Key Insights

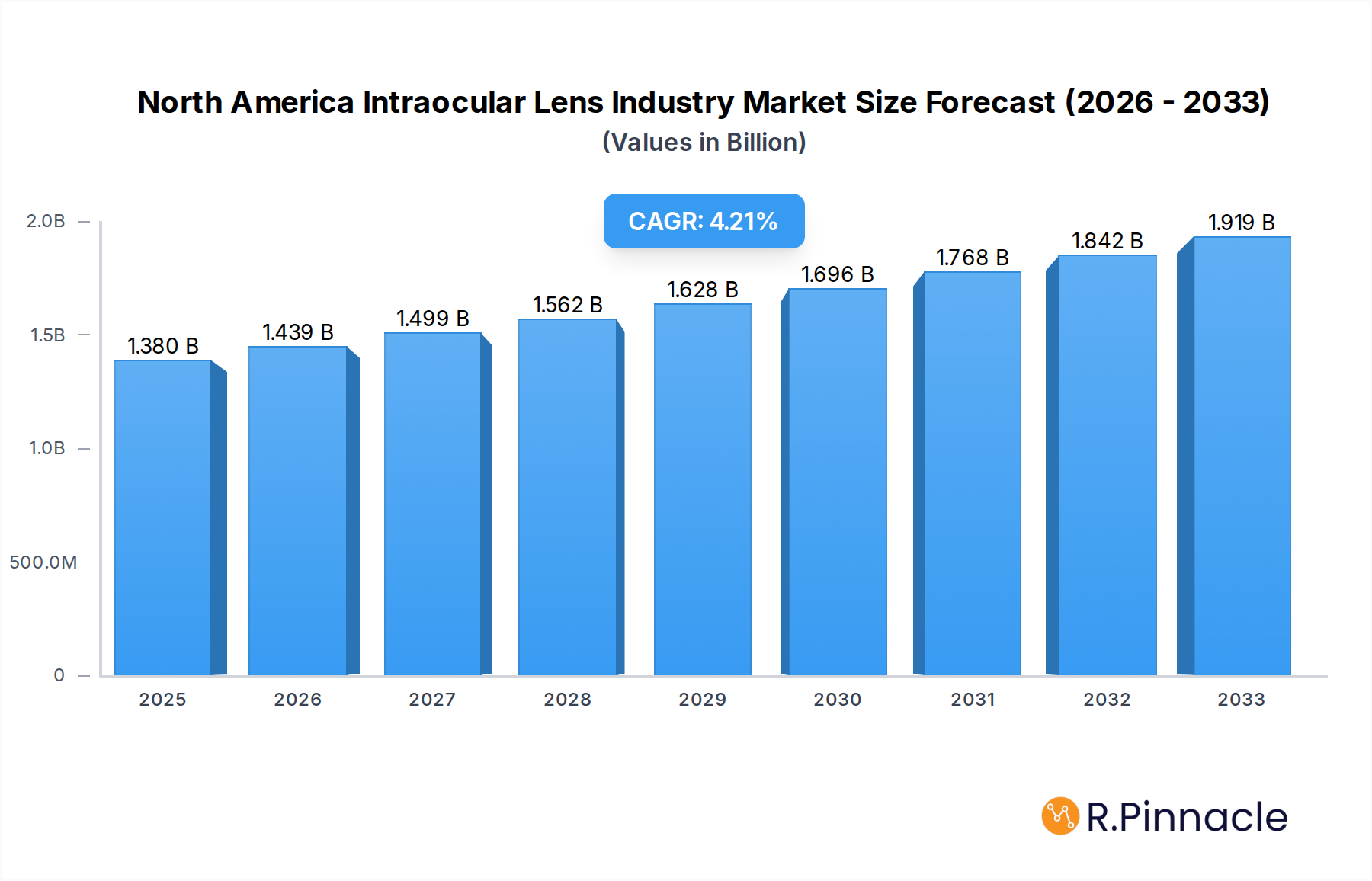

The North American Intraocular Lens (IOL) market is poised for robust expansion, projected to reach $1.38 billion by 2025 and grow at a Compound Annual Growth Rate (CAGR) of 4.33% through 2033. This substantial growth is fueled by a confluence of factors, including the increasing prevalence of age-related eye conditions such as cataracts, a growing aging population, and advancements in lens technology offering improved visual outcomes. The rising demand for sophisticated IOLs like multifocal and toric lenses, which correct both distance vision and astigmatism or presbyopia, is a significant driver. Furthermore, increasing healthcare expenditure and greater patient awareness regarding surgical options for vision correction contribute to market vitality. The market segmentation reveals a diverse landscape, with Monofocal Intraocular Lenses holding a substantial share, while Accommodative, Multifocal, and Toric Intraocular Lenses are experiencing rapid adoption due to their enhanced functional benefits. Hospitals and ambulatory surgery centers represent the primary end-user segments, reflecting the shift towards outpatient procedures.

North America Intraocular Lens Industry Market Size (In Billion)

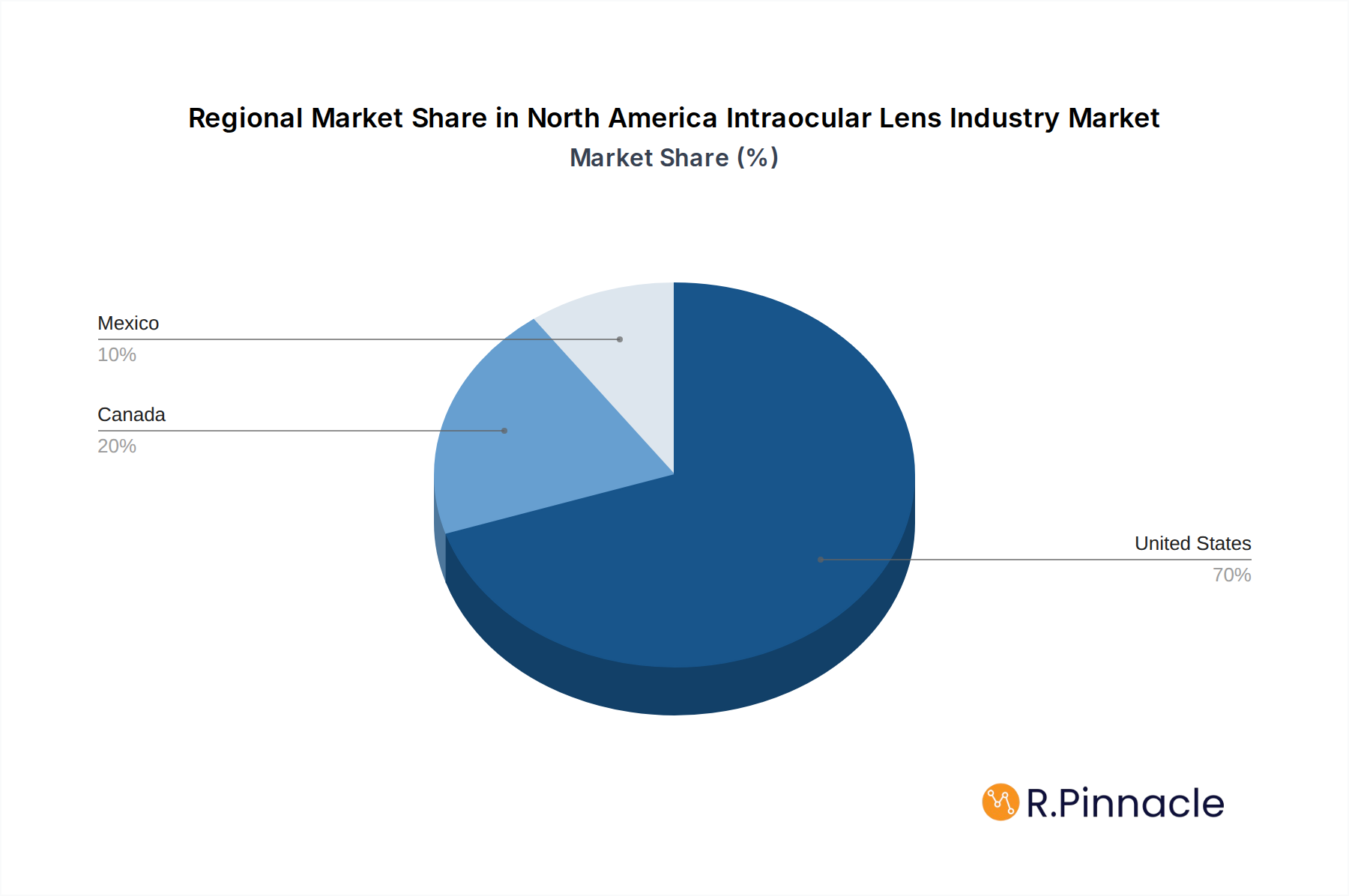

The North American IOL market is characterized by dynamic trends and strategic company initiatives aimed at capturing market share. Key players like STAAR Surgical Company, Carl Zeiss Meditec AG, and Johnson & Johnson are at the forefront, investing heavily in research and development to introduce innovative IOL designs and materials. The market also faces certain restraints, including the high cost of advanced lens technologies, reimbursement challenges, and the availability of alternative vision correction methods. However, the overwhelming benefits of modern IOLs in restoring and enhancing vision for a growing patient demographic are expected to outweigh these limitations. Geographically, the United States dominates the market due to its advanced healthcare infrastructure, high disposable incomes, and significant patient volume. Canada and Mexico, while smaller, present considerable growth opportunities driven by improving healthcare access and increasing adoption of ophthalmic surgical procedures. The forecast period is anticipated to witness continued innovation and strategic collaborations, solidifying the IOL market's importance in improving ocular health across North America.

North America Intraocular Lens Industry Company Market Share

North America Intraocular Lens Industry Market: Comprehensive Insights and Future Projections (2019-2033)

This report provides an in-depth analysis of the North America Intraocular Lens (IOL) industry, encompassing market structure, dynamics, segmentation, innovations, and future outlook. With a study period from 2019 to 2033 and a base year of 2025, this research offers critical insights for industry stakeholders. The North American IOL market is projected to experience significant growth, driven by an aging population, increasing prevalence of eye diseases, and advancements in surgical techniques.

North America Intraocular Lens Industry Market Structure & Innovation Trends

The North America Intraocular Lens industry exhibits a moderately concentrated market structure, with key players like Johnson & Johnson, Alcon, and Carl Zeiss Meditec AG holding substantial market share. Innovation is a primary driver, fueled by ongoing research and development in areas such as premium IOLs, including toric and multifocal designs, to address a wider range of patient needs and improve visual outcomes. Regulatory frameworks, primarily governed by the U.S. Food and Drug Administration (FDA) and Health Canada, play a crucial role in approving new devices and ensuring patient safety. Product substitutes, while limited in direct functionality, can include advancements in other vision correction methods. End-user demographics are shifting towards an aging population with higher disposable incomes, increasing demand for advanced IOLs. Mergers and acquisitions (M&A) activity, valued in the billions, continues to shape the competitive landscape as companies seek to expand their product portfolios and market reach. For instance, strategic partnerships and acquisitions are often driven by the pursuit of novel technologies that offer enhanced visual correction and patient satisfaction.

North America Intraocular Lens Industry Market Dynamics & Trends

The North America Intraocular Lens market is on a robust growth trajectory, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2025 to 2033. This growth is propelled by a confluence of factors. The escalating prevalence of age-related macular degeneration and cataracts, particularly in aging populations across the United States, Canada, and Mexico, is a primary demand accelerator. Technological disruptions are continuously reshaping the market, with the introduction of advanced IOLs such as accommodative and extended depth-of-focus (EDOF) lenses offering improved visual acuity across multiple distances, significantly reducing the need for corrective eyewear post-surgery. Consumer preferences are increasingly leaning towards premium IOLs that provide spectacle independence and enhanced quality of life, driving market penetration of these sophisticated lens types. Competitive dynamics are characterized by intense innovation and strategic collaborations. Key players are investing heavily in research and development to launch next-generation IOLs with superior optical performance and reduced side effects. The growing acceptance of refractive lens exchange (RLE) as an alternative to laser vision correction for individuals with presbyopia further fuels market expansion. Reimbursement policies and healthcare expenditure also play a pivotal role in market accessibility and growth. As healthcare systems continue to prioritize efficient and effective solutions for vision correction, the demand for high-quality IOLs is set to surge. The expanding base of ophthalmic surgeons adopting minimally invasive surgical techniques also contributes to the market's upward trend, facilitating quicker patient recovery and increased procedural volumes.

Dominant Regions & Segments in North America Intraocular Lens Industry

The United States stands as the dominant region within the North America Intraocular Lens industry, driven by its advanced healthcare infrastructure, high per capita healthcare spending, and a large, aging population susceptible to age-related eye conditions.

- Key Drivers in the United States:

- Demographics: A significant demographic of individuals aged 60 and above, a prime demographic for cataract surgery.

- Healthcare Expenditure: High levels of investment in healthcare, enabling access to advanced medical technologies.

- Technological Adoption: Rapid adoption of innovative IOL technologies due to a strong research and development ecosystem.

- Regulatory Environment: A well-established regulatory framework that supports innovation while ensuring patient safety.

From a product perspective, the Monofocal Intraocular Lens segment currently holds the largest market share due to its cost-effectiveness and widespread use in routine cataract surgeries. However, the Multifocal Intraocular Lens and Toric Intraocular Lens segments are experiencing rapid growth. Multifocal IOLs cater to the increasing demand for spectacle independence by providing vision correction at multiple distances, while Toric IOLs address astigmatism, offering a significant improvement in visual quality for affected patients. The demand for these premium IOLs is further bolstered by patient awareness and surgeon recommendations.

In terms of end-users, Hospitals represent the largest segment, performing a vast majority of cataract surgeries. However, Ambulatory Surgery Centers (ASCs) are witnessing substantial growth due to their cost-efficiency and convenience for outpatient procedures. The increasing volume of cataract surgeries performed in ASCs is a significant trend.

- Dominance Analysis: The dominance of the United States is underpinned by its economic prowess and the presence of major ophthalmic device manufacturers and research institutions. The continuous innovation pipeline originating from U.S.-based companies ensures a steady stream of advanced IOLs entering the market. The high prevalence of chronic diseases that can affect vision, such as diabetes, further contributes to the demand for ophthalmic procedures and IOLs. Canada and Mexico, while smaller markets, are also experiencing steady growth, influenced by increasing healthcare investments and a rising awareness of eye health. The trend towards premium IOLs is globally observed, but its adoption rate is particularly pronounced in the U.S. due to higher disposable incomes and insurance coverage for advanced procedures.

North America Intraocular Lens Industry Product Innovations

Product innovations in the North America Intraocular Lens industry are primarily focused on enhancing visual performance and patient outcomes. Developments include advanced aspheric designs for sharper vision, aberration-correcting lenses to mitigate visual distortions, and extended depth-of-focus (EDOF) IOLs that offer a wider range of clear vision. The integration of new materials and surface coatings aims to improve biocompatibility and reduce postoperative inflammation. Toric IOL advancements continue to refine astigmatism correction, while new accommodative IOLs promise more natural focus shifting. These innovations provide distinct competitive advantages by addressing unmet patient needs and expanding the therapeutic possibilities of cataract surgery.

Report Scope & Segmentation Analysis

This report meticulously segments the North America Intraocular Lens market across key categories. The Product segmentation includes Monofocal Intraocular Lens, Accommodative Intraocular Lens, Multifocal Intraocular Lens, and Toric Intraocular Lens. The End-User segmentation encompasses Hospitals, Ambulatory Centers, and Other Centers. The Geography segmentation covers the United States, Canada, and Mexico. Market size estimates and growth projections are provided for each segment, highlighting competitive dynamics and key influencing factors.

- Monofocal Intraocular Lens: Expected to maintain a significant market share due to its established efficacy and affordability, particularly in price-sensitive markets.

- Accommodative Intraocular Lens: Poised for robust growth driven by the desire for functional vision at various distances.

- Multifocal Intraocular Lens: Anticipated to witness substantial expansion as patients increasingly seek spectacle independence.

- Toric Intraocular Lens: Projected to grow steadily as the demand for precise astigmatism correction rises.

- Hospitals: Will remain the dominant end-user segment, but Ambulatory Centers will show faster growth.

- United States: Will continue to lead the market in revenue and volume.

Key Drivers of North America Intraocular Lens Industry Growth

The North America Intraocular Lens industry's growth is primarily propelled by the increasing prevalence of age-related eye diseases like cataracts, a direct consequence of the aging global population. Advancements in IOL technology, leading to premium lenses such as multifocal and toric implants, are creating new market opportunities by offering improved visual outcomes and reducing dependence on corrective eyewear. Favorable reimbursement policies and growing healthcare expenditure further support market expansion.

Challenges in the North America Intraocular Lens Industry Sector

Despite robust growth, the North America Intraocular Lens industry faces several challenges. Stringent regulatory approval processes for new IOLs can lead to lengthy development timelines and high costs. Intense competition among established players and emerging innovators can exert downward pressure on pricing. Furthermore, the high cost of premium IOLs can be a barrier for some patients, impacting market penetration in certain demographics. Supply chain disruptions, though less prevalent, can also pose a risk to market stability.

Emerging Opportunities in North America Intraocular Lens Industry

Emerging opportunities in the North America Intraocular Lens industry lie in the development and commercialization of next-generation EDOF IOLs and advanced toric IOLs with enhanced astigmatism correction. The growing interest in refractive lens exchange (RLE) for presbyopia treatment presents a significant untapped market. Furthermore, expanding into underserved regions and developing cost-effective IOL solutions for emerging economies offer substantial growth potential. Digital health integration, such as AI-powered diagnostic tools and personalized lens selection platforms, also represents a promising avenue for innovation and market differentiation.

Leading Players in the North America Intraocular Lens Industry Market

- STAAR Surgical Company

- Carl Zeiss Meditec AG

- USIOL Inc

- Rayner

- EyeKon Medical

- Bausch Health Companies Inc (Bausch + Lomb)

- Lenstec Inc

- HumanOptics Holding AG

- Johnson & Johnson

- HOYA Corporation

- Alcon

Key Developments in North America Intraocular Lens Industry Industry

- May 2023: Atia Vision presented the first clinical data on the patented OmniVu IOL System at the 2023 Annual Meeting of the American Society of Cataract Refractive Surgery (ASCRS) in San Diego, California.

- April 2023: ZEISS Medical Technology received the United States Food and Drug Administration (FDA) approval for CT LUCIA 621P Monofocal IOL, an aspheric, mono-focal, single-piece C-loop IOL.

Future Outlook for North America Intraocular Lens Industry Market

The future outlook for the North America Intraocular Lens industry is exceptionally bright, driven by continuous technological advancements and a growing demand for improved vision correction. The increasing adoption of premium IOLs, coupled with an expanding patient base seeking solutions for age-related vision impairments, will be key growth accelerators. Strategic partnerships and potential acquisitions are expected to further consolidate the market and foster innovation. The focus on personalized ophthalmology and minimally invasive surgical techniques will shape future product development and market strategies, promising enhanced patient outcomes and a sustained upward trajectory for the industry.

North America Intraocular Lens Industry Segmentation

-

1. Product

- 1.1. Monofocal Intraocular Lens

- 1.2. Accommodative Intraocular Lens

- 1.3. Multifocal Intraocular Lens

- 1.4. Toric Intraocular Lens

-

2. End-User

- 2.1. Hospitals

- 2.2. Ambulatory Centers

- 2.3. Other Centers

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Intraocular Lens Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Intraocular Lens Industry Regional Market Share

Geographic Coverage of North America Intraocular Lens Industry

North America Intraocular Lens Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.33% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Monofocal Intraocular Lens

- 5.1.2. Accommodative Intraocular Lens

- 5.1.3. Multifocal Intraocular Lens

- 5.1.4. Toric Intraocular Lens

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Centers

- 5.2.3. Other Centers

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Intraocular Lens Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Monofocal Intraocular Lens

- 6.1.2. Accommodative Intraocular Lens

- 6.1.3. Multifocal Intraocular Lens

- 6.1.4. Toric Intraocular Lens

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Centers

- 6.2.3. Other Centers

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. United States North America Intraocular Lens Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Monofocal Intraocular Lens

- 7.1.2. Accommodative Intraocular Lens

- 7.1.3. Multifocal Intraocular Lens

- 7.1.4. Toric Intraocular Lens

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Centers

- 7.2.3. Other Centers

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Canada North America Intraocular Lens Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Monofocal Intraocular Lens

- 8.1.2. Accommodative Intraocular Lens

- 8.1.3. Multifocal Intraocular Lens

- 8.1.4. Toric Intraocular Lens

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Centers

- 8.2.3. Other Centers

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Mexico North America Intraocular Lens Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Monofocal Intraocular Lens

- 9.1.2. Accommodative Intraocular Lens

- 9.1.3. Multifocal Intraocular Lens

- 9.1.4. Toric Intraocular Lens

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Hospitals

- 9.2.2. Ambulatory Centers

- 9.2.3. Other Centers

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 STAAR Surgical Company

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Carl Zeiss Meditec AG

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 USIOL Inc *List Not Exhaustive

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Rayner

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 EyeKon Medical

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Bausch Health Companies Inc (Bausch + Lomb)

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Lenstec Inc

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 HumanOptics Holding AG

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Johnson & Johnson

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 HOYA Corporation

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Alcon

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.1 STAAR Surgical Company

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Intraocular Lens Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Intraocular Lens Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Intraocular Lens Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: North America Intraocular Lens Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: North America Intraocular Lens Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Intraocular Lens Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Intraocular Lens Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 6: North America Intraocular Lens Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 7: North America Intraocular Lens Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North America Intraocular Lens Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Intraocular Lens Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 10: North America Intraocular Lens Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 11: North America Intraocular Lens Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: North America Intraocular Lens Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Intraocular Lens Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 14: North America Intraocular Lens Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 15: North America Intraocular Lens Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: North America Intraocular Lens Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Intraocular Lens Industry?

The projected CAGR is approximately 4.33%.

2. Which companies are prominent players in the North America Intraocular Lens Industry?

Key companies in the market include STAAR Surgical Company, Carl Zeiss Meditec AG, USIOL Inc *List Not Exhaustive, Rayner, EyeKon Medical, Bausch Health Companies Inc (Bausch + Lomb), Lenstec Inc, HumanOptics Holding AG, Johnson & Johnson, HOYA Corporation, Alcon.

3. What are the main segments of the North America Intraocular Lens Industry?

The market segments include Product, End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.38 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Burden of Ophthalmic Issues; Increasing Cases of Cataract in the Diabetic Population.

6. What are the notable trends driving market growth?

Accommodative Intraocular Lens is Expected to Exhibit Fastest Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Intraocular Lens; Lack of Reimbursement Policies.

8. Can you provide examples of recent developments in the market?

May 2023: Atia Vision presented the first clinical data on the patented OmniVu IOL System at the 2023 Annual Meeting of the American Society of Cataract Refractive Surgery (ASCRS) in San Diego, California.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Intraocular Lens Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Intraocular Lens Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Intraocular Lens Industry?

To stay informed about further developments, trends, and reports in the North America Intraocular Lens Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence