Key Insights

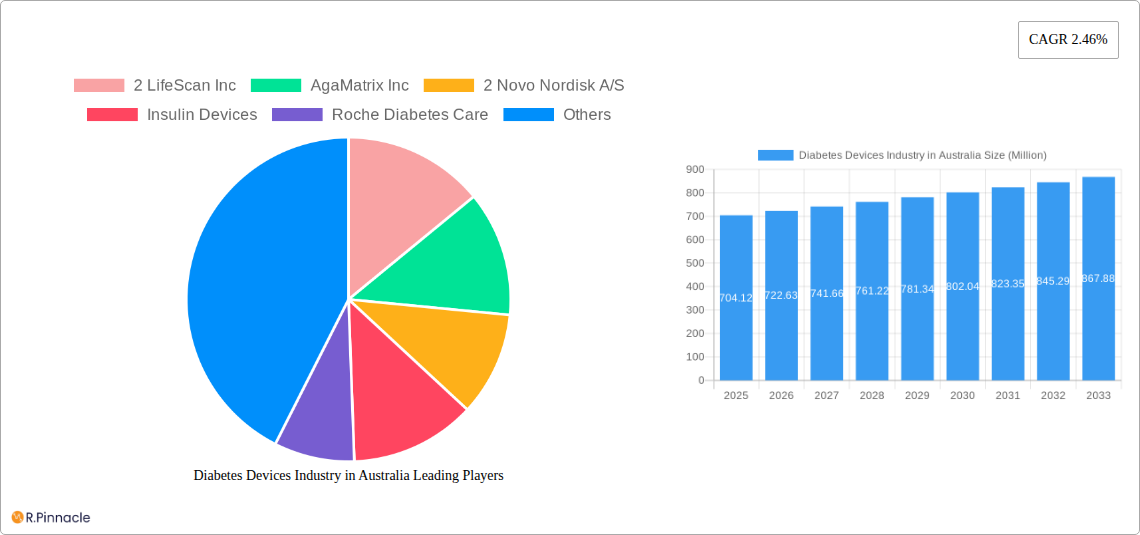

The Australian diabetes devices market, valued at $704.12 million in 2025, is projected to experience steady growth, driven by rising prevalence of diabetes, increasing geriatric population, and growing adoption of advanced monitoring and treatment technologies. The market's Compound Annual Growth Rate (CAGR) of 2.46% from 2019 to 2024 suggests a consistent, albeit moderate, expansion. Key segments driving this growth include continuous glucose monitoring (CGM) systems, which offer improved patient convenience and better diabetes management, and insulin pumps, providing precise insulin delivery for better glycemic control. The increasing awareness of the benefits of early diagnosis and proactive management, coupled with government initiatives promoting diabetes care, further fuels market expansion. However, the market faces restraints such as high device costs, particularly for advanced technologies like CGMs, potentially limiting accessibility for some patients. Furthermore, reimbursement policies and insurance coverage can influence market penetration, impacting adoption rates for newer, more expensive devices. Competition among major players like Abbott Diabetes Care, Medtronic, Dexcom, and Novo Nordisk is intense, leading to innovation and improved product offerings. The market is likely to see further segmentation based on device type, and the introduction of new technologies that offer greater convenience, affordability, and efficacy in diabetes management.

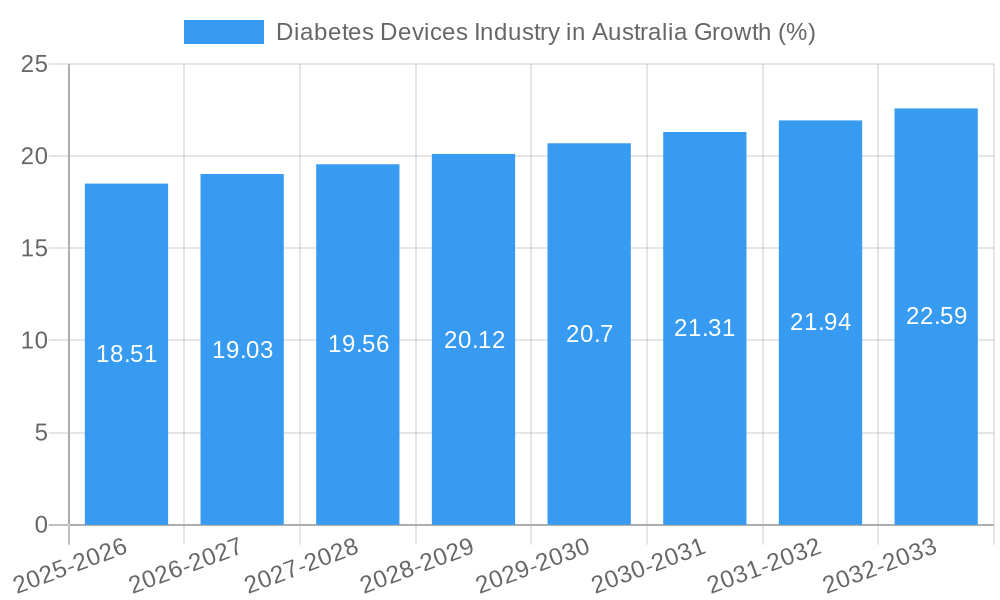

The forecast period of 2025-2033 suggests continued growth, albeit at a pace influenced by factors like technological advancements, pricing strategies, and regulatory changes. Further market segmentation will likely emerge based on specific device functionalities (e.g., integrated CGM and insulin pump systems), user demographics (e.g., pediatric vs. adult diabetes management), and the increasing demand for remote monitoring and telehealth solutions for diabetes care. The Australian government's initiatives promoting preventative health measures and access to quality diabetes care will play a significant role in shaping market dynamics during this period. Companies will likely focus on strategic collaborations, product innovation, and targeted marketing campaigns to capture a greater market share within this evolving landscape.

Diabetes Devices Industry in Australia: A Comprehensive Market Report (2019-2033)

This report provides a detailed analysis of the Australian diabetes devices market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. We examine market structure, dynamics, key players, and future growth potential, covering the period from 2019 to 2033, with a focus on 2025. The report leverages extensive market research, incorporating recent regulatory changes and technological advancements to provide actionable intelligence. The total market size in 2025 is estimated at AU$ XX Million.

Diabetes Devices Industry in Australia Market Structure & Innovation Trends

The Australian diabetes devices market exhibits a moderately concentrated structure, with key players like Medtronic, Abbott Diabetes Care, Dexcom Inc, and Eli Lilly holding significant market share (estimated at xx% collectively in 2025). Market share is dynamically shifting due to continuous innovation and regulatory changes. Innovation is driven by the increasing prevalence of diabetes, coupled with demand for advanced, user-friendly devices. The regulatory framework, while stringent, is evolving to facilitate access to newer technologies.

- Market Concentration: Moderately concentrated, with top players holding xx% market share (2025).

- Innovation Drivers: Rising diabetes prevalence, technological advancements, patient demand for better management tools.

- Regulatory Landscape: Stringent but evolving, with recent approvals boosting CGM accessibility.

- Product Substitutes: Limited, with technological improvements strengthening the market position of existing devices.

- End-User Demographics: Growing aged population and increasing diabetes diagnoses are key drivers.

- M&A Activity: Moderate activity, with deal values in 2024 estimated at AU$ xx Million, driven by expansion strategies and technological integration.

Diabetes Devices Industry in Australia Market Dynamics & Trends

The Australian diabetes devices market is experiencing robust growth, driven by factors such as rising diabetes prevalence, increasing healthcare expenditure, and technological advancements in continuous glucose monitoring (CGM) and insulin delivery systems. The market CAGR from 2025 to 2033 is projected at xx%. Increased patient awareness and improved access to sophisticated devices are contributing factors. Technological disruptions are reshaping the market landscape, creating opportunities for new entrants with innovative products. Consumer preferences are shifting towards user-friendly, connected devices that offer personalized data and insights. Competitive dynamics are intense, with key players investing heavily in R&D and strategic partnerships to maintain market leadership. Market penetration of CGMs is steadily increasing and expected to reach xx% by 2033.

Dominant Regions & Segments in Diabetes Devices Industry in Australia

While data on regional variations within Australia is limited, the market is likely driven by population density and access to healthcare resources. Major urban centers are expected to be the leading regions.

Dominant Segments:

- Management Devices:

- Insulin Pumps: Growing steadily driven by improved technology and patient preference for automated systems.

- Infusion Sets: Strong demand driven by increased usage of insulin pumps and continuous insulin delivery.

- Insulin Syringes, Cartridges in Reusable Pens, Insulin Disposable Pens: Remain significant segments despite increased insulin pump adoption.

- Jet Injectors: Niche segment with limited but growing adoption.

- Monitoring Devices:

- Self-monitoring Blood Glucose (SMBG): Large established market, albeit with declining growth as CGM gains traction.

- Continuous Glucose Monitoring (CGM): Fastest-growing segment, fuelled by government approvals and improved accuracy/ease of use.

- Lancets: Demand is directly linked to SMBG usage; growth is expected to decelerate.

Key Drivers (across all segments):

- Increased government funding for diabetes management.

- Rising awareness and better diagnosis rates.

- Improvements in device technology (accuracy, usability, connectivity).

Diabetes Devices Industry in Australia Product Innovations

Recent innovations focus on improving the accuracy, usability, and connectivity of diabetes devices. Continuous glucose monitoring (CGM) systems have seen significant advancements, offering real-time data and integration with insulin pumps for automated insulin delivery. The introduction of connected platforms, like Eli Lilly's Tempo system, aims to provide personalized diabetes management through data-driven insights. These innovations address key market needs for improved glycemic control, convenience, and patient empowerment.

Report Scope & Segmentation Analysis

This report segments the Australian diabetes devices market by device type (Management and Monitoring), and further sub-segments by specific product categories detailed above (Insulin Pumps, Infusion Sets, etc.). We provide detailed analysis of market size (AU$ Million), growth projections, and competitive dynamics for each segment. The study period is 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033 and the historical period is 2019-2024.

Key Drivers of Diabetes Devices Industry in Australia Growth

The growth of the Australian diabetes devices market is propelled by several factors, including:

- Rising Prevalence of Diabetes: The increasing incidence of type 1 and type 2 diabetes fuels demand for effective management tools.

- Technological Advancements: Continuous innovation in CGM and insulin delivery systems improves accuracy, ease of use, and patient outcomes.

- Government Initiatives: Policies encouraging access to advanced technologies and improved diabetes management support market expansion. The recent expansion of CGM prescription access is a prime example.

Challenges in the Diabetes Devices Industry in Australia Sector

The Australian diabetes devices market faces certain challenges:

- High Device Costs: The high price of advanced devices can limit accessibility, particularly for patients with limited financial resources.

- Supply Chain Disruptions: Global supply chain vulnerabilities can impact the availability of devices.

- Stringent Regulatory Approvals: The rigorous regulatory environment can delay product launches and market entry.

Emerging Opportunities in Diabetes Devices Industry in Australia

Significant opportunities exist in:

- Expansion of CGM Use: Continued growth in CGM adoption presents a substantial market opportunity.

- Integration of Digital Health Technologies: Connecting devices with smartphone apps and telehealth platforms enhances patient care and data management.

- Development of Personalized Diabetes Management Systems: Tailoring devices and therapies to individual patient needs is a promising avenue for innovation.

Leading Players in the Diabetes Devices Industry in Australia Market

- 2 LifeScan Inc

- AgaMatrix Inc

- 2 Novo Nordisk A/S

- Insulin Devices

- Roche Diabetes Care

- Eli Lilly

- 2 LifeScan Inc

- Abbott Diabetes Care

- Medtronic

- 1 Dexcom Inc

- Dexcom Inc

- Continuous Glucose Monitoring Devices

- 1 Abbott Diabetes Care

- Sanofi Aventis

- 2 Medtronic PLC

- Insulet Corporation

- ARKRAY Inc

- 1 Insulet Corporation

- Self-monitoring Blood Glucose Devices

- Novo Nordisk A/S

- Ypsomed Holding AG

- Ascensia Diabetes Care

Key Developments in Diabetes Devices Industry in Australia Industry

- November 2023: Australian government approves CGM prescriptions from GPs, diabetes educators, clinics, RNs, and specialists, significantly expanding access.

- November 2022: Eli Lilly launches Tempo Personalized Diabetes Management Platform, enhancing data-driven treatment decisions.

Future Outlook for Diabetes Devices Industry in Australia Market

The Australian diabetes devices market is poised for continued growth, driven by technological advancements, increased awareness, and supportive government policies. The expansion of CGM access and the integration of digital health technologies will be key growth accelerators. Strategic partnerships and investments in R&D will shape the future competitive landscape. The market's potential remains significant, given the rising prevalence of diabetes and the ongoing demand for innovative, effective management solutions.

Diabetes Devices Industry in Australia Segmentation

-

1. Management Devices

- 1.1. Insulin Pump

- 1.2. Insulin Syringes

- 1.3. cartridges in reusable pens

- 1.4. disposable pens

- 1.5. jet injectors

-

2. Monitoring Devices

- 2.1. Self-monitoring Blood Glucose

- 2.2. Continuous Glucose Monitoring

- 2.3. lancets

Diabetes Devices Industry in Australia Segmentation By Geography

- 1. Australia

Diabetes Devices Industry in Australia REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.46% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies

- 3.3. Market Restrains

- 3.3.1 ; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures

- 3.3.2 Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products

- 3.4. Market Trends

- 3.4.1. Increasing Diabetes Prevalence

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Diabetes Devices Industry in Australia Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Management Devices

- 5.1.1. Insulin Pump

- 5.1.2. Insulin Syringes

- 5.1.3. cartridges in reusable pens

- 5.1.4. disposable pens

- 5.1.5. jet injectors

- 5.2. Market Analysis, Insights and Forecast - by Monitoring Devices

- 5.2.1. Self-monitoring Blood Glucose

- 5.2.2. Continuous Glucose Monitoring

- 5.2.3. lancets

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Management Devices

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 2 LifeScan Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 AgaMatrix Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 2 Novo Nordisk A/S

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Insulin Devices

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Roche Diabetes Care

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Eli Lilly

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 LifeScan Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Abbott Diabetes Care

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Medtronic

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 1 Dexcom Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Dexcom Inc

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Continuous Glucose Monitoring Devices

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 1 Abbott Diabetes Care

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Sanofi Aventis

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 2 Medtronic PLC

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Insulet Corporation

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 ARKRAY Inc

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 1 Insulet Corporation

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Self-monitoring Blood Glucose Devices

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Novo Nordisk A/S

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.21 Ypsomed Holding AG

- 6.2.21.1. Overview

- 6.2.21.2. Products

- 6.2.21.3. SWOT Analysis

- 6.2.21.4. Recent Developments

- 6.2.21.5. Financials (Based on Availability)

- 6.2.22 Ascensia Diabetes Care

- 6.2.22.1. Overview

- 6.2.22.2. Products

- 6.2.22.3. SWOT Analysis

- 6.2.22.4. Recent Developments

- 6.2.22.5. Financials (Based on Availability)

- 6.2.1 2 LifeScan Inc

List of Figures

- Figure 1: Diabetes Devices Industry in Australia Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Diabetes Devices Industry in Australia Share (%) by Company 2024

List of Tables

- Table 1: Diabetes Devices Industry in Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Diabetes Devices Industry in Australia Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 4: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Management Devices 2019 & 2032

- Table 5: Diabetes Devices Industry in Australia Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 6: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Monitoring Devices 2019 & 2032

- Table 7: Diabetes Devices Industry in Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Diabetes Devices Industry in Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Diabetes Devices Industry in Australia Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 12: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Management Devices 2019 & 2032

- Table 13: Diabetes Devices Industry in Australia Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 14: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Monitoring Devices 2019 & 2032

- Table 15: Diabetes Devices Industry in Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Diabetes Devices Industry in Australia Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetes Devices Industry in Australia?

The projected CAGR is approximately 2.46%.

2. Which companies are prominent players in the Diabetes Devices Industry in Australia?

Key companies in the market include 2 LifeScan Inc, AgaMatrix Inc, 2 Novo Nordisk A/S, Insulin Devices, Roche Diabetes Care, Eli Lilly, LifeScan Inc, Abbott Diabetes Care, Medtronic, 1 Dexcom Inc, Dexcom Inc, Continuous Glucose Monitoring Devices, 1 Abbott Diabetes Care, Sanofi Aventis, 2 Medtronic PLC, Insulet Corporation, ARKRAY Inc, 1 Insulet Corporation, Self-monitoring Blood Glucose Devices, Novo Nordisk A/S, Ypsomed Holding AG, Ascensia Diabetes Care.

3. What are the main segments of the Diabetes Devices Industry in Australia?

The market segments include Management Devices, Monitoring Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD 704.12 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

Increasing Diabetes Prevalence.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

November 2023: The Australian government has granted approval for individuals to obtain prescriptions for continuous glucose monitoring (CGM) devices from various healthcare professionals, including General Practitioners (GPs), diabetes educators, diabetes clinics, Registered Nurses (RNs), and specialists.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetes Devices Industry in Australia," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetes Devices Industry in Australia report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetes Devices Industry in Australia?

To stay informed about further developments, trends, and reports in the Diabetes Devices Industry in Australia, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence