Key Insights

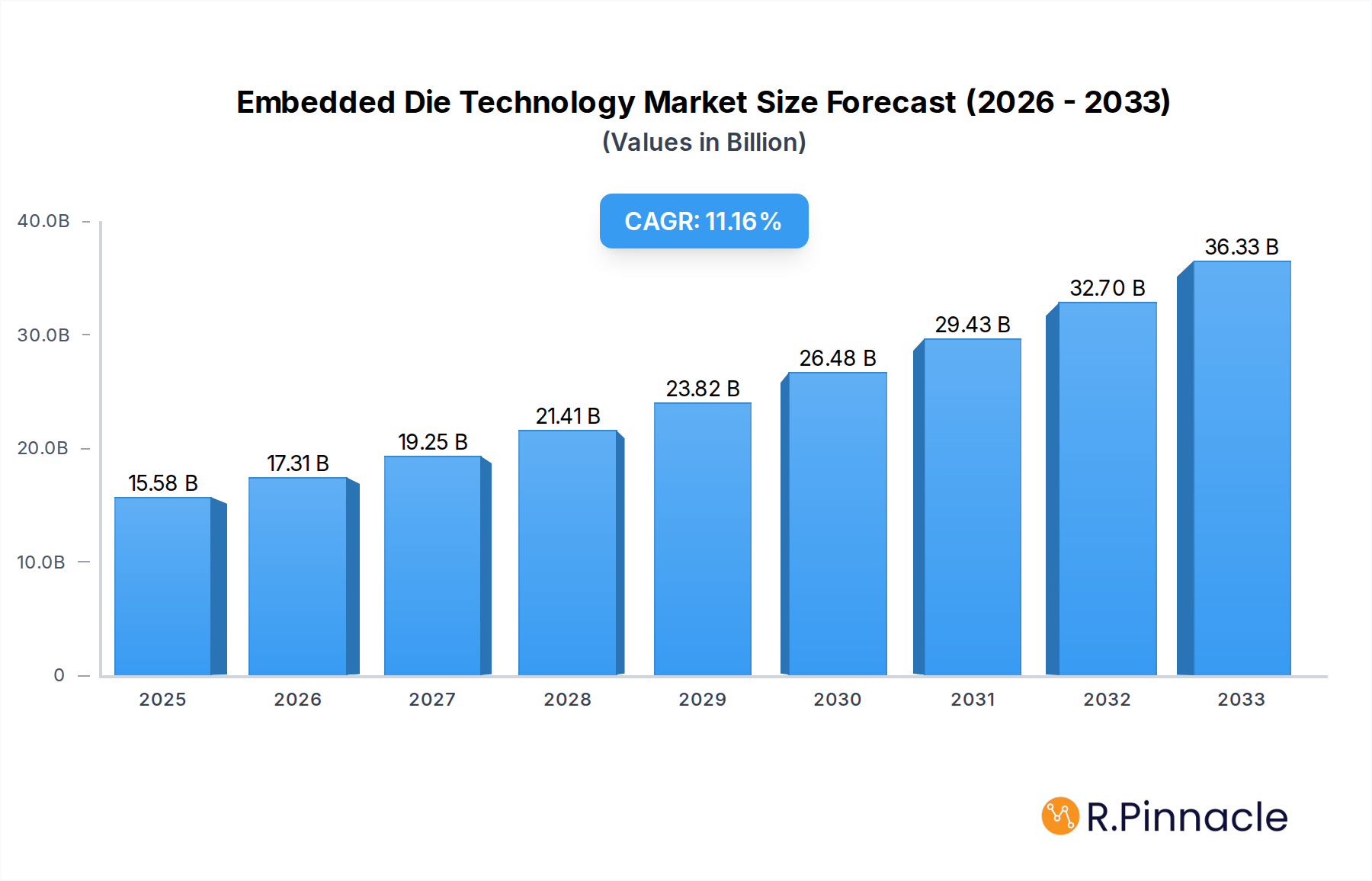

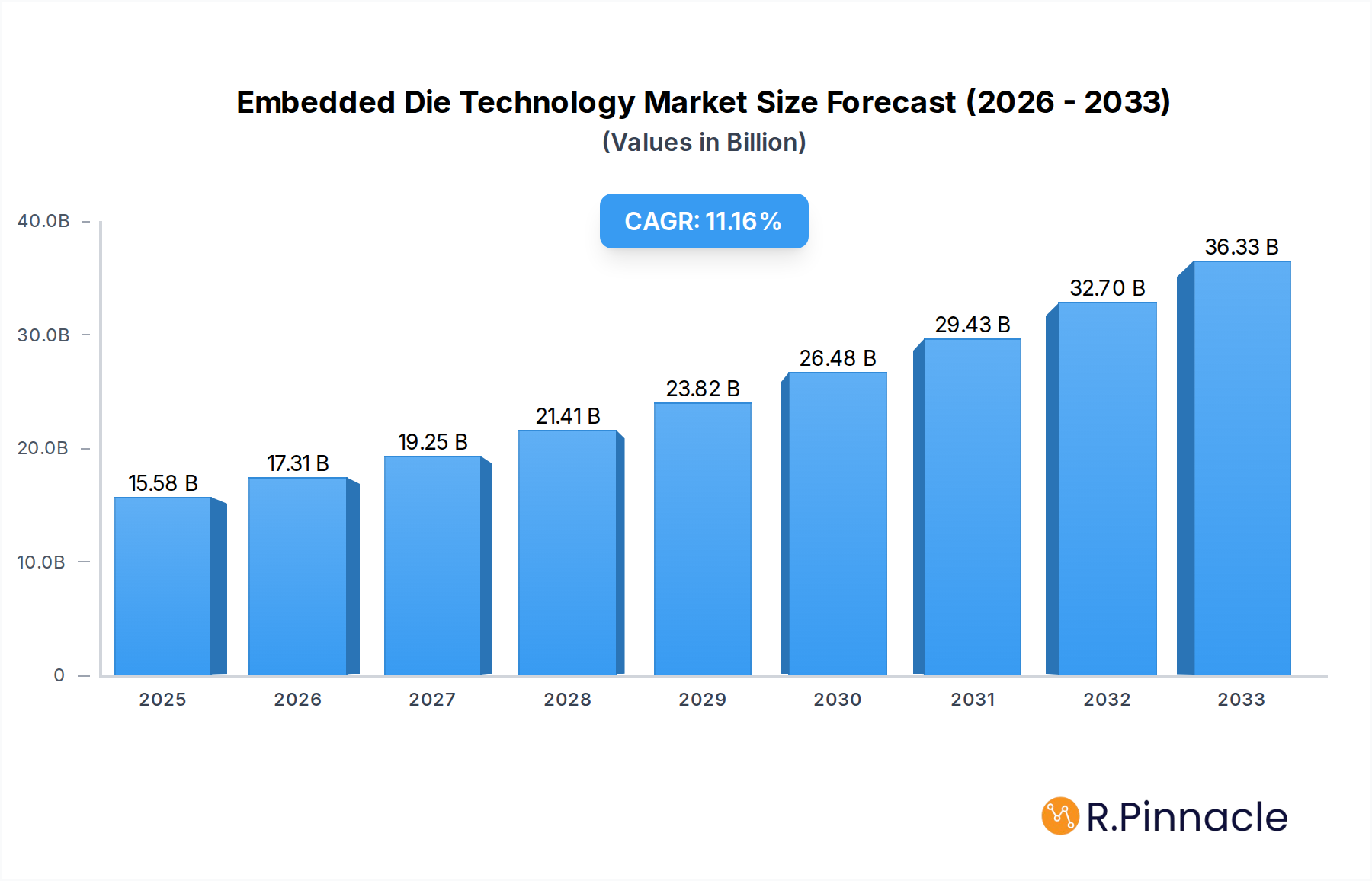

The global Embedded Die Technology market is poised for significant expansion, driven by the relentless demand for miniaturization, enhanced performance, and greater power efficiency across a multitude of industries. With a projected market size of $15.58 billion in 2025, this sector is on a robust growth trajectory, anticipated to expand at a Compound Annual Growth Rate (CAGR) of 11.11% through 2033. This impressive growth is fueled by the increasing integration of advanced semiconductor functionalities into compact and sophisticated electronic devices. Key drivers include the burgeoning consumer electronics sector, with smartphones, wearables, and smart home devices demanding ever-smaller and more powerful components. The automotive industry's transformation towards electric vehicles and autonomous driving systems also necessitates the adoption of embedded die technology for advanced driver-assistance systems (ADAS) and in-vehicle infotainment. Furthermore, the healthcare sector is leveraging this technology for miniaturized medical implants, diagnostic tools, and wearable health monitors, while the IT and telecommunications industry benefits from enhanced data processing capabilities and reduced form factors in networking equipment and servers.

Embedded Die Technology Market Size (In Billion)

The market's expansion is further bolstered by critical trends such as the increasing complexity of integrated circuits and the growing need for heterogeneous integration, where different types of chips are combined within a single package. Advancements in manufacturing processes and materials are enabling more intricate and efficient embedding of dies, leading to improved thermal management and signal integrity. While the market demonstrates strong upward momentum, it faces certain restraints. These include the high initial investment required for advanced manufacturing facilities and the technical challenges associated with yield management and quality control in highly complex embedded systems. However, the overwhelming benefits of embedded die technology, including reduced board space, lower power consumption, and improved overall performance, are expected to outweigh these challenges, ensuring sustained growth and innovation in the coming years. Key segments like Embedded Die in IC Package Substrate and Embedded Die in Rigid Board are expected to dominate, with significant contributions from regions like Asia Pacific and North America.

Embedded Die Technology Company Market Share

Here is an SEO-optimized, reader-centric report description for Embedded Die Technology, designed for high search visibility and engagement with industry professionals.

Embedded Die Technology Market Structure & Innovation Trends

The global Embedded Die Technology market exhibits a moderately concentrated structure, with key players like Intel Corporation, Taiwan Semiconductor Manufacturing Company, ASE Group, and Amkor Technology holding significant market shares, estimated to be over 20 billion by 2025. Innovation is primarily driven by the relentless demand for miniaturization, enhanced performance, and increased power efficiency across a burgeoning range of applications. Leading companies are heavily investing in research and development, focusing on advanced packaging techniques, novel materials, and intricate manufacturing processes. Regulatory frameworks are evolving to support the adoption of advanced semiconductor technologies, particularly in sectors like automotive and healthcare, where stringent reliability and safety standards are paramount. The threat of product substitutes remains relatively low due to the unique advantages offered by embedded die technology in achieving superior electrical and thermal performance compared to traditional packaging methods. End-user demographics are increasingly sophisticated, demanding smaller, more powerful, and integrated electronic devices. Mergers and acquisitions (M&A) are a crucial aspect of market consolidation and strategic growth, with a projected M&A deal value exceeding 10 billion by 2025, as companies seek to acquire specialized expertise and expand their technological portfolios. Fujikura Ltd, Microsemi Corporation, Infineon Technologies AG, Shinko Electric Industries Co. Ltd, TDK Corporation, AT&S Company, and Schweizer Electronic AG are also active participants, contributing to the dynamic competitive landscape and fostering continuous innovation.

Embedded Die Technology Market Dynamics & Trends

The Embedded Die Technology market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 15% from 2019 to 2033. This impressive trajectory is fueled by a confluence of powerful market growth drivers and transformative technological disruptions. The ever-increasing demand for smaller, lighter, and more powerful electronic devices across consumer electronics, automotive, and telecommunications sectors is a primary impetus. Consumers are increasingly expecting sophisticated functionalities within compact form factors, a need that embedded die technology expertly addresses by enabling the integration of multiple components, including ICs and passive elements, directly within the substrate. This not only reduces the overall footprint of electronic assemblies but also significantly improves electrical performance by minimizing signal path lengths and enhancing thermal management.

Technological disruptions are playing a pivotal role. Advances in substrate materials, such as high-density interconnect (HDI) laminates and flexible circuit boards, are enabling more complex and denser embedded die configurations. The development of advanced manufacturing processes, including precise die placement techniques, advanced interconnect technologies like copper pillars and micro-bumps, and sophisticated encapsulation methods, are crucial for realizing the full potential of this technology. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) in semiconductor design and manufacturing is optimizing yield, reducing development cycles, and paving the way for even more intricate embedded die designs.

Consumer preferences are shifting towards devices with enhanced features, longer battery life, and superior connectivity, all of which are facilitated by the advantages of embedded die technology. For instance, the miniaturization offered by embedded die solutions is critical for the proliferation of wearable devices, advanced driver-assistance systems (ADAS) in vehicles, and compact yet powerful medical implants. The competitive dynamics within the market are intense, with established semiconductor manufacturers and specialized packaging providers vying for market share. Strategic partnerships and collaborations are becoming increasingly common as companies aim to combine complementary expertise and offer integrated solutions. The market penetration of embedded die technology is steadily increasing across various applications, driven by its proven ability to deliver superior performance, reduced size, and improved reliability, making it an indispensable technology for next-generation electronic products. The estimated market size for embedded die technology is expected to reach over 70 billion by 2025, with robust growth projected throughout the forecast period.

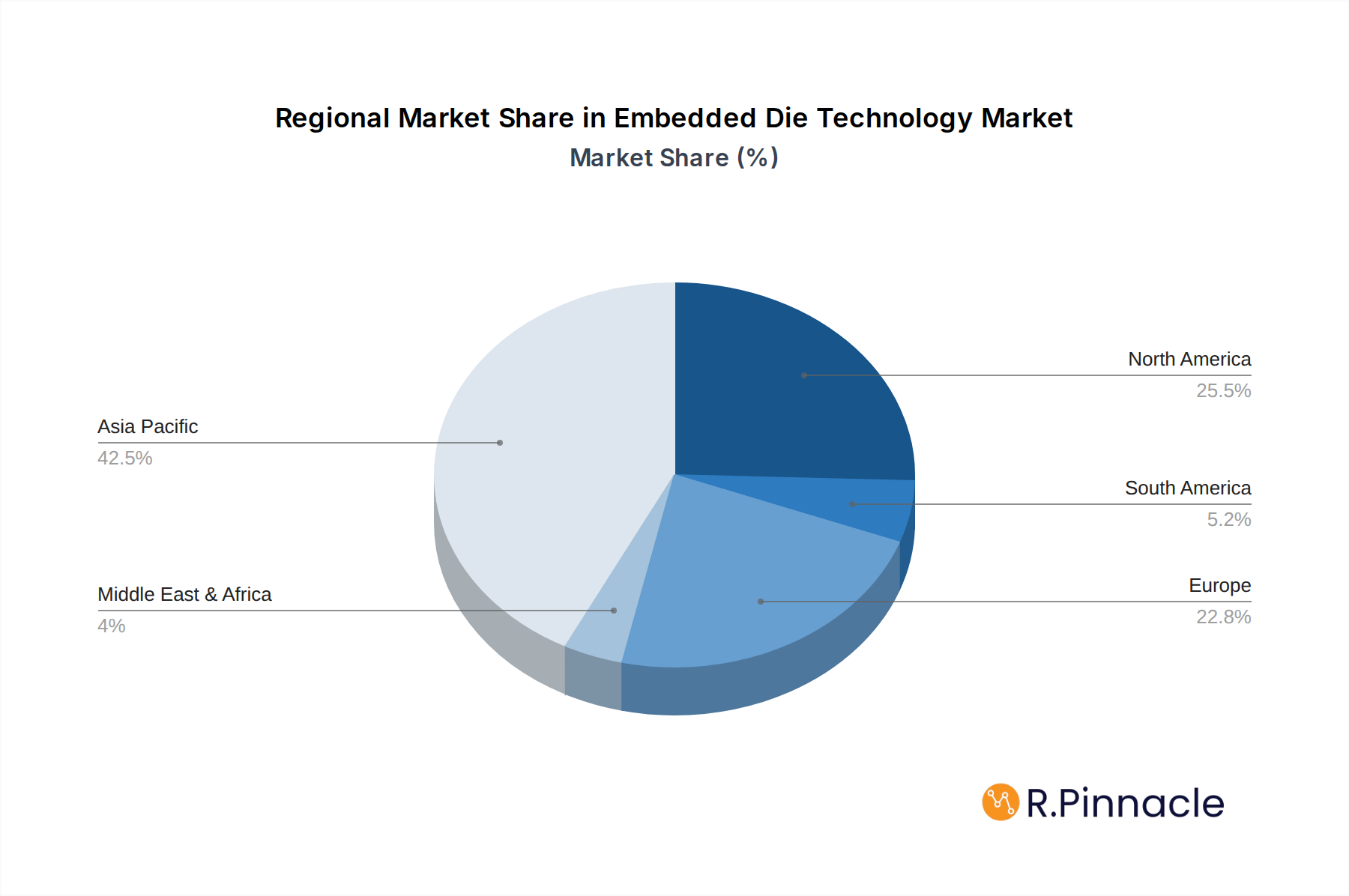

Dominant Regions & Segments in Embedded Die Technology

The Asia-Pacific region stands out as the dominant force in the global Embedded Die Technology market, primarily driven by the strong manufacturing prowess of countries like Taiwan, South Korea, and China. These nations are home to a significant concentration of leading semiconductor foundries, assembly, and testing facilities, including giants like Taiwan Semiconductor Manufacturing Company and ASE Group. Their robust industrial infrastructure, extensive supply chains, and government support for the electronics manufacturing sector create an unparalleled ecosystem for the advancement and adoption of embedded die technologies. The sheer volume of electronic device production in this region, catering to both domestic and international markets, naturally positions it at the forefront of demand for advanced packaging solutions.

Within the Application segmentation, Consumer Electronics represents the largest and most influential segment. The relentless consumer demand for smaller, more powerful, and feature-rich devices, such as smartphones, tablets, wearables, and smart home appliances, is a primary catalyst for the widespread adoption of embedded die technology. This segment benefits from rapid product cycles and a constant push for miniaturization and improved performance, making embedded die solutions indispensable for achieving these goals.

In terms of Type, Embedded Die in IC Package Substrate is currently the most prominent and widely utilized form. This approach allows for the integration of active semiconductor devices and passive components directly onto or within the IC package substrate, offering significant advantages in terms of form factor reduction, improved electrical performance, and enhanced thermal management. The maturity of this technology, coupled with its broad applicability across various electronic devices, contributes to its dominant market position.

Key Drivers for Dominance:

- Strong Manufacturing Base: Asia-Pacific's established semiconductor manufacturing infrastructure, including foundries, OSAT (Outsourced Semiconductor Assembly and Test) providers, and material suppliers.

- Extensive Supply Chain Integration: A well-developed and efficient supply chain that supports the complex processes involved in embedded die technology.

- Government Initiatives and Investment: Favorable government policies, R&D funding, and tax incentives aimed at fostering the growth of the semiconductor industry.

- Cost Competitiveness: The ability to produce at scale and at competitive costs, attracting global electronics manufacturers.

- Rapid Technological Adoption: A proactive approach to adopting and integrating new technologies, including advanced packaging solutions.

The Automotive segment is witnessing significant growth, driven by the increasing complexity of in-car electronics, including advanced driver-assistance systems (ADAS), infotainment systems, and electric vehicle (EV) powertrains, all of which benefit from the reliability, miniaturization, and performance enhancements offered by embedded die technology. The Healthcare sector, while smaller in volume, presents high-value opportunities due to the demand for miniaturized and highly reliable medical devices and implants. The IT and Telecommunications sector, encompassing servers, networking equipment, and data centers, also relies heavily on embedded die for high-performance computing and efficient signal processing. The "Other" segment, which includes industrial electronics and defense applications, further contributes to the diversified adoption of this technology.

The Embedded Die in Rigid Board segment is also experiencing robust growth, particularly for applications requiring structural integrity and higher power handling capabilities. Conversely, the Embedded Die in Flexible Board segment is emerging as a critical enabler for flexible electronics, wearable devices, and innovative form factors, showcasing significant growth potential. The interplay between these segments and their respective drivers underscores the pervasive impact and expanding reach of embedded die technology across a multitude of industries. The market size for embedded die technology is projected to exceed 70 billion by 2025, with significant contributions from all these segments.

Embedded Die Technology Product Innovations

Product innovations in embedded die technology are centered on achieving unprecedented levels of integration, performance, and miniaturization. Companies are developing advanced techniques for embedding high-density interconnect (HDI) substrates with multiple dies, including complex ICs and passive components, directly within a single package. This leads to substantial reductions in form factor and parasitic inductance, enhancing signal integrity and power efficiency. Innovations in heterogeneous integration, allowing for the seamless combination of diverse semiconductor technologies (e.g., logic, memory, RF, power) within a single package, are also key. These advancements provide manufacturers with a significant competitive advantage by enabling the creation of highly optimized and compact solutions for demanding applications in consumer electronics, automotive, and telecommunications. The market is expected to see further breakthroughs in thermal management solutions for densely packed embedded dies, ensuring reliability and longevity.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Embedded Die Technology market, segmented by Application and Type.

Under Application, the market is analyzed across Consumer Electronics, Automotive, Healthcare, IT and Telecommunications, and Other segments. Consumer Electronics is projected to maintain its leading position due to high volume demand. Automotive applications are expected to exhibit the highest growth rate, driven by advancements in vehicle electronics.

In terms of Type, the segmentation includes Embedded Die in IC Package Substrate, Embedded Die in Rigid Board, and Embedded Die in Flexible Board. Embedded Die in IC Package Substrate currently dominates the market but Embedded Die in Flexible Board is anticipated to experience rapid growth owing to its suitability for emerging flexible electronics. Each segment's growth projections, estimated market sizes, and competitive dynamics are thoroughly examined.

Key Drivers of Embedded Die Technology Growth

The growth of the Embedded Die Technology sector is primarily propelled by several key factors. The relentless demand for miniaturization and higher performance in electronic devices across all industries is a significant driver. Technological advancements in semiconductor manufacturing, particularly in packaging and interconnect technologies, enable more complex and efficient integration of multiple dies. The increasing adoption of advanced technologies like AI, 5G, and IoT requires more sophisticated and compact electronic solutions. Furthermore, the need for improved power efficiency and thermal management in high-density electronic assemblies directly benefits from the capabilities offered by embedded die technology. Regulatory support for innovation in advanced semiconductor manufacturing also plays a crucial role in fostering market expansion.

Challenges in the Embedded Die Technology Sector

Despite its strong growth trajectory, the Embedded Die Technology sector faces several significant challenges. The complexity of the manufacturing process demands high precision and introduces potential yield issues, leading to higher production costs compared to traditional packaging methods. The intricate nature of these advanced packages can also pose challenges for testing and reliability assessment, requiring specialized equipment and methodologies. Supply chain disruptions and the availability of critical raw materials can impact production schedules and costs. Moreover, the rapid pace of technological evolution necessitates continuous investment in R&D to remain competitive, posing a financial burden for some players. The intellectual property landscape, with numerous patents surrounding advanced packaging, can also create hurdles for market entrants.

Emerging Opportunities in Embedded Die Technology

Emerging opportunities in the Embedded Die Technology market are abundant and diverse. The burgeoning fields of augmented reality (AR) and virtual reality (VR) present a significant demand for compact, high-performance processing units. The expansion of the Internet of Things (IoT) ecosystem, with its myriad of connected devices, requires innovative and miniaturized electronic solutions that embedded die technology can provide. The growth of electric vehicles (EVs) and autonomous driving technologies is creating new opportunities for embedded power modules and advanced sensor integration. Furthermore, the development of next-generation medical devices, including implantable sensors and advanced diagnostics, offers lucrative avenues for this technology. The ongoing advancements in 3D IC integration and fan-out wafer-level packaging techniques also unlock new possibilities for creating highly integrated and powerful chiplets.

Leading Players in the Embedded Die Technology Market

- Microsemi Corporation

- Fujikura Ltd

- Infineon Technologies AG

- ASE Group

- AT&S Company

- Schweizer Electronic AG

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company

- Shinko Electric Industries Co. Ltd

- Amkor Technology

- TDK Corporation

Key Developments in Embedded Die Technology Industry

- 2023 Q4: Intel Corporation announces significant advancements in its Foveros 3D packaging technology, enabling more complex chiplet architectures suitable for embedded die applications.

- 2023 Q3: ASE Group expands its advanced packaging capabilities, investing in new facilities to support the growing demand for embedded die solutions in the automotive sector.

- 2023 Q2: Taiwan Semiconductor Manufacturing Company (TSMC) reports a breakthrough in its CoWoS (Chip-on-Wafer-on-Substrate) technology, enhancing its suitability for high-performance embedded die applications.

- 2023 Q1: Amkor Technology introduces a new generation of fan-out wafer-level packaging technology, offering smaller form factors and improved performance for embedded die integration.

- 2022 Q4: Fujikura Ltd showcases innovative flexible substrate materials designed for advanced embedded die applications in wearable and flexible electronics.

- 2022 Q3: Infineon Technologies AG highlights its progress in embedding power semiconductors directly into package substrates for more efficient automotive power management solutions.

- 2022 Q2: AT&S Company announces capacity expansion for its high-density interconnect (HDI) substrates, a critical component for embedded die technology.

- 2022 Q1: Shinko Electric Industries Co. Ltd unveils new interconnection technologies for high-density embedded die packages, improving thermal performance and reliability.

- 2021 Q4: Schweizer Electronic AG demonstrates advancements in embedding passive components alongside active dies on rigid boards, enhancing functional integration.

- 2021 Q3: TDK Corporation showcases its range of embedded passive components that can be integrated into embedded die substrates, offering a comprehensive solution.

Future Outlook for Embedded Die Technology Market

The future outlook for the Embedded Die Technology market is exceptionally bright, characterized by sustained high growth and continuous innovation. The increasing complexity of electronic systems, driven by advancements in AI, 5G, autonomous systems, and the expanding IoT landscape, will continue to fuel the demand for miniaturized, high-performance, and power-efficient solutions. The ongoing evolution of heterogeneous integration techniques, enabling the seamless combination of diverse chiplets and functionalities within a single package, will be a major growth accelerator. Strategic investments in advanced manufacturing processes, materials science, and intellectual property development will be crucial for market leaders to maintain their competitive edge. Emerging applications in areas like advanced healthcare, quantum computing, and high-performance computing will open up new market frontiers, ensuring a robust and dynamic future for embedded die technology. The market is projected to reach over 100 billion by 2033.

Embedded Die Technology Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Automotive

- 1.3. Healthcare

- 1.4. IT and Telecommunications

- 1.5. Other

-

2. Type

- 2.1. Embedded Die in IC Package Substrate

- 2.2. Embedded Die in Rigid Board

- 2.3. Embedded Die in Flexible Board

Embedded Die Technology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Embedded Die Technology Regional Market Share

Geographic Coverage of Embedded Die Technology

Embedded Die Technology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Automotive

- 5.1.3. Healthcare

- 5.1.4. IT and Telecommunications

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Embedded Die in IC Package Substrate

- 5.2.2. Embedded Die in Rigid Board

- 5.2.3. Embedded Die in Flexible Board

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Automotive

- 6.1.3. Healthcare

- 6.1.4. IT and Telecommunications

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Embedded Die in IC Package Substrate

- 6.2.2. Embedded Die in Rigid Board

- 6.2.3. Embedded Die in Flexible Board

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Automotive

- 7.1.3. Healthcare

- 7.1.4. IT and Telecommunications

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Embedded Die in IC Package Substrate

- 7.2.2. Embedded Die in Rigid Board

- 7.2.3. Embedded Die in Flexible Board

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Automotive

- 8.1.3. Healthcare

- 8.1.4. IT and Telecommunications

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Embedded Die in IC Package Substrate

- 8.2.2. Embedded Die in Rigid Board

- 8.2.3. Embedded Die in Flexible Board

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Automotive

- 9.1.3. Healthcare

- 9.1.4. IT and Telecommunications

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Embedded Die in IC Package Substrate

- 9.2.2. Embedded Die in Rigid Board

- 9.2.3. Embedded Die in Flexible Board

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Embedded Die Technology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Automotive

- 10.1.3. Healthcare

- 10.1.4. IT and Telecommunications

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Embedded Die in IC Package Substrate

- 10.2.2. Embedded Die in Rigid Board

- 10.2.3. Embedded Die in Flexible Board

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Microsemi Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Fujikura Ltd

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Infineon Technologies AG

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ASE Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 AT&S Company

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Schweizer Electronic AG

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Intel Corporation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Taiwan Semiconductor Manufacturing Company

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shinko Electric Industries Co. Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Amkor Technology

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 TDK Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Microsemi Corporation

List of Figures

- Figure 1: Global Embedded Die Technology Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Embedded Die Technology Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Embedded Die Technology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Embedded Die Technology Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Embedded Die Technology Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Embedded Die Technology Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Embedded Die Technology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Embedded Die Technology Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Embedded Die Technology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Embedded Die Technology Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Embedded Die Technology Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Embedded Die Technology Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Embedded Die Technology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Embedded Die Technology Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Embedded Die Technology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Embedded Die Technology Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Embedded Die Technology Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Embedded Die Technology Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Embedded Die Technology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Embedded Die Technology Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Embedded Die Technology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Embedded Die Technology Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Embedded Die Technology Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Embedded Die Technology Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Embedded Die Technology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Embedded Die Technology Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Embedded Die Technology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Embedded Die Technology Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Embedded Die Technology Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Embedded Die Technology Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Embedded Die Technology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Embedded Die Technology Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Embedded Die Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Embedded Die Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Embedded Die Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Embedded Die Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Embedded Die Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Embedded Die Technology Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Embedded Die Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Embedded Die Technology Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Embedded Die Technology?

The projected CAGR is approximately 20.5%.

2. Which companies are prominent players in the Embedded Die Technology?

Key companies in the market include Microsemi Corporation, Fujikura Ltd, Infineon Technologies AG, ASE Group, AT&S Company, Schweizer Electronic AG, Intel Corporation, Taiwan Semiconductor Manufacturing Company, Shinko Electric Industries Co. Ltd, Amkor Technology, TDK Corporation.

3. What are the main segments of the Embedded Die Technology?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Embedded Die Technology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Embedded Die Technology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Embedded Die Technology?

To stay informed about further developments, trends, and reports in the Embedded Die Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence