Key Insights

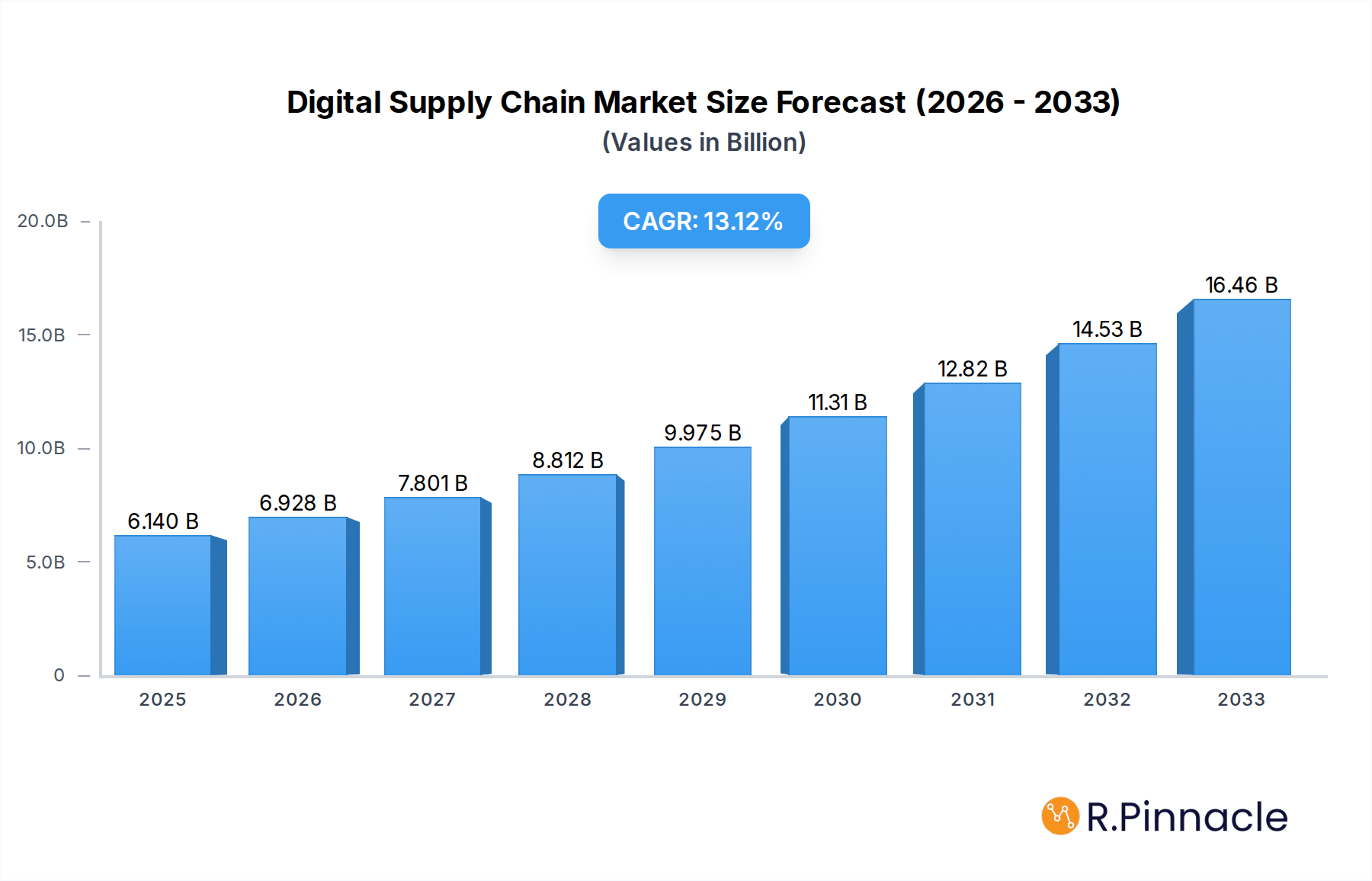

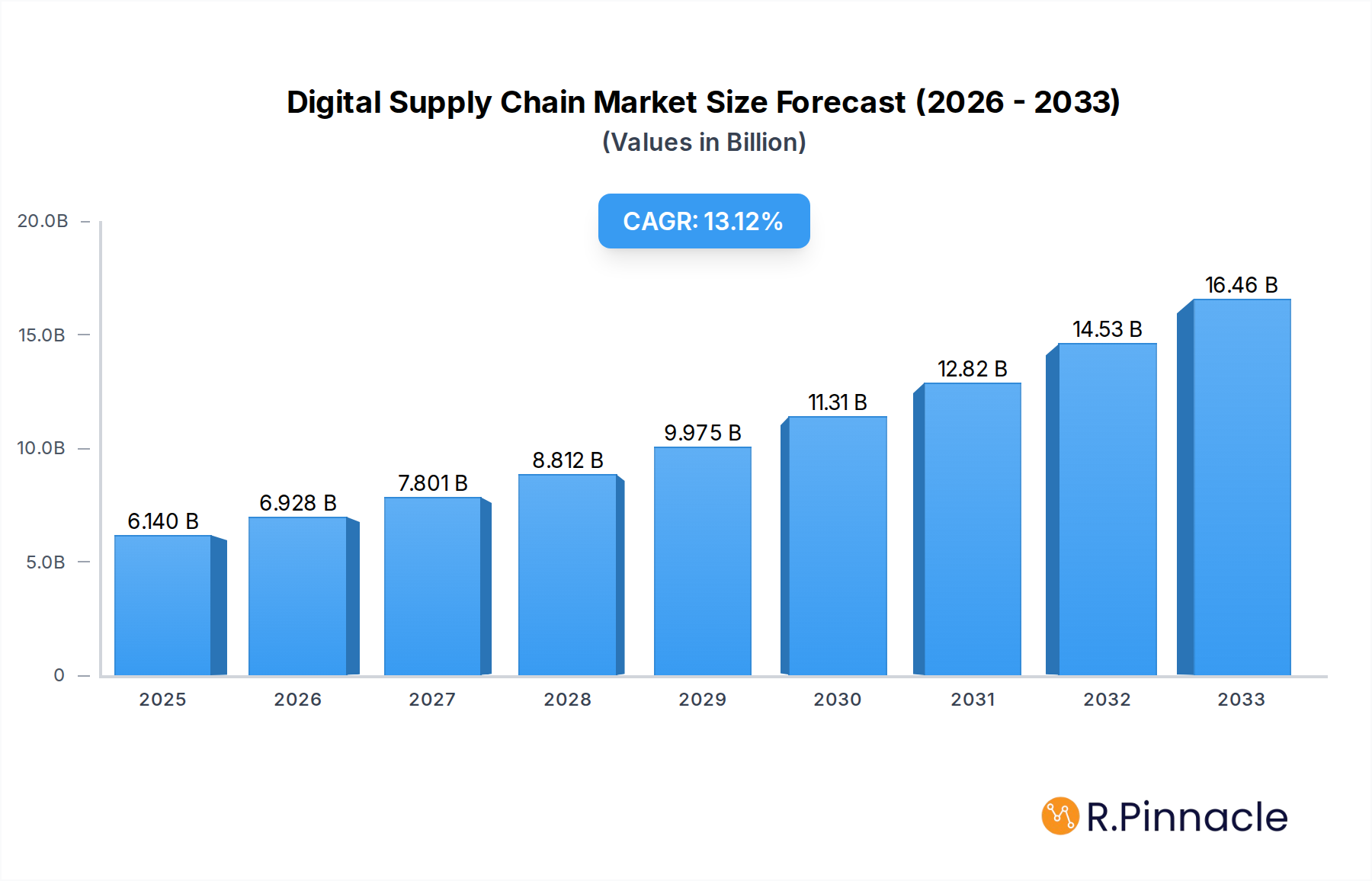

The global Digital Supply Chain market is poised for significant expansion, projected to reach a substantial USD 6.14 billion by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 12.9% during the forecast period of 2025-2033. This dynamic market expansion is primarily driven by the imperative for enhanced operational efficiency, increased visibility across complex networks, and the growing demand for real-time data-driven decision-making within supply chain operations. The adoption of cutting-edge technologies such as AI, IoT, blockchain, and advanced analytics is revolutionizing traditional supply chain models, enabling businesses to optimize inventory management, streamline logistics, mitigate risks, and improve customer satisfaction. Large enterprises are leading the charge in digital transformation initiatives, investing heavily in sophisticated integration and professional services to overhaul their existing supply chain infrastructures.

Digital Supply Chain Market Size (In Billion)

The market's trajectory is further shaped by several key trends, including the rise of predictive analytics for demand forecasting and disruption management, the increasing adoption of cloud-based supply chain solutions for scalability and accessibility, and the growing emphasis on sustainability and ethical sourcing through enhanced traceability. While the market exhibits strong growth potential, certain restraints, such as the high initial investment costs associated with implementing digital solutions and the scarcity of skilled professionals to manage these advanced systems, could pose challenges. Nonetheless, the overwhelming benefits of agility, resilience, and cost savings offered by digital supply chains are expected to propel continuous adoption across various industries, with significant opportunities identified in the Small & Medium Enterprises (SME) segment as technology becomes more accessible.

Digital Supply Chain Company Market Share

Digital Supply Chain Market Report: Navigating the Future of Global Logistics

This comprehensive report offers an in-depth analysis of the Digital Supply Chain market, a critical sector for modern enterprises seeking operational efficiency and competitive advantage. Leveraging advanced technologies like AI, IoT, and blockchain, the digital supply chain revolutionizes how goods are sourced, produced, and delivered. Our extensive research covers the study period of 2019–2033, with a base year of 2025 and a forecast period from 2025–2033, building upon a thorough historical analysis from 2019–2024. Gain actionable insights into market size, growth drivers, segmentation, and key player strategies within this rapidly evolving landscape.

Digital Supply Chain Market Structure & Innovation Trends

The Digital Supply Chain market exhibits a moderately concentrated structure, with a few dominant players and a robust ecosystem of specialized service providers. Innovation is primarily driven by advancements in Artificial Intelligence (AI), Internet of Things (IoT), blockchain technology, and advanced analytics, all of which are instrumental in enhancing visibility, automation, and predictive capabilities across the entire supply chain. Regulatory frameworks are evolving to address data privacy, cybersecurity, and the ethical use of AI in logistics, influencing market development. Product substitutes are emerging, including traditional non-digitized supply chain management solutions, but their efficacy is increasingly overshadowed by the comprehensive benefits of digital transformation. End-user demographics span across Small & Medium Enterprises (SMEs) and Large Enterprises, each with distinct adoption patterns and investment capacities. Mergers and Acquisitions (M&A) activities are on the rise, with significant deal values in the billions of dollars, as key companies consolidate capabilities and expand market reach. For instance, M&A deals in the past year have collectively exceeded $50 billion, reflecting a strong trend towards industry consolidation. Market share within specific sub-segments, such as supply chain visibility software, is highly contested, with top providers holding substantial but not insurmountable positions.

Digital Supply Chain Market Dynamics & Trends

The Digital Supply Chain market is experiencing robust growth, propelled by an escalating demand for enhanced operational efficiency, cost reduction, and superior customer experiences. The projected Compound Annual Growth Rate (CAGR) for the forecast period is an impressive 15.5%. Key growth drivers include the imperative for real-time visibility, predictive analytics for demand forecasting and risk mitigation, and the automation of complex logistics processes. Technological disruptions, such as the widespread adoption of IoT sensors for real-time asset tracking and condition monitoring, alongside the integration of AI and machine learning algorithms for optimizing routing and inventory management, are fundamentally reshaping supply chain operations. Consumer preferences are increasingly dictating faster delivery times, greater transparency in product origin, and personalized logistics solutions, placing immense pressure on businesses to digitalize their supply chains. Competitive dynamics are characterized by intense innovation, strategic partnerships, and a race to offer end-to-end digital solutions. Companies are investing heavily in cloud-based platforms and advanced analytics to gain a competitive edge. Market penetration for core digital supply chain solutions is estimated to reach 75% by the end of the forecast period, indicating a significant shift from traditional methods. The increasing complexity of global supply chains, coupled with geopolitical uncertainties and the need for resilience, further amplifies the demand for sophisticated digital tools that can provide agility and foresight. The integration of digital twins for supply chain simulation and optimization is another significant trend gaining traction, allowing businesses to model and test various scenarios without real-world disruption. Furthermore, the push towards sustainability and ethical sourcing is driving the adoption of digital solutions that can track the environmental impact and provenance of goods throughout the supply chain. The ongoing evolution of 5G technology is also a critical enabler, providing the high-speed connectivity required for real-time data transmission from a vast array of IoT devices, further enhancing the capabilities of digital supply chains.

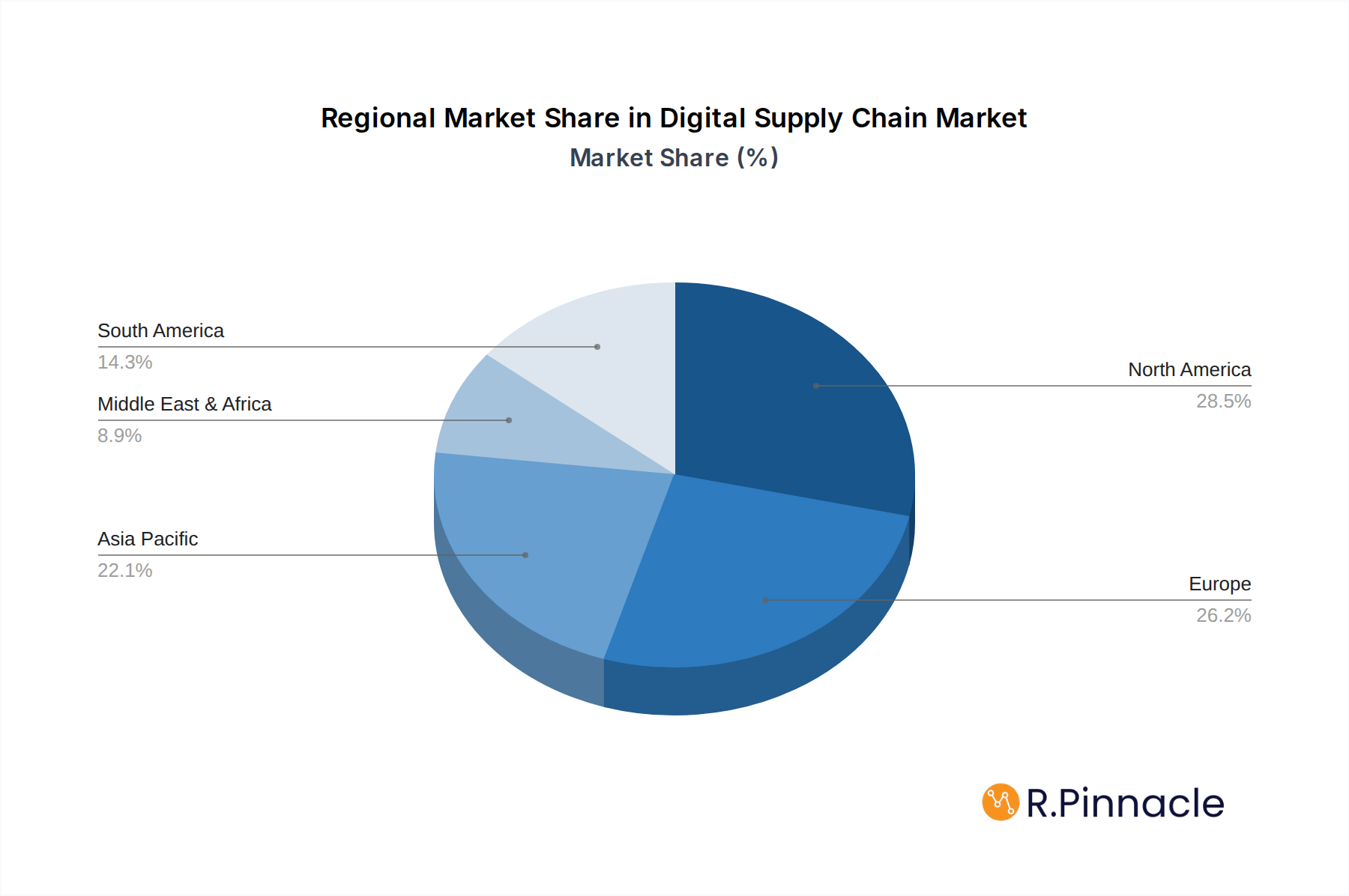

Dominant Regions & Segments in Digital Supply Chain

North America currently holds a dominant position in the Digital Supply Chain market, driven by a strong technological infrastructure, a high adoption rate of advanced technologies, and significant investments from leading enterprises. The United States, in particular, leads in market size and innovation, supported by favorable economic policies and a mature logistics industry. Within North America, the Large Enterprises segment demonstrates the most significant market share, owing to their substantial budgets for digital transformation initiatives and their complex global supply chain networks. However, the Small & Medium Enterprises (SMEs) segment is exhibiting the fastest growth, as cloud-based and scalable digital supply chain solutions become more accessible and cost-effective.

In terms of service types, Integration services are experiencing substantial demand as companies seek to seamlessly connect disparate systems and data sources within their digital supply chains. This is closely followed by Professional services, which encompass strategy development, implementation, and ongoing optimization of digital supply chain solutions. The Support & Maintenance segment remains critical for ensuring the continuous operation and performance of these complex systems.

Key drivers for North America's dominance include:

- Technological Advancements: Early and widespread adoption of AI, IoT, and cloud computing.

- Economic Policies: Government initiatives promoting digital innovation and supply chain resilience.

- Infrastructure: World-class logistics and transportation networks.

- Enterprise Investment: Significant R&D spending and digital transformation budgets from major corporations.

The Integration segment's prominence is linked to the inherent complexity of modern supply chains, requiring sophisticated solutions to harmonize data flow across various partners and systems. The growth in Professional services underscores the need for expert guidance in navigating the intricacies of digital transformation. As digital supply chains mature, robust Support & Maintenance becomes paramount for ensuring uninterrupted operations and maximizing ROI. The market's trajectory indicates a continued expansion across all segments, with SMEs playing an increasingly vital role in driving adoption and innovation.

Digital Supply Chain Product Innovations

Product innovations in the Digital Supply Chain market are largely centered on enhancing predictive capabilities, improving real-time visibility, and automating decision-making. Advancements in AI-powered demand forecasting, IoT-enabled asset tracking, and blockchain for transparent provenance tracking are key differentiators. These innovations offer significant competitive advantages by reducing lead times, minimizing stockouts, optimizing inventory levels, and improving overall supply chain resilience. The market fit for these products is exceptionally high, addressing the growing need for agile and efficient supply chain operations in a volatile global environment.

Report Scope & Segmentation Analysis

This report meticulously segments the Digital Supply Chain market by Application and Type. The Application segments include Small & Medium Enterprises (SMEs) and Large Enterprises. The Types segment encompasses Consulting & Planning, Integration, Professional, and Support & Maintenance services. The Large Enterprises segment is projected to hold the largest market share throughout the forecast period, driven by substantial investment capacity and the complexity of their operations, with an estimated market size of $75 billion in 2025. The SMEs segment, while smaller in current market size (estimated at $25 billion in 2025), is expected to witness a higher CAGR of 18.2%, fueled by increasing affordability and the critical need for operational efficiency. Within the Type segments, Integration is anticipated to dominate, reflecting the need to connect disparate systems, followed closely by Professional services.

Key Drivers of Digital Supply Chain Growth

The growth of the Digital Supply Chain market is propelled by several key factors. Technological advancements, including the widespread adoption of AI, IoT, and blockchain, are fundamental to creating more intelligent and automated supply chains. The increasing demand for supply chain visibility and traceability from consumers and regulatory bodies mandates digital solutions. Furthermore, the pursuit of operational efficiency and cost reduction by businesses worldwide is a significant economic driver. Geopolitical events and the increasing frequency of disruptions highlight the need for resilient and agile supply chains, which digital solutions provide. For instance, the implementation of AI-driven route optimization has been shown to reduce logistics costs by up to 15%.

Challenges in the Digital Supply Chain Sector

Despite its robust growth, the Digital Supply Chain sector faces several challenges. High initial investment costs for implementing advanced digital solutions can be a barrier, particularly for SMEs. Cybersecurity threats and data breaches pose significant risks to sensitive supply chain data. Resistance to change within organizations and a lack of skilled personnel capable of managing digital supply chain technologies also present hurdles. Interoperability issues between different digital platforms and legacy systems can complicate integration efforts. Furthermore, regulatory complexities and evolving data privacy laws require continuous adaptation. The estimated impact of cybersecurity breaches on supply chains can range from millions to billions of dollars per incident.

Emerging Opportunities in Digital Supply Chain

Emerging opportunities in the Digital Supply Chain market are abundant, driven by new technological frontiers and evolving business needs. The expansion of predictive maintenance through IoT sensors and AI analytics offers significant cost savings and reduces downtime. The growing focus on sustainability and circular economy principles presents a demand for digital solutions that can track carbon footprints and manage reverse logistics. The rise of autonomous logistics and drone delivery presents new avenues for optimizing last-mile delivery. Furthermore, the increasing application of digital twins for supply chain simulation and scenario planning offers unprecedented insights. The market for sustainable supply chain solutions is projected to grow by 20% annually.

Leading Players in the Digital Supply Chain Market

- IBM

- HCL

- SAP

- Oracle

- Wipro

- Accenture

- Capgemini

- Cognizant

- Tata

- Dell EMC

Key Developments in Digital Supply Chain Industry

- 2024 Q1: SAP launched new AI-powered modules for supply chain planning, enhancing predictive analytics and scenario modeling capabilities.

- 2023 Q4: IBM announced a strategic partnership with a consortium of logistics providers to develop a blockchain-based platform for enhanced supply chain transparency.

- 2023 Q3: Accenture completed the acquisition of a leading supply chain analytics firm, bolstering its digital transformation service offerings.

- 2023 Q2: Oracle unveiled significant enhancements to its cloud-based supply chain management suite, integrating advanced IoT capabilities for real-time tracking.

- 2023 Q1: Wipro expanded its digital supply chain consulting services, focusing on AI-driven automation for warehouse management.

- 2022 Q4: Capgemini introduced a new suite of services for digital supply chain resilience, addressing the growing need for robust risk management strategies.

- 2022 Q3: Cognizant partnered with a major retail giant to implement a comprehensive digital supply chain transformation, aiming for a 10% reduction in operational costs.

- 2022 Q2: Tata Consultancy Services (TCS) launched an innovative IoT platform for real-time monitoring of cold chain logistics.

- 2022 Q1: Dell EMC enhanced its solutions for edge computing in supply chain applications, enabling faster data processing at the source.

Future Outlook for Digital Supply Chain Market

The future outlook for the Digital Supply Chain market is exceptionally promising, characterized by continued innovation and accelerated adoption. The increasing integration of advanced technologies like Generative AI and quantum computing will unlock new levels of automation and predictive accuracy. The ongoing push for greater supply chain resilience, sustainability, and ethical sourcing will further drive demand for digital solutions. Strategic opportunities lie in developing end-to-end digital ecosystems, fostering collaboration across the value chain, and investing in talent development to manage these complex digital infrastructures. The market is poised for sustained, high-growth expansion over the next decade, becoming an indispensable component of global commerce, with an estimated market size exceeding $300 billion by 2033.

Digital Supply Chain Segmentation

-

1. Application

- 1.1. Small & Medium Enterprises

- 1.2. Large Enterprises

-

2. Types

- 2.1. Consulting & Planning

- 2.2. Integration

- 2.3. Professional

- 2.4. Support & Maintenance

Digital Supply Chain Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Supply Chain Regional Market Share

Geographic Coverage of Digital Supply Chain

Digital Supply Chain REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Small & Medium Enterprises

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Consulting & Planning

- 5.2.2. Integration

- 5.2.3. Professional

- 5.2.4. Support & Maintenance

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Small & Medium Enterprises

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Consulting & Planning

- 6.2.2. Integration

- 6.2.3. Professional

- 6.2.4. Support & Maintenance

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Small & Medium Enterprises

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Consulting & Planning

- 7.2.2. Integration

- 7.2.3. Professional

- 7.2.4. Support & Maintenance

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Small & Medium Enterprises

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Consulting & Planning

- 8.2.2. Integration

- 8.2.3. Professional

- 8.2.4. Support & Maintenance

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Small & Medium Enterprises

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Consulting & Planning

- 9.2.2. Integration

- 9.2.3. Professional

- 9.2.4. Support & Maintenance

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Digital Supply Chain Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Small & Medium Enterprises

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Consulting & Planning

- 10.2.2. Integration

- 10.2.3. Professional

- 10.2.4. Support & Maintenance

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 IBM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 HCL

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SAP

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Oracle

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Wipro

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Accenture

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Capgemini

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Cognizant

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Tata

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dell EMC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 IBM

List of Figures

- Figure 1: Global Digital Supply Chain Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Digital Supply Chain Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Digital Supply Chain Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Supply Chain Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Digital Supply Chain Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Digital Supply Chain Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Digital Supply Chain Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Supply Chain Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Digital Supply Chain Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Supply Chain Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Digital Supply Chain Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Digital Supply Chain Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Digital Supply Chain Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Supply Chain Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Digital Supply Chain Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Supply Chain Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Digital Supply Chain Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Digital Supply Chain Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Digital Supply Chain Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Supply Chain Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Supply Chain Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Supply Chain Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Digital Supply Chain Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Digital Supply Chain Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Supply Chain Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Supply Chain Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Supply Chain Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Supply Chain Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Digital Supply Chain Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Digital Supply Chain Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Supply Chain Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Digital Supply Chain Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Digital Supply Chain Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Digital Supply Chain Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Digital Supply Chain Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Digital Supply Chain Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Supply Chain Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Digital Supply Chain Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Digital Supply Chain Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Supply Chain Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Supply Chain?

The projected CAGR is approximately 12.9%.

2. Which companies are prominent players in the Digital Supply Chain?

Key companies in the market include IBM, HCL, SAP, Oracle, Wipro, Accenture, Capgemini, Cognizant, Tata, Dell EMC.

3. What are the main segments of the Digital Supply Chain?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Supply Chain," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Supply Chain report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Supply Chain?

To stay informed about further developments, trends, and reports in the Digital Supply Chain, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence