Key Insights

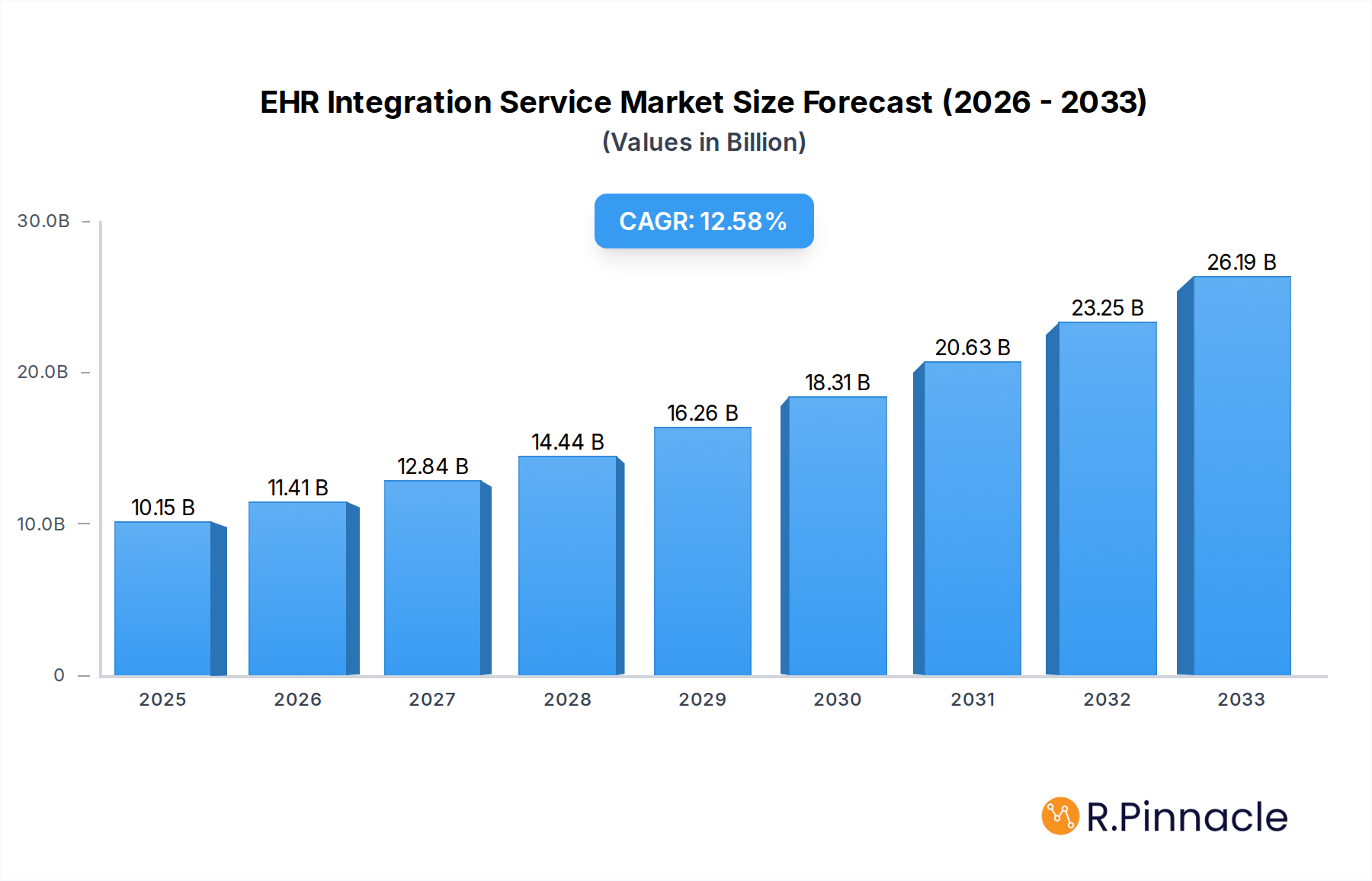

The Electronic Health Record (EHR) Integration Service market is poised for significant expansion, projecting a market size of $10.15 billion in 2025. This robust growth is fueled by a CAGR of 12.46%, indicating a dynamic and rapidly evolving landscape. The primary drivers of this surge include the increasing demand for seamless data interoperability between disparate healthcare systems, the growing adoption of digital health technologies, and the imperative for enhanced patient care coordination. As healthcare providers grapple with the complexities of managing vast amounts of patient data, the need for efficient EHR integration services to streamline workflows, reduce errors, and improve clinical decision-making becomes paramount. Furthermore, the push for value-based care models necessitates better data sharing and analysis, making EHR integration a critical component for achieving organizational goals and improving patient outcomes. The market is witnessing a strong preference for cloud-based solutions, offering greater scalability, accessibility, and cost-effectiveness compared to on-premises alternatives.

EHR Integration Service Market Size (In Billion)

Key trends shaping the EHR Integration Service market include the rise of FHIR (Fast Healthcare Interoperability Resources) standards, which are simplifying data exchange and enabling greater connectivity. The increasing focus on cybersecurity and data privacy regulations also drives the demand for secure and compliant integration solutions. While the market is experiencing substantial growth, certain restraints remain. These include the high initial implementation costs, potential resistance to change among healthcare professionals, and the ongoing challenges associated with data standardization and legacy system compatibility. However, the overarching benefits of improved efficiency, enhanced patient safety, and the potential for significant cost savings in the long run are expected to outweigh these challenges, propelling the market forward. The market is segmented by application into Personal, Hospital, Clinic, and Other, with Hospitals and Clinics being the dominant segments. Types of integration services are On-premises and Cloud Based, with Cloud Based solutions gaining significant traction.

EHR Integration Service Company Market Share

Comprehensive EHR Integration Service Market Report: Trends, Dynamics, and Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the global EHR integration service market, offering critical insights for industry stakeholders. Covering a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025-2033, this report details historical trends, current market dynamics, and future projections. We delve into the intricate market structure, innovative solutions, and the evolving competitive landscape, leveraging high-ranking keywords to ensure maximum search visibility. This report is designed for industry professionals seeking actionable intelligence to navigate the complexities of EHR integration.

EHR Integration Service Market Structure & Innovation Trends

The EHR integration service market is characterized by a moderate to high degree of market concentration, with a blend of established players and emerging innovators. Key innovation drivers include the increasing demand for interoperability, the need for seamless data exchange between disparate healthcare systems, and the relentless pursuit of improved patient care outcomes. Regulatory frameworks, such as HIPAA and HITECH in the United States, and GDPR in Europe, significantly influence market development by mandating data security and privacy standards. The landscape is dynamic, with ongoing M&A activities aimed at consolidating market share and expanding service portfolios. Notable deals, valued in the billions of dollars, signify the strategic importance of acquiring specialized integration capabilities. Product substitutes, while present in the form of manual data entry or siloed systems, are increasingly rendered obsolete by the efficiency and accuracy offered by robust EHR integration solutions. End-user demographics span a wide spectrum, from large hospital networks to independent clinics and personal healthcare applications, all seeking to optimize their digital health infrastructure.

- Market Concentration: Moderate to High, with key players like Allscripts, TELUS, and PointClickCare holding significant shares.

- Innovation Drivers: Interoperability, data security, patient engagement, AI-driven analytics.

- Regulatory Influence: HIPAA, HITECH, GDPR mandates, driving compliance and security features.

- M&A Activity: Significant, with billions of dollars invested in acquiring complementary technologies and market access.

- Product Substitutes: Manual data transfer, legacy systems, are declining in relevance.

- End-User Demographics: Hospitals, Clinics, Personal Healthcare, Other Healthcare entities.

EHR Integration Service Market Dynamics & Trends

The EHR integration service market is experiencing robust growth, propelled by an array of interconnected factors. A primary growth driver is the escalating need for seamless data flow across the healthcare ecosystem to facilitate better clinical decision-making, reduce medical errors, and enhance patient safety. Technological disruptions, including the rise of cloud-based solutions and the integration of AI and machine learning for predictive analytics, are reshaping service offerings and driving efficiency. Consumer preferences are increasingly leaning towards integrated digital health platforms that offer a holistic view of patient information, accessible from multiple touchpoints. This shift is compelling healthcare providers to invest heavily in modernizing their IT infrastructure through advanced EHR integration. The Compound Annual Growth Rate (CAGR) of the market is projected to remain strong, fueled by increasing healthcare IT spending globally. Market penetration is expanding as more healthcare organizations recognize the indispensable role of interoperability in achieving their strategic objectives. The competitive dynamics are intensifying, with companies differentiating themselves through specialized integration capabilities, adherence to evolving standards like FHIR (Fast Healthcare Interoperability Resources), and robust security protocols. The adoption of API-first strategies is also a significant trend, enabling agile and scalable integration solutions. Furthermore, the increasing prevalence of chronic diseases and the aging global population are creating sustained demand for efficient healthcare management, which EHR integration directly supports. The push towards value-based care models also necessitates integrated data systems to track patient outcomes and resource utilization effectively.

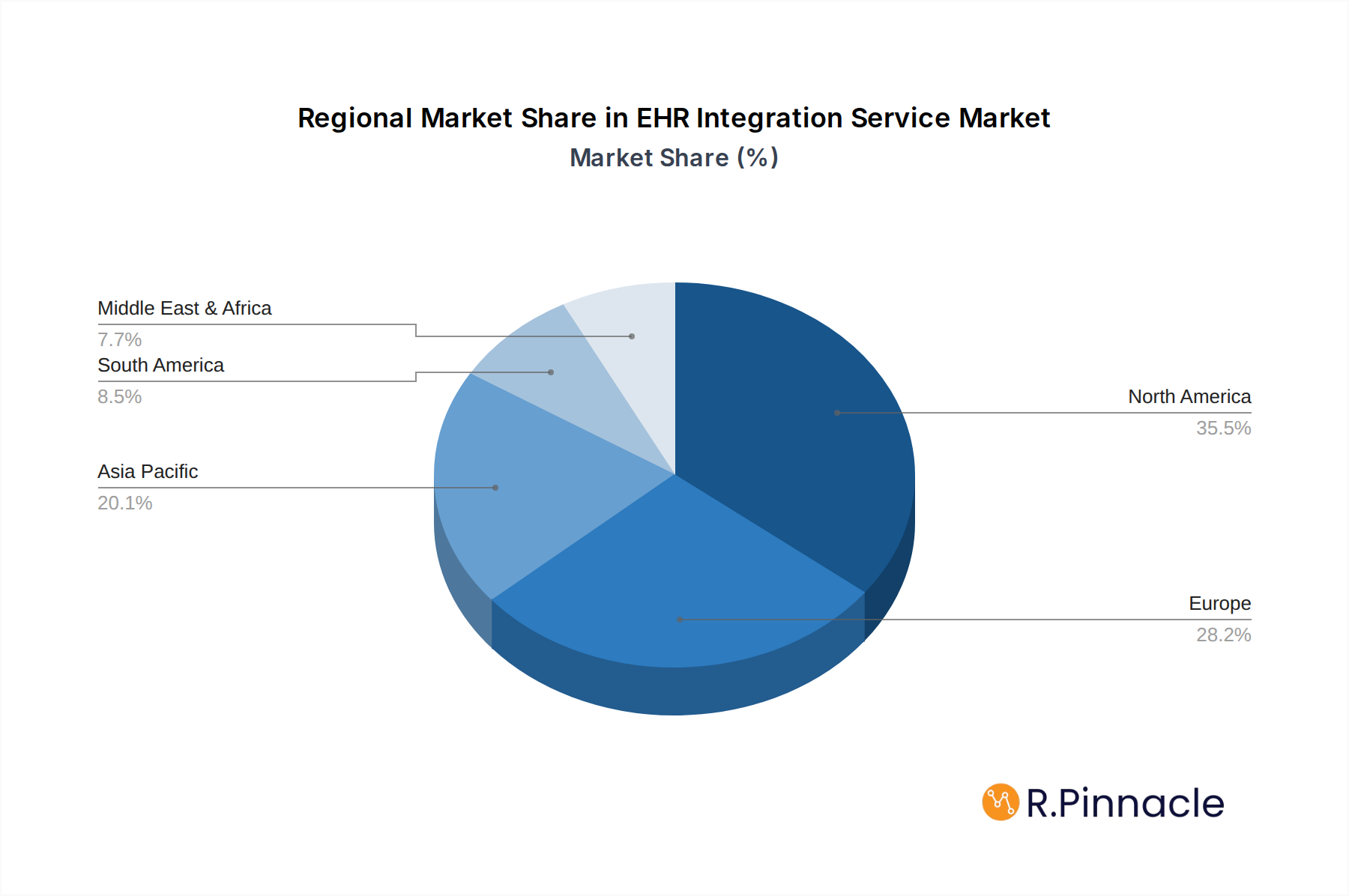

Dominant Regions & Segments in EHR Integration Service

The North American region, particularly the United States, currently holds dominance in the EHR integration service market. This leadership is attributable to several key drivers, including a well-established healthcare infrastructure, significant government investment in healthcare IT, and a proactive regulatory environment that has historically encouraged the adoption of electronic health records and subsequent integration. Advanced technological adoption and a high concentration of leading healthcare organizations further solidify its position.

Within North America, Hospitals represent the largest and most influential segment for EHR integration services. This is driven by the complex operational needs of large healthcare facilities, the critical requirement for seamless data exchange between various departments (e.g., radiology, pathology, emergency rooms), and the substantial budgets allocated to IT infrastructure upgrades. The sheer volume of patient data and the intricate workflows within hospitals necessitate robust and scalable integration solutions.

The Cloud Based type segment is experiencing the most rapid growth and is projected to surpass on-premises solutions in the coming years. This surge is fueled by the inherent advantages of cloud computing: scalability, flexibility, reduced upfront costs, and enhanced accessibility. Cloud-based EHR integration services offer greater agility in deployment and updates, aligning with the dynamic nature of healthcare IT.

Economic policies supportive of digital health initiatives, coupled with robust infrastructure, continue to drive demand. The ongoing digital transformation across healthcare providers, coupled with increasing emphasis on data interoperability for improved patient care and operational efficiency, are key factors contributing to the market's expansion. Furthermore, government incentives and mandates for EHR adoption and meaningful use have historically paved the way for the widespread implementation of integration services, creating a fertile ground for market growth.

EHR Integration Service Product Innovations

Recent product innovations in EHR integration services are primarily focused on enhancing interoperability, improving data security, and leveraging advanced analytics. Companies are developing API-driven platforms that enable seamless data exchange between diverse EHR systems, wearables, and other health applications. The integration of AI and machine learning is enabling smarter data interpretation, predictive analytics for patient risk stratification, and automated workflows. These advancements translate to competitive advantages by offering greater efficiency, enhanced data accuracy, and a more comprehensive view of patient health, ultimately leading to improved care delivery and operational cost savings.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the EHR integration service market. The Application segment includes: Personal (e.g., patient portals, personal health records), Hospital (large healthcare systems), Clinic (physician practices, specialized centers), and Other (e.g., research institutions, public health agencies). The Types segment comprises On-premises solutions and Cloud Based solutions.

Personal applications are expected to witness steady growth as patient engagement with digital health tools increases. Hospital applications will continue to dominate in terms of market size due to the critical need for integrated data in complex environments. The Clinic segment is poised for significant expansion as smaller practices adopt digital solutions to improve efficiency and patient care. The Other segment will see growth driven by specialized healthcare research and public health initiatives.

The Cloud Based segment is projected to exhibit the highest growth rate due to its scalability, cost-effectiveness, and accessibility. The On-premises segment, while still relevant, is expected to see a slower growth trajectory as organizations migrate to cloud solutions.

Key Drivers of EHR Integration Service Growth

The EHR integration service market's growth is propelled by several interconnected factors. Technological advancements, particularly in API development and cloud computing, enable more seamless and scalable data exchange. The regulatory push for interoperability and data sharing, aimed at improving patient outcomes and reducing healthcare costs, is a significant catalyst. Increasing healthcare IT spending by providers globally, driven by the need to modernize infrastructure and enhance operational efficiency, further fuels demand. The growing adoption of value-based care models necessitates integrated data systems for performance tracking and patient outcome measurement.

Challenges in the EHR Integration Service Sector

Despite its growth, the EHR integration service sector faces several challenges. Interoperability challenges remain a persistent hurdle, with varying data standards and legacy systems creating integration complexities. Data security and privacy concerns require robust solutions to comply with stringent regulations like HIPAA and GDPR, increasing implementation costs. High implementation and maintenance costs can be a barrier for smaller healthcare organizations. Furthermore, resistance to change from healthcare professionals and the shortage of skilled IT personnel specialized in healthcare integration can impede adoption.

Emerging Opportunities in EHR Integration Service

Emerging opportunities in the EHR integration service market are abundant. The increasing demand for patient-facing applications and telehealth platforms presents a significant avenue for growth. The integration of AI and machine learning into EHR systems for advanced analytics, predictive diagnostics, and personalized medicine offers new service possibilities. The expansion of wearable device integration for remote patient monitoring and chronic disease management is another key opportunity. Furthermore, the growing need for data analytics and reporting tools to support value-based care initiatives opens doors for specialized integration solutions.

Leading Players in the EHR Integration Service Market

- Keena Health

- Daffodil

- Vocera

- Blue Eagle

- Taction

- ICU Medical

- Clear Arch Health

- EHR Concepts

- Craneware

- Redox

- Folio3

- PointClickCare

- Allscripts

- TELUS

- Wizproinc

- MDofficeManager

- Arcweb Technologies

- Zio

- Bridge Interface

- iatricSystems

- Interopion

- ePDMP

- Chetu

- MEDHOST

- Clarity

- Hyland

- ChartRequest

- PatientIQ

- Silverline

- Cvikota

- HealthTechWiz

- ELEKS

- Knovator

- Datica

- Colan Infotech

Key Developments in EHR Integration Service Industry

- 2023 October: Redox launches enhanced API suite for broader healthcare data exchange.

- 2023 September: Allscripts announces strategic partnership to expand cloud-based integration capabilities.

- 2023 July: PointClickCare acquires a leading provider of clinical data analytics for enhanced interoperability.

- 2023 May: TELUS Health introduces new FHIR-compliant integration platform.

- 2023 April: Hyland acquires a specialist in healthcare content management and integration.

- 2023 February: Chetu expands its EHR integration services for specialized healthcare providers.

- 2022 December: Datica strengthens its cloud integration offerings for healthcare organizations.

- 2022 October: Folio3 announces advancements in custom EHR integration solutions.

- 2022 August: HealthTechWiz showcases innovative solutions for clinic-to-hospital data transfer.

- 2022 June: ELEKS demonstrates AI-powered integration for improved clinical workflows.

Future Outlook for EHR Integration Service Market

The future outlook for the EHR integration service market is exceptionally promising, driven by an unwavering demand for seamless data interoperability and the continuous evolution of digital health technologies. Growth accelerators include the widespread adoption of AI and machine learning for intelligent data utilization, the expansion of telehealth and remote patient monitoring services, and the ongoing push towards value-based care models that rely heavily on integrated data analytics. Strategic opportunities lie in developing specialized integration solutions for niche healthcare segments, enhancing cybersecurity protocols, and fostering greater collaboration across the healthcare ecosystem to overcome existing interoperability barriers. The market is poised for sustained innovation and significant expansion.

EHR Integration Service Segmentation

-

1. Application

- 1.1. Personal

- 1.2. Hospital

- 1.3. Clinic

- 1.4. Other

-

2. Types

- 2.1. On-premises

- 2.2. Cloud Based

EHR Integration Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

EHR Integration Service Regional Market Share

Geographic Coverage of EHR Integration Service

EHR Integration Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.46% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Personal

- 5.1.2. Hospital

- 5.1.3. Clinic

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. On-premises

- 5.2.2. Cloud Based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Personal

- 6.1.2. Hospital

- 6.1.3. Clinic

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. On-premises

- 6.2.2. Cloud Based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Personal

- 7.1.2. Hospital

- 7.1.3. Clinic

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. On-premises

- 7.2.2. Cloud Based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Personal

- 8.1.2. Hospital

- 8.1.3. Clinic

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. On-premises

- 8.2.2. Cloud Based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Personal

- 9.1.2. Hospital

- 9.1.3. Clinic

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. On-premises

- 9.2.2. Cloud Based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific EHR Integration Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Personal

- 10.1.2. Hospital

- 10.1.3. Clinic

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. On-premises

- 10.2.2. Cloud Based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Keena Health

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Daffodil

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Vocera

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Blue Eagle

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Taction

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ICU Medical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Clear Arch Health

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 EHR Concepts

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Craneware

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Redox

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Folio3

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 PointClickCare

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Allscripts

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 TELUS

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Wizproinc

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 MDofficeManager

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Arcweb Technologies

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Zio

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Bridge Interface

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 iatricSystems

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Interopion

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 ePDMP

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Chetu

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 MEDHOST

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Clarity

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Hyland

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 ChartRequest

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 PatientIQ

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Silverline

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Cvikota

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 HealthTechWiz

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 ELEKS

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 Knovator

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 Datica

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 Colan Infotech

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.1 Keena Health

List of Figures

- Figure 1: Global EHR Integration Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America EHR Integration Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America EHR Integration Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America EHR Integration Service Revenue (billion), by Types 2025 & 2033

- Figure 5: North America EHR Integration Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America EHR Integration Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America EHR Integration Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America EHR Integration Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America EHR Integration Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America EHR Integration Service Revenue (billion), by Types 2025 & 2033

- Figure 11: South America EHR Integration Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America EHR Integration Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America EHR Integration Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe EHR Integration Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe EHR Integration Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe EHR Integration Service Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe EHR Integration Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe EHR Integration Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe EHR Integration Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa EHR Integration Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa EHR Integration Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa EHR Integration Service Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa EHR Integration Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa EHR Integration Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa EHR Integration Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific EHR Integration Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific EHR Integration Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific EHR Integration Service Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific EHR Integration Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific EHR Integration Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific EHR Integration Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global EHR Integration Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global EHR Integration Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global EHR Integration Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global EHR Integration Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global EHR Integration Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global EHR Integration Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global EHR Integration Service Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global EHR Integration Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific EHR Integration Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the EHR Integration Service?

The projected CAGR is approximately 12.46%.

2. Which companies are prominent players in the EHR Integration Service?

Key companies in the market include Keena Health, Daffodil, Vocera, Blue Eagle, Taction, ICU Medical, Clear Arch Health, EHR Concepts, Craneware, Redox, Folio3, PointClickCare, Allscripts, TELUS, Wizproinc, MDofficeManager, Arcweb Technologies, Zio, Bridge Interface, iatricSystems, Interopion, ePDMP, Chetu, MEDHOST, Clarity, Hyland, ChartRequest, PatientIQ, Silverline, Cvikota, HealthTechWiz, ELEKS, Knovator, Datica, Colan Infotech.

3. What are the main segments of the EHR Integration Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "EHR Integration Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the EHR Integration Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the EHR Integration Service?

To stay informed about further developments, trends, and reports in the EHR Integration Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence