Key Insights

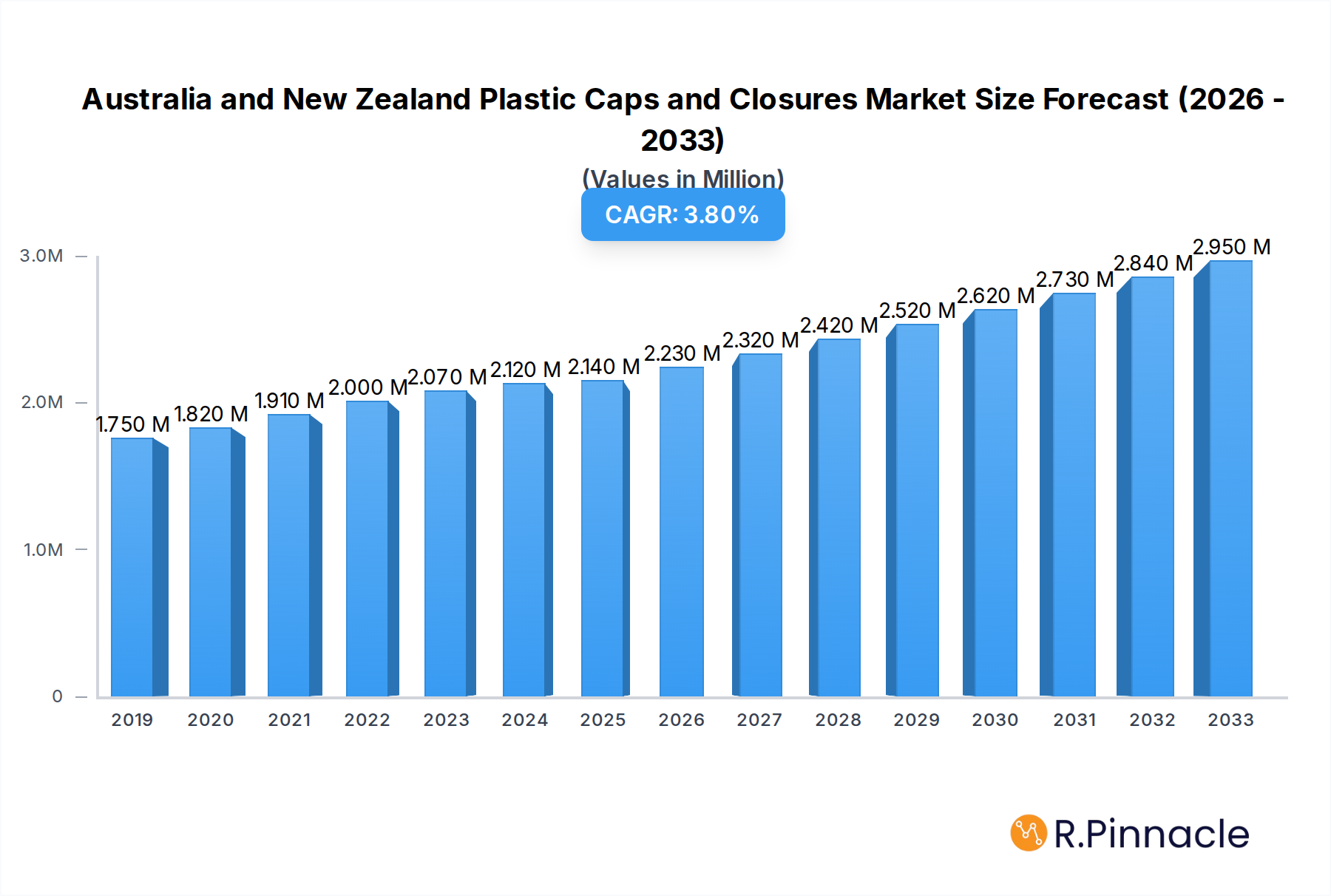

The Australia and New Zealand plastic caps and closures market is experiencing robust growth, projected to reach $2.14 million in value in 2025. This expansion is fueled by a CAGR of 4.29%, indicating a steady and significant upward trajectory for the industry. A primary driver of this growth is the increasing demand from the food and beverage sector, particularly for bottled water and carbonated soft drinks, which rely heavily on secure and functional plastic closures. The personal care and cosmetics industry also contributes substantially, driven by evolving consumer preferences for convenient and aesthetically pleasing packaging. Furthermore, the growing awareness and adoption of child-resistant closures across various product types, including household chemicals, are bolstering market expansion. Emerging trends such as the incorporation of sustainable materials and innovative designs, including dispensing closures for enhanced user experience, are shaping market dynamics and creating new opportunities for manufacturers.

Australia and New Zealand Plastic Caps and Closures Market Market Size (In Million)

The market's expansion is further supported by the versatility and cost-effectiveness of plastic caps and closures, making them a preferred choice for a wide array of applications. Polyethylene (PE) and Polypropylene (PP) remain dominant resin types due to their excellent properties and widespread availability. While the market is generally optimistic, potential restraints include rising raw material costs and stringent environmental regulations concerning plastic waste, which are prompting a shift towards recycled content and biodegradable alternatives. Despite these challenges, the continued innovation in product types and the persistent demand from key end-user industries in Australia and New Zealand are expected to sustain the market's growth momentum throughout the forecast period. Key players like Amcor Group GmbH and Bericap Holding GmbH are actively investing in research and development to offer advanced and sustainable solutions.

Australia and New Zealand Plastic Caps and Closures Market Company Market Share

Gain comprehensive insights into the dynamic Australia and New Zealand plastic caps and closures market with our latest report. This extensive analysis delves into market structure, key drivers, dominant segments, product innovations, and future outlook, providing actionable intelligence for industry stakeholders. Covering the period from 2019 to 2033, with a base year of 2025, this report offers a granular view of market trends and growth opportunities.

Australia and New Zealand Plastic Caps and Closures Market Market Structure & Innovation Trends

The Australia and New Zealand plastic caps and closures market exhibits a moderate to high level of concentration, with key players like Amcor Group GmbH, Bericap Holding GmbH, and Pact Group Holdings Limited holding significant market share. Innovation is primarily driven by the demand for sustainable packaging solutions, enhanced safety features such as child-resistant closures, and the development of lightweight, cost-effective designs. Regulatory frameworks, particularly concerning food safety and environmental impact, play a crucial role in shaping product development and market entry. While direct product substitutes are limited, the broader shift towards alternative packaging materials and refillable systems presents a strategic challenge. End-user demographics, characterized by a growing population and evolving consumer lifestyles, continuously influence demand for convenience and specialized closures. Merger and acquisition activities, such as the January 2024 acquisition of Plas-Pak WA by TricorBraun, highlight the ongoing consolidation and strategic expansion within the market, with deal values reaching millions, signaling a robust M&A landscape.

Australia and New Zealand Plastic Caps and Closures Market Market Dynamics & Trends

The Australia and New Zealand plastic caps and closures market is experiencing robust growth, propelled by several key dynamics. A significant growth driver is the expanding food and beverage sector, particularly the bottled water and juice segments, which rely heavily on reliable and tamper-evident closures. Furthermore, the increasing consumer demand for convenience and single-serve packaging in personal care and household chemical products is bolstering market penetration. Technological advancements in injection molding and material science are enabling the production of more sophisticated and sustainable closures, including those made from recycled and bio-based plastics. The competitive landscape is characterized by a blend of large multinational corporations and smaller, agile local manufacturers, each vying for market share through product differentiation, cost leadership, and strategic partnerships. The market is also influenced by evolving consumer preferences, with a growing emphasis on aesthetics, ease of use, and eco-friendliness. The overall CAGR for the forecast period is projected to be around 5.5%, reflecting sustained growth driven by these multifaceted trends. The increasing adoption of advanced sealing technologies and the rise of e-commerce, necessitating robust packaging for transit, also contribute significantly to market expansion. The focus on reducing material usage without compromising functionality, driven by both cost considerations and environmental regulations, is another critical trend shaping the market's trajectory.

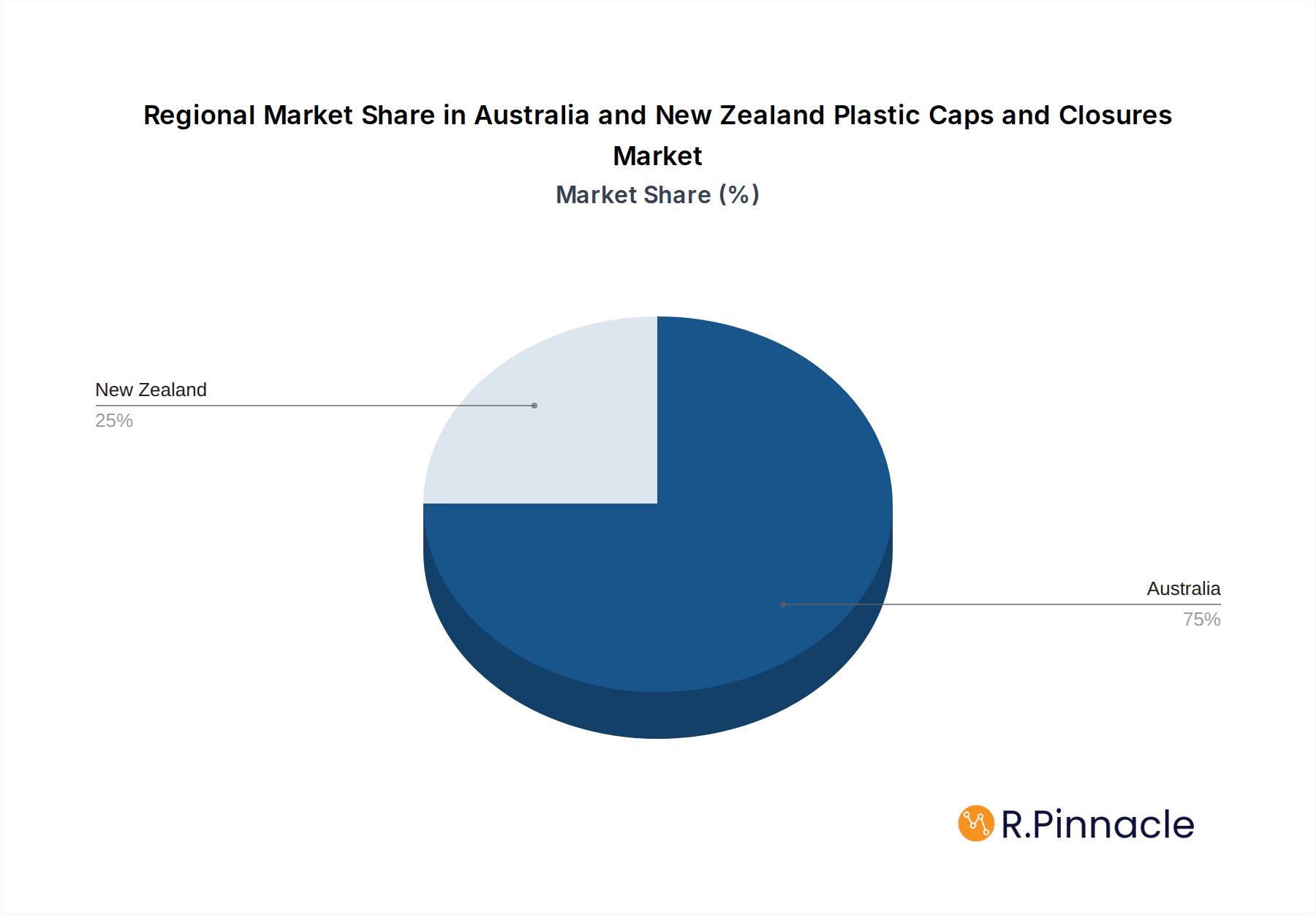

Dominant Regions & Segments in Australia and New Zealand Plastic Caps and Closures Market

Within the Australia and New Zealand plastic caps and closures market, Australia emerges as the dominant region due to its larger economy and population base. Within Australia, New South Wales and Victoria are leading states in terms of consumption and manufacturing. The Beverage end-user industry, particularly Bottled Water and Juices and Energy Drinks, represents the most significant segment, driven by high per capita consumption and the sheer volume of packaged goods.

- Resin: Polyethylene (PE) is the dominant resin type, owing to its cost-effectiveness, versatility, and excellent sealing properties. Polypropylene (PP) also holds a substantial market share, especially for applications requiring higher heat resistance and rigidity. Polyethylene Terephthalate (PET) is primarily used for bottles and their corresponding closures, often exhibiting a strong correlation with the PET bottle market.

- Key Drivers for PE Dominance: Cost-effectiveness, chemical resistance, flexibility, wide availability, and established manufacturing processes.

- Growth in PP: Driven by demand for tamper-evident features and applications requiring higher temperature stability.

- Product Type: Threaded closures continue to dominate due to their widespread use across various industries, offering secure sealing and ease of operation. However, the demand for Child-resistant closures is steadily increasing, especially within the pharmaceutical and household chemical sectors, driven by stringent safety regulations. Dispensing closures are also gaining traction in the personal care and food sectors for enhanced user experience.

- Threaded Closures: Ubiquitous across beverages, food, and personal care for their reliability and cost-effectiveness.

- Child-resistant Closures: Driven by regulatory mandates and growing consumer awareness of product safety.

- Dispensing Closures: Gaining popularity in personal care and certain food applications for controlled product release.

- End-user Industries: The Beverage sector accounts for the largest share, followed closely by Food. The Personal Care and Cosmetics and Household Chemicals industries also represent substantial markets, with specific needs for specialized closures.

- Beverage Sector Dominance: Driven by high volume demand from bottled water, soft drinks, juices, and energy drinks, requiring efficient and secure closure solutions.

- Food Industry Growth: Fueled by packaged food products, condiments, and sauces that demand tamper-evident and convenient closures.

- Personal Care & Cosmetics: Characterized by a demand for aesthetically pleasing and functional dispensing closures.

- Household Chemicals: Primarily driven by safety regulations and the need for child-resistant and leak-proof closures.

Australia and New Zealand Plastic Caps and Closures Market Product Innovations

Product innovation in the Australia and New Zealand plastic caps and closures market is focused on enhancing sustainability through the use of recycled content and biodegradable materials, as well as improving functionality with features like tamper-evident bands and easy-open mechanisms. Companies are developing lightweight designs to reduce material consumption and transportation costs, while also focusing on advanced dispensing technologies for personal care and household products. Competitive advantages are being built through the integration of smart features and specialized closures that offer improved shelf life for products.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the Australia and New Zealand plastic caps and closures market. The Resin segmentation includes Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), and Other Plastics, with PE and PP projected to hold the largest market shares due to their widespread application and cost-effectiveness. In terms of Product Type, Threaded closures are expected to lead, followed by the growing segments of Child-resistant and Dispensing closures. The End-user Industries are segmented into Food, Beverage (further broken down into Bottled Water, Carbonated Soft Drinks, Alcoholic Beverages, Juices and Energy Drinks, Other Beverages), Personal Care and Cosmetics, Household Chemicals, and Other End-user Industries, with the Beverage sector anticipated to dominate in terms of market size and growth.

Key Drivers of Australia and New Zealand Plastic Caps and Closures Market Growth

The growth of the Australia and New Zealand plastic caps and closures market is propelled by several key drivers. The expanding food and beverage industry, driven by increasing consumer demand for packaged goods and a growing population, is a primary catalyst. Growing awareness and adoption of sustainable packaging solutions, including those made from recycled plastics, are also significant contributors. Technological advancements in manufacturing processes, leading to more efficient and cost-effective production, further fuel market expansion. Additionally, evolving consumer preferences for convenience, safety, and enhanced product experience are driving demand for specialized closures like child-resistant and dispensing variants.

Challenges in the Australia and New Zealand Plastic Caps and Closures Market Sector

Despite the positive growth trajectory, the Australia and New Zealand plastic caps and closures market faces certain challenges. Fluctuations in raw material prices, particularly for virgin plastics, can impact manufacturing costs and profitability. Stringent environmental regulations and increasing consumer pressure for sustainable alternatives are compelling manufacturers to invest in eco-friendly solutions, which can incur significant R&D and capital expenditure. The competitive landscape, characterized by numerous players, intensifies pricing pressures. Furthermore, potential supply chain disruptions, though less frequent, can impact material availability and delivery timelines.

Emerging Opportunities in Australia and New Zealand Plastic Caps and Closures Market

Emerging opportunities in the Australia and New Zealand plastic caps and closures market lie in the growing demand for sustainable packaging solutions. The development and adoption of closures made from post-consumer recycled (PCR) content and bio-based plastics present a significant growth avenue. The expansion of the e-commerce sector necessitates innovative and secure packaging, creating opportunities for specialized closures that ensure product integrity during transit. Furthermore, the increasing focus on health and wellness is driving demand for tamper-evident and hygienic closures in food, beverage, and pharmaceutical applications. The innovation in dispensing technologies for personal care and household products also opens up new market segments.

Leading Players in the Australia and New Zealand Plastic Caps and Closures Market Market

- Amcor Group GmbH

- Bericap Holding GmbH

- Pact Group Holdings Limited

- Caprite Australia Pty Ltd

- Guala Closures SPA

- Primo Plastics

- Caps and Closures Pty Ltd

- Forward Plastics Ltd

- Flexicon Plastics

Key Developments in Australia and New Zealand Plastic Caps and Closures Market Industry

- January 2024: TricorBraun, a US-based company with operations in Australia, announced the acquisition of Plas-Pak WA, an Australian packaging manufacturer of bottles, caps, lids, and closures. This move will bolster TricorBraun's presence in Western Australia and broaden its customer reach.

- September 2023: TricorBraun, a US-based company with operations in Australia, unveiled its latest manufacturing hub in Sydney. With 16 cutting-edge injection molding machines, the facility is geared to churn out a diverse array of caps and closures, catering primarily to the food, beverage, and pharmaceutical sectors.

Future Outlook for Australia and New Zealand Plastic Caps and Closures Market Market

The future outlook for the Australia and New Zealand plastic caps and closures market remains positive, driven by ongoing innovation and evolving consumer demands. The strong emphasis on sustainability will continue to shape product development, with increased adoption of recycled and bio-based materials. Growth in key end-user industries, particularly beverages and personal care, will sustain demand for a wide range of closure solutions. Strategic collaborations and acquisitions are expected to continue as companies seek to expand their market reach and technological capabilities. The market is poised for steady growth, fueled by a combination of economic expansion, technological advancements, and a growing consumer consciousness regarding packaging solutions.

Australia and New Zealand Plastic Caps and Closures Market Segmentation

-

1. Resin

- 1.1. Polyethylene (PE)

- 1.2. Polyethylene Terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Other Pl

-

2. Product Type

- 2.1. Threaded

- 2.2. Dispensing

- 2.3. Unthreaded

- 2.4. Child-resistant

-

3. End-user Industries

- 3.1. Food

-

3.2. Beverage

- 3.2.1. Bottled Water

- 3.2.2. Carbonated Soft Drinks

- 3.2.3. Alcoholic Beverages

- 3.2.4. Juices and Energy Drinks

- 3.2.5. Other Beverages

- 3.3. Personal Care and Cosmetics

- 3.4. Household Chemicals

- 3.5. Other End-user Industries

Australia and New Zealand Plastic Caps and Closures Market Segmentation By Geography

- 1. Australia

Australia and New Zealand Plastic Caps and Closures Market Regional Market Share

Geographic Coverage of Australia and New Zealand Plastic Caps and Closures Market

Australia and New Zealand Plastic Caps and Closures Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Polyethylene (PE)

- 5.1.2. Polyethylene Terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Other Pl

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Threaded

- 5.2.2. Dispensing

- 5.2.3. Unthreaded

- 5.2.4. Child-resistant

- 5.3. Market Analysis, Insights and Forecast - by End-user Industries

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.2.1. Bottled Water

- 5.3.2.2. Carbonated Soft Drinks

- 5.3.2.3. Alcoholic Beverages

- 5.3.2.4. Juices and Energy Drinks

- 5.3.2.5. Other Beverages

- 5.3.3. Personal Care and Cosmetics

- 5.3.4. Household Chemicals

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Australia and New Zealand Plastic Caps and Closures Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Polyethylene (PE)

- 6.1.2. Polyethylene Terephthalate (PET)

- 6.1.3. Polypropylene (PP)

- 6.1.4. Other Pl

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Threaded

- 6.2.2. Dispensing

- 6.2.3. Unthreaded

- 6.2.4. Child-resistant

- 6.3. Market Analysis, Insights and Forecast - by End-user Industries

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.2.1. Bottled Water

- 6.3.2.2. Carbonated Soft Drinks

- 6.3.2.3. Alcoholic Beverages

- 6.3.2.4. Juices and Energy Drinks

- 6.3.2.5. Other Beverages

- 6.3.3. Personal Care and Cosmetics

- 6.3.4. Household Chemicals

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bericap Holding GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Pact Group Holdings Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Caprite Australia Pty Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Guala Closures SPA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Primo Plastics

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Caps and Closures Pty Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Forward Plastics Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Flexicon Plastics*List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Amcor Group GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia and New Zealand Plastic Caps and Closures Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australia and New Zealand Plastic Caps and Closures Market Share (%) by Company 2025

List of Tables

- Table 1: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 2: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Resin 2020 & 2033

- Table 3: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Product Type 2020 & 2033

- Table 5: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by End-user Industries 2020 & 2033

- Table 6: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by End-user Industries 2020 & 2033

- Table 7: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 10: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Resin 2020 & 2033

- Table 11: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Product Type 2020 & 2033

- Table 13: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by End-user Industries 2020 & 2033

- Table 14: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by End-user Industries 2020 & 2033

- Table 15: Australia and New Zealand Plastic Caps and Closures Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Australia and New Zealand Plastic Caps and Closures Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia and New Zealand Plastic Caps and Closures Market?

The projected CAGR is approximately 4.29%.

2. Which companies are prominent players in the Australia and New Zealand Plastic Caps and Closures Market?

Key companies in the market include Amcor Group GmbH, Bericap Holding GmbH, Pact Group Holdings Limited, Caprite Australia Pty Ltd, Guala Closures SPA, Primo Plastics, Caps and Closures Pty Ltd, Forward Plastics Ltd, Flexicon Plastics*List Not Exhaustive.

3. What are the main segments of the Australia and New Zealand Plastic Caps and Closures Market?

The market segments include Resin, Product Type, End-user Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.14 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in the Food and Beverage Sector; Rising Demand of Innovative Caps and Closures.

6. What are the notable trends driving market growth?

Polyethylene (PE) Segment is Estimated to Have the Largest Market Share.

7. Are there any restraints impacting market growth?

Growth in the Food and Beverage Sector; Rising Demand of Innovative Caps and Closures.

8. Can you provide examples of recent developments in the market?

January 2024: TricorBraun, a US-based company with operations in Australia, announced the acquisition of Plas-Pak WA, an Australian packaging manufacturer of bottles, caps, lids, and closures. This move will bolster TricorBraun's presence in Western Australia and broaden its customer reach.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia and New Zealand Plastic Caps and Closures Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia and New Zealand Plastic Caps and Closures Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia and New Zealand Plastic Caps and Closures Market?

To stay informed about further developments, trends, and reports in the Australia and New Zealand Plastic Caps and Closures Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence