Key Insights

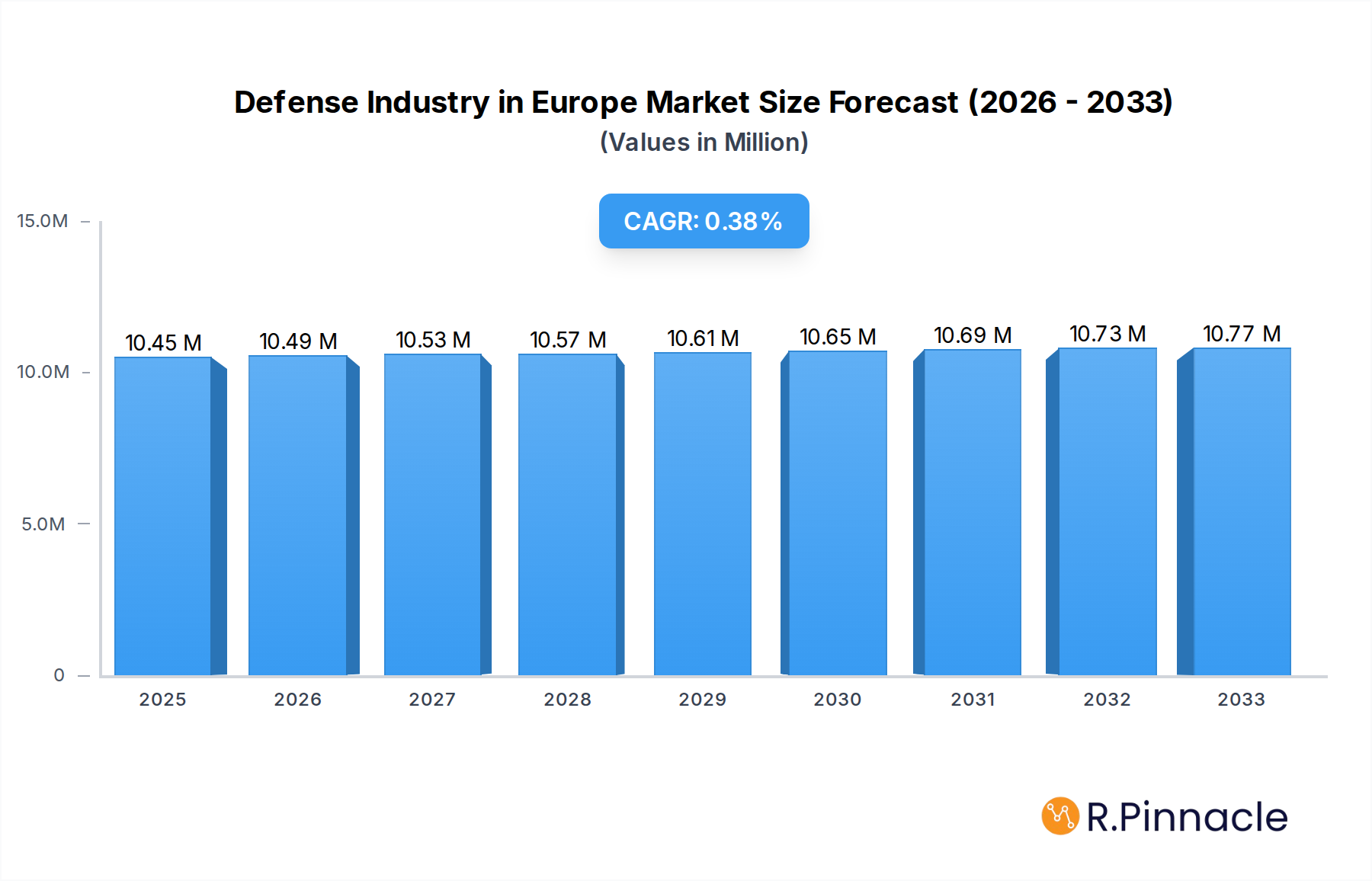

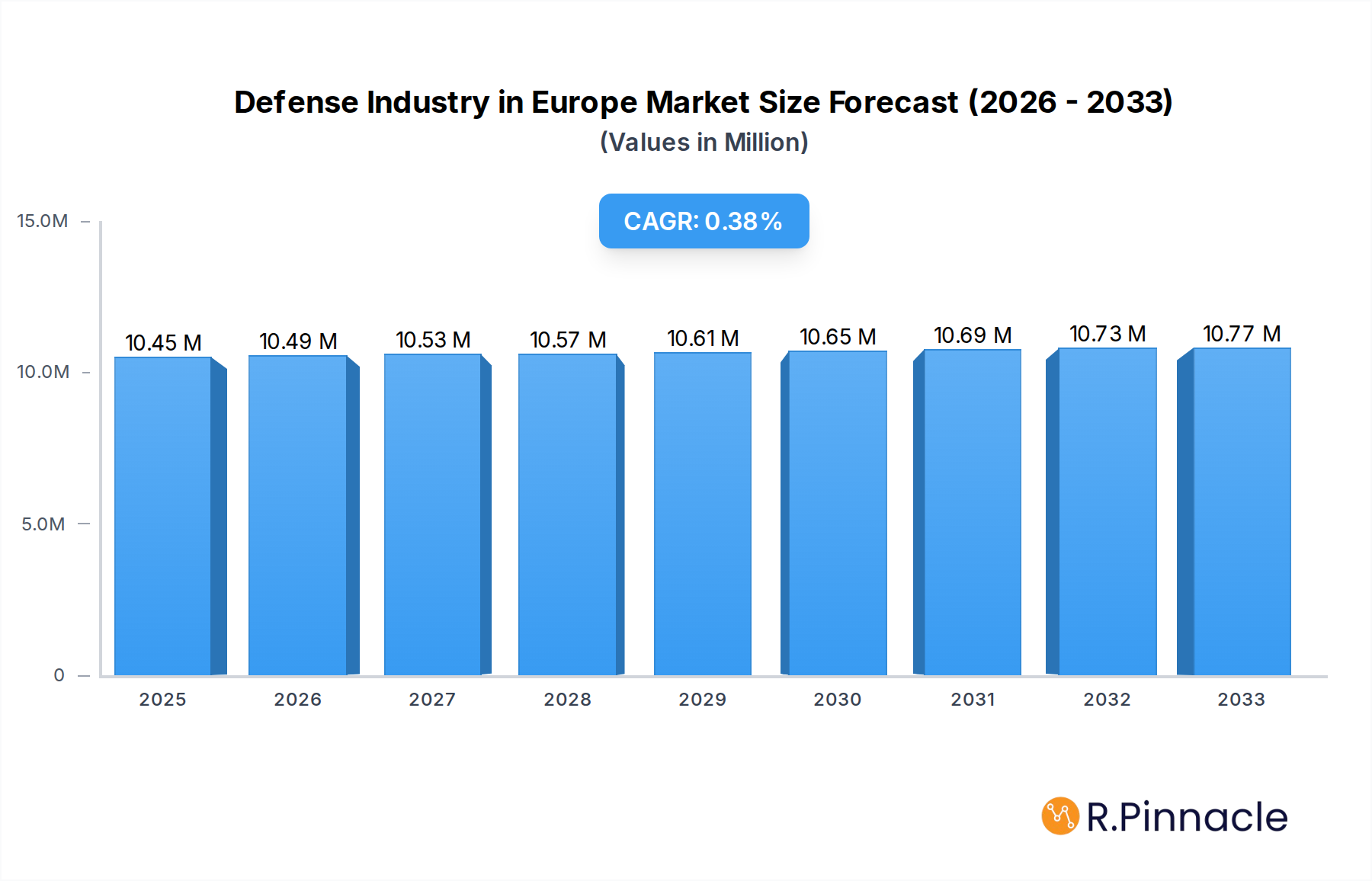

The European defense industry is poised for steady expansion, with a projected market size of 10.45 Million value units. The industry is expected to grow at a Compound Annual Growth Rate (CAGR) of 0.04% over the forecast period of 2025-2033, indicating a period of consistent, albeit moderate, development. This growth is underpinned by a complex interplay of drivers, including the escalating geopolitical tensions and the ongoing need for modernization of existing military capabilities across European nations. The increasing focus on cybersecurity and the demand for advanced communication systems are also significant contributors. Furthermore, evolving threat landscapes are compelling governments to invest in sophisticated armament and protection equipment, thereby fueling market expansion. The strategic importance of maintaining robust defense postures in light of global uncertainties will continue to be a primary catalyst for sustained investment and technological advancement within the sector.

Defense Industry in Europe Market Size (In Million)

The European defense market is characterized by a dynamic segmentation across equipment types and platforms. Within "Equipment Type," "Armament" and "Personnel Training and Protection" are anticipated to witness robust demand as nations prioritize enhancing their combat readiness and soldier safety. "Communication" systems, crucial for coordinated operations in increasingly complex theaters, also represent a significant growth area. On the "Platform" front, "Terrestrial" and "Aerial" segments are expected to dominate investments, driven by the need for modern ground vehicles, aircraft, and associated technologies. While the CAGR is modest, the sheer scale of the market and the strategic imperative for defense spending suggest substantial absolute value growth. Key players like Thales, Rheinmetall AG, BAE Systems plc, and Airbus SE are at the forefront of innovation, developing cutting-edge solutions to meet the evolving demands of European armed forces. The focus will be on integrated systems and platform modernization, alongside emerging technologies like AI and autonomous systems.

Defense Industry in Europe Company Market Share

Defense Industry in Europe: Market Insights, Innovation Trends, and Future Outlook 2019–2033

This comprehensive report offers an in-depth analysis of the European defense industry, covering market structure, dynamics, regional dominance, product innovations, and future growth trajectories. Covering the historical period of 2019–2024 and a forecast period extending to 2033, with a base and estimated year of 2025, this report is essential for defense manufacturers, policymakers, and investors seeking to understand the evolving landscape. We analyze key segments like Personnel Training and Protection, Communication, Armament, Transport, and Platforms including Terrestrial, Aerial, and Naval, providing actionable insights.

Defense Industry in Europe Market Structure & Innovation Trends

The European defense industry exhibits a moderately consolidated market structure, with significant players like BAE Systems plc, Leonardo S p A, and Rheinmetall AG holding substantial market shares. Innovation is a critical driver, fueled by substantial R&D investments estimated to be in the tens of billions of Euros annually across leading companies such as Lockheed Martin Corporation and RTX Corporation. Regulatory frameworks, guided by national security interests and EU initiatives like the European Defence Fund, shape procurement and development. Product substitutes are limited due to the specialized nature of defense equipment, but advancements in civilian technologies can influence dual-use applications. End-user demographics are primarily national defense forces, with evolving requirements driven by geopolitical shifts. Merger and acquisition (M&A) activities are strategic, focusing on technology acquisition and market consolidation, with deal values often in the hundreds of millions to billions of Euros. Recent M&A activities include strategic partnerships and smaller acquisitions aimed at bolstering specific capabilities.

Defense Industry in Europe Market Dynamics & Trends

The European defense market is experiencing robust growth, driven by escalating geopolitical tensions and a renewed emphasis on national security. Market growth drivers include increased defense spending by NATO member states, the ongoing conflict in Ukraine, and the imperative to modernize aging military hardware. Technological disruptions are at the forefront, with advancements in artificial intelligence, cyber warfare, unmanned systems, and advanced materials reshaping defense capabilities. Consumer preferences, or rather, the demands of end-users (national armed forces), are shifting towards networked warfare, agile platforms, and enhanced situational awareness. Competitive dynamics are intensifying, with established European giants like Airbus SE and Thales competing fiercely with global players like General Dynamics Corporation and Northrop Grumman Corporation. The market penetration of advanced technologies is steadily increasing, particularly in areas like electronic warfare and precision-guided munitions. The overall CAGR is projected to be in the range of 4–6% during the forecast period, reflecting a sustained investment in defense. Market expansion is also being influenced by a growing demand for robust communication systems and sophisticated personnel training and protection equipment, with market sizes in these segments projected to reach hundreds of millions of Euros.

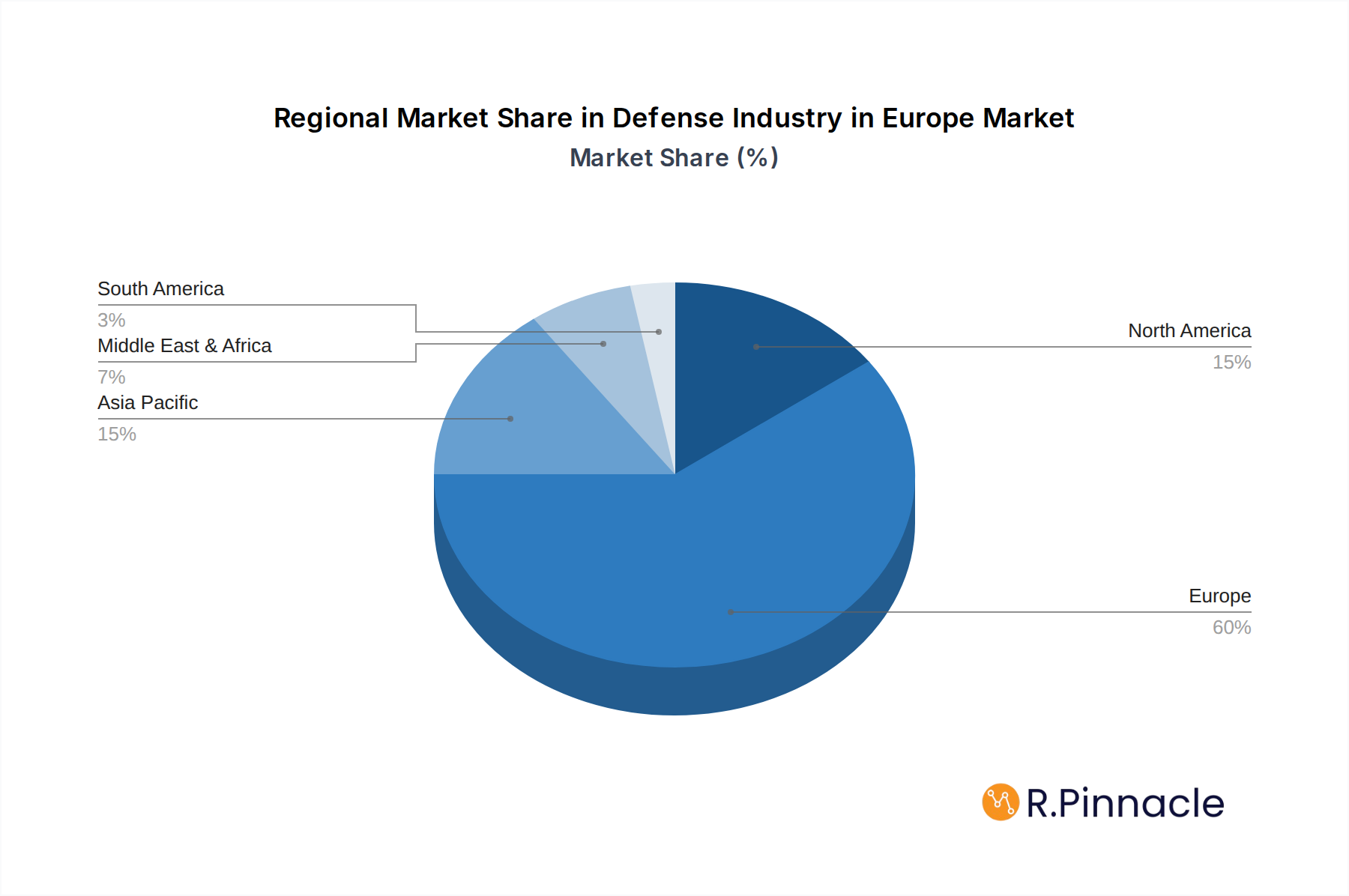

Dominant Regions & Segments in Defense Industry in Europe

The dominant region within the European defense industry is Western Europe, with countries like the United Kingdom, France, Germany, and Italy leading in defense expenditure and manufacturing capabilities. This dominance is underpinned by strong governmental support, established industrial bases, and active participation in international defense cooperation initiatives.

- Key Drivers of Regional Dominance:

- Economic Policies: Robust national defense budgets and strategic investment in defense R&D.

- Infrastructure: Advanced manufacturing facilities, research centers, and skilled workforces.

- Geopolitical Positioning: Proximity to perceived security threats, necessitating strong defense postures.

- Technological Prowess: Leading capabilities in areas like aerospace, naval technology, and cybersecurity.

Among the equipment types, Armament commands a significant market share, driven by the ongoing need for advanced weaponry, including missiles, artillery, and small arms. The Aerial platform segment is also a major contributor, with substantial investments in fighter jets, transport aircraft, and unmanned aerial vehicles (UAVs). Companies like BAE Systems plc and Airbus SE are at the forefront of these segments. The Naval platform segment is experiencing a resurgence, with increased focus on frigates, submarines, and naval patrol vessels. Communication systems are integral to modern warfare, with a continuous demand for secure and resilient networks, making it a crucial growth area. Personnel Training and Protection remains a foundational segment, with continuous innovation in protective gear, simulation technologies, and training methodologies. The market size for Armament is estimated to be in the tens of billions of Euros, followed closely by Aerial and Naval platforms.

Defense Industry in Europe Product Innovations

Product innovations in the European defense industry are driven by the pursuit of enhanced operational effectiveness and technological superiority. Key trends include the development of AI-enabled autonomous systems, advanced cyber defense solutions, and next-generation stealth technologies. Companies like Lockheed Martin Corporation are pushing boundaries with F-35 advancements, while Rheinmetall AG focuses on next-generation armored vehicles and Leonardo S p A on sophisticated sensor and avionics systems. These innovations offer significant competitive advantages by providing enhanced capabilities such as improved targeting accuracy, superior survivability, and reduced logistical footprints. The market fit for these innovations is strong, addressing the evolving threats and operational requirements of modern armed forces.

Report Scope & Segmentation Analysis

This report segments the European defense market across key equipment types and platforms.

- Personnel Training and Protection: This segment encompasses advanced simulation systems, protective armor, and combat readiness training solutions. Projected growth is moderate but steady, with a market size expected to reach several billion Euros.

- Communication: Focuses on secure, resilient, and networked communication systems, including satellite communication and tactical data links. This segment is experiencing robust growth, with an estimated market size in the billions of Euros.

- Armament: Includes missiles, artillery, small arms, and associated munitions. This segment is the largest by market size, projected to be in the tens of billions of Euros, driven by modernization and new threat environments.

- Transport: Covers military aircraft, naval vessels, and ground vehicles designed for troop and equipment deployment. Significant market size, with steady growth anticipated, reaching billions of Euros.

- Platform: Terrestrial: Includes tanks, armored personnel carriers, and logistics vehicles. Stable growth is expected, with market size in the billions of Euros.

- Platform: Aerial: Encompasses fighter jets, helicopters, UAVs, and transport aircraft. A high-growth segment with a substantial market size in the tens of billions of Euros.

- Platform: Naval: Includes warships, submarines, and patrol vessels. Experiencing renewed investment and growth, with a market size projected to be in the billions of Euros.

Key Drivers of Defense Industry in Europe Growth

The European defense industry's growth is propelled by several interconnected factors. Geopolitical instability and increased regional security concerns, particularly in Eastern Europe, are driving significant increases in defense spending. This is further augmented by national commitments to NATO's defense spending targets. Technological advancements, such as the integration of artificial intelligence, quantum computing, and advanced robotics, are creating demand for new capabilities and modernization programs. Furthermore, strategic initiatives like the European Defence Fund and the Permanent Structured Cooperation (PESCO) foster collaborative development and procurement, boosting innovation and market opportunities.

Challenges in the Defense Industry in Europe Sector

Despite its growth, the European defense sector faces several significant challenges. Regulatory hurdles and complex procurement processes across different member states can slow down development and acquisition timelines. Supply chain disruptions, exacerbated by global events, continue to impact the availability of critical components and raw materials, potentially increasing costs by 5-10%. Intense global competition, particularly from North American and Asian manufacturers, puts pressure on market share. Moreover, political sensitivities and varying national interests can complicate collaborative defense projects, hindering economies of scale. Cybersecurity threats pose a persistent risk, requiring continuous investment in protective measures.

Emerging Opportunities in Defense Industry in Europe

Emerging opportunities in the European defense industry are abundant, driven by technological innovation and evolving security landscapes. The growing demand for cyber warfare capabilities and resilient communication networks presents a significant opportunity for specialized companies. The rise of drone technology, both for surveillance and attack, is creating new markets for unmanned systems and counter-drone solutions. Furthermore, increased focus on sustainable defense practices and energy-efficient platforms opens avenues for green defense technologies. Collaborative defense initiatives within the EU and with international partners offer opportunities for joint development and production, reducing costs and enhancing interoperability. The modernization of aging fleets across aerial, naval, and terrestrial platforms presents substantial upgrade and replacement opportunities.

Leading Players in the Defense Industry in Europe Market

- BAE Systems plc

- Lockheed Martin Corporation

- Airbus SE

- Rheinmetall AG

- Thales

- General Dynamics Corporation

- RTX Corporation

- Leonardo S p A

- Saab AB

- Indra Sistemas S A

- Northrop Grumman Corporation

- United Aircraft Corporation (PJSC UAC)

- Rostec State Corporation

- UkrOboronProm

Key Developments in Defense Industry in Europe Industry

- September 2023: A consortium of European defense manufacturers led by Indra Sistemas S.A. launched work on an electronic warfare capability for the European Union to protect friendly aircraft against missile attacks. The Responsive Electronic Attack for Cooperative Tasks (REACT) program aims to develop a system capable of jamming targeting signals and disabling adversary electronic warfare emitters.

- June 2023: The UK Royal Air Force received two F-35B Lightning II stealth multirole combat aircraft from Lockheed Martin, part of a 48-aircraft order for the RAF and Royal Navy.

- April 2023: A USD 225-million support agreement was awarded to Lockheed Martin to sustain the British F-35 fleet's operability.

Future Outlook for Defense Industry in Europe Market

The future outlook for the European defense industry is highly positive, driven by sustained geopolitical imperatives and a commitment to technological advancement. Increased defense spending, a focus on modernization, and collaborative European initiatives will continue to accelerate growth. Key growth accelerators include the integration of AI and autonomous systems, the expansion of cyber defense capabilities, and the development of next-generation aerial and naval platforms. Strategic investments in research and development will be crucial for maintaining a competitive edge. The market is poised for significant expansion, with opportunities in niche segments like electronic warfare and advanced training solutions, alongside continued demand for core platforms and armaments. The ongoing evolution of threats will necessitate agile and responsive defense solutions, ensuring a dynamic and robust market for years to come.

Defense Industry in Europe Segmentation

-

1. Equipment Type

- 1.1. Personnel Training and Protection

- 1.2. Communication

- 1.3. Armament

- 1.4. Transport

-

2. Platform

- 2.1. Terrestrial

- 2.2. Aerial

- 2.3. Naval

Defense Industry in Europe Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Defense Industry in Europe Regional Market Share

Geographic Coverage of Defense Industry in Europe

Defense Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Equipment Type

- 5.1.1. Personnel Training and Protection

- 5.1.2. Communication

- 5.1.3. Armament

- 5.1.4. Transport

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Terrestrial

- 5.2.2. Aerial

- 5.2.3. Naval

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Equipment Type

- 6. Global Defense Industry in Europe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Equipment Type

- 6.1.1. Personnel Training and Protection

- 6.1.2. Communication

- 6.1.3. Armament

- 6.1.4. Transport

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Terrestrial

- 6.2.2. Aerial

- 6.2.3. Naval

- 6.1. Market Analysis, Insights and Forecast - by Equipment Type

- 7. North America Defense Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Equipment Type

- 7.1.1. Personnel Training and Protection

- 7.1.2. Communication

- 7.1.3. Armament

- 7.1.4. Transport

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Terrestrial

- 7.2.2. Aerial

- 7.2.3. Naval

- 7.1. Market Analysis, Insights and Forecast - by Equipment Type

- 8. South America Defense Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Equipment Type

- 8.1.1. Personnel Training and Protection

- 8.1.2. Communication

- 8.1.3. Armament

- 8.1.4. Transport

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Terrestrial

- 8.2.2. Aerial

- 8.2.3. Naval

- 8.1. Market Analysis, Insights and Forecast - by Equipment Type

- 9. Europe Defense Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Equipment Type

- 9.1.1. Personnel Training and Protection

- 9.1.2. Communication

- 9.1.3. Armament

- 9.1.4. Transport

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Terrestrial

- 9.2.2. Aerial

- 9.2.3. Naval

- 9.1. Market Analysis, Insights and Forecast - by Equipment Type

- 10. Middle East & Africa Defense Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Equipment Type

- 10.1.1. Personnel Training and Protection

- 10.1.2. Communication

- 10.1.3. Armament

- 10.1.4. Transport

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Terrestrial

- 10.2.2. Aerial

- 10.2.3. Naval

- 10.1. Market Analysis, Insights and Forecast - by Equipment Type

- 11. Asia Pacific Defense Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Equipment Type

- 11.1.1. Personnel Training and Protection

- 11.1.2. Communication

- 11.1.3. Armament

- 11.1.4. Transport

- 11.2. Market Analysis, Insights and Forecast - by Platform

- 11.2.1. Terrestrial

- 11.2.2. Aerial

- 11.2.3. Naval

- 11.1. Market Analysis, Insights and Forecast - by Equipment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 THALE

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 General Dynamics Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Rheinmetall AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lockheed Martin Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Airbus SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rostec State Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 RTX Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 United Aircraft Corporation (PJSC UAC)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 UkrOboronProm

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Leonardo S p A

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 BAE Systems plc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Indra Sistemas S A

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Northrop Grumman Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Saab AB

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 THALE

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Defense Industry in Europe Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Defense Industry in Europe Revenue (Million), by Equipment Type 2025 & 2033

- Figure 3: North America Defense Industry in Europe Revenue Share (%), by Equipment Type 2025 & 2033

- Figure 4: North America Defense Industry in Europe Revenue (Million), by Platform 2025 & 2033

- Figure 5: North America Defense Industry in Europe Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Defense Industry in Europe Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Defense Industry in Europe Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Defense Industry in Europe Revenue (Million), by Equipment Type 2025 & 2033

- Figure 9: South America Defense Industry in Europe Revenue Share (%), by Equipment Type 2025 & 2033

- Figure 10: South America Defense Industry in Europe Revenue (Million), by Platform 2025 & 2033

- Figure 11: South America Defense Industry in Europe Revenue Share (%), by Platform 2025 & 2033

- Figure 12: South America Defense Industry in Europe Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Defense Industry in Europe Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Defense Industry in Europe Revenue (Million), by Equipment Type 2025 & 2033

- Figure 15: Europe Defense Industry in Europe Revenue Share (%), by Equipment Type 2025 & 2033

- Figure 16: Europe Defense Industry in Europe Revenue (Million), by Platform 2025 & 2033

- Figure 17: Europe Defense Industry in Europe Revenue Share (%), by Platform 2025 & 2033

- Figure 18: Europe Defense Industry in Europe Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Defense Industry in Europe Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Defense Industry in Europe Revenue (Million), by Equipment Type 2025 & 2033

- Figure 21: Middle East & Africa Defense Industry in Europe Revenue Share (%), by Equipment Type 2025 & 2033

- Figure 22: Middle East & Africa Defense Industry in Europe Revenue (Million), by Platform 2025 & 2033

- Figure 23: Middle East & Africa Defense Industry in Europe Revenue Share (%), by Platform 2025 & 2033

- Figure 24: Middle East & Africa Defense Industry in Europe Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Defense Industry in Europe Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Defense Industry in Europe Revenue (Million), by Equipment Type 2025 & 2033

- Figure 27: Asia Pacific Defense Industry in Europe Revenue Share (%), by Equipment Type 2025 & 2033

- Figure 28: Asia Pacific Defense Industry in Europe Revenue (Million), by Platform 2025 & 2033

- Figure 29: Asia Pacific Defense Industry in Europe Revenue Share (%), by Platform 2025 & 2033

- Figure 30: Asia Pacific Defense Industry in Europe Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Defense Industry in Europe Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 2: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 3: Global Defense Industry in Europe Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 5: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 6: Global Defense Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 11: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 12: Global Defense Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 17: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 18: Global Defense Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 29: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 30: Global Defense Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Defense Industry in Europe Revenue Million Forecast, by Equipment Type 2020 & 2033

- Table 38: Global Defense Industry in Europe Revenue Million Forecast, by Platform 2020 & 2033

- Table 39: Global Defense Industry in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Defense Industry in Europe Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Defense Industry in Europe?

The projected CAGR is approximately 0.04%.

2. Which companies are prominent players in the Defense Industry in Europe?

Key companies in the market include THALE, General Dynamics Corporation, Rheinmetall AG, Lockheed Martin Corporation, Airbus SE, Rostec State Corporation, RTX Corporation, United Aircraft Corporation (PJSC UAC), UkrOboronProm, Leonardo S p A, BAE Systems plc, Indra Sistemas S A, Northrop Grumman Corporation, Saab AB.

3. What are the main segments of the Defense Industry in Europe?

The market segments include Equipment Type, Platform.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.45 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Naval Segment Will Showcase Remarkable Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

September 2023: A consortium of European defense manufacturers led by Indra Sistemas S.A. launched work on an electronic warfare capability for the European Union to protect friendly aircraft against missile attacks. According to a European Defence Fund fact sheet, the Responsive Electronic Attack for Cooperative Tasks (REACT) program is intended to develop a system capable of jamming any signals used for targeting European aircraft while being able to turn off adversary electronic warfare emitters.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Defense Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Defense Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Defense Industry in Europe?

To stay informed about further developments, trends, and reports in the Defense Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence