevention: Growing emphasis on preventative strategies opens avenues for drugs that can target early stages of atherosclerosis or high-risk individuals.

- Emerging Markets: Rapid economic development and increasing healthcare expenditure in Asia-Pacific and Latin America present significant growth potential.

- Combination Therapies: Development of synergistic drug combinations that target multiple pathways of atherosclerosis could offer enhanced therapeutic benefits.

Leading Players in the Atherosclerosis Drugs Industry Market

- Regeneron Pharmaceuticals Inc

- Bayer AG

- Novartis AG

- Amgen Inc

- Merck & Co Inc

- GlaxoSmithKline Plc

- Eli Lilly and Company

- AstraZeneca

- Viatris (Mylan N V )

Key Developments in Atherosclerosis Drugs Industry Industry

- December 2021: Novartis announced the US Food and Drug Administration (FDA) approval of Leqvio, the first and only small interfering RNA (siRNA) therapy to lower low-density lipoprotein cholesterol with two doses a year, after an initial dose and one at three months.

- December 2021: Royal Philips announced that it has signed an agreement to acquire Vesper Medical Inc., a US-based medical technology company that develops minimally invasive peripheral vascular devices. Vesper Medical will further expand Philips' portfolio of diagnostic and therapeutic devices with an advanced venous stent portfolio for the treatment of deep venous disease.

Future Outlook for Atherosclerosis Drugs Industry Market

The future outlook for the Atherosclerosis Drugs industry is exceptionally positive, driven by continuous innovation and a persistent, growing global need. Advancements in understanding the complex pathophysiology of atherosclerosis will undoubtedly lead to the development of more targeted and effective therapies. The integration of artificial intelligence and machine learning in drug discovery promises to accelerate the identification of novel drug candidates and optimize clinical trial designs. The increasing focus on preventative medicine and early intervention will create new market segments for drugs that can halt or even reverse the progression of the disease. Furthermore, the expanding healthcare infrastructure and rising disposable incomes in emerging economies will unlock significant growth potential. Strategic partnerships, mergers, and acquisitions will continue to shape the market landscape, fostering collaboration and driving innovation. The market is projected to witness sustained growth, reaching billions in value, and becoming an increasingly vital component of global cardiovascular healthcare.

Atherosclerosis Drugs Industry Segmentation

-

1. Drug Class

- 1.1. Anti-platelet Medications

- 1.2. Cholesterol Lowering Medications

- 1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 1.4. Beta Blockers

- 1.5. Others

-

2. Distribution Channel

- 2.1. Retail Pharmacies

- 2.2. Hospital Pharmacies

- 2.3. Online Pharmacies

Atherosclerosis Drugs Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Atherosclerosis Drugs Industry Regional Market Share

Geographic Coverage of Atherosclerosis Drugs Industry

Atherosclerosis Drugs Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 5.1.1. Anti-platelet Medications

- 5.1.2. Cholesterol Lowering Medications

- 5.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 5.1.4. Beta Blockers

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Retail Pharmacies

- 5.2.2. Hospital Pharmacies

- 5.2.3. Online Pharmacies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 6. Global Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 6.1.1. Anti-platelet Medications

- 6.1.2. Cholesterol Lowering Medications

- 6.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 6.1.4. Beta Blockers

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Retail Pharmacies

- 6.2.2. Hospital Pharmacies

- 6.2.3. Online Pharmacies

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 7. North America Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 7.1.1. Anti-platelet Medications

- 7.1.2. Cholesterol Lowering Medications

- 7.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 7.1.4. Beta Blockers

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Retail Pharmacies

- 7.2.2. Hospital Pharmacies

- 7.2.3. Online Pharmacies

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 8. Europe Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 8.1.1. Anti-platelet Medications

- 8.1.2. Cholesterol Lowering Medications

- 8.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 8.1.4. Beta Blockers

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Retail Pharmacies

- 8.2.2. Hospital Pharmacies

- 8.2.3. Online Pharmacies

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 9. Asia Pacific Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 9.1.1. Anti-platelet Medications

- 9.1.2. Cholesterol Lowering Medications

- 9.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 9.1.4. Beta Blockers

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Retail Pharmacies

- 9.2.2. Hospital Pharmacies

- 9.2.3. Online Pharmacies

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 10. Middle East and Africa Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 10.1.1. Anti-platelet Medications

- 10.1.2. Cholesterol Lowering Medications

- 10.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 10.1.4. Beta Blockers

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Retail Pharmacies

- 10.2.2. Hospital Pharmacies

- 10.2.3. Online Pharmacies

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 11. South America Atherosclerosis Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Drug Class

- 11.1.1. Anti-platelet Medications

- 11.1.2. Cholesterol Lowering Medications

- 11.1.3. Fibric Acid and Omega-3 Fatty Acid Derivatives

- 11.1.4. Beta Blockers

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Retail Pharmacies

- 11.2.2. Hospital Pharmacies

- 11.2.3. Online Pharmacies

- 11.1. Market Analysis, Insights and Forecast - by Drug Class

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Regeneron Pharmaceuticals Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bayer AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Novartis AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amgen Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Merck & Co Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GlaxoSmithKline Plc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Eli Lilly and Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 AstraZeneca

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Viatris (Mylan N V )

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Regeneron Pharmaceuticals Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Atherosclerosis Drugs Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Atherosclerosis Drugs Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Atherosclerosis Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 4: North America Atherosclerosis Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 5: North America Atherosclerosis Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 6: North America Atherosclerosis Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 7: North America Atherosclerosis Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 8: North America Atherosclerosis Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 9: North America Atherosclerosis Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Atherosclerosis Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America Atherosclerosis Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Atherosclerosis Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Atherosclerosis Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Atherosclerosis Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Atherosclerosis Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 16: Europe Atherosclerosis Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 17: Europe Atherosclerosis Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 18: Europe Atherosclerosis Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 19: Europe Atherosclerosis Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 20: Europe Atherosclerosis Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 21: Europe Atherosclerosis Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: Europe Atherosclerosis Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: Europe Atherosclerosis Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Atherosclerosis Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Atherosclerosis Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Atherosclerosis Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Atherosclerosis Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 28: Asia Pacific Atherosclerosis Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 29: Asia Pacific Atherosclerosis Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 30: Asia Pacific Atherosclerosis Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 31: Asia Pacific Atherosclerosis Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 32: Asia Pacific Atherosclerosis Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 33: Asia Pacific Atherosclerosis Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Asia Pacific Atherosclerosis Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Asia Pacific Atherosclerosis Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Pacific Atherosclerosis Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Atherosclerosis Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Atherosclerosis Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Atherosclerosis Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 40: Middle East and Africa Atherosclerosis Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 41: Middle East and Africa Atherosclerosis Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 42: Middle East and Africa Atherosclerosis Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 43: Middle East and Africa Atherosclerosis Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 44: Middle East and Africa Atherosclerosis Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 45: Middle East and Africa Atherosclerosis Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East and Africa Atherosclerosis Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Middle East and Africa Atherosclerosis Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East and Africa Atherosclerosis Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Atherosclerosis Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Atherosclerosis Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Atherosclerosis Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 52: South America Atherosclerosis Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 53: South America Atherosclerosis Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 54: South America Atherosclerosis Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 55: South America Atherosclerosis Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 56: South America Atherosclerosis Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 57: South America Atherosclerosis Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: South America Atherosclerosis Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: South America Atherosclerosis Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: South America Atherosclerosis Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Atherosclerosis Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Atherosclerosis Drugs Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 2: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 3: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 8: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 9: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 20: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 21: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Germany Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: France Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Italy Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Spain Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 38: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 39: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 40: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 41: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: China Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Japan Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: India Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Australia Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: South Korea Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 56: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 57: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 58: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 59: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: GCC Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: South Africa Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 68: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 69: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 70: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 71: Global Atherosclerosis Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 72: Global Atherosclerosis Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: Brazil Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Argentina Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Atherosclerosis Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Atherosclerosis Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Atherosclerosis Drugs Industry?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the Atherosclerosis Drugs Industry?

Key companies in the market include Regeneron Pharmaceuticals Inc, Bayer AG, Novartis AG, Amgen Inc, Merck & Co Inc, GlaxoSmithKline Plc, Eli Lilly and Company, AstraZeneca, Viatris (Mylan N V ).

3. What are the main segments of the Atherosclerosis Drugs Industry?

The market segments include Drug Class, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.91 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Prevalence of Atherosclerosis & Cardiovascular Diseases; Rising Awareness about Cardiovascular Diseases.

6. What are the notable trends driving market growth?

Cholesterol Lowering Medications Segment is Dominating the Atherosclerosis Drugs Market..

7. Are there any restraints impacting market growth?

Low Diagnostic Rate; Availability of Generic Products.

8. Can you provide examples of recent developments in the market?

In December 2021, Novartis announced the US Food and Drug Administration (FDA) approval of Leqvio, the first and only small interfering RNA (siRNA) therapy to lower low-density lipoprotein cholesterol with two doses a year, after an initial dose and one at three months.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Atherosclerosis Drugs Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Atherosclerosis Drugs Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Atherosclerosis Drugs Industry?

To stay informed about further developments, trends, and reports in the Atherosclerosis Drugs Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence