Key Insights

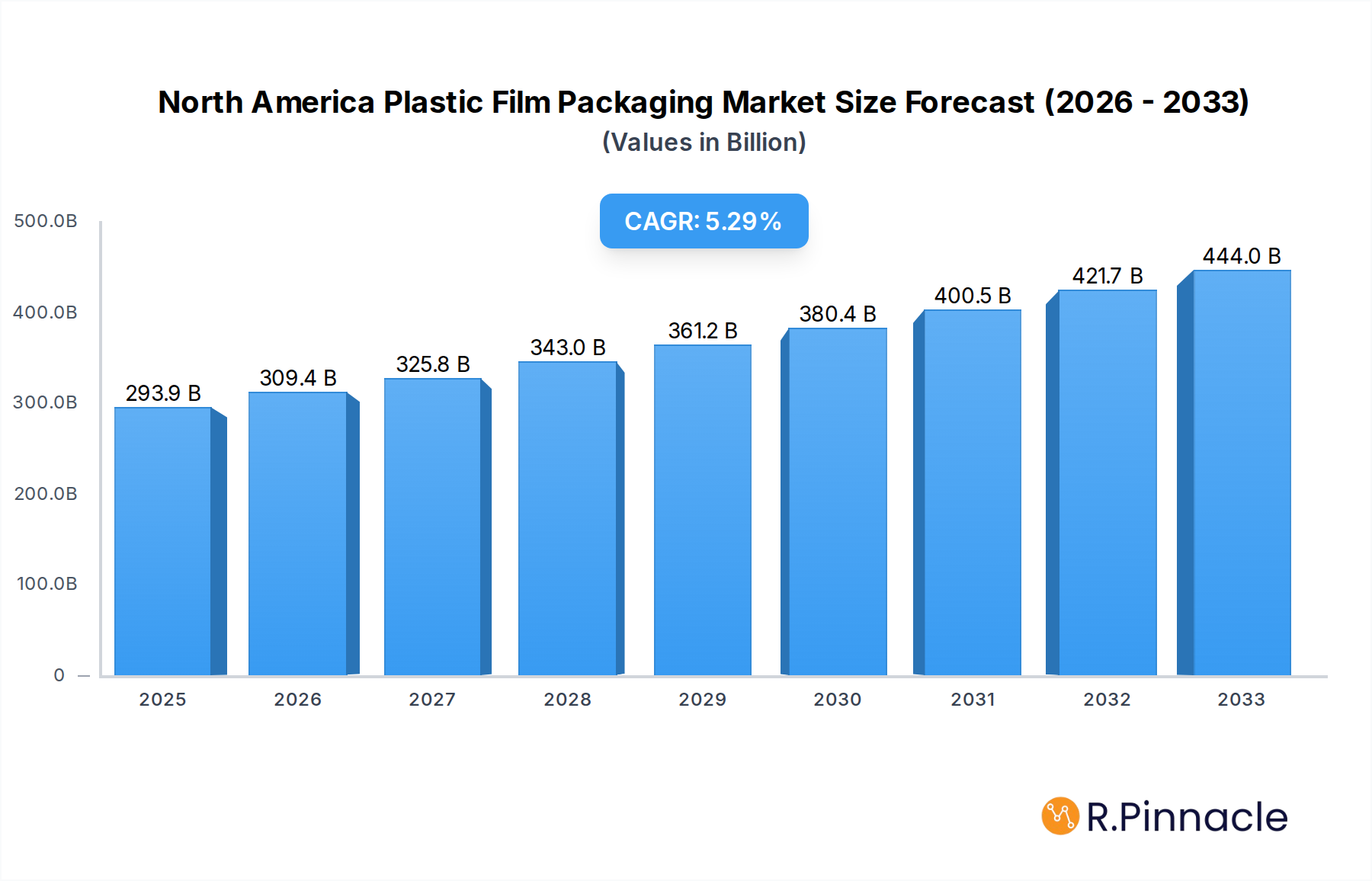

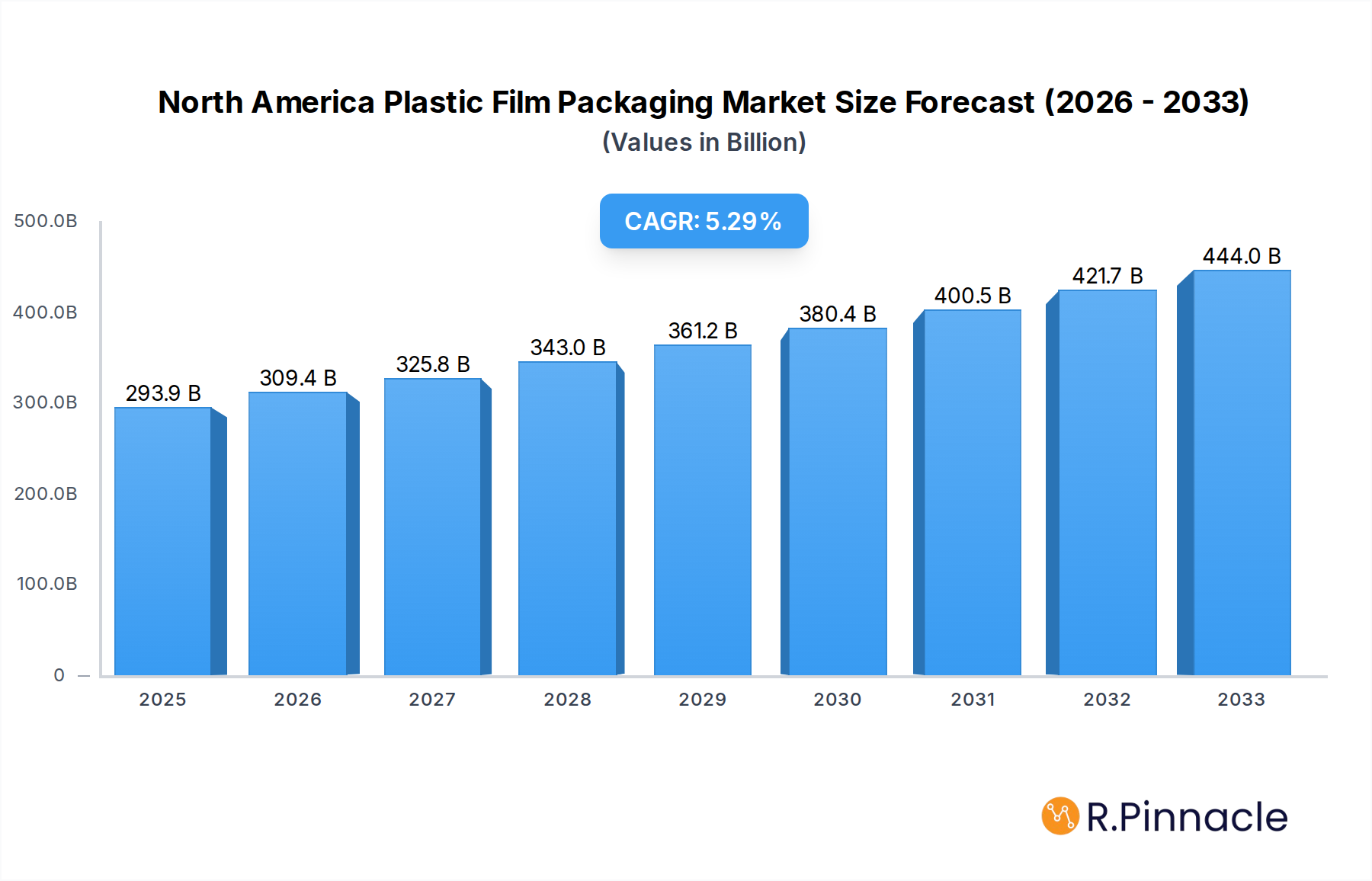

The North America Plastic Film Packaging Market is poised for significant growth, with an estimated market size of $293.92 billion in 2025. Driven by the ever-increasing demand for flexible, lightweight, and cost-effective packaging solutions across various industries, the market is projected to expand at a robust CAGR of 5.3% throughout the forecast period (2025-2033). The food and beverage sector remains the dominant end-user industry, fueled by the need for extended shelf life, product protection, and consumer convenience. Trends such as the rising popularity of ready-to-eat meals, convenience foods, and individual portion sizes are directly contributing to the demand for specialized plastic films. Furthermore, the growing emphasis on aesthetic appeal and branding in consumer goods packaging also plays a crucial role in market expansion.

North America Plastic Film Packaging Market Market Size (In Billion)

Despite this optimistic outlook, certain factors may present challenges. Increasing environmental concerns and stringent regulations regarding plastic waste are prompting a shift towards sustainable alternatives. While bio-based films are emerging as a viable segment, their adoption is still in its nascent stages compared to traditional plastics. Moreover, fluctuating raw material prices, particularly for petroleum-based resins, can impact the profitability of plastic film manufacturers. However, continuous innovation in material science, the development of advanced barrier properties, and the integration of recycling technologies are expected to mitigate these restraints. The market is characterized by the presence of a diverse range of film types, including polyethylene (PE) and polypropylene (PP), which hold substantial market share due to their versatility and cost-effectiveness. Emerging segments like bio-based films are also gaining traction, reflecting the industry's commitment to sustainability.

North America Plastic Film Packaging Market Company Market Share

This in-depth market research report offers a comprehensive analysis of the North America Plastic Film Packaging Market, a dynamic sector poised for significant expansion. Covering the historical period of 2019-2024 and projecting growth through 2033, with a base year of 2025, this report provides critical insights for industry stakeholders. Explore market size, segmentation, competitive landscape, innovation trends, and future outlook, all within a reader-centric framework designed for actionable intelligence.

North America Plastic Film Packaging Market Market Structure & Innovation Trends

The North America Plastic Film Packaging Market exhibits a moderately concentrated structure, characterized by the presence of both global giants and specialized regional players. Innovation remains a key differentiator, driven by the escalating demand for enhanced barrier properties, sustainability, and cost-effectiveness. Regulatory frameworks, particularly those concerning environmental impact and recyclability, are increasingly influencing product development and market strategies. The threat of product substitutes, such as paper-based or compostable packaging, is present but currently limited by performance and cost considerations for many applications. End-user demographics are evolving, with a growing emphasis on convenience, health consciousness, and eco-friendly options, particularly within the food and personal care segments. Mergers and acquisitions (M&A) activities are a recurring theme, consolidating market share and fostering technological integration. For instance, recent M&A deals have seen valuations in the multi-billion dollar range, underscoring the strategic importance of this market. While specific market share data varies by segment, key players like Amcor Group GmbH and Berry Global Group hold substantial positions.

- Market Concentration: Moderately concentrated, with significant influence from top players.

- Innovation Drivers: Enhanced barrier properties, sustainability, cost optimization, consumer demand for convenience.

- Regulatory Frameworks: Increasing focus on recyclability, waste reduction, and sustainable materials.

- Product Substitutes: Limited but growing, particularly from paper and compostable alternatives.

- End-User Demographics: Growing demand for convenience, health-conscious packaging, and eco-friendly solutions.

- M&A Activities: Strategic consolidation, technology acquisition, and market expansion.

North America Plastic Film Packaging Market Market Dynamics & Trends

The North America Plastic Film Packaging Market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.5% from 2025 to 2033. This growth is primarily fueled by an escalating demand for convenient and safe packaging solutions across diverse end-user industries, most notably the food and beverage sector. The increasing global population, coupled with rising disposable incomes, has spurred consumption of packaged goods, thereby driving the demand for plastic films. Technological disruptions, including advancements in polymer science and manufacturing processes, are enabling the development of films with superior barrier properties, extended shelf life, and improved printability. This innovation allows for better product preservation, reduced food waste, and enhanced brand visibility. Consumer preferences are continuously shifting towards lightweight, durable, and aesthetically appealing packaging. The convenience offered by flexible plastic films in terms of ease of opening, resealability, and portion control aligns perfectly with modern lifestyles. Furthermore, the ongoing emphasis on sustainability is compelling manufacturers to invest in the development of recyclable, compostable, and bio-based plastic films, thereby opening new avenues for market penetration. The competitive dynamics within the market are characterized by intense price competition, a focus on product differentiation, and strategic partnerships aimed at enhancing market reach and technological capabilities. The market penetration of specialized films, such as those with advanced barrier properties for sensitive products like fresh produce and pharmaceuticals, is also on the rise. The overall market size is estimated to reach over $60 billion by 2025, with continuous upward trajectory expected during the forecast period.

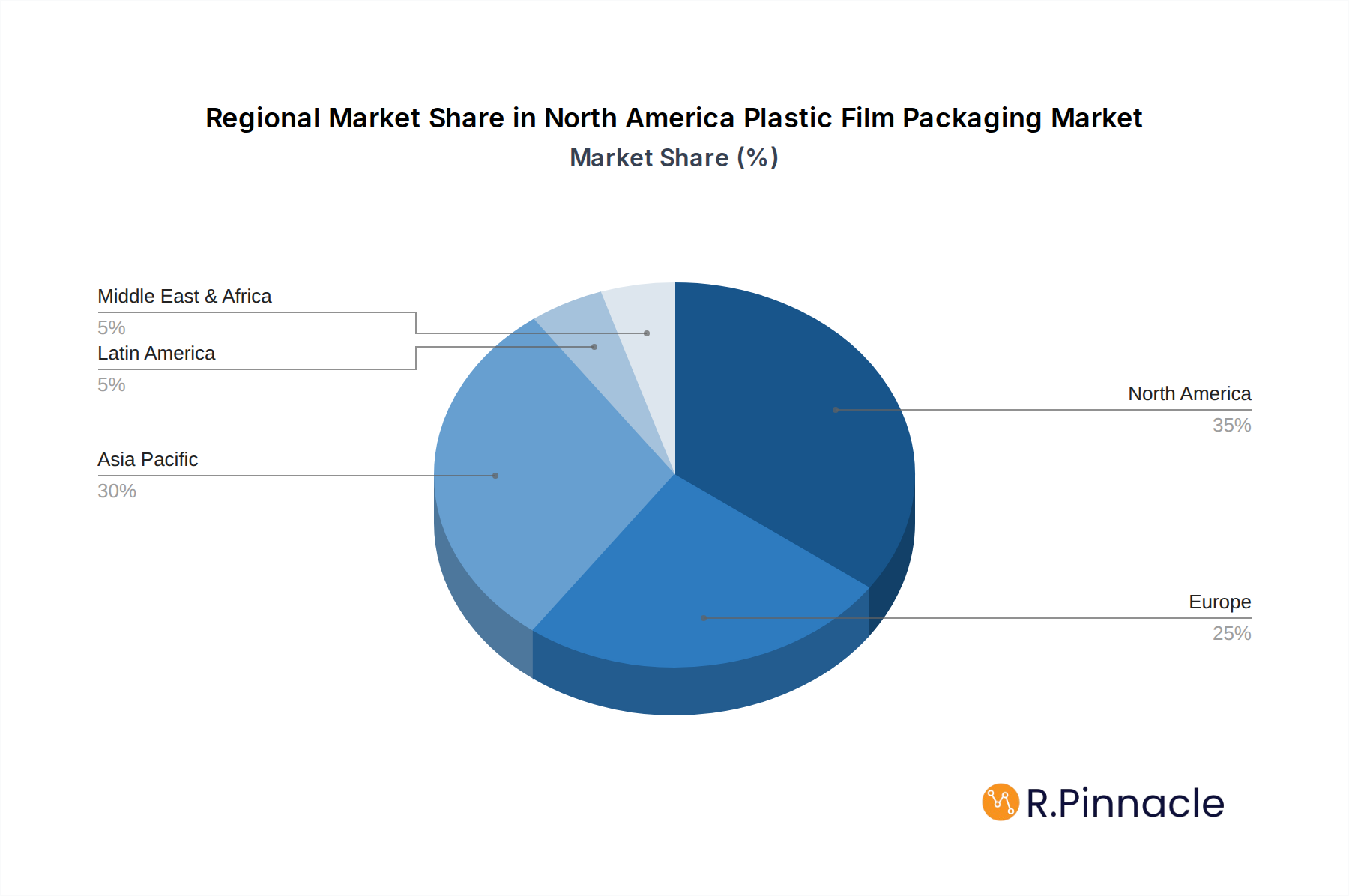

Dominant Regions & Segments in North America Plastic Film Packaging Market

The United States continues to dominate the North America Plastic Film Packaging Market, driven by its large consumer base, sophisticated manufacturing sector, and strong demand from the food and healthcare industries. Canada and Mexico also represent significant markets, with their respective economic growth and industrial development contributing to market expansion.

Within the Type segmentation, Polyethylene (PE) films, encompassing both low-density (LDPE) and high-density (HDPE) variants, hold the largest market share. This dominance is attributed to their versatility, cost-effectiveness, and excellent barrier properties, making them suitable for a wide range of applications from food packaging to industrial wrapping. Polypropylene (PP) films follow closely, particularly biaxially oriented polypropylene (BOPP) films, which offer superior clarity, stiffness, and printability, making them ideal for confectionery, snack, and bakery packaging. PETG films are gaining traction due to their excellent clarity and impact resistance, finding applications in specialized packaging where visual appeal and durability are paramount. Bio-Based films, while currently a smaller segment, are experiencing rapid growth driven by increasing environmental consciousness and regulatory support for sustainable alternatives. PVC and EVOH films are crucial for applications requiring high barrier properties against oxygen and moisture, respectively, and are vital in the packaging of sensitive food items and medical devices. Polystyrene films cater to specific needs for rigidity and clarity in certain packaging formats.

The End-User Industry segmentation is spearheaded by Food packaging, which accounts for the largest share. This segment is further subdivided into numerous sub-segments:

- Candy & Confectionery: High demand for visually appealing and barrier-protected films to maintain freshness and texture.

- Frozen Foods: Requires films with excellent low-temperature performance and moisture resistance.

- Fresh Produce: Growing demand for modified atmosphere packaging (MAP) films that extend shelf life and reduce spoilage.

- Dairy Products: Needs films offering excellent barrier properties against oxygen and light.

- Dry Foods: Benefits from films that provide moisture protection and extend shelf life.

- Meat, Poultry, And Seafood: Requires advanced barrier films to prevent oxidation and microbial growth.

- Pet Food: Increasing demand for durable and high-barrier packaging to maintain palatability and freshness.

- Other Foods: Encompasses a broad range of products requiring tailored film solutions.

The Healthcare sector is another significant contributor, with plastic films used for pharmaceutical packaging, medical device pouches, and sterile barrier systems, demanding high levels of purity and barrier protection. Personal Care & Home Care applications leverage plastic films for packaging of cosmetics, toiletries, detergents, and cleaning products, emphasizing aesthetics and functionality. Industrial Packaging utilizes films for pallet wrapping, protective coverings, and component packaging, where strength and durability are key.

- Dominant Region: United States.

- Leading Film Types: Polyethylene (PE), Polypropylene (PP), PETG.

- Fastest Growing Film Type: Bio-Based.

- Dominant End-User Industry: Food.

- Key Food Sub-segments: Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products.

- Other Key End-User Industries: Healthcare, Personal Care & Home Care.

- Key Drivers for Regional Dominance: Large consumer base, strong manufacturing, industry demand.

- Key Drivers for Segment Dominance: Versatility, cost-effectiveness, barrier properties, consumer demand, regulatory support.

North America Plastic Film Packaging Market Product Innovations

Product innovation in the North America Plastic Film Packaging Market is rapidly advancing, focusing on delivering superior performance and sustainability. Manufacturers are developing advanced barrier films, such as those with metallized or co-extruded layers, to significantly extend the shelf life of perishable goods and reduce food waste. The introduction of 'B-UUB-M' Outstanding Barrier Metallized BOPP Film by UFlex is a prime example, catering to a wide array of dry goods and snacks with enhanced protection. Furthermore, there's a strong push towards thinner, yet stronger, films that reduce material consumption without compromising on durability. The development of films with improved heat-sealability and puncture resistance also enhances operational efficiency for converters and end-users. The market is also witnessing innovations in printable films with enhanced graphics capabilities and the integration of smart features like indicators for freshness or temperature.

Report Scope & Segmentation Analysis

This report meticulously analyzes the North America Plastic Film Packaging Market across its diverse segments. The Type segmentation includes Polyprop (Polypropylene), Polyethy (Polyethylene - LDPE, HDPE, LLDPE), Polystyrene, Bio-Based, PVC, EVOH, PETG, and Other Film Types. Market sizes and growth projections are detailed for each, with Polyethylene and Polypropylene expected to maintain their leading positions while Bio-Based films are projected for significant expansion, reaching an estimated market size of over $2 billion by 2033. The End-User Industry segmentation covers Food (further broken down into Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Fo), Healthcare, Personal Care & Home Care, Industrial Packaging, and Other En. The Food segment is expected to continue its dominance, driven by increasing consumption and demand for extended shelf life, projected to cross $35 billion by 2033. Healthcare applications are also anticipated for steady growth due to stringent packaging requirements and rising healthcare spending.

- Type Segmentation: Polyprop, Polyethy, Polystyrene, Bio-Based, PVC, EVOH, PETG, and Other Film Types. Growth in Bio-Based films is expected to be significant.

- End-User Industry Segmentation: Food (with numerous sub-segments), Healthcare, Personal Care & Home Care, Industrial Packaging, Other En. The Food segment leads, with Healthcare and Personal Care showing strong growth potential.

Key Drivers of North America Plastic Film Packaging Market Growth

The North America Plastic Film Packaging Market is propelled by several key drivers. The ever-increasing global demand for convenience and shelf-stable food products, coupled with a growing population, significantly boosts the need for effective plastic film packaging. Advancements in material science and manufacturing technologies are enabling the creation of higher-performance films with superior barrier properties, extended shelf life, and enhanced durability, directly addressing consumer and industry needs. Furthermore, the inherent cost-effectiveness and versatility of plastic films make them an attractive packaging solution across various sectors, from food and healthcare to personal care. Growing e-commerce activities also necessitate robust and lightweight packaging for safe transit, further fueling market expansion. The trend towards sustainable packaging, with an increasing focus on recyclability and the development of bio-based alternatives, is also creating new opportunities and driving innovation.

Challenges in the North America Plastic Film Packaging Market Sector

Despite its growth trajectory, the North America Plastic Film Packaging Market faces several challenges. Growing environmental concerns and stringent regulations regarding plastic waste and pollution are creating significant pressure on the industry to adopt more sustainable practices. Public perception and increasing demand for eco-friendly alternatives can impact the market share of traditional plastic films. Supply chain disruptions, including volatile raw material prices and availability, can affect production costs and lead times, impacting profitability and market stability. The competitive landscape is also intense, with numerous players vying for market share, leading to price pressures and the need for continuous innovation to maintain a competitive edge. Developing cost-effective and scalable solutions for the recycling and end-of-life management of flexible plastic films remains a critical challenge.

Emerging Opportunities in North America Plastic Film Packaging Market

The North America Plastic Film Packaging Market is ripe with emerging opportunities. The burgeoning demand for sustainable packaging solutions presents a significant growth avenue for manufacturers developing and producing bio-based, compostable, and highly recyclable plastic films. Innovations in smart packaging, incorporating features like active oxygen absorbers, moisture regulators, and antimicrobial agents, offer enhanced product protection and extended shelf life, particularly in the food and healthcare sectors. The expanding e-commerce market necessitates the development of lightweight, durable, and tamper-evident packaging films, creating new application areas. Furthermore, the increasing focus on health and wellness is driving the demand for specialized packaging for nutraceuticals, functional foods, and sensitive healthcare products, requiring advanced barrier properties and sterile solutions. Investments in advanced recycling technologies and infrastructure to improve the circularity of plastic films also represent a substantial opportunity for innovation and market leadership.

Leading Players in the North America Plastic Film Packaging Market Market

- Profol Americas Inc

- TEKRA LLC (A Mativ Brand)

- Cosmo Films Inc

- Taghleef Industries Inc

- Flex Films (USA) Inc (UFlex Limited)

- Klockner Pentaplast Group

- Tara Plastics Corporation (A Part of Sigma Plastic Group)

- Berry Global Group

- Jindal Films (Jindal Films Europe S A R L)

- Winpak Ltd

- Amcor Group GmbH

- Innovia Films (CCL Industries Inc )

- SUDPACK Holding Gmb

Key Developments in North America Plastic Film Packaging Market Industry

- May 2024: UFlex, a flexible packaging manufacturer with operations in the United States, launched its offerings in the final quarter of FY 2024. The company introduced new products specifically designed for both labels and flexible packaging. UFlex's packaging films division notably rolled out the 'B-UUB-M' Outstanding Barrier Metallized BOPP Film. This innovative film is crafted to cater to various products, including dry fruits, beverages, chips, snacks, biscuits, cookies, confectionery, and chocolate items.

- March 2024: The Plastics Industry Association (PLASTICS) launched the Flexible Film Recycling Alliance (FFRA) to boost recycling rates, improve access, and educate the public on flexible plastic film products in the United States. FFRA's primary goal is to tackle the hurdles of recycling flexible films and bags by uniting stakeholders from the entire supply chain.

Future Outlook for North America Plastic Film Packaging Market Market

The future outlook for the North America Plastic Film Packaging Market remains exceptionally positive, driven by sustained demand from its core end-user industries and a continuous stream of technological advancements. The market is poised for further growth, with an anticipated expansion of over $30 billion in market value during the forecast period, reaching an estimated value exceeding $90 billion by 2033. The increasing emphasis on sustainability will undoubtedly shape the market's evolution, leading to greater adoption of recycled content, bio-based materials, and improved recyclability of existing film structures. Innovations in high-barrier films, active and intelligent packaging, and specialized films for niche applications will continue to drive value and create new market segments. Strategic collaborations, investments in R&D, and a focus on circular economy principles will be crucial for players aiming to maintain a competitive edge and capitalize on the evolving landscape of plastic film packaging.

North America Plastic Film Packaging Market Segmentation

-

1. Type

- 1.1. Polyprop

- 1.2. Polyethy

- 1.3. Polyethy

- 1.4. Polystyrene

- 1.5. Bio-Based

- 1.6. PVC, EVOH, PETG, and Other Film Types

-

2. End-User Industry

-

2.1. Food

- 2.1.1. Candy & Confectionery

- 2.1.2. Frozen Foods

- 2.1.3. Fresh Produce

- 2.1.4. Dairy Products

- 2.1.5. Dry Foods

- 2.1.6. Meat, Poultry, And Seafood

- 2.1.7. Pet Food

- 2.1.8. Other Fo

- 2.2. Healthcare

- 2.3. Personal Care & Home Care

- 2.4. Industrial Packaging

- 2.5. Other En

-

2.1. Food

North America Plastic Film Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Plastic Film Packaging Market Regional Market Share

Geographic Coverage of North America Plastic Film Packaging Market

North America Plastic Film Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Polyprop

- 5.1.2. Polyethy

- 5.1.3. Polyethy

- 5.1.4. Polystyrene

- 5.1.5. Bio-Based

- 5.1.6. PVC, EVOH, PETG, and Other Film Types

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Food

- 5.2.1.1. Candy & Confectionery

- 5.2.1.2. Frozen Foods

- 5.2.1.3. Fresh Produce

- 5.2.1.4. Dairy Products

- 5.2.1.5. Dry Foods

- 5.2.1.6. Meat, Poultry, And Seafood

- 5.2.1.7. Pet Food

- 5.2.1.8. Other Fo

- 5.2.2. Healthcare

- 5.2.3. Personal Care & Home Care

- 5.2.4. Industrial Packaging

- 5.2.5. Other En

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Plastic Film Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Polyprop

- 6.1.2. Polyethy

- 6.1.3. Polyethy

- 6.1.4. Polystyrene

- 6.1.5. Bio-Based

- 6.1.6. PVC, EVOH, PETG, and Other Film Types

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Food

- 6.2.1.1. Candy & Confectionery

- 6.2.1.2. Frozen Foods

- 6.2.1.3. Fresh Produce

- 6.2.1.4. Dairy Products

- 6.2.1.5. Dry Foods

- 6.2.1.6. Meat, Poultry, And Seafood

- 6.2.1.7. Pet Food

- 6.2.1.8. Other Fo

- 6.2.2. Healthcare

- 6.2.3. Personal Care & Home Care

- 6.2.4. Industrial Packaging

- 6.2.5. Other En

- 6.2.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Profol Americas Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TEKRA LLC (A Mativ Brand)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cosmo Films Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Taghleef Industries Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Flex Films (USA) Inc (UFlex Limited)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Klockner Pentaplast Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Tara Plastics Corporation (A Part of Sigma Plastic Group)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Berry Global Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jindal Films (Jindal Films Europe S A R L)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Winpak Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Amcor Group GmbH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Innovia Films (CCL Industries Inc )

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 SUDPACK Holding Gmb

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Profol Americas Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Plastic Film Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Plastic Film Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: North America Plastic Film Packaging Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Plastic Film Packaging Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 3: North America Plastic Film Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Plastic Film Packaging Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: North America Plastic Film Packaging Market Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: North America Plastic Film Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Plastic Film Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Plastic Film Packaging Market?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the North America Plastic Film Packaging Market?

Key companies in the market include Profol Americas Inc, TEKRA LLC (A Mativ Brand), Cosmo Films Inc, Taghleef Industries Inc, Flex Films (USA) Inc (UFlex Limited), Klockner Pentaplast Group, Tara Plastics Corporation (A Part of Sigma Plastic Group), Berry Global Group, Jindal Films (Jindal Films Europe S A R L), Winpak Ltd, Amcor Group GmbH, Innovia Films (CCL Industries Inc ), SUDPACK Holding Gmb.

3. What are the main segments of the North America Plastic Film Packaging Market?

The market segments include Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 293.92 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Convenient Packaging.

6. What are the notable trends driving market growth?

Polyethylene Film Is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Increased Demand for Convenient Packaging.

8. Can you provide examples of recent developments in the market?

May 2024: UFlex, a flexible packaging manufacturer with operations in the United States, launched its offerings in the final quarter of FY 2024. The company introduced new products specifically designed for both labels and flexible packaging. UFlex's packaging films division notably rolled out the 'B-UUB-M' Outstanding Barrier Metallized BOPP Film. This innovative film is crafted to cater to various products, including dry fruits, beverages, chips, snacks, biscuits, cookies, confectionery, and chocolate items.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Plastic Film Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Plastic Film Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Plastic Film Packaging Market?

To stay informed about further developments, trends, and reports in the North America Plastic Film Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence