Key Insights

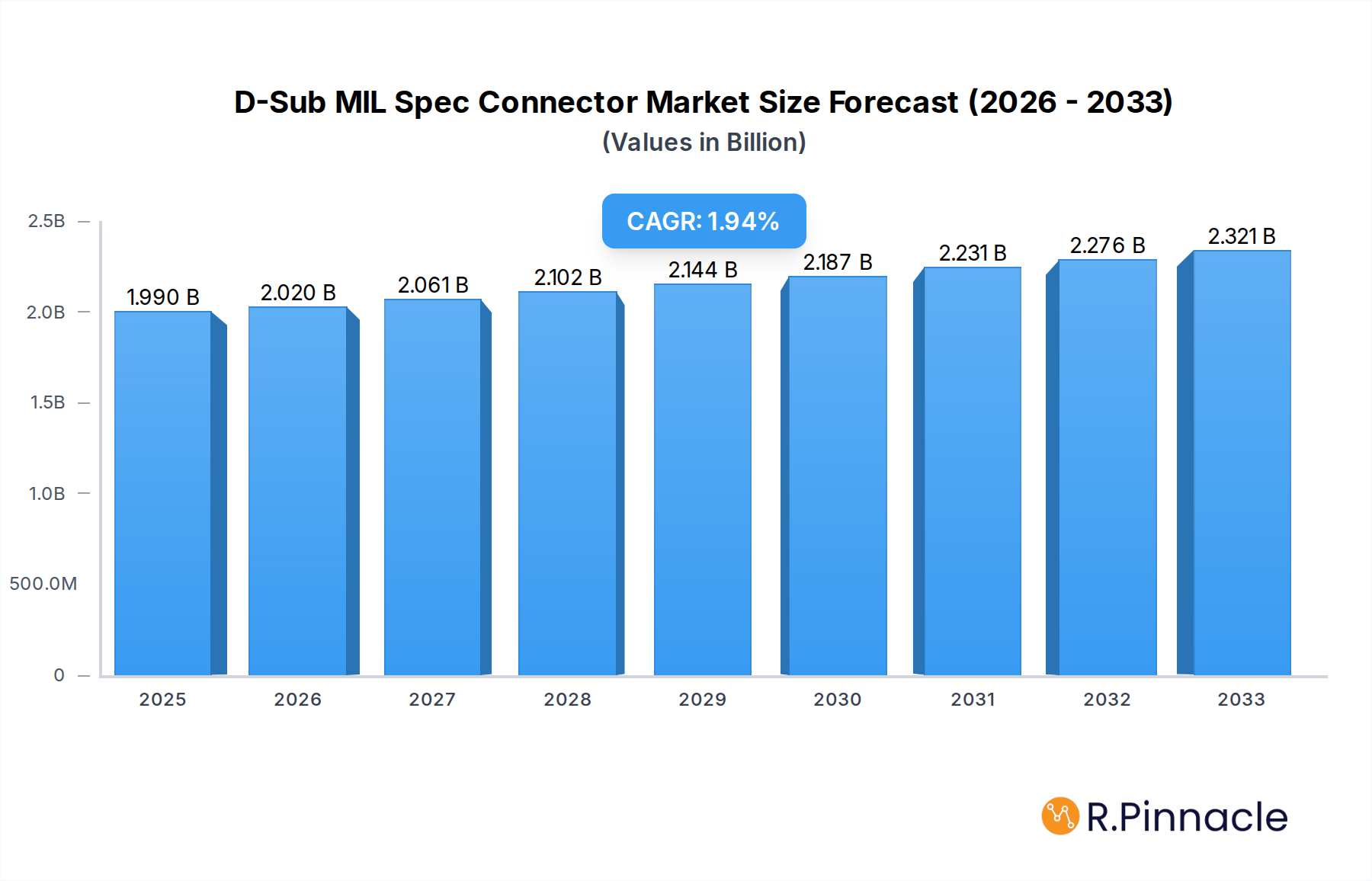

The D-Sub MIL-SPEC Connector market is poised for steady expansion, projected to reach USD 1.99 billion by 2025. This growth is underpinned by a CAGR of 2%, indicating a sustained and predictable upward trajectory for the industry over the forecast period. The military and aerospace sectors are the primary beneficiaries and drivers of this market, with significant demand emanating from Navy, Air Force, and Army applications. These applications necessitate robust, reliable, and high-performance connectivity solutions, where D-Sub MIL-SPEC connectors excel due to their established legacy, proven durability, and stringent adherence to military specifications. The ongoing modernization efforts within these defense branches, coupled with increasing global defense budgets, are fueling the demand for these critical components. Furthermore, advancements in materials and manufacturing processes are leading to the development of lighter, more efficient, and environmentally resistant connector variants, further solidifying their relevance.

D-Sub MIL Spec Connector Market Size (In Billion)

The market's trajectory is influenced by several key factors. Dominant growth drivers include the continuous need for advanced communication and data transfer systems in defense, alongside the replacement and upgrade cycles of existing military hardware. Trends such as miniaturization of electronic components, while presenting a challenge, also create opportunities for specialized miniature D-Sub MIL-SPEC connectors designed for space-constrained platforms. Conversely, restraints like the development of newer, potentially more advanced connector technologies and the high cost of MIL-SPEC certification can present hurdles. However, the inherent reliability and established infrastructure supporting D-Sub MIL-SPEC connectors ensure their continued dominance in critical military applications. Geographically, North America and Europe are expected to remain leading markets due to the substantial defense spending and established manufacturing bases, while the Asia Pacific region presents significant growth potential driven by increasing defense investments.

D-Sub MIL Spec Connector Company Market Share

This comprehensive report provides an in-depth analysis of the global D-Sub MIL Spec Connector market, a critical component in defense and aerospace applications. Leveraging billions in historical data and future projections, this study offers unparalleled insights into market dynamics, leading players, and emerging trends.

D-Sub MIL Spec Connector Market Structure & Innovation Trends

The D-Sub MIL Spec Connector market, while mature, exhibits dynamic characteristics driven by stringent defense and aerospace requirements. Market concentration is moderate, with a few dominant players like Amphenol, TE Connectivity, and ITT Cannon holding significant market share, estimated to be in the billions. However, the presence of specialized manufacturers such as AirBorn, C&K Switches, CW Industries, Glenair, HARTING, and Positronic fosters healthy competition and drives innovation. Regulatory frameworks, primarily driven by military specifications (MIL-DTL-24308 and its predecessors), dictate product design and performance, acting as both a barrier to entry and a benchmark for quality. Product substitutes are limited due to the critical reliability and ruggedness demanded in military environments, but advancements in alternative connector technologies are closely monitored. End-user demographics are overwhelmingly defense organizations and their prime contractors, with a focus on the Navy, Air Force, and Army segments. Mergers and acquisitions (M&A) activities, while not constant, are strategic, often aimed at consolidating technology portfolios or expanding geographical reach, with deal values often in the hundreds of millions. Innovation trends are geared towards miniaturization for space-constrained platforms, enhanced environmental resistance (e.g., extreme temperatures, vibration, EMI/RFI shielding), and integrated functionalities.

D-Sub MIL Spec Connector Market Dynamics & Trends

The global D-Sub MIL Spec Connector market is experiencing steady growth, projected to continue its upward trajectory throughout the forecast period. The primary growth driver is the persistent demand from the defense sector for reliable and robust connectivity solutions for a wide array of military platforms, including aircraft, naval vessels, ground vehicles, and communication systems. This demand is further fueled by ongoing modernization programs and the increasing complexity of defense electronics. Technological disruptions, while less frequent than in consumer electronics, are focused on enhancing performance characteristics such as higher signal integrity, increased power handling capabilities, and improved electromagnetic compatibility (EMC). The market penetration of D-Sub MIL Spec Connectors remains high within their specialized application niches due to their proven track record and established reliability. Consumer preferences, in this context, translate to rigorous qualification processes and a strong emphasis on product longevity and performance under extreme conditions. Competitive dynamics are characterized by a blend of established giants and specialized niche players, each vying for contracts through product innovation, superior quality, and competitive pricing. The market size is estimated to be in the billions, with a Compound Annual Growth Rate (CAGR) projected to be in the low single digits, reflecting the maturity of the technology but also its indispensable nature. The shift towards smaller, lighter, and more ruggedized components, driven by the need for advanced avionics and sensor integration, is a significant trend shaping market dynamics. Furthermore, the increasing adoption of digitalization and networked warfare necessitates connectors that can support higher bandwidth and data transfer rates, even in harsh environments.

Dominant Regions & Segments in D-Sub MIL Spec Connector

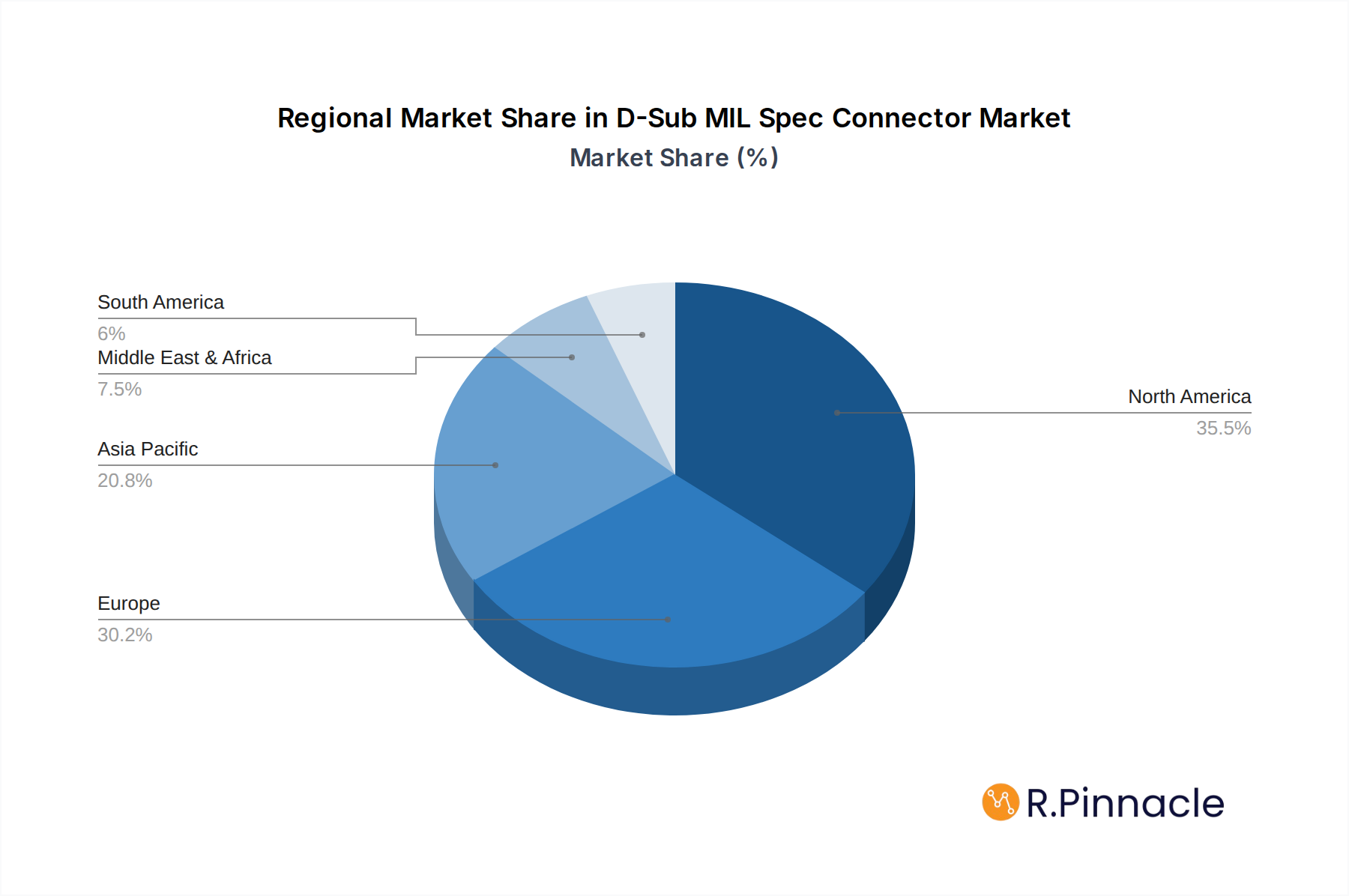

The North America region, particularly the United States, stands as the dominant force in the global D-Sub MIL Spec Connector market. This dominance is underpinned by the substantial defense spending of the U.S. government, its extensive military infrastructure, and the presence of leading defense contractors.

Application Segment Dominance (Navy, Air Force, Army):

- Navy: The U.S. Navy's vast fleet of aircraft carriers, submarines, destroyers, and littoral combat ships requires a continuous supply of robust and reliable connectors for critical systems, including combat management, sonar, navigation, and communication. Investment in naval modernization programs further bolsters this demand.

- Air Force: The U.S. Air Force's advanced fighter jets, bombers, transport aircraft, and surveillance platforms necessitate high-performance D-Sub MIL Spec Connectors for avionics, radar systems, electronic warfare suites, and cockpit controls. Ongoing upgrades to existing fleets and development of new aerial platforms contribute significantly to market growth.

- Army: The U.S. Army's ground forces, encompassing tanks, armored vehicles, communication systems, and field equipment, rely heavily on ruggedized D-Sub MIL Spec Connectors for their operational integrity. The development of networked battlefield capabilities and the deployment of advanced sensor technologies amplify this demand.

Type Segment Dominance (Miniature, Standard):

- Standard D-Sub Connectors: While miniaturization is a growing trend, standard D-Sub connectors continue to hold a significant market share due to their established reliability and cost-effectiveness in applications where space is not the primary constraint. These are prevalent in legacy systems and larger equipment.

- Miniature D-Sub Connectors: The increasing demand for compact and lightweight solutions in modern military platforms, especially in avionics, portable communication devices, and unmanned aerial vehicles (UAVs), is driving the growth of the miniature D-Sub connector segment. These often incorporate advanced features for enhanced performance in smaller footprints.

Economic policies favoring defense procurement, robust R&D investments in military technology, and a strong ecosystem of manufacturers and suppliers contribute to North America's leadership. Countries like the United Kingdom, Germany, and France in Europe, and China and India in Asia-Pacific, represent significant and growing markets, driven by their own defense modernization initiatives and regional security concerns.

D-Sub MIL Spec Connector Product Innovations

Product innovations in the D-Sub MIL Spec Connector market are primarily focused on enhancing performance and reliability in demanding military environments. This includes the development of connectors with improved environmental sealing against moisture, dust, and extreme temperatures, as well as superior shielding against electromagnetic interference (EMI) and radio-frequency interference (RFI). Miniaturization of existing designs, allowing for higher pin densities in smaller form factors, is another key trend, addressing the need for space-saving solutions in modern avionics and portable equipment. Furthermore, advancements in materials science are leading to the use of more robust and lightweight alloys, improving durability and reducing the overall weight of military platforms. These innovations provide a competitive advantage by meeting evolving military specifications and enabling the integration of more advanced electronic systems.

Report Scope & Segmentation Analysis

This report encompasses a thorough analysis of the D-Sub MIL Spec Connector market, segmented by critical application areas and connector types. The study includes detailed projections and market size estimations for each segment, alongside an examination of competitive dynamics within these specific niches.

Application Segments:

- Navy: Projected to show consistent growth driven by naval modernization programs and the need for robust connectivity in maritime environments. Market size estimated to be in the hundreds of millions, with a steady CAGR.

- Air Force: Expected to experience strong growth due to advancements in avionics, electronic warfare systems, and the development of new aerial platforms. Market size in the billions, with a moderate CAGR.

- Army: Anticipated to witness steady growth, fueled by the digitization of the battlefield and the demand for reliable connectivity in ground-based systems. Market size in the hundreds of millions, with a consistent CAGR.

Type Segments:

- Miniature: Projected to exhibit the highest growth rate due to the increasing demand for compact and lightweight solutions in modern military hardware. Market size in the hundreds of millions, with a significant CAGR.

- Standard: Expected to maintain stable growth, serving legacy systems and applications where space is not a primary concern. Market size in the hundreds of millions, with a moderate CAGR.

Key Drivers of D-Sub MIL Spec Connector Growth

The D-Sub MIL Spec Connector market is propelled by several key drivers:

- Technological: Ongoing advancements in military hardware, including the integration of sophisticated avionics, sensor systems, and communication networks, necessitate high-performance and reliable connectors. The push for miniaturization and enhanced environmental ruggedness is a significant factor.

- Economic: Robust defense budgets in major economies worldwide, coupled with ongoing geopolitical tensions, drive sustained investment in military modernization and procurement programs, directly impacting connector demand.

- Regulatory: Stringent military specifications (MIL-SPEC) mandate the use of highly reliable and tested connectors, creating a barrier to entry for inferior products and ensuring continued demand for compliant D-Sub connectors. The need to adhere to evolving standards for interoperability and future-proofing also drives demand.

Challenges in the D-Sub MIL Spec Connector Sector

Despite strong growth prospects, the D-Sub MIL Spec Connector sector faces several challenges:

- Regulatory Hurdles: While driving quality, the complex and ever-evolving MIL-SPEC standards can be costly and time-consuming to meet, posing a challenge for smaller manufacturers.

- Supply Chain Vulnerabilities: The global nature of the electronics supply chain, coupled with geopolitical uncertainties, can lead to disruptions in the availability of raw materials and components, impacting production timelines and costs.

- Competitive Pressures: While niche, competition from manufacturers of alternative connector technologies, and even the continuous innovation within the D-Sub space itself, requires significant R&D investment to maintain market share. The increasing demand for higher bandwidth solutions also presents a challenge for traditional D-Sub designs.

Emerging Opportunities in D-Sub MIL Spec Connector

The D-Sub MIL Spec Connector market presents several promising emerging opportunities:

- Advanced Materials: The development and adoption of new, lighter, and more durable materials for connector housings and contacts can lead to enhanced performance and reduced weight for military platforms.

- Smart Connectors: Integration of embedded intelligence, such as self-diagnostic capabilities or active signal conditioning within connectors, could offer significant advantages in complex military systems.

- Niche Defense Applications: The increasing use of unmanned systems (UAVs, UGVs), directed energy weapons, and advanced ISR (Intelligence, Surveillance, and Reconnaissance) platforms creates new demand for specialized, high-performance D-Sub connectors.

- Cybersecurity Integration: Developing connectors with inherent cybersecurity features to protect sensitive data transmission in networked military environments is a burgeoning opportunity.

Leading Players in the D-Sub MIL Spec Connector Market

- Amphenol

- AirBorn

- C&K Switches

- CW Industries

- TE Connectivity

- Glenair

- HARTING

- ITT Cannon

- Positronic

Key Developments in D-Sub MIL Spec Connector Industry

- 2023 Q4: Amphenol announces the launch of a new series of high-density MIL-DTL-38999 Series III connectors featuring advanced sealing technology for enhanced environmental protection.

- 2024 Q1: TE Connectivity acquires a specialized connector manufacturer, expanding its portfolio in ruggedized solutions for aerospace applications, with an estimated deal value in the hundreds of millions.

- 2024 Q2: Glenair introduces a new range of lightweight and corrosion-resistant D-Sub connectors specifically designed for naval applications, focusing on improved salt spray resistance.

- 2024 Q3: ITT Cannon secures a multi-year contract, valued in the billions, to supply D-Sub MIL Spec Connectors for a new generation of fighter aircraft platforms for a major defense contractor.

Future Outlook for D-Sub MIL Spec Connector Market

The future outlook for the D-Sub MIL Spec Connector market remains robust, driven by continued global defense spending and the persistent need for reliable connectivity in critical military applications. The emphasis on advanced technologies, such as miniaturization, increased ruggedness, and enhanced signal integrity, will continue to shape product development. Emerging opportunities in smart connectors and specialized defense platforms offer significant growth potential. Strategic investments in R&D, a focus on supply chain resilience, and the ability to adapt to evolving military specifications will be crucial for market players to maintain their competitive edge and capitalize on the evolving landscape of defense and aerospace technology. The market is projected to sustain its upward trend, with continued innovation playing a pivotal role in defining its trajectory.

D-Sub MIL Spec Connector Segmentation

-

1. Application

- 1.1. Navy

- 1.2. Air Force

- 1.3. Army

-

2. Types

- 2.1. Miniature

- 2.2. Standard

D-Sub MIL Spec Connector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

D-Sub MIL Spec Connector Regional Market Share

Geographic Coverage of D-Sub MIL Spec Connector

D-Sub MIL Spec Connector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Navy

- 5.1.2. Air Force

- 5.1.3. Army

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Miniature

- 5.2.2. Standard

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Navy

- 6.1.2. Air Force

- 6.1.3. Army

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Miniature

- 6.2.2. Standard

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Navy

- 7.1.2. Air Force

- 7.1.3. Army

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Miniature

- 7.2.2. Standard

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Navy

- 8.1.2. Air Force

- 8.1.3. Army

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Miniature

- 8.2.2. Standard

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Navy

- 9.1.2. Air Force

- 9.1.3. Army

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Miniature

- 9.2.2. Standard

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific D-Sub MIL Spec Connector Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Navy

- 10.1.2. Air Force

- 10.1.3. Army

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Miniature

- 10.2.2. Standard

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Amphenol

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AirBorn

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 C&K Switches

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CW Industries

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 TE Connectivity

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Glenair

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 HARTING

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ITT Cannon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Positronic

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Amphenol

List of Figures

- Figure 1: Global D-Sub MIL Spec Connector Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America D-Sub MIL Spec Connector Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America D-Sub MIL Spec Connector Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America D-Sub MIL Spec Connector Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America D-Sub MIL Spec Connector Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America D-Sub MIL Spec Connector Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America D-Sub MIL Spec Connector Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America D-Sub MIL Spec Connector Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America D-Sub MIL Spec Connector Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America D-Sub MIL Spec Connector Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America D-Sub MIL Spec Connector Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America D-Sub MIL Spec Connector Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America D-Sub MIL Spec Connector Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe D-Sub MIL Spec Connector Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe D-Sub MIL Spec Connector Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe D-Sub MIL Spec Connector Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe D-Sub MIL Spec Connector Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe D-Sub MIL Spec Connector Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe D-Sub MIL Spec Connector Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa D-Sub MIL Spec Connector Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa D-Sub MIL Spec Connector Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa D-Sub MIL Spec Connector Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa D-Sub MIL Spec Connector Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa D-Sub MIL Spec Connector Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa D-Sub MIL Spec Connector Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific D-Sub MIL Spec Connector Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific D-Sub MIL Spec Connector Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific D-Sub MIL Spec Connector Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific D-Sub MIL Spec Connector Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific D-Sub MIL Spec Connector Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific D-Sub MIL Spec Connector Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global D-Sub MIL Spec Connector Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific D-Sub MIL Spec Connector Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the D-Sub MIL Spec Connector?

The projected CAGR is approximately 2%.

2. Which companies are prominent players in the D-Sub MIL Spec Connector?

Key companies in the market include Amphenol, AirBorn, C&K Switches, CW Industries, TE Connectivity, Glenair, HARTING, ITT Cannon, Positronic.

3. What are the main segments of the D-Sub MIL Spec Connector?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "D-Sub MIL Spec Connector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the D-Sub MIL Spec Connector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the D-Sub MIL Spec Connector?

To stay informed about further developments, trends, and reports in the D-Sub MIL Spec Connector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence