Key Insights

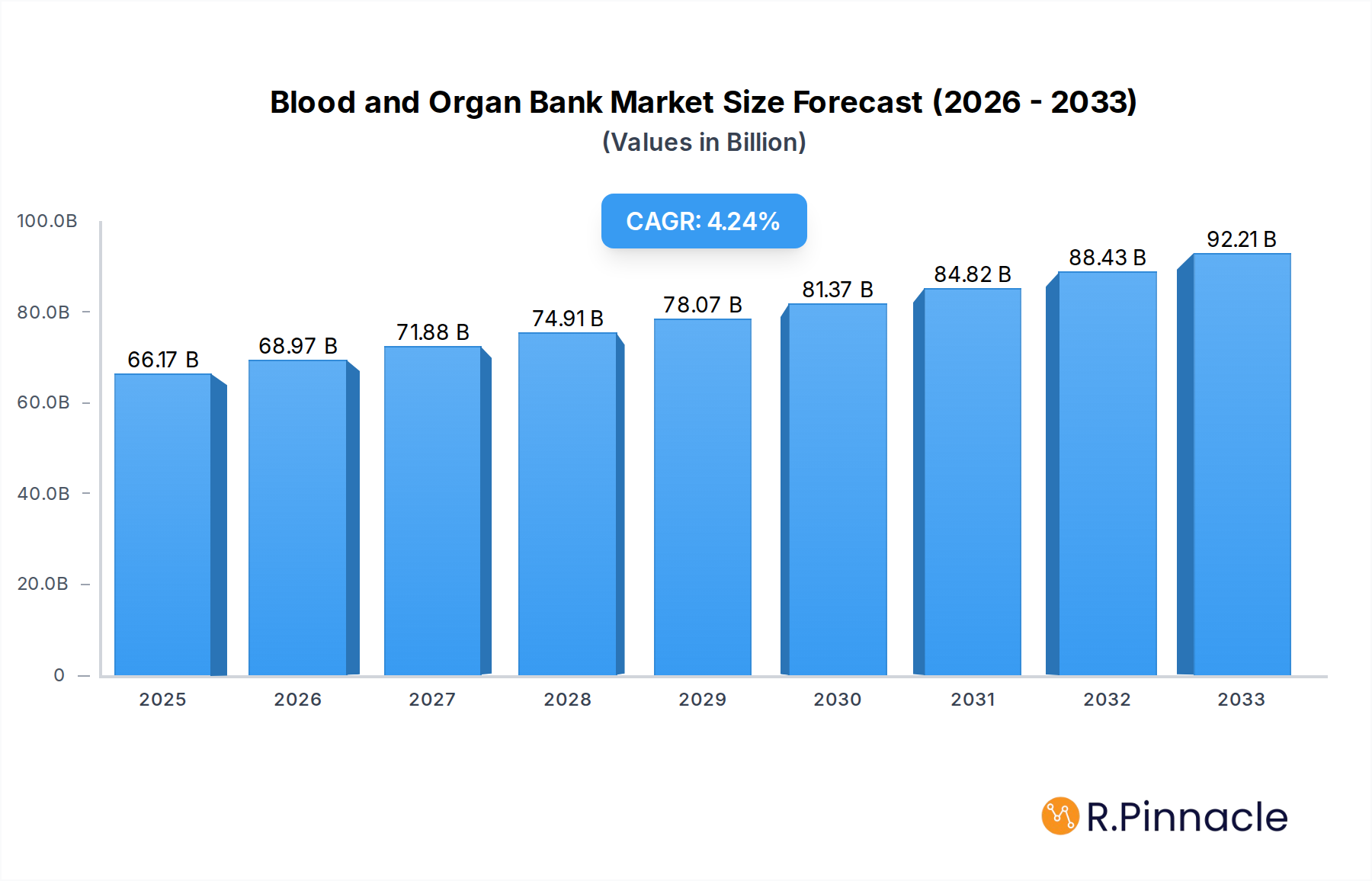

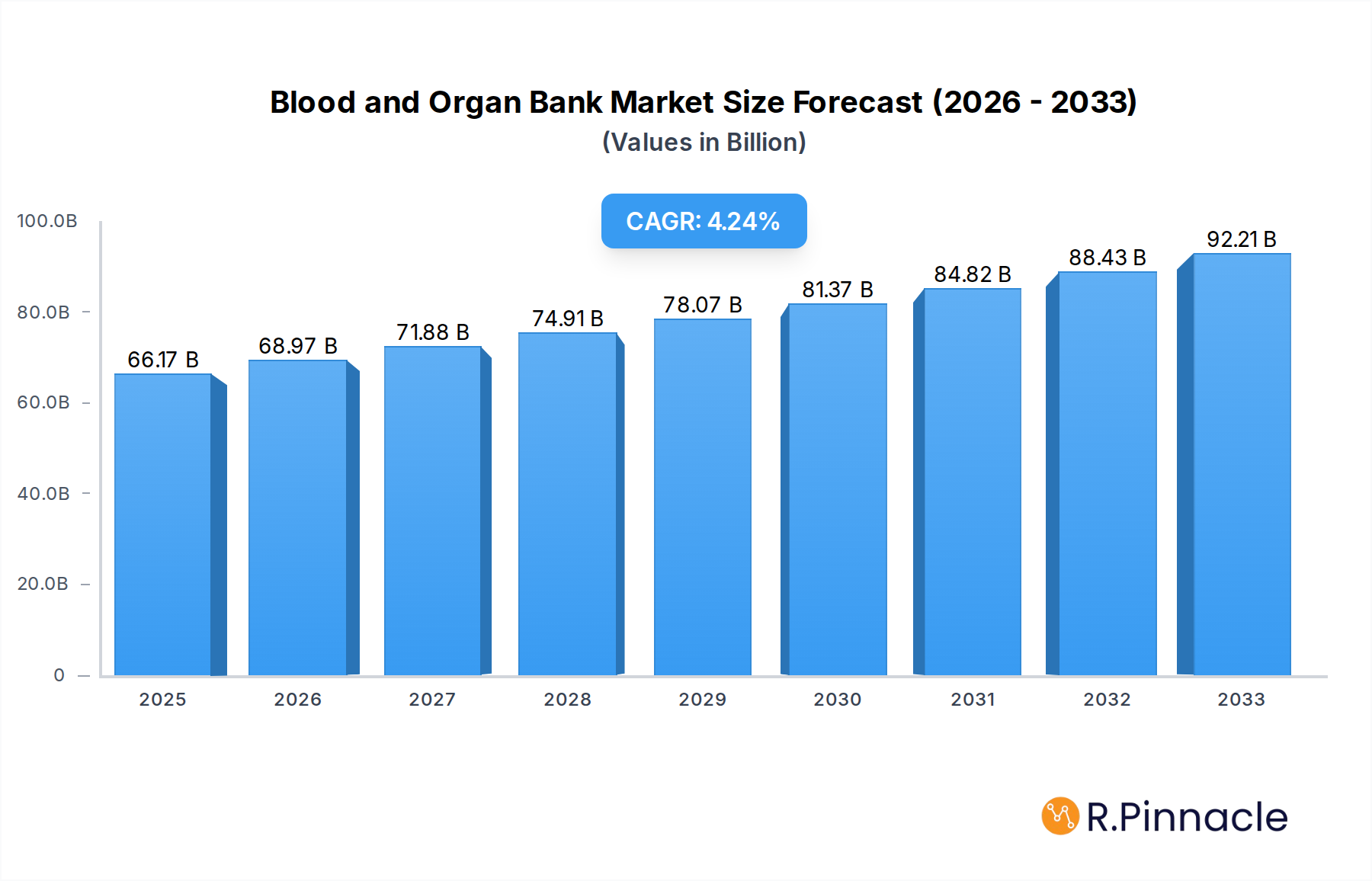

The global Blood and Organ Bank market is poised for significant expansion, projected to reach a valuation of $66.17 billion in 2025. This robust growth is driven by an increasing demand for life-saving blood transfusions and organ transplants, fueled by aging populations, rising incidences of chronic diseases like cancer and cardiovascular ailments, and advancements in medical technologies that enhance transplantation success rates. The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 4.3% from 2025 to 2033. Key segments contributing to this growth include Hospitals and Diagnostic Centers, which represent the primary end-users, and services related to Red Blood Cell Collection, Processing, and Distribution, as well as Blood Plasma Collection, Processing, and Distribution, highlighting the foundational aspects of blood banking. Furthermore, the burgeoning field of Reproductive and Stem Cell Bank Services is emerging as a significant growth area, reflecting a greater societal emphasis on proactive health management and future medical possibilities.

Blood and Organ Bank Market Size (In Billion)

The market's expansion is further supported by favorable government initiatives aimed at promoting blood donation and organ registration, alongside increasing awareness campaigns that encourage voluntary contributions. However, challenges such as stringent regulatory frameworks governing blood and organ procurement, storage, and distribution, coupled with concerns regarding the cost of specialized infrastructure and trained personnel, could present moderate headwinds. Nonetheless, the overarching positive trajectory is expected to continue, with ongoing technological innovations in blood processing and preservation techniques, as well as improvements in organ procurement logistics and recipient matching systems, playing a crucial role in overcoming these restraints. Key players are strategically focusing on expanding their service offerings and geographic reach to capitalize on the growing global demand for these critical healthcare services.

Blood and Organ Bank Company Market Share

Here's the SEO-optimized, reader-centric report description for the Blood and Organ Bank market:

Blood and Organ Bank Market Structure & Innovation Trends

The global Blood and Organ Bank market, valued at an estimated xx billion in the base year 2025, exhibits a moderately consolidated structure with key players driving innovation and market expansion. The study period, 2019–2033, encompasses significant advancements and evolving regulatory landscapes that shape market concentration. Innovation drivers are primarily centered around enhanced preservation techniques for blood and organs, advanced diagnostic tools, and the increasing adoption of cord blood banking for therapeutic purposes. Regulatory frameworks, while crucial for ensuring safety and efficacy, can also present hurdles to market entry and product development. Substitutes for traditional blood transfusions and organ transplants, such as artificial blood and bio-engineered organs, are nascent but represent a growing area of research. End-user demographics are shifting, with an aging global population and a rising prevalence of chronic diseases contributing to increased demand. Mergers and acquisition (M&A) activities, with a total deal value estimated at xx billion historically and projected to reach xx billion by 2033, are strategic initiatives aimed at consolidating market share, expanding service portfolios, and leveraging technological synergies. Leading companies like American Red Cross and New England Donor Services hold significant market share.

Blood and Organ Bank Market Dynamics & Trends

The Blood and Organ Bank market is poised for robust growth, driven by a confluence of demographic shifts, technological advancements, and evolving healthcare paradigms. The global CAGR is projected at xx% during the forecast period of 2025–2033, propelling the market from an estimated xx billion in 2025 to xx billion by 2033. Key growth drivers include the increasing incidence of chronic diseases requiring blood transfusions and organ transplantation, such as cardiovascular diseases, diabetes, and cancer. The aging global population further exacerbates this demand, as older individuals are more susceptible to organ failure and blood-related conditions. Technological disruptions are revolutionizing the sector, with advancements in organ preservation techniques extending viability and improving transplant outcomes. The development of more sophisticated blood processing and storage solutions, alongside rapid diagnostics, is enhancing efficiency and safety. Consumer preferences are leaning towards personalized medicine and proactive health management, boosting the demand for reproductive and stem cell banking services. The competitive dynamics are characterized by strategic collaborations between research institutions and commercial entities, as well as increasing investment in research and development by both established players and emerging biotechnology firms. Market penetration for advanced services like cord blood banking is steadily increasing, driven by greater awareness of their therapeutic potential. The integration of artificial intelligence (AI) and machine learning (ML) in donor matching and logistical optimization is a significant trend shaping operational efficiency. Furthermore, government initiatives promoting organ donation and blood availability, coupled with rising healthcare expenditures in developing economies, are creating a fertile ground for market expansion. The growing emphasis on regenerative medicine and cell-based therapies is also a significant factor driving innovation and demand within the broader blood and organ banking ecosystem.

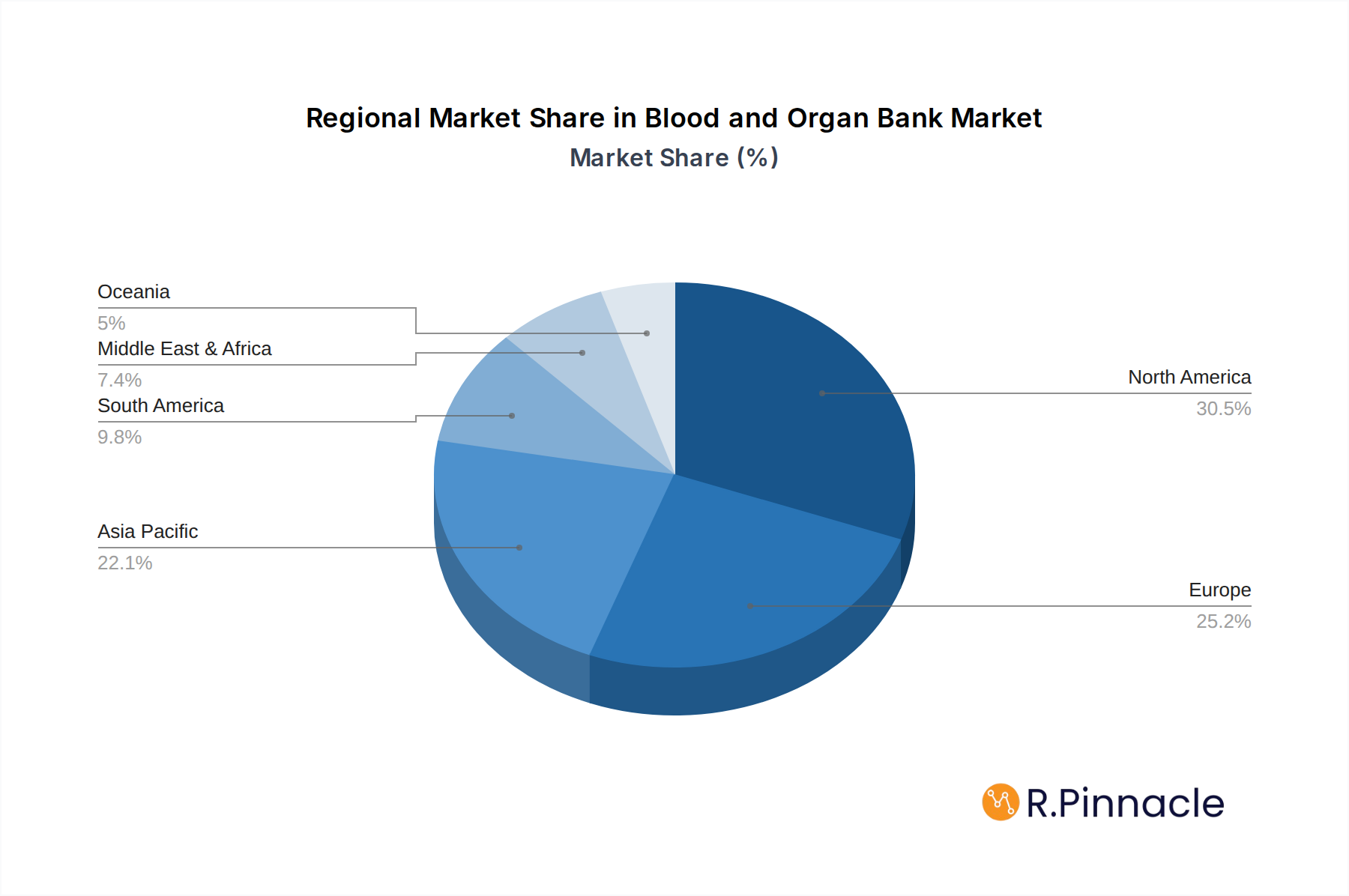

Dominant Regions & Segments in Blood and Organ Bank

North America currently dominates the Blood and Organ Bank market, driven by a well-established healthcare infrastructure, high disposable incomes, and robust government support for medical research and donation initiatives. Within North America, the United States leads with a substantial market share due to the presence of major players like American Red Cross and New England Donor Services, and a high rate of organ transplants and blood transfusions.

Key Drivers of Dominance in North America:

- Advanced Healthcare Infrastructure: State-of-the-art hospitals and diagnostic centers equipped with the latest technology facilitate efficient blood and organ banking operations.

- High Public Awareness and Donation Rates: Extensive public awareness campaigns and established organ donation networks contribute to a steady supply of blood and organs.

- Strong Research and Development Ecosystem: Significant investment in R&D by academic institutions and private companies fuels innovation in preservation and processing techniques.

- Favorable Regulatory Environment: Supportive policies and regulatory frameworks streamline the processes for collection, processing, and distribution, while ensuring stringent quality standards.

Among the Application segments, Hospitals represent the largest share, as they are the primary centers for transfusion, transplantation surgeries, and associated diagnostic procedures. Diagnostic Centers are also crucial for blood typing, screening, and organ viability assessment.

In terms of Types, Red Blood Cell Collection, Processing, and Distribution Services command the largest market share due to the widespread and continuous demand for blood transfusions across various medical conditions. Blood Plasma Collection, Processing, and Distribution Services follow closely, with plasma being vital for numerous therapeutic applications and the manufacturing of blood-derived products. Reproductive and Stem Cell Bank Services are experiencing rapid growth, fueled by increasing awareness of stem cell therapy and the desire for future health security.

Blood and Organ Bank Product Innovations

Product innovations in the Blood and Organ Bank sector are focused on enhancing the viability, safety, and accessibility of biological materials. Advances in organ preservation solutions, such as hypothermic storage and machine perfusion, are significantly extending the time organs remain viable, thereby improving transplant success rates and broadening the donor pool. For blood products, innovations include novel anticoagulant solutions and advanced filtration technologies to improve quality and reduce adverse reactions. The development of more sensitive and rapid diagnostic testing for infectious diseases and compatibility further strengthens the sector's offerings, ensuring safer transfusions and transplants. Competitive advantages are derived from superior preservation technologies, efficient logistical networks, and robust quality control measures.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global Blood and Organ Bank market, segmenting it across key applications and service types. The Application segmentation includes Hospitals, the largest segment driven by continuous demand for transfusions and transplants; Diagnostic Centers, crucial for pre-transplant evaluations and blood screening; and Others, encompassing research institutions and specialized clinics. The Types segmentation covers Red Blood Cell Collection, Processing, and Distribution Services, a foundational segment with consistent demand; Blood Plasma Collection, Processing, and Distribution Services, vital for critical care and biopharmaceutical production; and Reproductive and Stem Cell Bank Services, a rapidly growing segment with significant future potential. Growth projections indicate a Compound Annual Growth Rate (CAGR) of xx% for reproductive and stem cell banking, with an estimated market size of xx billion by 2033.

Key Drivers of Blood and Organ Bank Growth

Several factors are propelling the growth of the Blood and Organ Bank market. Technologically, advancements in organ preservation techniques, like machine perfusion, are extending organ viability and widening the window for transplantation. The development of more efficient blood processing and storage solutions also contributes significantly. Economically, increasing healthcare expenditure globally, particularly in emerging economies, and rising insurance coverage for medical procedures are making these services more accessible. Regulatory factors, such as government initiatives promoting organ donation awareness and streamlined donation processes, play a crucial role. Furthermore, the growing prevalence of chronic diseases requiring blood transfusions and organ transplants, coupled with an aging global population, creates a persistent and escalating demand.

Challenges in the Blood and Organ Bank Sector

The Blood and Organ Bank sector faces notable challenges that impact its growth trajectory. Regulatory hurdles, including stringent approval processes for new technologies and differing regulations across regions, can slow down innovation adoption. Supply chain complexities, particularly in ensuring timely and efficient transportation of organs and blood products, pose significant logistical challenges, especially over long distances. Competitive pressures from both established players and emerging biotech firms, vying for market share and investment, necessitate continuous innovation and cost-effectiveness. Furthermore, the inherent ethical considerations and public perception surrounding organ donation and banking can influence supply and demand. The significant cost associated with advanced preservation technologies and specialized banking services can also be a barrier for wider adoption.

Emerging Opportunities in Blood and Organ Bank

The Blood and Organ Bank sector is ripe with emerging opportunities driven by technological advancements and evolving healthcare needs. The burgeoning field of regenerative medicine, leveraging stem cells for tissue repair and disease treatment, presents a significant growth avenue. Development of artificial blood substitutes and bio-engineered organs, while in early stages, holds transformative potential for the future. Expansion into emerging markets with growing healthcare infrastructure and increasing disposable incomes offers substantial untapped potential. The integration of AI and big data analytics for optimized donor matching, inventory management, and predictive demand forecasting presents a key opportunity to enhance efficiency and reduce wastage. Furthermore, personalized medicine approaches are paving the way for more targeted blood and organ banking strategies.

Leading Players in the Blood and Organ Bank Market

- American Red Cross

- New England Donor Services

- 21st Century Medicine

- New York Blood Centre

- The Living Bank

- Musculoskeletal Transplant Foundation

- National Organ & Tissue Transplant Organisation

- China Cord Blood Corporation

- National Cord Blood Program

- Cord Blood Registry

Key Developments in Blood and Organ Bank Industry

- 2023 (Ongoing): Increased investment in AI-powered donor matching algorithms to improve efficiency and reduce wait times for organ transplants.

- 2023 (Ongoing): Advancements in machine perfusion technology for extended organ viability, leading to higher transplant success rates.

- 2023 (Ongoing): Growing adoption of private cord blood banking services due to enhanced awareness of stem cell therapeutic potential.

- 2022: Several mergers and acquisitions among smaller blood collection agencies and stem cell banks to consolidate market presence and resources.

- 2021: Development of novel cryopreservation techniques for blood components, leading to longer shelf life and improved stability.

- 2020: Increased focus on public health initiatives to boost voluntary blood donation rates following global health challenges.

Future Outlook for Blood and Organ Bank Market

The future outlook for the Blood and Organ Bank market is exceptionally promising, characterized by sustained growth and transformative innovation. The increasing global demand for blood transfusions and organ transplants, driven by an aging population and the rising incidence of chronic diseases, will continue to be a primary growth accelerator. Advances in organ preservation and ex vivo machine perfusion technologies are expected to revolutionize transplant outcomes, making more organs available and extending their viability. The burgeoning field of regenerative medicine and stem cell therapies, particularly from cord blood banking, represents a significant long-term growth opportunity, offering potential treatments for a wide range of diseases. Furthermore, the integration of cutting-edge technologies like AI and blockchain for enhanced donor matching, supply chain management, and data security will streamline operations and improve patient care. Strategic collaborations between research institutions, biotechnology companies, and healthcare providers will foster a dynamic environment for product development and market expansion.

Blood and Organ Bank Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Diagnostic Canters

- 1.3. Others

-

2. Types

- 2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 2.2. Blood Plasma Collection, Processing, and Distribution Services

- 2.3. Reproductive and Stem Cell Bank Services

- 2.4. Others

Blood and Organ Bank Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Blood and Organ Bank Regional Market Share

Geographic Coverage of Blood and Organ Bank

Blood and Organ Bank REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Diagnostic Canters

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 5.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 5.2.3. Reproductive and Stem Cell Bank Services

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Diagnostic Canters

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 6.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 6.2.3. Reproductive and Stem Cell Bank Services

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Diagnostic Canters

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 7.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 7.2.3. Reproductive and Stem Cell Bank Services

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Diagnostic Canters

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 8.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 8.2.3. Reproductive and Stem Cell Bank Services

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Diagnostic Canters

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 9.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 9.2.3. Reproductive and Stem Cell Bank Services

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Blood and Organ Bank Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Diagnostic Canters

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Red Blood Cell Collection, Processing, and Distribution Services

- 10.2.2. Blood Plasma Collection, Processing, and Distribution Services

- 10.2.3. Reproductive and Stem Cell Bank Services

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 American Red Cross

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 New England Donor Services

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 21st Century Medicine

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 New York Blood Centre

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 The Living Bank

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Musculoskeletal Transplant Foundation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 National Organ & Tissue Transplant Organisation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 China Cord Blood Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 National Cord Blood Program

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cord Blood Registry

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 American Red Cross

List of Figures

- Figure 1: Global Blood and Organ Bank Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Blood and Organ Bank Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Blood and Organ Bank Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Blood and Organ Bank Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Blood and Organ Bank Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Blood and Organ Bank Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Blood and Organ Bank Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Blood and Organ Bank Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Blood and Organ Bank Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Blood and Organ Bank Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Blood and Organ Bank Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Blood and Organ Bank Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Blood and Organ Bank Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Blood and Organ Bank Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Blood and Organ Bank Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Blood and Organ Bank Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Blood and Organ Bank Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Blood and Organ Bank Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Blood and Organ Bank Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Blood and Organ Bank Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Blood and Organ Bank Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Blood and Organ Bank Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Blood and Organ Bank Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Blood and Organ Bank Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Blood and Organ Bank Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Blood and Organ Bank Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Blood and Organ Bank Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Blood and Organ Bank Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Blood and Organ Bank Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Blood and Organ Bank Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Blood and Organ Bank Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Blood and Organ Bank Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Blood and Organ Bank Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Blood and Organ Bank Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Blood and Organ Bank Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Blood and Organ Bank Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Blood and Organ Bank Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Blood and Organ Bank Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Blood and Organ Bank Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Blood and Organ Bank Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood and Organ Bank?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Blood and Organ Bank?

Key companies in the market include American Red Cross, New England Donor Services, 21st Century Medicine, New York Blood Centre, The Living Bank, Musculoskeletal Transplant Foundation, National Organ & Tissue Transplant Organisation, China Cord Blood Corporation, National Cord Blood Program, Cord Blood Registry.

3. What are the main segments of the Blood and Organ Bank?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4000.00, USD 6000.00, and USD 8000.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blood and Organ Bank," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blood and Organ Bank report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blood and Organ Bank?

To stay informed about further developments, trends, and reports in the Blood and Organ Bank, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence