Key Insights

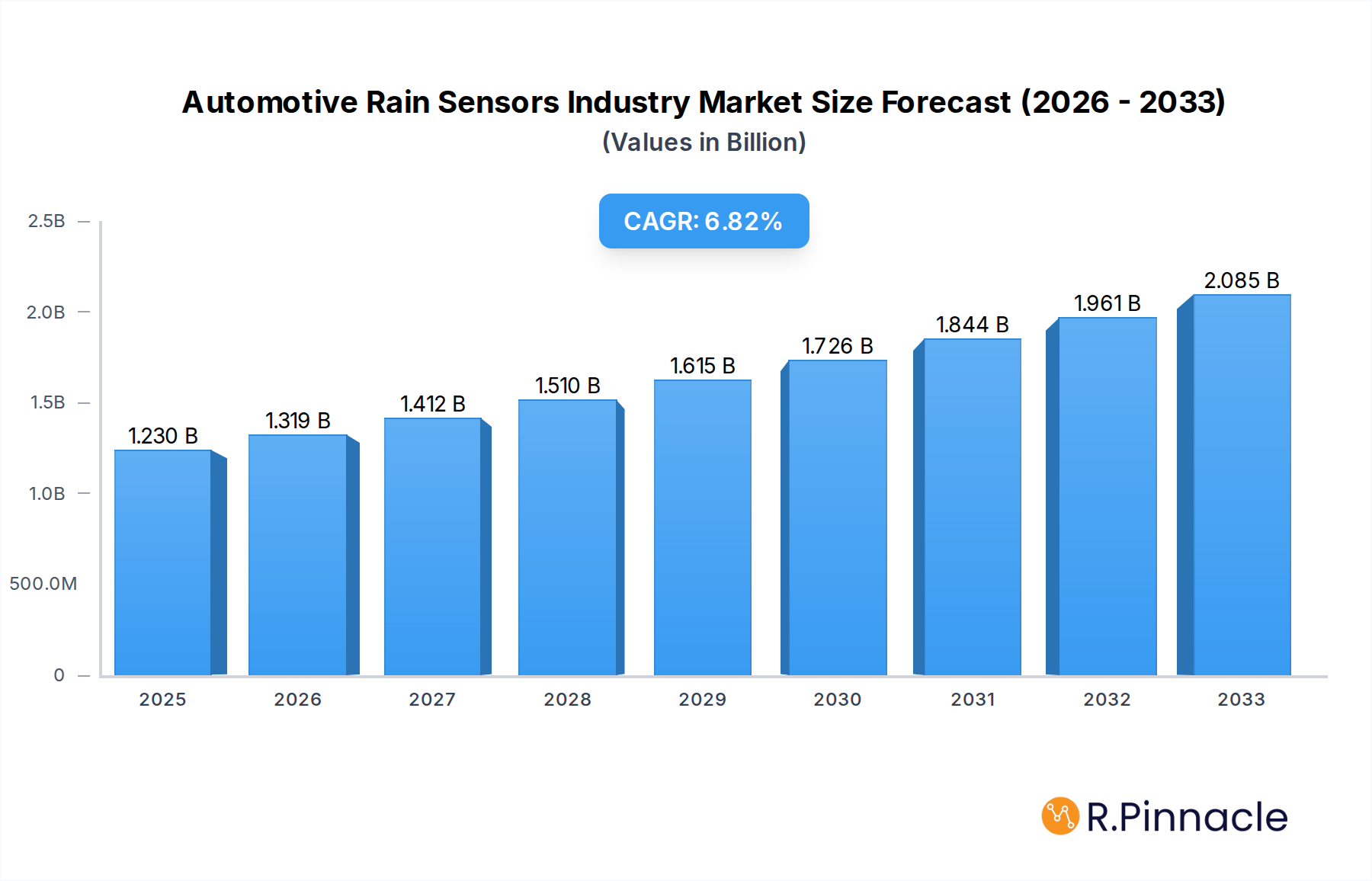

The global Automotive Rain Sensors market is poised for significant expansion, projected to reach a substantial $1.23 Billion by 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 7.20%, indicating a dynamic and evolving industry landscape. The increasing integration of advanced driver-assistance systems (ADAS) and the growing consumer demand for enhanced vehicle safety and convenience are primary market drivers. As automotive manufacturers strive to differentiate their offerings and meet stringent safety regulations, the adoption of rain sensors, which automate windshield wiper operation and enhance visibility during adverse weather, is becoming a standard feature rather than a luxury. The market is segmented into Passenger Cars and Commercial Vehicles, with passenger cars currently dominating due to higher production volumes and a faster adoption rate of new technologies. However, the commercial vehicle segment is expected to witness accelerated growth as fleet operators recognize the safety and operational benefits of these sensors in reducing accidents and improving driver comfort.

Automotive Rain Sensors Industry Market Size (In Billion)

Further fueling market expansion are technological advancements, such as the development of more sophisticated optical and infrared-based rain sensors that offer higher accuracy and reliability. The increasing focus on autonomous driving technology also indirectly benefits the rain sensor market, as these sensors play a crucial role in providing environmental data to the vehicle's central processing unit. Key players like Denso Corporation, Valeo Group, and ams-OSRAM International GmbH are actively investing in research and development to introduce innovative solutions and expand their market reach. While the market enjoys strong growth, potential restraints include the initial cost of integration for some vehicle segments and the ongoing development of alternative sensing technologies. Nonetheless, the overarching trend towards smarter, safer vehicles, coupled with a growing global automotive production, firmly positions the Automotive Rain Sensors market for sustained and impressive growth through 2033.

Automotive Rain Sensors Industry Company Market Share

Automotive Rain Sensors Industry Report Description: Driving Future Autonomous Mobility

This comprehensive report delves into the dynamic Automotive Rain Sensors Industry, a critical component for advanced driver-assistance systems (ADAS) and autonomous driving (AD) technologies. Analyze market dynamics, innovation trends, regional dominance, and key players shaping the future of vehicle safety and convenience. Leveraging high-ranking keywords such as "automotive rain sensors," "ADAS sensors," "autonomous driving technology," "vehicle safety systems," and "automotive electronics," this report is designed for industry professionals seeking actionable insights and strategic growth opportunities. The study period spans from 2019 to 2033, with the base and estimated year at 2025, and a robust forecast period of 2025–2033, building upon the historical data from 2019–2024.

Automotive Rain Sensors Industry Market Structure & Innovation Trends

The Automotive Rain Sensors Industry exhibits a moderately concentrated market structure, with leading players like Denso Corporation, Valeo group, ams-OSRAM International GmbH, STMicroelectronics, HELLA GmbH & Co KGaA, HAMAMATSU PHOTONICS KK, Semiconductor Components Industries LLC, Analog Devices Inc, and ZF Friedrichshafen AG holding significant market shares. Innovation is primarily driven by the escalating demand for enhanced vehicle safety, the rapid adoption of ADAS features, and the push towards higher levels of vehicle automation. Regulatory frameworks mandating advanced safety features are also instrumental in fostering innovation. Product substitutes, while emerging in sophisticated ADAS architectures, currently do not fully replicate the direct functionality and cost-effectiveness of dedicated rain sensors for wiper activation and sensor cleaning. End-user demographics increasingly favor vehicles equipped with advanced comfort and safety features, driving demand. Mergers and acquisition (M&A) activities, with an estimated total deal value of over $500 Million historically, are strategically consolidating the market and accelerating technological integration to meet the evolving needs of the automotive sector. Key innovation drivers include the development of more robust and cost-effective sensor technologies, improved algorithms for adverse weather detection, and seamless integration into complex vehicle electronic architectures.

Automotive Rain Sensors Industry Market Dynamics & Trends

The Automotive Rain Sensors Industry is experiencing robust growth, propelled by several interconnected market dynamics and trends. The primary growth driver is the relentless advancement and widespread adoption of Advanced Driver-Assistance Systems (ADAS). As automotive manufacturers strive to enhance vehicle safety and offer more sophisticated driver comfort features, the integration of rain sensors has become almost standard in mid-range to premium vehicles. This is further amplified by the global push towards autonomous driving, where reliable perception of environmental conditions, including precipitation, is paramount for safe operation. Technological disruptions are constantly reshaping the landscape, with advancements in optical sensor technology leading to more accurate and reliable performance across a wider range of conditions. The miniaturization and cost reduction of these sensors also contribute to their broader integration. Consumer preferences are increasingly shifting towards vehicles equipped with intelligent features that automate routine tasks and enhance safety, making rain-sensing wipers and headlight activation highly desirable. The competitive dynamics within the industry are characterized by intense R&D efforts, strategic partnerships between sensor manufacturers and automotive OEMs, and a focus on developing integrated sensor solutions. The market penetration of rain sensors is steadily increasing, and the Compound Annual Growth Rate (CAGR) is projected to remain strong throughout the forecast period, driven by evolving automotive standards and consumer expectations. The market is also influenced by the growing demand for electric vehicles (EVs), which often feature advanced electronic systems that can readily accommodate sensor integration. Furthermore, the increasing sophistication of vehicle electronics and the trend towards centralized computing architectures create opportunities for more integrated and intelligent sensor solutions.

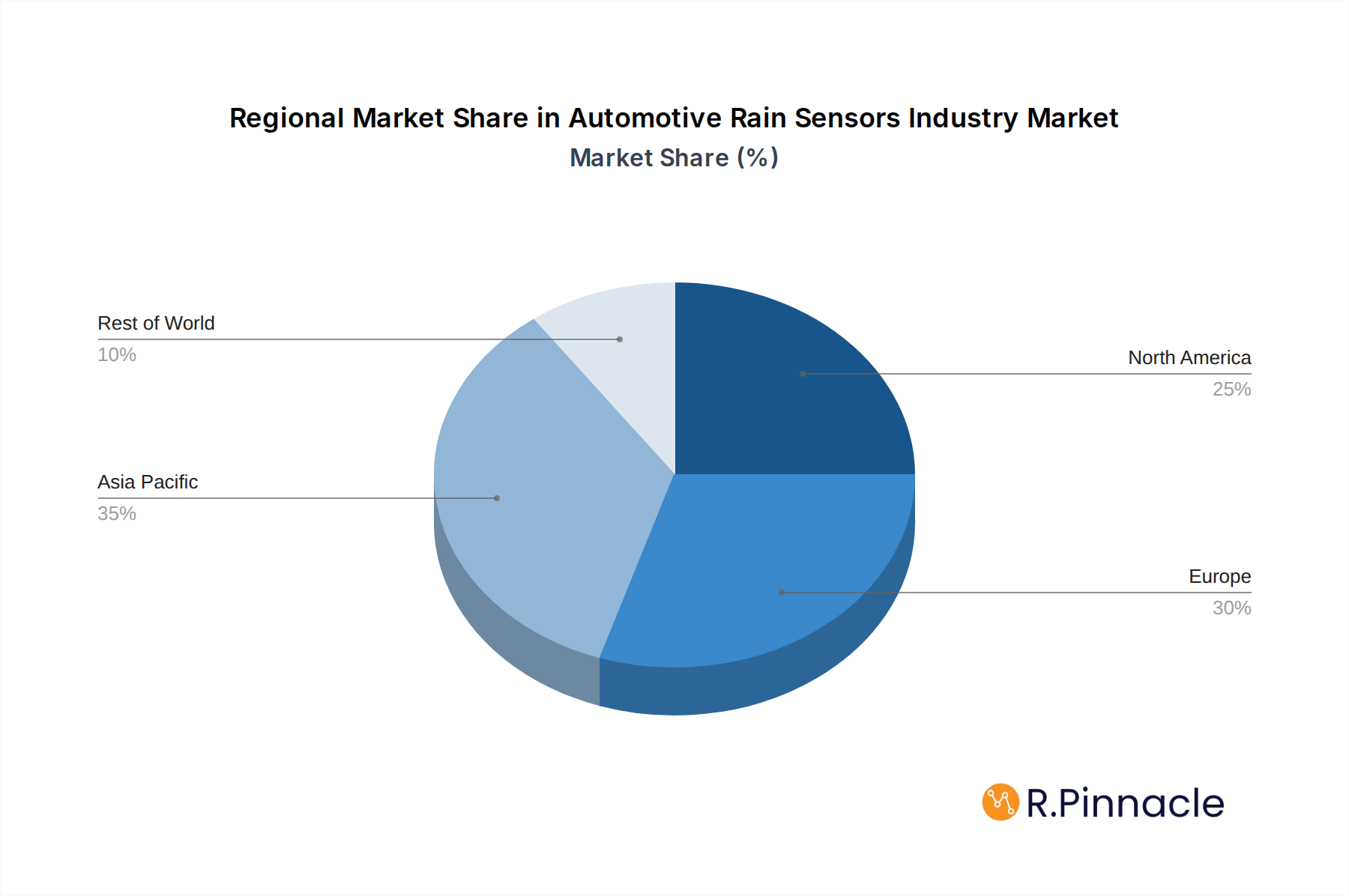

Dominant Regions & Segments in Automotive Rain Sensors Industry

The Passenger Cars segment overwhelmingly dominates the Automotive Rain Sensors Industry. This dominance is fueled by the sheer volume of passenger car production globally and the high penetration rate of ADAS features in this vehicle type. As consumer demand for comfort and safety in personal vehicles continues to rise, so does the integration of rain sensors. Key drivers for this segment's dominance include:

- Consumer Demand for Comfort and Safety: Buyers of passenger cars actively seek features that enhance their driving experience and provide peace of mind, with automatic rain-sensing wipers and headlights being highly valued.

- ADAS Feature Proliferation: The widespread integration of ADAS, from basic convenience features to advanced safety systems, makes rain sensors an essential component in modern passenger vehicles.

- Automotive OEM Strategy: Manufacturers are leveraging ADAS features, including rain sensors, as key selling points to differentiate their models and capture market share.

- Economic Policies: Favorable economic conditions in major automotive markets lead to higher disposable incomes, enabling consumers to opt for vehicles with more advanced features.

In terms of regional dominance, Asia Pacific currently leads the Automotive Rain Sensors Industry and is expected to maintain its position. This leadership is attributed to several critical factors:

- Largest Automotive Production Hub: Asia Pacific, particularly China, is the world's largest automotive manufacturing hub, producing millions of vehicles annually across all segments.

- Growing Middle Class and Disposable Income: The expanding middle class in countries like China, India, and Southeast Asian nations drives demand for new vehicles equipped with advanced technologies.

- Government Initiatives and Regulations: Increasing focus on road safety and the implementation of regulations mandating ADAS features in new vehicles are boosting the adoption of rain sensors.

- Technological Advancement and Investment: Significant investments in automotive R&D and manufacturing infrastructure within the region facilitate the production and integration of sophisticated automotive electronics.

Automotive Rain Sensors Industry Product Innovations

Product innovations in the Automotive Rain Sensors Industry are focused on enhancing accuracy, reliability, and cost-effectiveness. Advancements include the development of optical sensors that can better distinguish between rain, snow, and other obscurants, as well as integrated sensor modules that combine rain sensing with other functionalities like ambient light sensing. These innovations offer competitive advantages by improving ADAS performance, enabling more precise automatic wiper control, and supporting autonomous driving systems in adverse weather conditions. The trend towards miniaturization and reduced power consumption further improves market fit and facilitates seamless integration into vehicle architectures.

Report Scope & Segmentation Analysis

This report meticulously segments the Automotive Rain Sensors Industry by Vehicle Type, encompassing Passenger Cars and Commercial Vehicles. The Passenger Cars segment is projected to exhibit substantial growth due to its high volume and rapid adoption of ADAS technologies. Market sizes for this segment are estimated to reach approximately $3.5 Billion by 2033, with a CAGR of around 8.5%. The Commercial Vehicles segment, while currently smaller, is anticipated to witness significant growth, driven by increasing safety regulations and the adoption of autonomous features in trucking and logistics. Market projections for commercial vehicles indicate a market size of roughly $800 Million by 2033, with a CAGR of approximately 9.2%. Competitive dynamics within each segment are shaped by the specific integration needs and cost sensitivities inherent to each vehicle type.

Key Drivers of Automotive Rain Sensors Industry Growth

The growth of the Automotive Rain Sensors Industry is propelled by several key drivers. The escalating adoption of Advanced Driver-Assistance Systems (ADAS) and the increasing pursuit of higher levels of vehicle automation are paramount. Stringent government regulations mandating enhanced vehicle safety features worldwide also play a crucial role. Furthermore, rising consumer demand for convenience and comfort in vehicles, coupled with technological advancements leading to more accurate and cost-effective sensor solutions, contributes significantly to market expansion. The increasing electrification of vehicles also presents an opportunity, as EV architectures are well-suited for integrating advanced electronic components.

Challenges in the Automotive Rain Sensors Industry Sector

Despite its robust growth, the Automotive Rain Sensors Industry faces several challenges. The high cost of advanced sensor technologies can be a barrier to widespread adoption in entry-level vehicles. Intense competition among established players and emerging market entrants can lead to price pressures. Supply chain disruptions, as evidenced by recent global events, can impact component availability and manufacturing timelines. Moreover, the complexity of integrating sensors into diverse vehicle architectures and ensuring their reliability across a wide range of environmental conditions requires continuous R&D investment and rigorous testing. Regulatory hurdles related to data privacy and cybersecurity for connected vehicles also present a growing concern.

Emerging Opportunities in Automotive Rain Sensors Industry

Emerging opportunities in the Automotive Rain Sensors Industry are abundant. The development of multi-functional sensors that combine rain sensing with other environmental perception capabilities, such as light and fog detection, presents significant potential. The expanding market for autonomous driving, which necessitates highly reliable perception systems for all weather conditions, offers a substantial growth avenue. Furthermore, the increasing demand for smart city infrastructure and connected vehicle ecosystems creates opportunities for integrated sensor solutions that communicate with external systems. The aftermarket segment, offering retrofitting solutions for older vehicles, also represents a niche but growing area.

Leading Players in the Automotive Rain Sensors Industry Market

- Denso Corporation

- Valeo group

- ams-OSRAM International GmbH

- STMicroelectronics

- HELLA GmbH & Co KGaA

- HAMAMATSU PHOTONICS KK

- Semiconductor Components Industries LLC

- Analog Devices Inc

- ZF Friedrichshafen AG

Key Developments in Automotive Rain Sensors Industry Industry

- March 2022: StradVision and ZF announced a partnership to expand their automated driving perception software portfolio. StradVision's SVNet software could enable vehicles to detect and identify objects even in adverse weather or low-light conditions, environmental sensor fusion for shuttles, and commercial and light vehicles that could be optimized for centralized electrical architectures.

- July 2021: After the partnership with LiDAR expert AEye, Continental could integrate the long-range LiDAR technology into its full sensor stack solution to create the first full-stack automotive-grade system for Level 2+ up to Level 4 automated and autonomous driving applications. The solution based on AEye's LiDAR technology is a substantial part of the sensor setup for high-level automation systems.

Future Outlook for Automotive Rain Sensors Industry Market

The future outlook for the Automotive Rain Sensors Industry remains exceptionally positive. The sustained drive towards enhanced vehicle safety, the accelerating integration of ADAS and autonomous driving technologies, and evolving consumer expectations for intelligent vehicle features will continue to propel market growth. Strategic investments in R&D, focusing on improving sensor accuracy, reducing costs, and developing integrated sensor solutions, will be crucial for market leaders. The increasing adoption of electric vehicles, which are inherently equipped with advanced electronic systems, will further accelerate the integration of rain sensors. Opportunities for market expansion also lie in emerging economies and the development of specialized sensor solutions for commercial and niche automotive applications. The industry is poised for continuous innovation, ensuring safer and more convenient mobility in the years to come.

Automotive Rain Sensors Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

Automotive Rain Sensors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of World

- 4.1. Brazil

- 4.2. Saudi Arabia

- 4.3. United Arab Emirates

- 4.4. South Africa

- 4.5. Rest of World

Automotive Rain Sensors Industry Regional Market Share

Geographic Coverage of Automotive Rain Sensors Industry

Automotive Rain Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of World

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Pacific Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Rest of World Automotive Rain Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Denso Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Valeo group

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 ams-OSRAM International GmbH

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 STMicroelectronics

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 HELLA GmbH & Co KGaA

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 HAMAMATSU PHOTONICS KK*List Not Exhaustive

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Semiconductor Components Industries LLC

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Analog Devices Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 ZF Friedrichshafen AG

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 Denso Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Rain Sensors Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 3: North America Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 7: Europe Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: Europe Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Asia Pacific Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Asia Pacific Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of World Automotive Rain Sensors Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 15: Rest of World Automotive Rain Sensors Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Rest of World Automotive Rain Sensors Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Rest of World Automotive Rain Sensors Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Rest of North America Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 10: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Germany Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: United Kingdom Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: France Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Russia Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Spain Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Rest of Europe Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 18: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: India Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: China Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Japan Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Asia Pacific Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 25: Global Automotive Rain Sensors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Brazil Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Saudi Arabia Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Arab Emirates Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: South Africa Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of World Automotive Rain Sensors Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Rain Sensors Industry?

The projected CAGR is approximately 7.20%.

2. Which companies are prominent players in the Automotive Rain Sensors Industry?

Key companies in the market include Denso Corporation, Valeo group, ams-OSRAM International GmbH, STMicroelectronics, HELLA GmbH & Co KGaA, HAMAMATSU PHOTONICS KK*List Not Exhaustive, Semiconductor Components Industries LLC, Analog Devices Inc, ZF Friedrichshafen AG.

3. What are the main segments of the Automotive Rain Sensors Industry?

The market segments include Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.23 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Urbanization and Demand for Convinient Transportation.

6. What are the notable trends driving market growth?

RISING AWARENESS TOWARDS SAFETY AND COMFORT EXPECTED TO DRIVE DEMAND.

7. Are there any restraints impacting market growth?

Traffic Congestion in Major Cities.

8. Can you provide examples of recent developments in the market?

In March 2022, StradVision and ZF announced a partnership to expand their automated driving perception software portfolio. StradVision's SVNet software could enable vehicles to detect and identify objects even in adverse weather or low-light conditions, environmental sensor fusion for shuttles, and commercial and light vehicles that could be optimized for centralized electrical architectures.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Rain Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Rain Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Rain Sensors Industry?

To stay informed about further developments, trends, and reports in the Automotive Rain Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence