Key Insights

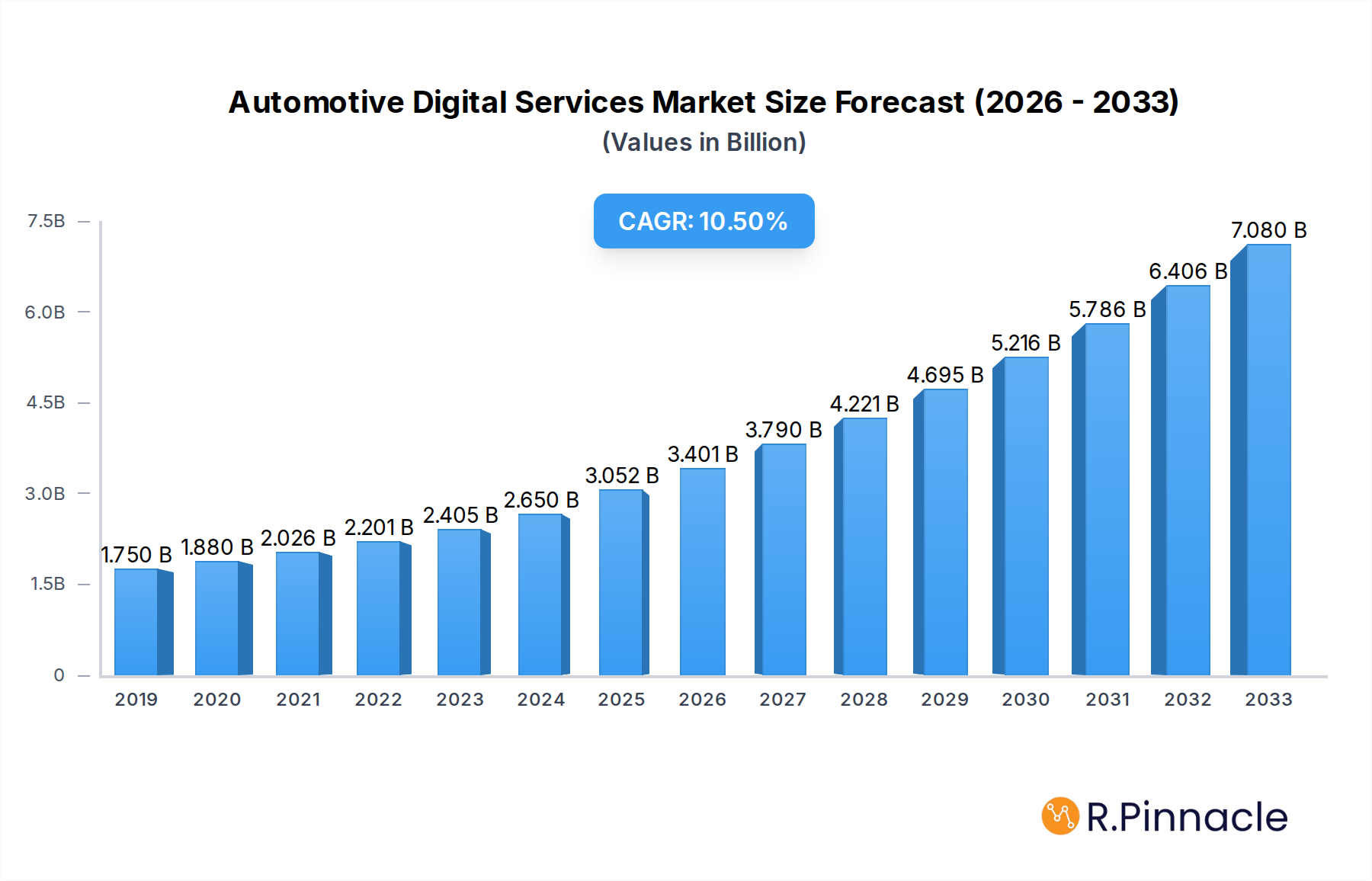

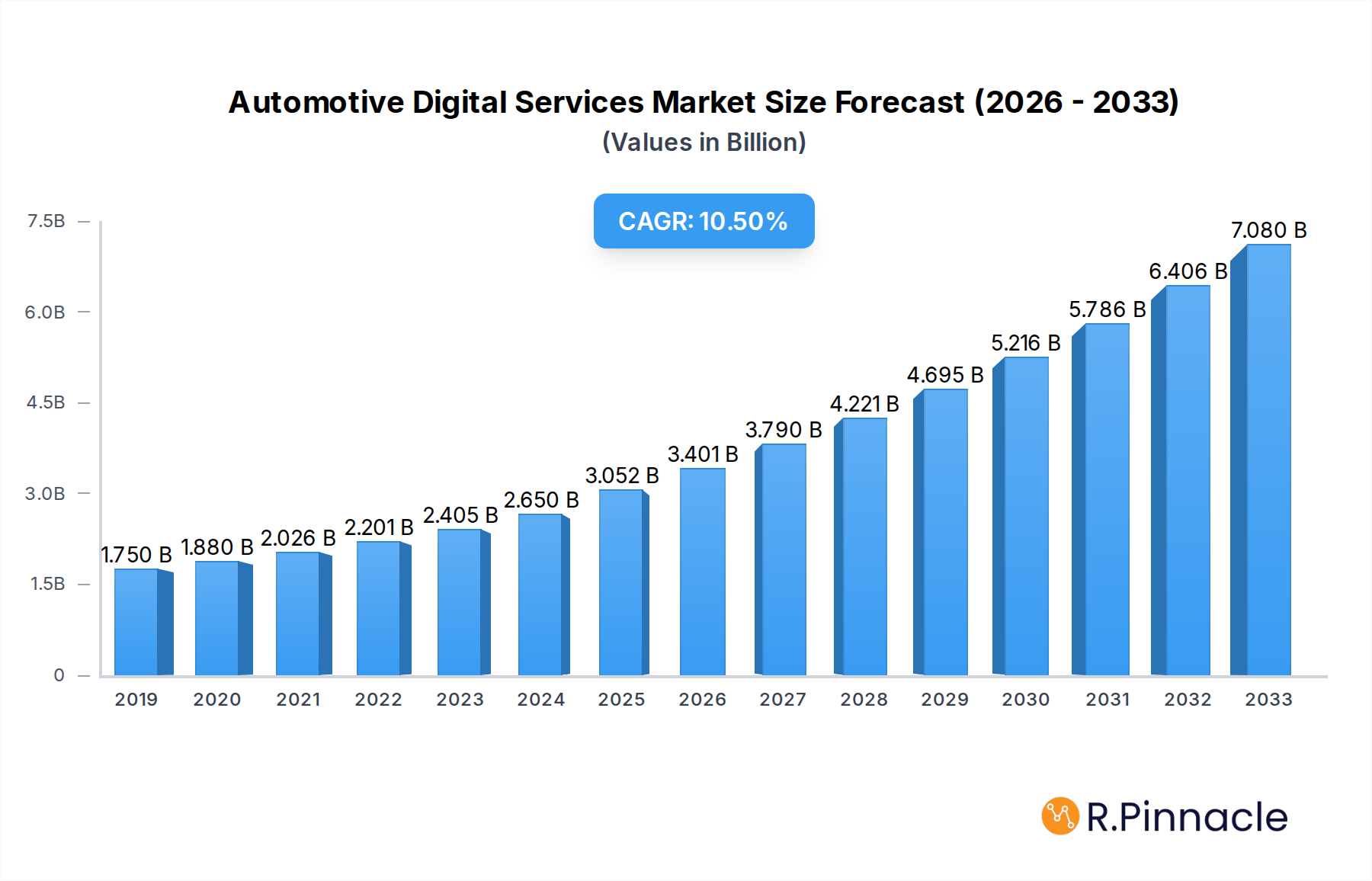

The global Automotive Digital Services market is poised for significant expansion, projected to reach an impressive $3052.4 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 10.9% throughout the forecast period. This remarkable growth is underpinned by several key drivers that are reshaping the automotive landscape. The increasing adoption of connected car technologies, fueled by advancements in IoT, 5G connectivity, and artificial intelligence, is paramount. Consumers' escalating demand for seamless, personalized, and convenient in-car experiences, including advanced infotainment, navigation, and driver assistance systems, is also a major catalyst. Furthermore, the burgeoning autonomous driving sector, which heavily relies on sophisticated digital services for perception, decision-making, and communication, is contributing substantially. The growing emphasis on fleet management optimization and the rise of mobility-as-a-service (MaaS) platforms further bolster market growth by creating new avenues for digital service integration and revenue generation.

Automotive Digital Services Market Size (In Billion)

The market segmentation reveals diverse opportunities across various applications and service types. The "Customer" segment is expected to lead, reflecting the direct impact of enhanced user experiences on vehicle adoption and loyalty. Automobile Manufacturers are investing heavily in digital services to differentiate their offerings and build brand value. Automobile Service Providers are leveraging digital solutions for predictive maintenance, remote diagnostics, and improved customer engagement. Transportation Management Companies are utilizing these services for enhanced operational efficiency, route optimization, and real-time tracking. Mobility on Demand Services are intrinsically linked to digital platforms for booking, payment, and service delivery. Logistic Fleet Management Services are benefiting from the digital transformation to improve asset utilization and supply chain visibility. In-vehicle Digital Services, encompassing everything from entertainment to advanced safety features, are becoming a core component of vehicle value. Key players like Uber Technologies, Daimler, Bosch, and Volkswagen are actively innovating and expanding their digital service portfolios, indicating a highly competitive yet dynamic market.

Automotive Digital Services Company Market Share

This comprehensive report dives deep into the burgeoning Automotive Digital Services market, offering unparalleled insights and actionable intelligence for industry stakeholders. With a study period spanning 2019–2033, and building upon a robust base year of 2025, this research provides critical forecasts for the 2025–2033 period, informed by historical data from 2019–2024. We meticulously analyze the dynamic landscape of mobility on demand services, logistic fleet management services, and in-vehicle digital services, examining their impact across diverse applications including Customer, Automobile Manufacturer, Automobile Service Provider, Transportation Management Company, and Other segments.

Automotive Digital Services Market Structure & Innovation Trends

The automotive digital services market exhibits a moderate concentration, with key players like Uber Technologies, Daimler, Bosch, TomTom, FEV Group, MAN, PCG, Continental, Bayerische Motoren Werke (BMW) Group, and Volkswagen driving innovation and capturing significant market share. Innovation is primarily fueled by advancements in Artificial Intelligence (AI), the Internet of Things (IoT), 5G connectivity, and data analytics, leading to the development of sophisticated in-vehicle digital services and advanced logistic fleet management services. Regulatory frameworks are evolving to address data privacy, cybersecurity, and autonomous driving integration, presenting both opportunities and challenges. Product substitutes are emerging, particularly in the form of integrated software solutions and platform-based services that offer enhanced functionalities. End-user demographics are shifting towards tech-savvy consumers and businesses demanding seamless, connected experiences. Mergers and acquisitions (M&A) activity is robust, with significant deal values, such as the estimated acquisition of a leading telematics provider for over 500 million by a major automotive OEM, indicating strategic consolidation. The market share of mobility on demand services is projected to reach over 70% of the total digital services market by 2030.

Automotive Digital Services Market Dynamics & Trends

The automotive digital services market is poised for substantial growth, driven by an escalating demand for connected car technologies, enhanced user experiences, and efficient operational management. The projected Compound Annual Growth Rate (CAGR) for the forecast period is an impressive 18.5%, with the market size anticipated to surge from an estimated 700 million in 2025 to over 2.5 billion by 2033. This expansion is underpinned by several key trends. Firstly, the increasing penetration of smartphones and the growing consumer expectation for integrated digital ecosystems are compelling automotive manufacturers to embed sophisticated in-vehicle digital services such as infotainment systems, navigation, and remote diagnostics. Secondly, the burgeoning e-commerce and logistics sectors are fueling the demand for advanced logistic fleet management services, enabling real-time tracking, route optimization, and predictive maintenance, thereby enhancing operational efficiency for businesses. Thirdly, the rise of the mobility on demand service sector, exemplified by ride-sharing and car-sharing platforms, continues to reshape personal transportation, making digital services indispensable for seamless booking, payment, and user management. Technological disruptions, including the widespread adoption of 5G, edge computing, and AI, are enabling more responsive and personalized digital services. Furthermore, evolving consumer preferences, such as a growing interest in subscription-based models for digital features and a demand for over-the-air (OTA) updates, are compelling manufacturers to innovate rapidly. Competitive dynamics are intense, with traditional automotive players, tech giants, and specialized service providers vying for market dominance through strategic partnerships and product differentiation. The market penetration of connected vehicles is expected to exceed 90% by 2030, creating a fertile ground for digital service adoption.

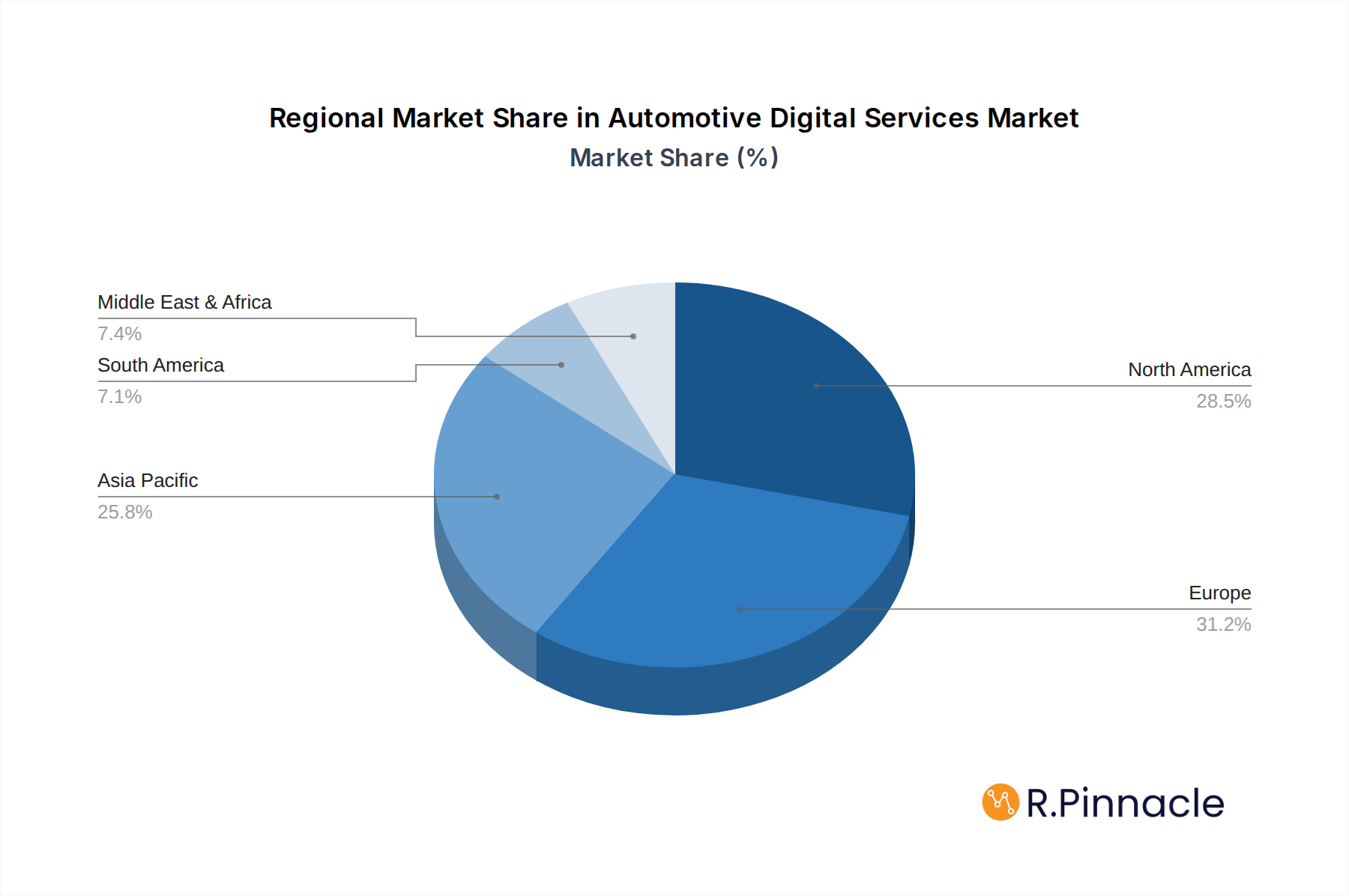

Dominant Regions & Segments in Automotive Digital Services

North America currently stands as the dominant region in the automotive digital services market, driven by a strong adoption rate of advanced technologies, a mature automotive industry, and favorable economic policies. The United States, in particular, leads with significant investments in connected vehicle infrastructure and a large consumer base receptive to innovative digital solutions. Economic policies promoting technological innovation and government initiatives supporting smart city development further bolster market growth.

Key Drivers in North America:

- High disposable income: Facilitating consumer adoption of premium digital services.

- Advanced technological infrastructure: Including widespread 4G/5G network coverage.

- Strong presence of key players: Such as Uber Technologies and Continental, fostering competition and innovation.

- Supportive regulatory environment: For autonomous driving and data-driven services.

In terms of application segments, Automobile Manufacturers are major stakeholders, actively developing and integrating a wide array of in-vehicle digital services to enhance customer experience and create new revenue streams. This segment is projected to account for over 40% of the total market value by 2030. The drive towards software-defined vehicles and the increasing reliance on data analytics for product development and maintenance solidify their dominance.

Within the Types segmentation, In-vehicle Digital Services are experiencing the most significant expansion, encompassing everything from advanced navigation and infotainment systems to predictive maintenance alerts and personalized driver assistance features. The market share for this segment is expected to reach over 50% by 2028. The integration of AI and machine learning further enhances the capabilities and appeal of these services, offering a truly connected and intelligent driving experience.

The Transportation Management Company segment is also a crucial growth driver, particularly for Logistic Fleet Management Services. Companies are leveraging these services for optimizing delivery routes, monitoring driver behavior, and improving overall fleet efficiency, leading to significant cost savings and enhanced customer satisfaction. This segment is projected to witness a CAGR of 17.8% during the forecast period.

Automotive Digital Services Product Innovations

Product innovations in automotive digital services are rapidly transforming the driving experience. Advanced AI-powered driver-assistance systems (ADAS), predictive maintenance platforms utilizing IoT sensors, and seamless integration of in-car infotainment with personal digital ecosystems are key developments. These innovations offer enhanced safety, convenience, and efficiency, providing significant competitive advantages for manufacturers and service providers. The focus is on creating personalized, intuitive, and highly connected automotive experiences.

Report Scope & Segmentation Analysis

This report meticulously segments the automotive digital services market by Application and Types. The Application segments include Customer, Automobile Manufacturer, Automobile Service Provider, Transportation Management Company, and Other. The Types segments are Mobility on Demand Service, Logistic Fleet Management Service, In-vehicle Digital Service, and Other. Each segment is analyzed for its market size, growth projections, and competitive dynamics. For instance, the In-vehicle Digital Service segment is projected to grow at a CAGR of 19.2% and reach over 1.2 billion by 2033, driven by increasing adoption of connected car technologies by Automobile Manufacturers.

Key Drivers of Automotive Digital Services Growth

The exponential growth of the automotive digital services market is propelled by a confluence of technological advancements, evolving consumer demands, and strategic industry investments. The proliferation of high-speed internet connectivity, particularly 5G networks, is a foundational element, enabling real-time data exchange and the deployment of sophisticated in-vehicle digital services. Growing consumer expectations for seamless connectivity, personalized experiences, and on-demand services are compelling manufacturers to invest heavily in digital solutions. Furthermore, the increasing emphasis on operational efficiency and cost reduction within the logistics sector is driving the adoption of advanced logistic fleet management services. Regulatory support for smart mobility initiatives and autonomous driving technologies also acts as a significant catalyst, encouraging innovation and market expansion.

Challenges in the Automotive Digital Services Sector

Despite the promising growth trajectory, the automotive digital services sector faces notable challenges. Cybersecurity threats pose a significant risk, with the potential for data breaches and disruption of critical vehicle functions. Ensuring robust data privacy and compliance with evolving regulations, such as GDPR, is paramount. Interoperability issues between different platforms and systems can hinder seamless integration and user experience. The high cost of developing and implementing advanced digital solutions can also be a barrier for smaller players. Furthermore, consumer adoption rates for certain advanced services may vary due to awareness, affordability, and perceived value, requiring strategic marketing and educational efforts. The supply chain for critical components, such as advanced semiconductors, can also experience disruptions, impacting production timelines and service availability.

Emerging Opportunities in Automotive Digital Services

The automotive digital services market is ripe with emerging opportunities. The expansion of mobility on demand service platforms into new geographic markets and the integration of new service offerings, such as autonomous ride-hailing, represent significant growth avenues. The increasing demand for sustainable transportation solutions is driving the development of digital services that optimize electric vehicle (EV) charging infrastructure and battery management. The integration of augmented reality (AR) and virtual reality (VR) into in-vehicle digital services for enhanced navigation and driver training is another promising frontier. Furthermore, the growing focus on data monetization and the development of personalized insurance products based on driver behavior analysis are opening up new revenue streams for companies in this sector. The development of specialized digital services for commercial fleets, focusing on areas like predictive maintenance and driver safety, also presents substantial potential.

Leading Players in the Automotive Digital Services Market

- Uber Technologies

- Daimler

- Bosch

- TomTom

- FEV Group

- MAN

- PCG

- Continental

- Bayerische Motoren Werke (BMW) Group

- Volkswagen

Key Developments in Automotive Digital Services Industry

- 2023 Q4: Bosch announces strategic partnership with a major cloud provider to enhance its connected vehicle services platform, focusing on data analytics and IoT integration.

- 2024 Q1: Continental invests over 150 million in a startup specializing in advanced driver-assistance systems (ADAS) to bolster its portfolio of in-vehicle digital services.

- 2024 Q2: Volkswagen launches its new 'Car-Net' digital services suite, offering enhanced infotainment, navigation, and remote vehicle control features for its global fleet.

- 2024 Q3: Uber Technologies expands its mobility on demand service offerings to include premium ride options in key European cities, projecting a 10% increase in average revenue per user.

- 2024 Q4: MAN unveils its next-generation logistic fleet management service, incorporating AI-powered route optimization and real-time predictive maintenance, aiming to reduce operational costs by 12% for its clients.

Future Outlook for Automotive Digital Services Market

The future outlook for the automotive digital services market is exceptionally bright, driven by continuous innovation and expanding consumer adoption. The transition towards software-defined vehicles will further cement the importance of digital services, creating recurring revenue streams for manufacturers and offering unparalleled personalization for users. The integration of AI and machine learning will lead to more intelligent and proactive services, enhancing safety, comfort, and efficiency. As connectivity becomes ubiquitous and autonomous driving technologies mature, the demand for sophisticated in-vehicle digital services and integrated mobility solutions will surge. Strategic partnerships and acquisitions are expected to continue shaping the competitive landscape, with a growing emphasis on data analytics, cybersecurity, and the development of comprehensive digital ecosystems that cater to the evolving needs of drivers and fleet operators. The market is projected to experience sustained high growth rates, presenting significant opportunities for all stakeholders involved.

Automotive Digital Services Segmentation

-

1. Application

- 1.1. Customer

- 1.2. Automobile Manufacturer

- 1.3. Automobile Service Provider

- 1.4. Transportation Management Company

- 1.5. Other

-

2. Types

- 2.1. Mobility on Demand Service

- 2.2. Logistic Fleet Management Service

- 2.3. In-vehicle Digital Service

- 2.4. Other

Automotive Digital Services Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Digital Services Regional Market Share

Geographic Coverage of Automotive Digital Services

Automotive Digital Services REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Customer

- 5.1.2. Automobile Manufacturer

- 5.1.3. Automobile Service Provider

- 5.1.4. Transportation Management Company

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mobility on Demand Service

- 5.2.2. Logistic Fleet Management Service

- 5.2.3. In-vehicle Digital Service

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Customer

- 6.1.2. Automobile Manufacturer

- 6.1.3. Automobile Service Provider

- 6.1.4. Transportation Management Company

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mobility on Demand Service

- 6.2.2. Logistic Fleet Management Service

- 6.2.3. In-vehicle Digital Service

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Customer

- 7.1.2. Automobile Manufacturer

- 7.1.3. Automobile Service Provider

- 7.1.4. Transportation Management Company

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mobility on Demand Service

- 7.2.2. Logistic Fleet Management Service

- 7.2.3. In-vehicle Digital Service

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Customer

- 8.1.2. Automobile Manufacturer

- 8.1.3. Automobile Service Provider

- 8.1.4. Transportation Management Company

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mobility on Demand Service

- 8.2.2. Logistic Fleet Management Service

- 8.2.3. In-vehicle Digital Service

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Customer

- 9.1.2. Automobile Manufacturer

- 9.1.3. Automobile Service Provider

- 9.1.4. Transportation Management Company

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mobility on Demand Service

- 9.2.2. Logistic Fleet Management Service

- 9.2.3. In-vehicle Digital Service

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Digital Services Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Customer

- 10.1.2. Automobile Manufacturer

- 10.1.3. Automobile Service Provider

- 10.1.4. Transportation Management Company

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mobility on Demand Service

- 10.2.2. Logistic Fleet Management Service

- 10.2.3. In-vehicle Digital Service

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Uber Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Daimler

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Bosch

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TomTom

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 FEV Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MAN

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 PCG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Continental

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Bayerische Motoren Werke (BMW) Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Volkswagen

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Uber Technologies

List of Figures

- Figure 1: Global Automotive Digital Services Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Digital Services Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Digital Services Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Digital Services Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Digital Services Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Digital Services Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Digital Services Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Digital Services Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Digital Services Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Digital Services Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Digital Services Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Digital Services Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Digital Services Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Digital Services Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Digital Services Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Digital Services Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Digital Services Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Digital Services Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Digital Services Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Digital Services Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Digital Services Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Digital Services Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Digital Services Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Digital Services Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Digital Services Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Digital Services Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Digital Services Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Digital Services Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Digital Services Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Digital Services Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Digital Services Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Digital Services Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Digital Services Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Digital Services Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Digital Services Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Digital Services Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Digital Services Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Digital Services Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Digital Services Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Digital Services Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Digital Services?

The projected CAGR is approximately 10.9%.

2. Which companies are prominent players in the Automotive Digital Services?

Key companies in the market include Uber Technologies, Daimler, Bosch, TomTom, FEV Group, MAN, PCG, Continental, Bayerische Motoren Werke (BMW) Group, Volkswagen.

3. What are the main segments of the Automotive Digital Services?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3052.4 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Digital Services," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Digital Services report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Digital Services?

To stay informed about further developments, trends, and reports in the Automotive Digital Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence