Key Insights

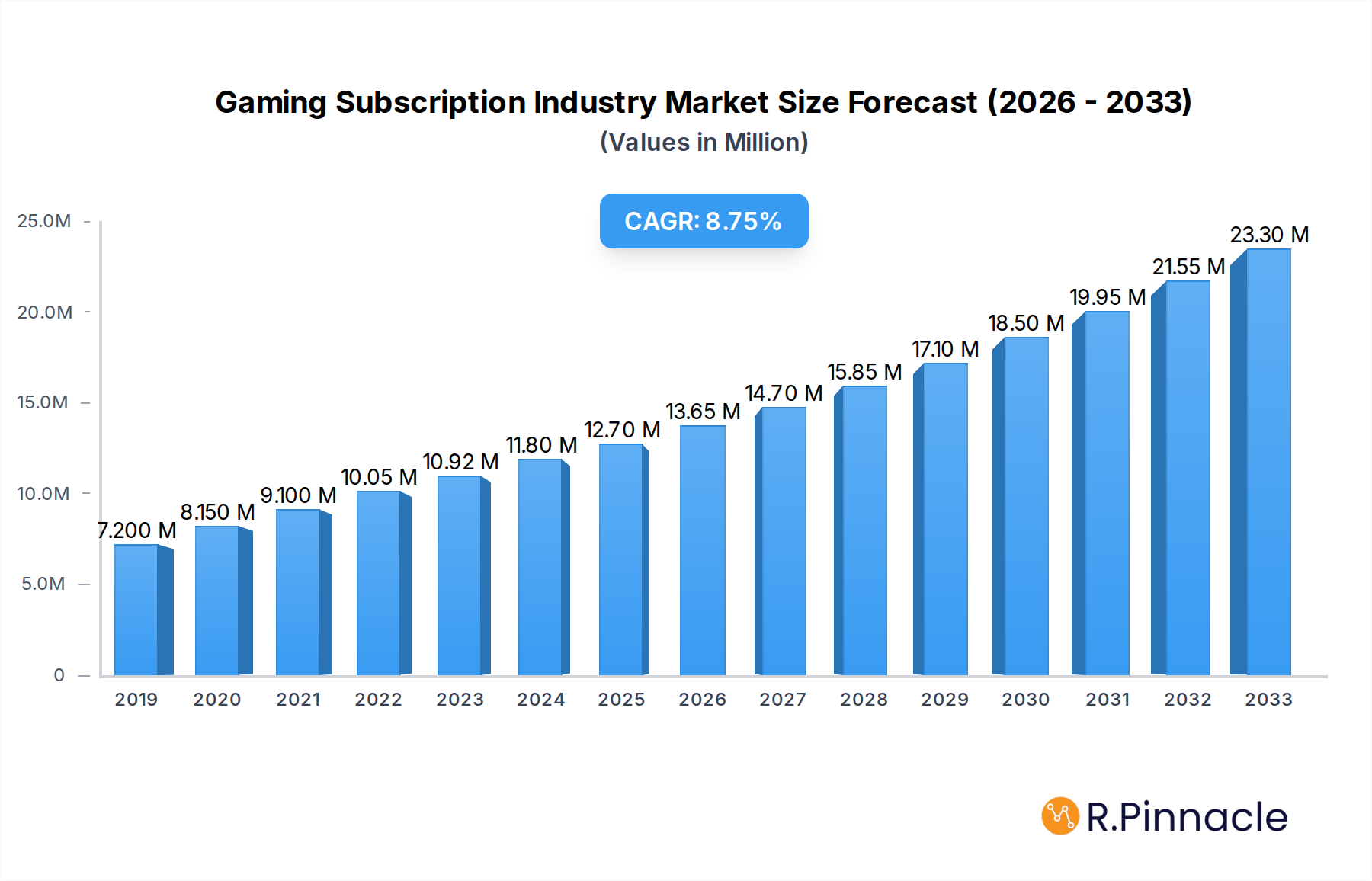

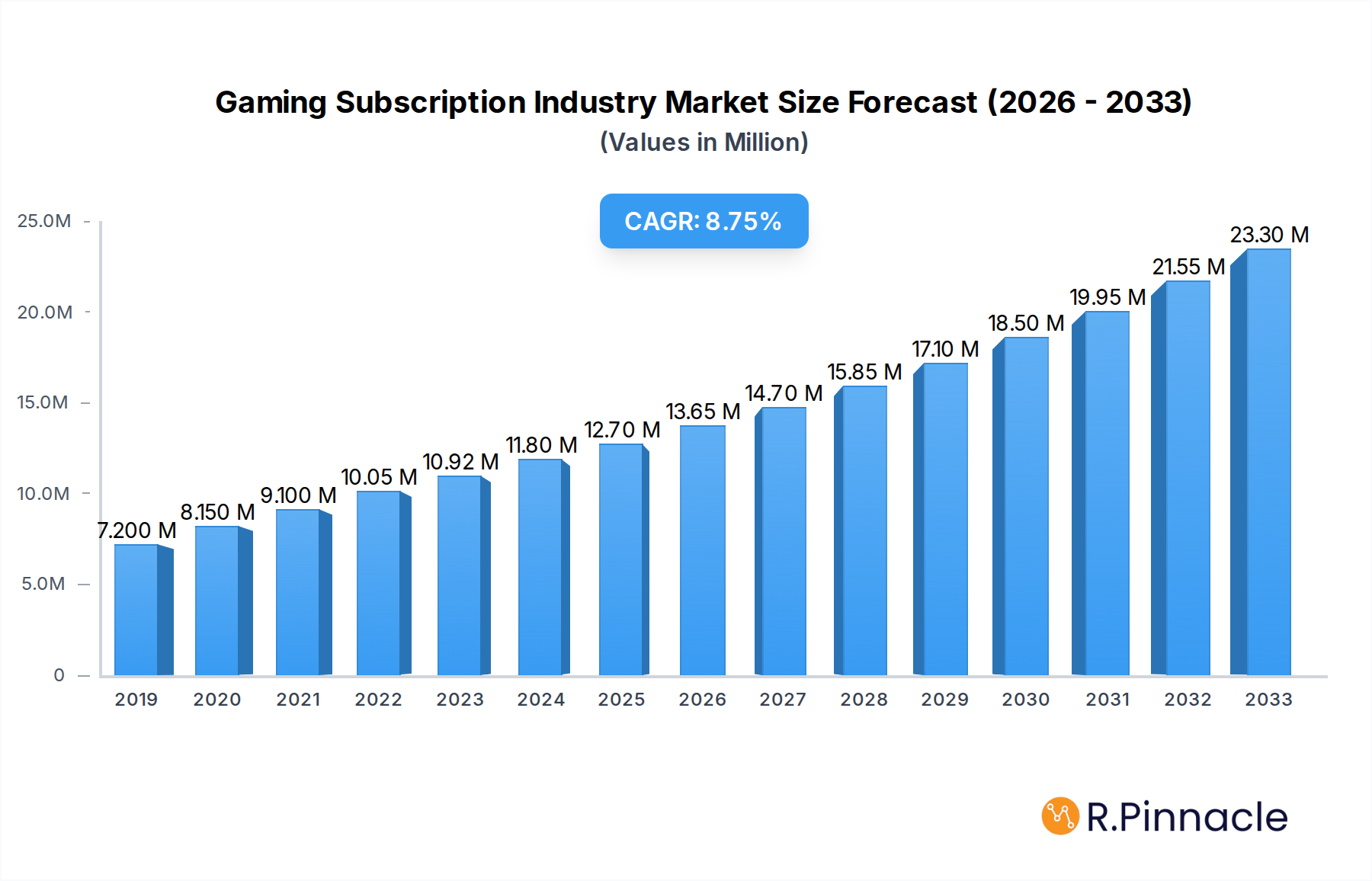

The global gaming subscription industry is poised for significant expansion, with a current market size estimated at $10.92 billion. Projections indicate a robust compound annual growth rate (CAGR) of 9.84% during the study period of 2019-2033, suggesting a dynamic and expanding market. This growth is fueled by several key drivers, including the increasing adoption of cloud gaming, the proliferation of mobile devices as primary gaming platforms, and the growing demand for diverse and accessible gaming content. The convenience and cost-effectiveness of subscription models, which offer access to a vast library of games for a recurring fee, are particularly appealing to a broad spectrum of gamers, from casual players to dedicated enthusiasts. Furthermore, the evolving landscape of digital distribution and the strategic investments by major players like Microsoft, Sony, Amazon, and Nintendo are instrumental in shaping the market's trajectory, pushing innovation and expanding subscription offerings.

Gaming Subscription Industry Market Size (In Million)

The industry's expansion is also being shaped by emerging trends such as the integration of subscription services with broader entertainment ecosystems, exemplified by platforms like Prime Gaming. The increasing sophistication of cloud gaming technology is democratizing access to high-fidelity gaming experiences, breaking down hardware barriers and attracting new user segments. However, the market also faces certain restraints. High initial investment costs for developing and maintaining extensive game libraries, coupled with the potential for subscription fatigue among consumers bombarded with numerous service options, present challenges. Intense competition among established players and the constant need to secure exclusive content to retain subscribers are critical factors influencing market dynamics. The market is segmented into Console Gaming, PC-based Gaming, and Mobile Gaming, each with its unique growth patterns and consumer preferences, contributing to the overall industry's multifaceted development.

Gaming Subscription Industry Company Market Share

Dive deep into the dynamic gaming subscription industry with this definitive market analysis. Covering the historical period (2019–2024), base year (2025), and forecast period (2025–2033), this report provides unparalleled insights into market structure, dynamics, dominant regions, and groundbreaking product innovations. Essential for industry professionals, investors, and stakeholders seeking to capitalize on the booming game-as-a-service (GaaS) model. Discover growth drivers, emerging opportunities, and key challenges shaping the global gaming subscription market. Leverage high-ranking keywords such as console gaming, PC-based gaming, mobile gaming, cloud gaming, game streaming, and subscription services.

Gaming Subscription Industry Market Structure & Innovation Trends

The gaming subscription industry exhibits a moderately concentrated market structure, driven by significant investments from major technology and gaming giants. Innovation is predominantly fueled by the continuous release of new game titles, enhanced streaming technologies, and tiered subscription offerings designed to capture diverse consumer segments. Regulatory frameworks are evolving, focusing on data privacy and fair competition, particularly as cloud gaming services expand. Product substitutes, including direct game purchases and free-to-play models, present ongoing competition, though subscription models offer predictable revenue streams. End-user demographics are broadening, encompassing a wider age range and geographical distribution. Mergers and acquisitions (M&A) activities remain a key strategy for market consolidation and expansion, with notable deal values in the tens of millions impacting market share.

- Market Concentration: Dominated by a few key players with substantial market share, but with increasing fragmentation driven by niche subscription services.

- Innovation Drivers: New game releases, cloud infrastructure advancements, AI-driven personalization, and exclusive content partnerships.

- Regulatory Frameworks: Evolving regulations around data privacy, age restrictions, and anti-monopoly concerns.

- Product Substitutes: Traditional game purchases, free-to-play titles, and rental services.

- End-User Demographics: Skewing younger but with increasing adoption among casual and older gamers.

- M&A Activities: Strategic acquisitions aimed at expanding content libraries, user bases, and technological capabilities. Deal values in the hundreds of millions have been observed.

Gaming Subscription Industry Market Dynamics & Trends

The gaming subscription industry is experiencing robust growth, propelled by several key market growth drivers. The increasing penetration of high-speed internet and the proliferation of affordable gaming-capable devices, including smartphones and consoles, have democratized access to gaming. Technological disruptions, particularly in cloud gaming and game streaming technologies, are redefining how consumers access and play games, eliminating the need for expensive hardware. This shift is significantly influencing consumer preferences, with an increasing demand for flexible, all-you-can-play access to vast game libraries over outright ownership. The competitive dynamics are intensifying, with established players like Microsoft's Xbox Game Pass, Sony's PlayStation Now (evolving into PlayStation Plus), and Nintendo Switch Online fiercely vying for subscriber loyalty. Amazon's Prime Gaming and Luna, Google Play Pass, Apple Arcade, and EA Play are also key contributors to this competitive landscape. The CAGR is projected to remain strong, estimated in the high teens over the forecast period. Market penetration is rapidly increasing, particularly in developed regions, with tens of millions of new subscribers expected annually. The ongoing evolution of the PC-based gaming segment, alongside the continued dominance of console gaming and the explosive growth of mobile gaming subscriptions, creates a multifaceted market.

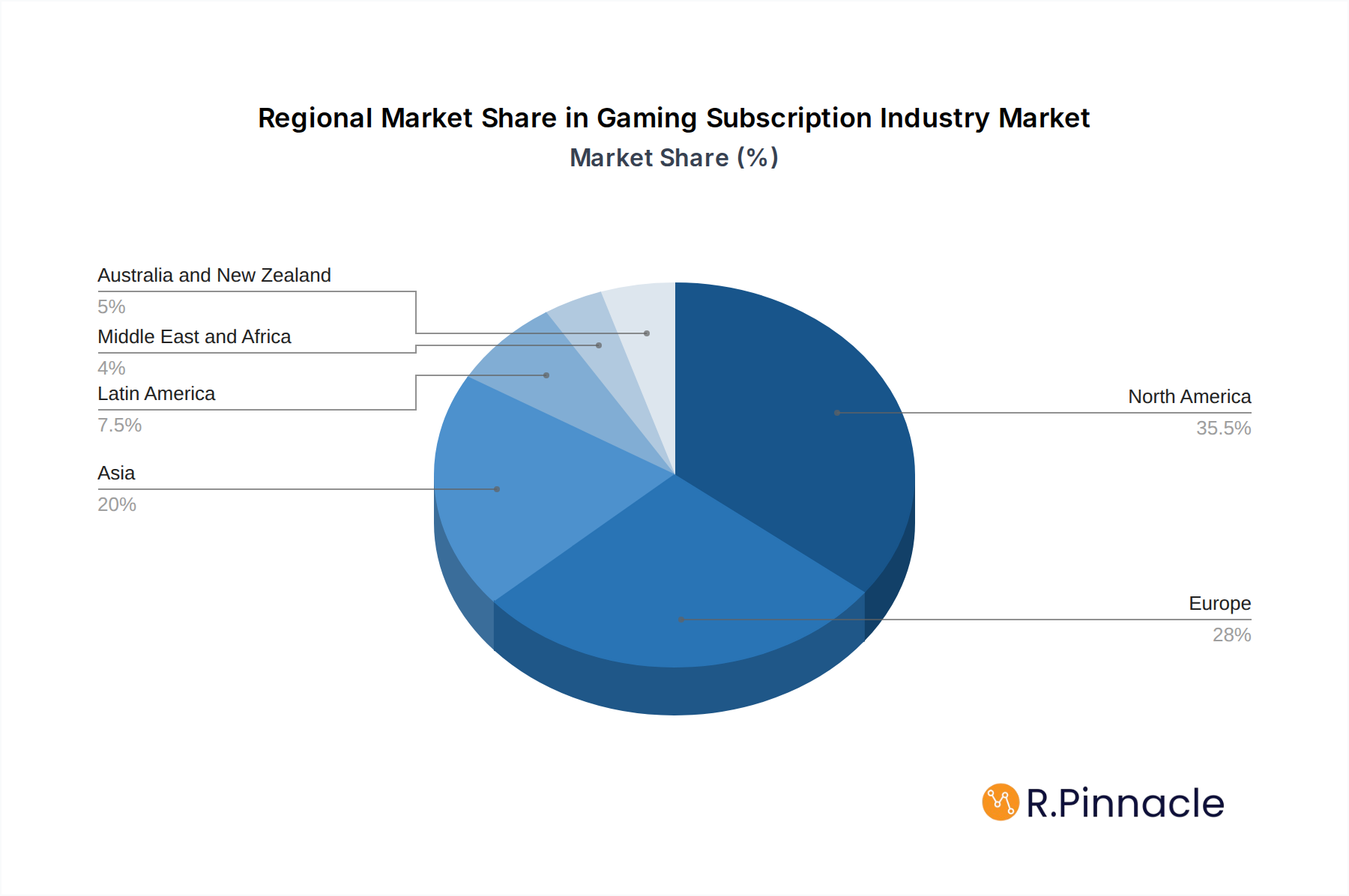

Dominant Regions & Segments in Gaming Subscription Industry

North America currently holds a dominant position in the gaming subscription industry, driven by high disposable incomes, advanced digital infrastructure, and a deeply ingrained gaming culture. The United States, in particular, represents a significant market due to its large population of avid gamers and early adoption of subscription services.

- Console Gaming: Remains a cornerstone of the subscription market, with services like Xbox Game Pass and PlayStation Plus offering extensive libraries of AAA titles. The convenience of accessing a vast collection of games without individual purchases fuels its dominance.

- PC-based Gaming: Shows significant growth, fueled by platforms like Epic Games Store and NVIDIA's GeForce Now, offering flexibility and access to a wide range of PC titles. The ability to play games on multiple devices and the increasing power of PCs contribute to its strong performance.

- Mobile Gaming: Presents the most explosive growth potential. Services like Google Play Pass and Apple Arcade cater to the massive global mobile gaming audience, offering a curated selection of ad-free and in-app purchase-free experiences. The low barrier to entry for mobile devices makes this segment highly accessible.

Economic policies supporting digital entertainment, robust internet infrastructure, and a strong ecosystem of game developers and publishers are key drivers of regional dominance. The Asia-Pacific region, particularly China and South Korea, is rapidly emerging as a significant growth engine, driven by the vast player base and the rise of Tencent Holdings Ltd.

Gaming Subscription Industry Product Innovations

Product innovations in the gaming subscription industry are centered on enhancing user experience and expanding content accessibility. Services are increasingly offering exclusive titles, day-one releases, and bundled content, creating strong competitive advantages. The integration of cloud gaming technology allows for seamless play across various devices without the need for powerful hardware, broadening the appeal of subscription models. Technological advancements in streaming quality, reduced latency, and AI-driven content recommendations are further refining the market fit for these services. The competitive landscape is pushing companies to differentiate through unique features and exclusive partnerships, ensuring sustained market relevance.

Report Scope & Segmentation Analysis

This report meticulously analyzes the gaming subscription industry across key segments:

- Console Gaming: This segment focuses on subscription services tied to gaming consoles. It encompasses offerings that provide access to a library of games playable on platforms like Xbox, PlayStation, and Nintendo Switch. Projections indicate steady growth, with market sizes in the billions of dollars, driven by exclusive content and bundled hardware deals.

- PC-based Gaming: This segment covers subscriptions for PC gaming, including access to game libraries, cloud streaming services, and digital storefront benefits. The market is expected to witness substantial expansion, with market sizes reaching tens of billions of dollars, fueled by the flexibility and power of PCs.

- Mobile Gaming: This segment targets subscription services for mobile devices. It includes curated app stores and game collections optimized for smartphones and tablets. This segment is poised for the most rapid growth, with market sizes projected to exceed hundreds of billions of dollars due to the vast global user base.

Key Drivers of Gaming Subscription Industry Growth

The gaming subscription industry is propelled by several powerful growth drivers. The increasing affordability and accessibility of internet connectivity globally, particularly high-speed broadband, is fundamental. The proliferation of smartphones and other internet-enabled devices has created a massive potential user base. Technological advancements, especially in cloud gaming and streaming technology, are lowering the barrier to entry for playing high-fidelity games. Furthermore, the evolving consumer preference for access over ownership, driven by a desire for variety and value, significantly boosts subscription models. Major players like Microsoft with Xbox Game Pass and Sony with their revamped PlayStation Plus are investing heavily, introducing exclusive content and aggressive pricing strategies that further stimulate growth. Economic policies favoring digital content consumption and a robust digital payments infrastructure also play a crucial role.

Challenges in the Gaming Subscription Industry Sector

Despite its rapid growth, the gaming subscription industry faces significant challenges. Intense competitive pressure from numerous players, including established giants and emerging startups, leads to subscriber acquisition costs that can reach hundreds of dollars per user. The increasing cost of game development, with AAA titles costing upwards of hundreds of millions of dollars, puts pressure on profitability and the ability to offer compelling value. Regulatory hurdles related to data privacy, content moderation, and potential monopolistic practices are also a concern. Ensuring consistent and high-quality streaming for cloud gaming services across diverse network conditions remains a technical challenge. Furthermore, subscriber churn, driven by a lack of fresh content or dissatisfaction with existing offerings, can impact revenue predictability. The need for continuous investment in new games and technology represents a substantial ongoing financial commitment.

Emerging Opportunities in Gaming Subscription Industry

Emerging opportunities within the gaming subscription industry are vast and varied. The untapped potential in developing economies, with their rapidly growing middle class and increasing smartphone penetration, presents a significant expansion frontier. The integration of augmented reality (AR) and virtual reality (VR) into subscription models could unlock entirely new immersive gaming experiences. Niche subscription services catering to specific genres or demographics, such as retro gaming or educational gaming, can capture dedicated audiences. The growing trend of cross-platform play and cross-progression further enhances the value proposition of subscription services, allowing players to seamlessly switch between devices. Partnerships with hardware manufacturers and mobile carriers can also create unique bundled offerings and expand reach. The increasing demand for live-service games and esports integration within subscription platforms offers further avenues for engagement and monetization, potentially generating revenue in the billions of dollars annually.

Leading Players in the Gaming Subscription Industry Market

- Microsoft Corporation

- Sony Corporation

- Nintendo Co Ltd

- Amazon Inc

- Google LLC

- Electronic Arts Inc

- Apple Inc

- Tencent Holdings Ltd

- Ubisoft

- NVIDIA

- Epic games Inc

- Humble Bundle Inc

Key Developments in Gaming Subscription Industry Industry

- March 2022: Nintendo Switch Online (Nintendo Co. Ltd) announced new additions to its library, including three Sega Genesis games: Light Crusader, Super Fantasy Zone, and Alien Soldier. This move aims to enhance the value proposition for existing subscribers and attract new ones.

- March 2022: Google Play Pass (Google LLC) began its rollout to Android devices in India. This expansion offers users access to a curated collection of over 1000 titles across 41 categories, sourced from developers in 59 countries, including India, providing a significant boost to mobile gaming accessibility.

Future Outlook for Gaming Subscription Industry Market

The future outlook for the gaming subscription industry is exceptionally bright, characterized by sustained growth and evolving business models. Continued innovation in cloud gaming technology will further democratize access, breaking down hardware barriers and expanding the global addressable market, potentially to hundreds of millions of new users. The increasing demand for high-quality, curated content will drive further investment in exclusive titles and partnerships, creating stronger subscriber loyalty. Emerging markets represent significant growth accelerators, offering vast untapped potential. The integration of AI for personalized recommendations and player experiences will become more sophisticated, enhancing engagement. Strategic acquisitions and collaborations will continue to shape the competitive landscape, leading to more comprehensive service offerings. The industry is poised for substantial expansion, with market values projected to reach hundreds of billions of dollars by the end of the forecast period, driven by technological advancements and shifting consumer preferences towards subscription-based entertainment.

Gaming Subscription Industry Segmentation

-

1. Gaming Type

- 1.1. Console Gaming

- 1.2. PC-based Gaming

- 1.3. Mobile Gaming

Gaming Subscription Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Gaming Subscription Industry Regional Market Share

Geographic Coverage of Gaming Subscription Industry

Gaming Subscription Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Gaming Type

- 5.1.1. Console Gaming

- 5.1.2. PC-based Gaming

- 5.1.3. Mobile Gaming

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia

- 5.2.4. Australia and New Zealand

- 5.2.5. Latin America

- 5.2.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Gaming Type

- 6. Global Gaming Subscription Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Gaming Type

- 6.1.1. Console Gaming

- 6.1.2. PC-based Gaming

- 6.1.3. Mobile Gaming

- 6.1. Market Analysis, Insights and Forecast - by Gaming Type

- 7. North America Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Gaming Type

- 7.1.1. Console Gaming

- 7.1.2. PC-based Gaming

- 7.1.3. Mobile Gaming

- 7.1. Market Analysis, Insights and Forecast - by Gaming Type

- 8. Europe Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Gaming Type

- 8.1.1. Console Gaming

- 8.1.2. PC-based Gaming

- 8.1.3. Mobile Gaming

- 8.1. Market Analysis, Insights and Forecast - by Gaming Type

- 9. Asia Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Gaming Type

- 9.1.1. Console Gaming

- 9.1.2. PC-based Gaming

- 9.1.3. Mobile Gaming

- 9.1. Market Analysis, Insights and Forecast - by Gaming Type

- 10. Australia and New Zealand Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Gaming Type

- 10.1.1. Console Gaming

- 10.1.2. PC-based Gaming

- 10.1.3. Mobile Gaming

- 10.1. Market Analysis, Insights and Forecast - by Gaming Type

- 11. Latin America Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Gaming Type

- 11.1.1. Console Gaming

- 11.1.2. PC-based Gaming

- 11.1.3. Mobile Gaming

- 11.1. Market Analysis, Insights and Forecast - by Gaming Type

- 12. Middle East and Africa Gaming Subscription Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Gaming Type

- 12.1.1. Console Gaming

- 12.1.2. PC-based Gaming

- 12.1.3. Mobile Gaming

- 12.1. Market Analysis, Insights and Forecast - by Gaming Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Nintendo Switch Online (Nintendo Co Ltd)

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Prime Gaming (Amazon Inc )*List Not Exhaustive

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Google Play Pass (Google LLC)

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Humble Bundle Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Amazon Luna (Amazon Inc )

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 PlayStation Now (Sony Corporation)

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 EA Play (Electronic Arts Inc )

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Tencent Holdings Ltd

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Uplay Pass (Ubisoft)

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Xbox (Game Pass) (Microsoft Corporation)

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Epic games Inc

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 GeForce Now (NVIDIA)

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Apple Arcade (Apple Inc )

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.1 Nintendo Switch Online (Nintendo Co Ltd)

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Gaming Subscription Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 3: North America Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 4: North America Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 7: Europe Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 8: Europe Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 11: Asia Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 12: Asia Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Australia and New Zealand Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 15: Australia and New Zealand Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 16: Australia and New Zealand Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Australia and New Zealand Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Latin America Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 19: Latin America Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 20: Latin America Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Latin America Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Middle East and Africa Gaming Subscription Industry Revenue (Million), by Gaming Type 2025 & 2033

- Figure 23: Middle East and Africa Gaming Subscription Industry Revenue Share (%), by Gaming Type 2025 & 2033

- Figure 24: Middle East and Africa Gaming Subscription Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Gaming Subscription Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 2: Global Gaming Subscription Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 4: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 6: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 8: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 10: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 12: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Gaming Subscription Industry Revenue Million Forecast, by Gaming Type 2020 & 2033

- Table 14: Global Gaming Subscription Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming Subscription Industry?

The projected CAGR is approximately 9.84%.

2. Which companies are prominent players in the Gaming Subscription Industry?

Key companies in the market include Nintendo Switch Online (Nintendo Co Ltd), Prime Gaming (Amazon Inc )*List Not Exhaustive, Google Play Pass (Google LLC), Humble Bundle Inc, Amazon Luna (Amazon Inc ), PlayStation Now (Sony Corporation), EA Play (Electronic Arts Inc ), Tencent Holdings Ltd, Uplay Pass (Ubisoft), Xbox (Game Pass) (Microsoft Corporation), Epic games Inc, GeForce Now (NVIDIA), Apple Arcade (Apple Inc ).

3. What are the main segments of the Gaming Subscription Industry?

The market segments include Gaming Type .

4. Can you provide details about the market size?

The market size is estimated to be USD 10.92 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Tools to Make Work Seamless and Agile; Continuous Innovation in Team Collaborative Tool Offerings.

6. What are the notable trends driving market growth?

Mobile gaming to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Compliance and Governance Issues.

8. Can you provide examples of recent developments in the market?

March 2022- The Nintendo Switch Online (Nintendo Co. Ltd) announced new additions that include three Sega Genesis games. Light Crusader, Super Fantasy Zone, and Alien Soldier are among the most recent additions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gaming Subscription Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gaming Subscription Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gaming Subscription Industry?

To stay informed about further developments, trends, and reports in the Gaming Subscription Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence