Key Insights

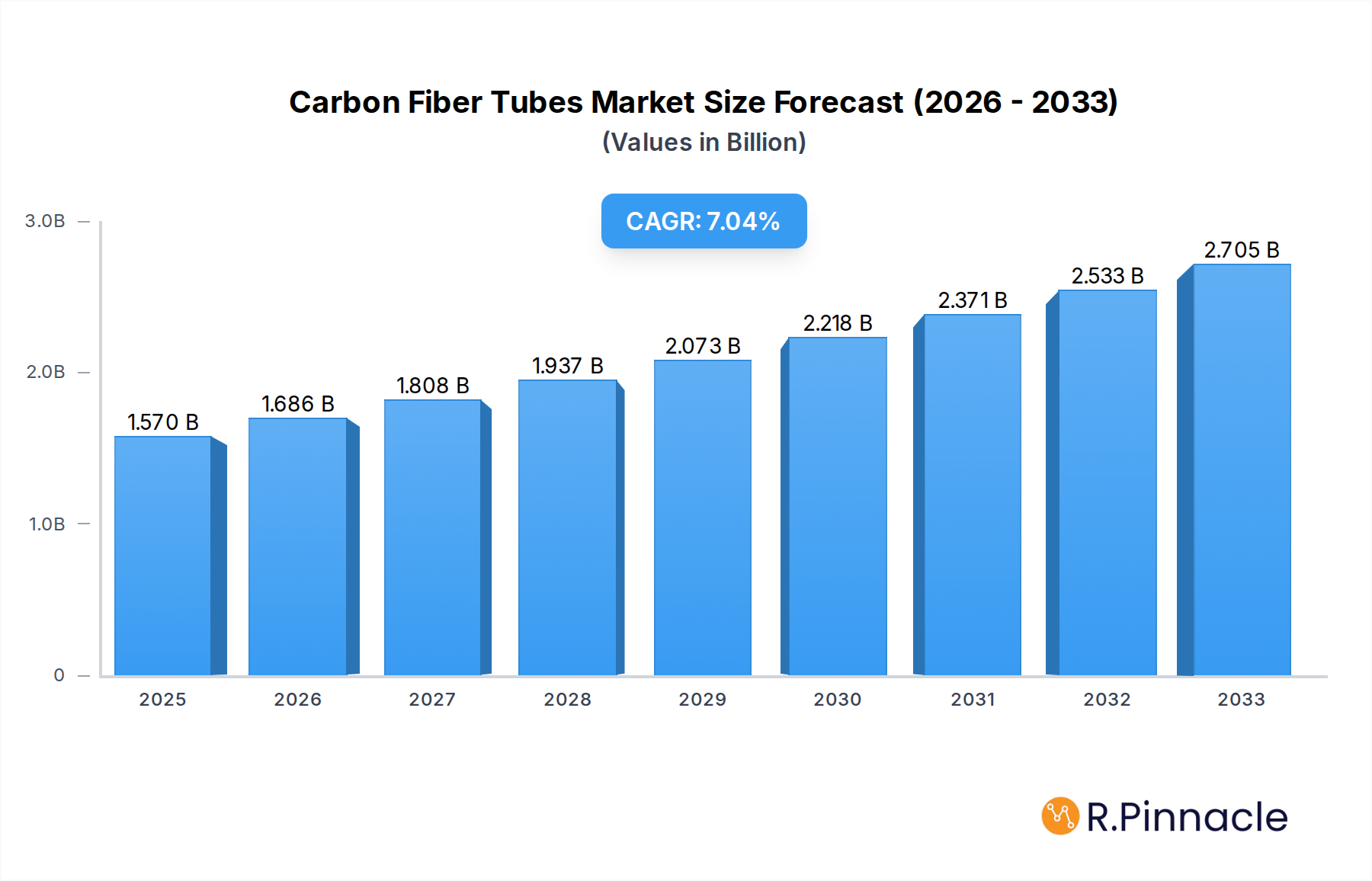

The global carbon fiber tubes market is poised for significant expansion, projected to reach approximately $1.57 billion in 2025. Driven by a robust CAGR of 7.2%, the market is expected to demonstrate sustained growth through 2033. This upward trajectory is largely attributed to the material's exceptional strength-to-weight ratio, superior stiffness, and corrosion resistance, making it an increasingly sought-after alternative to traditional materials like steel and aluminum. Key applications fueling this demand include sophisticated drinking water systems requiring durable and lightweight piping, critical chemical handling processes where material integrity is paramount, and efficient gas handling infrastructure. Furthermore, the growing adoption in utilities water management for enhanced infrastructure longevity and the diverse "Other" applications underscore the versatility of carbon fiber tubes. The market's expansion is also being bolstered by technological advancements in manufacturing processes, leading to more cost-effective production and wider accessibility.

Carbon Fiber Tubes Market Size (In Billion)

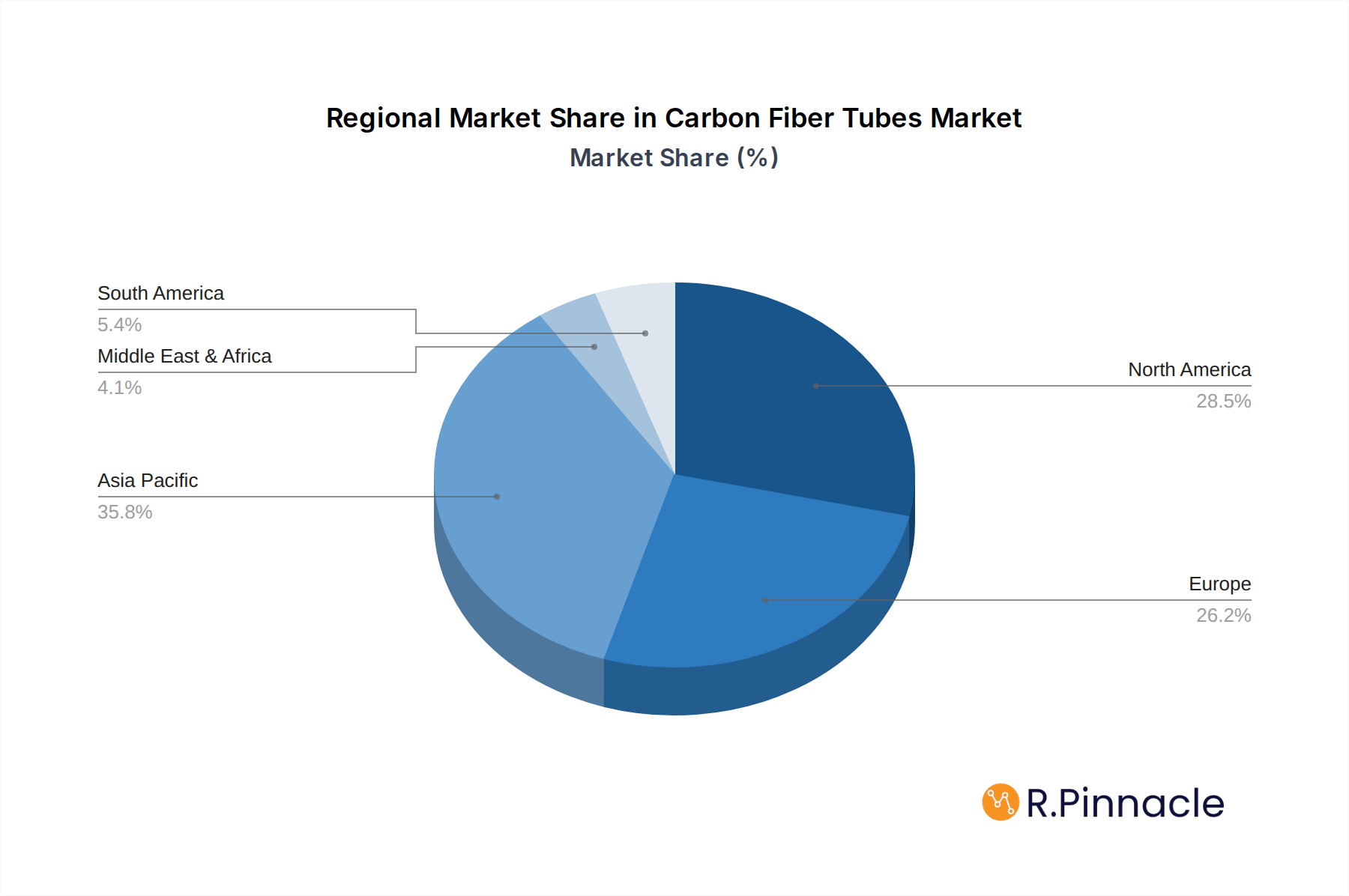

The market segmentation by diameter highlights a strong demand across various sizes, from the commonly used 1/2 inch to larger diameters exceeding 4 inches, catering to a broad spectrum of industrial and commercial needs. Leading manufacturers such as Exel Composites, Carbon Fibre Tubes Ltd, and Attwater Group are at the forefront of innovation, developing advanced composite solutions. Geographically, the Asia Pacific region, led by China and India, is emerging as a significant growth engine due to rapid industrialization and infrastructure development. North America and Europe continue to be substantial markets, driven by stringent performance requirements and a focus on lightweighting in various sectors. While opportunities abound, potential restraints such as the initial cost of carbon fiber production and the need for specialized handling and installation expertise, although diminishing with advancements, remain factors to monitor.

Carbon Fiber Tubes Company Market Share

This in-depth report delves into the dynamic carbon fiber tubes market, providing critical analysis and actionable intelligence for industry professionals, investors, and stakeholders. Covering a comprehensive study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this report offers a deep dive into market structures, growth drivers, regional dominance, product innovations, and future outlook. With an estimated market size in the billions of dollars, this analysis leverages high-ranking keywords to ensure maximum visibility and relevance for search engines and discerning readers seeking to capitalize on the burgeoning opportunities within this advanced materials sector.

Carbon Fiber Tubes Market Structure & Innovation Trends

The carbon fiber tubes market exhibits a moderate to high concentration, driven by specialized manufacturing processes and significant capital investment. Innovation is a key differentiator, with ongoing advancements in material science and manufacturing techniques aimed at enhancing strength-to-weight ratios, durability, and cost-effectiveness. Regulatory frameworks, particularly concerning safety and environmental standards in applications like drinking water and chemical handling, play a crucial role in shaping market entry and product development. The threat of product substitutes, such as high-strength steel or advanced polymers, is present but often mitigated by the superior performance characteristics of carbon fiber in demanding applications. End-user demographics are increasingly sophisticated, seeking lightweight, corrosion-resistant, and high-performance solutions across various industries. Mergers and acquisitions (M&A) activities, valued in the billions, are observed as established players seek to consolidate market share and acquire innovative technologies. Key M&A deal values are estimated to be in the hundreds of millions to billions of dollars annually, reflecting strategic consolidation. Market share is closely watched, with top players holding significant percentages, particularly in specialized niches.

Carbon Fiber Tubes Market Dynamics & Trends

The carbon fiber tubes market is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of xx% over the forecast period. This expansion is primarily fueled by the escalating demand for lightweight and high-strength materials across diverse applications. Technological disruptions, including advancements in composite manufacturing, automated production, and nanotechnology integration, are continuously pushing the boundaries of performance and cost-efficiency. Consumer preferences are increasingly skewed towards sustainable and durable solutions, aligning perfectly with the inherent benefits of carbon fiber tubes, such as their exceptional corrosion resistance and extended lifespan. The competitive landscape is characterized by a blend of established global manufacturers and emerging regional players, each vying for market penetration through product differentiation, strategic partnerships, and price optimization. Market penetration for carbon fiber tubes is steadily increasing, particularly in sectors where traditional materials are reaching their performance limits. The relentless pursuit of innovation in areas like resin formulations, fiber weaving techniques, and finishing processes further intensifies the competitive dynamics. The growing emphasis on reducing operational costs and enhancing infrastructure resilience across sectors like utilities water and gas handling is a significant catalyst for sustained market expansion. Furthermore, the aerospace and automotive industries’ continuous drive for weight reduction to improve fuel efficiency and performance directly translates into higher demand for these advanced composite solutions. The development of novel manufacturing techniques, such as additive manufacturing for composite structures, is also poised to revolutionize the production and customization of carbon fiber tubes, opening up new avenues for market growth and application diversity. The increasing adoption of stringent performance standards and environmental regulations worldwide is also acting as a strong tailwind, favoring materials like carbon fiber that offer superior performance and longevity with a reduced environmental footprint over their lifecycle. The ongoing research into enhancing the recyclability and end-of-life management of composite materials will further solidify the long-term sustainability appeal of carbon fiber tubes.

Dominant Regions & Segments in Carbon Fiber Tubes

North America currently holds a dominant position in the carbon fiber tubes market, driven by its advanced industrial infrastructure, significant investments in aerospace and defense, and strong emphasis on technological innovation. Within North America, the United States leads due to its robust manufacturing base and high adoption rates of advanced materials. Key drivers for this dominance include substantial government funding for research and development, favorable economic policies encouraging industrial growth, and extensive investments in infrastructure upgrades across utilities water and gas handling sectors.

The Application segment demonstrating significant traction includes Chemical Handling and Utilities Water. The chemical industry's need for corrosion-resistant, high-pressure tubing for aggressive media, coupled with the utilities sector's requirement for durable and long-lasting pipelines for water distribution and treatment, are major growth catalysts. The Gas Handling application is also experiencing notable growth due to the increasing demand for lightweight and secure solutions in the oil and gas sector, especially for offshore operations and exploration.

In terms of Types, the Diameter: Above 4 inch segment is witnessing substantial growth. This is attributed to the increasing scale of infrastructure projects, particularly in water management and industrial fluid transport, where larger diameter tubes are essential. However, the Diameter: 2 inch and Diameter: 3 inch segments remain critical for a wide array of industrial and specialized applications, including manufacturing equipment and structural components. The Diameter: 4 inch segment also plays a vital role in medium-scale industrial applications and specialized fluid conveyance systems. The demand for precise, high-performance tubing in the 1/2 inch diameter range continues to be significant in specialized electronic, medical, and sporting goods applications.

Carbon Fiber Tubes Product Innovations

Product innovations in the carbon fiber tubes market are centered on enhancing material properties and expanding application versatility. Developments include advancements in high-temperature resistance, increased impact strength, and improved chemical inertness, creating competitive advantages for manufacturers. New resin systems and advanced fiber architectures are enabling lighter, stronger tubes tailored for demanding environments, such as specialized chemical handling or high-pressure gas handling. The integration of smart functionalities, like embedded sensors for real-time monitoring, is also an emerging trend, offering enhanced operational efficiency and safety.

Report Scope & Segmentation Analysis

This report meticulously analyzes the carbon fiber tubes market across its diverse segmentations. The Application segments include Drinking Water, Chemical Handling, Gas Handling, Utilities Water, and Other. Each segment is projected to experience varying growth rates and market sizes, with Chemical Handling and Utilities Water expected to exhibit robust expansion due to their critical infrastructure roles and the demand for high-performance materials. The Types segmentation covers Diameter: 1/2 inch, Diameter: 2 inch, Diameter: 3 inch, Diameter: 4 inch, and Diameter: Above 4 inch. The Diameter: Above 4 inch segment is anticipated to lead in growth, driven by large-scale industrial and infrastructure projects, while other diameter segments will maintain strong relevance in specialized applications. Competitive dynamics within each segment are assessed to provide a comprehensive market overview.

Key Drivers of Carbon Fiber Tubes Growth

The growth of the carbon fiber tubes market is propelled by several key drivers. Technologically, the ongoing advancements in composite manufacturing, leading to improved material properties such as enhanced strength-to-weight ratios and superior corrosion resistance, are paramount. Economically, increasing global infrastructure development, particularly in water management and energy sectors, necessitates durable and long-lasting solutions. Regulatory factors, such as stricter environmental regulations and safety standards, favor the adoption of high-performance, low-maintenance materials like carbon fiber. For instance, the need for leak-proof and corrosion-resistant pipelines in utilities water systems directly supports this growth.

Challenges in the Carbon Fiber Tubes Sector

Despite its promising growth, the carbon fiber tubes sector faces several challenges. High initial manufacturing costs and the complex production processes can be a barrier to entry and adoption, especially for smaller enterprises. Regulatory hurdles related to material certifications and long-term performance validation in specific applications can also slow down market penetration. Supply chain volatility for raw materials, particularly carbon fiber precursors, can lead to price fluctuations and affect production timelines. Furthermore, competition from established materials like steel and aluminum, which often have lower upfront costs, remains a significant pressure point.

Emerging Opportunities in Carbon Fiber Tubes

Emerging opportunities in the carbon fiber tubes market are abundant. The increasing global focus on renewable energy infrastructure, such as wind turbines and solar panel supports, presents a significant avenue for growth. The development of novel applications in the medical device industry, where lightweight and biocompatible materials are crucial, offers substantial potential. Furthermore, advancements in recycling technologies for composite materials are poised to address environmental concerns and unlock new circular economy opportunities. The growing trend of lightweighting in transportation, beyond aerospace and automotive, including rail and marine sectors, also presents untapped market potential.

Leading Players in the Carbon Fiber Tubes Market

- Attwater Group

- Langtec

- Tri-cast Composite Tubes

- ICE

- Carbon Fibre Tubes Ltd

- Guangzhou Shengrui Insulation Materials

- Exel Composites

- Forte Carbon Fiber Tubing

- Clearwater Composites

- Jiangsu Toptek Composite Materials

Key Developments in Carbon Fiber Tubes Industry

- 2023: Increased focus on sustainable manufacturing processes and development of bio-based resins for carbon fiber composite tubes.

- 2022: Introduction of advanced, high-pressure resistant carbon fiber tubes for demanding oil and gas applications.

- 2021: Significant M&A activity as larger composites manufacturers acquire specialized carbon fiber tube producers to expand their portfolio.

- 2020: Enhanced research into self-healing composite materials for extended tube lifespan in critical infrastructure.

- 2019: Growing adoption of carbon fiber tubes in renewable energy infrastructure, particularly for offshore wind turbine components.

Future Outlook for Carbon Fiber Tubes Market

The carbon fiber tubes market is poised for sustained and significant growth in the coming years. The increasing demand for lightweight, durable, and corrosion-resistant materials across key sectors such as infrastructure, renewable energy, and advanced manufacturing will continue to be a primary growth accelerator. Technological advancements in production efficiency and material science are expected to further reduce costs and expand application possibilities. Strategic opportunities lie in developing customized solutions for niche markets and investing in research to enhance the sustainability and recyclability of carbon fiber composites, ensuring long-term market viability and environmental responsibility. The global shift towards greener technologies and infrastructure will further solidify the importance of carbon fiber tubes.

Carbon Fiber Tubes Segmentation

-

1. Application

- 1.1. Drinking Water

- 1.2. Chemical Handling

- 1.3. Gas Handling

- 1.4. Utilities Water

- 1.5. Other

-

2. Types

- 2.1. Diameter: 1/2 inch

- 2.2. Diameter: 2 inch

- 2.3. Diameter: 3 inch

- 2.4. Diameter: 4 inch

- 2.5. Diameter: Above 4 inch

Carbon Fiber Tubes Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Carbon Fiber Tubes Regional Market Share

Geographic Coverage of Carbon Fiber Tubes

Carbon Fiber Tubes REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Drinking Water

- 5.1.2. Chemical Handling

- 5.1.3. Gas Handling

- 5.1.4. Utilities Water

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Diameter: 1/2 inch

- 5.2.2. Diameter: 2 inch

- 5.2.3. Diameter: 3 inch

- 5.2.4. Diameter: 4 inch

- 5.2.5. Diameter: Above 4 inch

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Carbon Fiber Tubes Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Drinking Water

- 6.1.2. Chemical Handling

- 6.1.3. Gas Handling

- 6.1.4. Utilities Water

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Diameter: 1/2 inch

- 6.2.2. Diameter: 2 inch

- 6.2.3. Diameter: 3 inch

- 6.2.4. Diameter: 4 inch

- 6.2.5. Diameter: Above 4 inch

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Carbon Fiber Tubes Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Drinking Water

- 7.1.2. Chemical Handling

- 7.1.3. Gas Handling

- 7.1.4. Utilities Water

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Diameter: 1/2 inch

- 7.2.2. Diameter: 2 inch

- 7.2.3. Diameter: 3 inch

- 7.2.4. Diameter: 4 inch

- 7.2.5. Diameter: Above 4 inch

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Carbon Fiber Tubes Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Drinking Water

- 8.1.2. Chemical Handling

- 8.1.3. Gas Handling

- 8.1.4. Utilities Water

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Diameter: 1/2 inch

- 8.2.2. Diameter: 2 inch

- 8.2.3. Diameter: 3 inch

- 8.2.4. Diameter: 4 inch

- 8.2.5. Diameter: Above 4 inch

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Carbon Fiber Tubes Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Drinking Water

- 9.1.2. Chemical Handling

- 9.1.3. Gas Handling

- 9.1.4. Utilities Water

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Diameter: 1/2 inch

- 9.2.2. Diameter: 2 inch

- 9.2.3. Diameter: 3 inch

- 9.2.4. Diameter: 4 inch

- 9.2.5. Diameter: Above 4 inch

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Carbon Fiber Tubes Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Drinking Water

- 10.1.2. Chemical Handling

- 10.1.3. Gas Handling

- 10.1.4. Utilities Water

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Diameter: 1/2 inch

- 10.2.2. Diameter: 2 inch

- 10.2.3. Diameter: 3 inch

- 10.2.4. Diameter: 4 inch

- 10.2.5. Diameter: Above 4 inch

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Carbon Fiber Tubes Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Drinking Water

- 11.1.2. Chemical Handling

- 11.1.3. Gas Handling

- 11.1.4. Utilities Water

- 11.1.5. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Diameter: 1/2 inch

- 11.2.2. Diameter: 2 inch

- 11.2.3. Diameter: 3 inch

- 11.2.4. Diameter: 4 inch

- 11.2.5. Diameter: Above 4 inch

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Attwater Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Langtec

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tri-cast Composite Tubes

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ICE

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Carbon Fibre Tubes Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Guangzhou Shengrui Insulation Materials

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Exel Composites

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Forte Carbon Fiber Tubing

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Clearwater Composites

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Jiangsu Toptek Composite Materials

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Attwater Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Carbon Fiber Tubes Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Carbon Fiber Tubes Revenue (million), by Application 2025 & 2033

- Figure 3: North America Carbon Fiber Tubes Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Carbon Fiber Tubes Revenue (million), by Types 2025 & 2033

- Figure 5: North America Carbon Fiber Tubes Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Carbon Fiber Tubes Revenue (million), by Country 2025 & 2033

- Figure 7: North America Carbon Fiber Tubes Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Carbon Fiber Tubes Revenue (million), by Application 2025 & 2033

- Figure 9: South America Carbon Fiber Tubes Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Carbon Fiber Tubes Revenue (million), by Types 2025 & 2033

- Figure 11: South America Carbon Fiber Tubes Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Carbon Fiber Tubes Revenue (million), by Country 2025 & 2033

- Figure 13: South America Carbon Fiber Tubes Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Carbon Fiber Tubes Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Carbon Fiber Tubes Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Carbon Fiber Tubes Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Carbon Fiber Tubes Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Carbon Fiber Tubes Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Carbon Fiber Tubes Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Carbon Fiber Tubes Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Carbon Fiber Tubes Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Carbon Fiber Tubes Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Carbon Fiber Tubes Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Carbon Fiber Tubes Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Carbon Fiber Tubes Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Carbon Fiber Tubes Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Carbon Fiber Tubes Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Carbon Fiber Tubes Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Carbon Fiber Tubes Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Carbon Fiber Tubes Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Carbon Fiber Tubes Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Carbon Fiber Tubes Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Carbon Fiber Tubes Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Carbon Fiber Tubes Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Carbon Fiber Tubes Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Carbon Fiber Tubes Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Carbon Fiber Tubes Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Carbon Fiber Tubes Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Carbon Fiber Tubes Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Carbon Fiber Tubes Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Carbon Fiber Tubes?

The projected CAGR is approximately 14%.

2. Which companies are prominent players in the Carbon Fiber Tubes?

Key companies in the market include Attwater Group, Langtec, Tri-cast Composite Tubes, ICE, Carbon Fibre Tubes Ltd, Guangzhou Shengrui Insulation Materials, Exel Composites, Forte Carbon Fiber Tubing, Clearwater Composites, Jiangsu Toptek Composite Materials.

3. What are the main segments of the Carbon Fiber Tubes?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 715 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Carbon Fiber Tubes," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Carbon Fiber Tubes report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Carbon Fiber Tubes?

To stay informed about further developments, trends, and reports in the Carbon Fiber Tubes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence