Key Insights

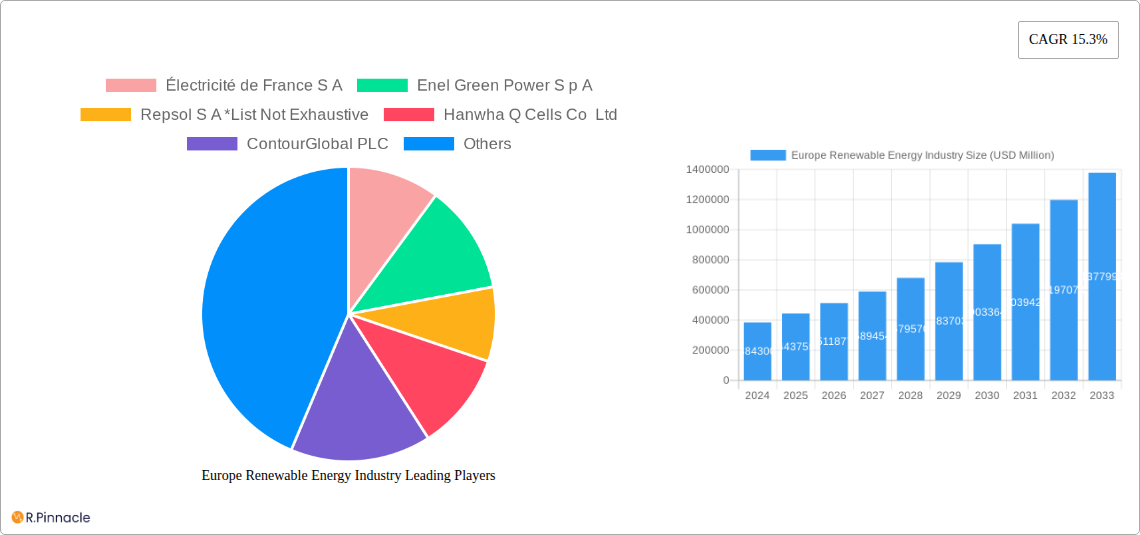

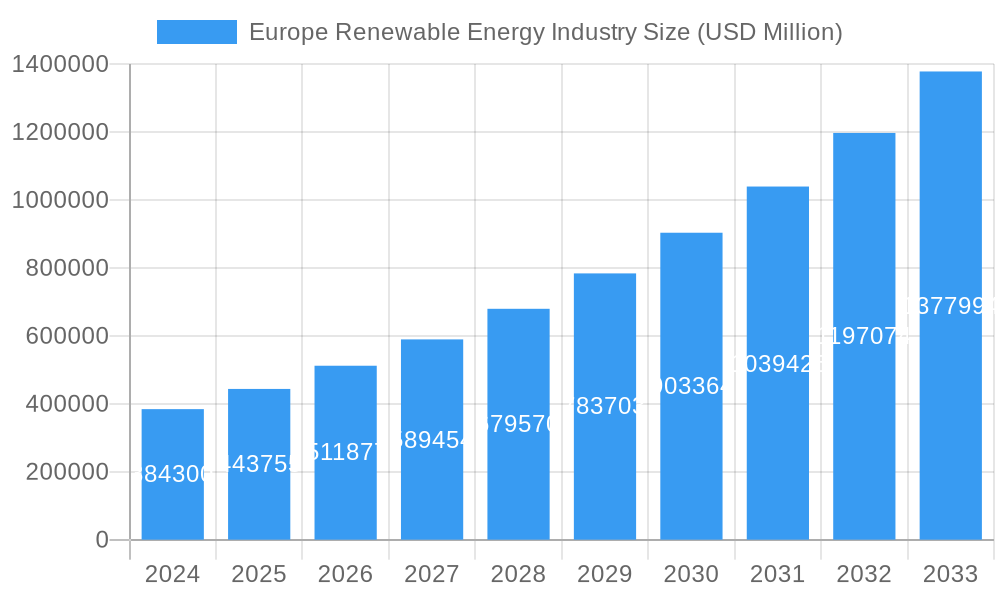

The European Renewable Energy Industry is experiencing robust growth, projected to reach a substantial $384.3 billion in 2024, with a compelling Compound Annual Growth Rate (CAGR) of 15.3% over the forecast period from 2025 to 2033. This expansion is primarily fueled by a confluence of factors, including ambitious government policies and regulatory frameworks across the continent aimed at decarbonization and energy independence. The increasing urgency to combat climate change, coupled with declining technology costs for solar photovoltaic and wind power, are significant drivers propelling market adoption. Furthermore, a growing public awareness and demand for sustainable energy solutions are creating a favorable environment for renewable energy investments. The industry is witnessing a pronounced trend towards greater integration of renewable sources into the existing grid infrastructure, supported by advancements in energy storage technologies and smart grid solutions.

Europe Renewable Energy Industry Market Size (In Billion)

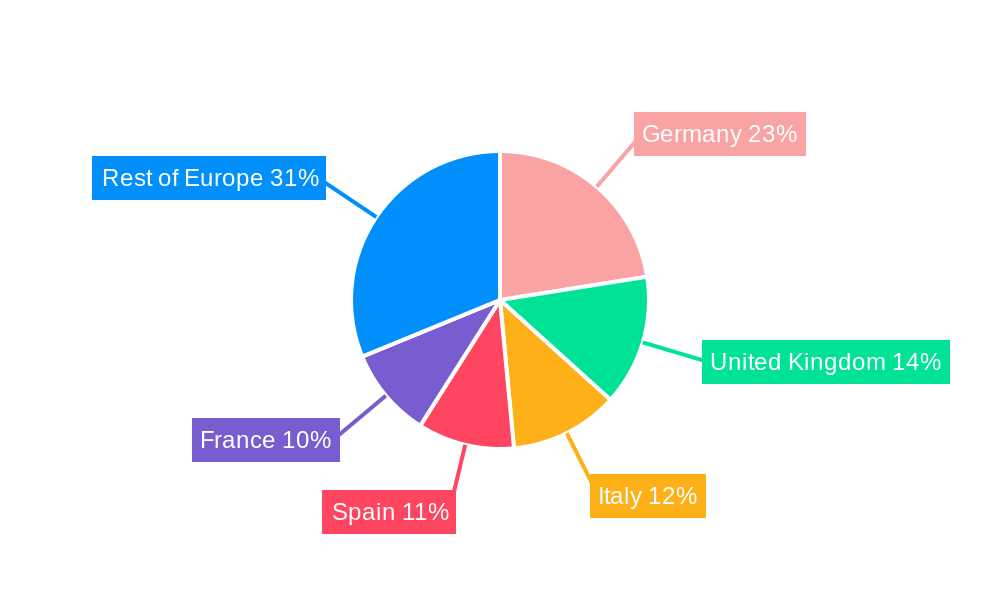

Despite the overwhelmingly positive trajectory, certain restraints are present. The initial capital investment for large-scale renewable energy projects can be substantial, posing a hurdle for some developers. Grid modernization and expansion efforts, while underway, sometimes lag behind the pace of renewable energy deployment, leading to integration challenges. Intermittency of certain renewable sources like solar and wind power necessitates sophisticated grid management and backup solutions. Nonetheless, the overarching drive towards a green economy, coupled with the strategic imperative for energy security in light of geopolitical shifts, ensures that these restraints are actively being addressed through innovation and policy. Key segments include Hydropower, Solar, Wind, and Others, with significant players like Électricité de France S.A., Enel Green Power S.p.A., and Repsol S.A. driving innovation and market expansion across key European regions like Germany, France, and Spain.

Europe Renewable Energy Industry Company Market Share

Europe Renewable Energy Industry Market Analysis Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe Renewable Energy Industry, covering the historical period from 2019-2024 and forecasting market performance through 2033. With a base year of 2025, this study leverages high-ranking keywords and actionable insights to equip industry professionals, investors, and policymakers with critical data for strategic decision-making. The European renewable energy sector is projected to witness significant expansion, driven by ambitious decarbonization targets and technological advancements.

Europe Renewable Energy Industry Market Structure & Innovation Trends

The European renewable energy market is characterized by a moderate level of concentration, with key players like Électricité de France S.A., Enel Green Power S.p.A., and Repsol S.A. holding substantial market shares, estimated in the billions of Euros. Innovation is a primary driver, fueled by substantial research and development investments in areas such as offshore wind turbine efficiency, advanced solar photovoltaic (PV) technologies, and smart grid integration. Regulatory frameworks, including the EU's Renewable Energy Directive and national support schemes, play a pivotal role in shaping market dynamics and encouraging investment. While product substitutes exist, such as advancements in energy storage solutions, the inherent sustainability and declining costs of renewable sources are diminishing their competitive threat. End-user demographics are increasingly leaning towards corporate power purchase agreements (PPAs) and individual green energy adoption. Mergers and acquisitions (M&A) activity is robust, with deal values in the billions, demonstrating consolidation and strategic expansion. For instance, in September 2022, Orsted AS's acquisition of Ostwind's wind and solar PV projects in Germany and France, valued in the hundreds of millions of Euros, highlights this trend.

Europe Renewable Energy Industry Market Dynamics & Trends

The Europe renewable energy industry is poised for remarkable growth, with a projected Compound Annual Growth Rate (CAGR) of over 10% during the forecast period. This expansion is primarily fueled by escalating global demand for clean energy, driven by stringent climate change policies and a growing awareness of environmental sustainability. Technological disruptions are at the forefront of this transformation. Innovations in solar PV technology, such as perovskite solar cells, are enhancing efficiency and reducing manufacturing costs, making solar power increasingly competitive. Similarly, advancements in wind turbine technology, including larger rotor diameters and enhanced offshore capabilities, are unlocking new potential. Consumer preferences are shifting significantly, with a growing demand for renewable energy sources from both residential and commercial sectors. Companies are increasingly setting ambitious renewable energy targets, further stimulating market penetration. Competitive dynamics are intensifying, with a race to secure prime locations for renewable energy projects and to develop cutting-edge technologies. The market penetration of renewable energy in the overall European energy mix is expected to surpass 50% by 2030, representing a substantial shift away from fossil fuels. Significant investments, estimated in the tens of billions of Euros annually, are pouring into the sector, supporting the development of new projects and the upgrading of existing infrastructure.

Dominant Regions & Segments in Europe Renewable Energy Industry

The Wind segment is a dominant force in the European renewable energy landscape, driven by favorable geographical conditions, particularly in Northern Europe, and significant government support. Countries like Germany, the United Kingdom, and Denmark are leading the charge in wind energy deployment, with substantial installed capacities reaching hundreds of gigawatts.

- Economic Policies: Robust feed-in tariffs, tax incentives, and auction mechanisms have historically provided strong financial backing for wind farm development, encouraging substantial investment in the billions of Euros.

- Infrastructure: The development of offshore wind farms, supported by extensive port facilities and specialized vessels, has opened up vast untapped resources and contributed significantly to job creation and economic growth in coastal regions.

- Technological Advancements: Continuous innovation in turbine design, leading to increased efficiency and reduced operational costs, has made wind power an increasingly cost-effective energy source, further solidifying its dominance.

The Solar segment is also experiencing rapid growth, particularly in Southern Europe, where sunlight availability is abundant. Spain, Italy, and France are at the forefront of solar PV adoption, with market growth driven by declining panel costs and the increasing popularity of distributed generation.

- Policy Support: National solar strategies and net-metering policies have incentivized both utility-scale projects and rooftop solar installations, attracting investments in the billions of Euros.

- Technological Innovation: Improvements in solar panel efficiency and the development of energy storage solutions are enhancing the reliability and dispatchability of solar power.

- Corporate Demand: A growing number of corporations are seeking to power their operations with solar energy through Power Purchase Agreements (PPAs), contributing to market expansion.

While Hydropower remains a significant contributor to the renewable energy mix in Europe, particularly in countries with extensive river systems like Norway and Switzerland, its growth potential is more limited due to site-specific constraints. The Others segment, encompassing geothermal, biomass, and emerging technologies, is gradually gaining traction, supported by diversification strategies and niche market opportunities.

Europe Renewable Energy Industry Product Innovations

Product innovations in the Europe renewable energy industry are primarily focused on enhancing efficiency, reducing costs, and improving grid integration. Developments in solar PV include bifacial solar panels that capture sunlight from both sides, increasing energy yield by up to 25%, and flexible solar films for wider application possibilities. In wind energy, advancements in smart rotor blade technology and floating offshore wind platforms are enabling installations in previously inaccessible deep-water locations, unlocking vast untapped potential. Furthermore, innovations in energy storage solutions, such as solid-state batteries and advanced flow batteries, are crucial for overcoming the intermittency of renewable sources, offering enhanced grid stability and enabling higher renewable energy penetration. These innovations provide a significant competitive advantage by making renewable energy more reliable, cost-effective, and versatile.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Europe Renewable Energy Industry segmented by Type. The Hydropower segment, a mature but stable contributor, is projected to maintain a steady market share, with growth primarily driven by upgrades to existing facilities and small-scale projects, estimated to be in the hundreds of millions of Euros. The Solar segment is expected to experience the highest growth rate, fueled by declining costs and supportive policies, with market sizes projected to reach tens of billions of Euros by 2033. The Wind segment, encompassing both onshore and offshore installations, will continue its robust expansion, driven by large-scale project development and technological advancements, with market values reaching hundreds of billions of Euros. The Others segment, including geothermal and biomass, represents a growing area of opportunity, with targeted investments in niche applications and emerging technologies, contributing several billions of Euros to the overall market.

Key Drivers of Europe Renewable Energy Industry Growth

The growth of the Europe renewable energy industry is propelled by a confluence of critical factors. Foremost among these is the strong and unwavering commitment from European Union member states to achieve ambitious decarbonization targets and enhance energy security, exemplified by policies aiming for a significant increase in renewable energy's share in the total energy mix. Technologically, continuous innovation in solar photovoltaic (PV) efficiency, wind turbine technology (including larger turbines and floating offshore platforms), and advanced energy storage solutions is making renewables increasingly competitive and reliable. Economically, declining capital costs for renewable energy technologies and favorable financing mechanisms, such as green bonds and PPAs, are attracting substantial investments. Furthermore, a growing public awareness and demand for sustainable energy solutions are creating a favorable market environment.

Challenges in the Europe Renewable Energy Industry Sector

Despite its robust growth, the Europe renewable energy industry faces several significant challenges. Regulatory hurdles and permitting complexities can lead to project delays and increased costs, particularly for large-scale infrastructure projects. Supply chain disruptions and the rising cost of raw materials, such as rare earth metals for wind turbine components and polysilicon for solar panels, can impact project economics and timelines. Intermittency of renewable sources and the need for substantial grid upgrades and energy storage solutions to ensure grid stability represent ongoing technical and financial challenges. Intense competition among developers and the need for continuous innovation to maintain cost-competitiveness also pressure profit margins. The evolving geopolitical landscape and energy security concerns can also introduce market volatility.

Emerging Opportunities in Europe Renewable Energy Industry

The Europe renewable energy industry is ripe with emerging opportunities. The burgeoning offshore wind market, particularly in the North Sea and Baltic Sea, presents vast potential for large-scale project development, attracting billions in investment. Advancements in green hydrogen production, utilizing renewable electricity, are opening new avenues for decarbonizing hard-to-abate sectors like heavy industry and transportation. The increasing adoption of smart grids and distributed energy resources, including battery storage and electric vehicles, is creating a more flexible and resilient energy system. Furthermore, the growing demand for sustainable aviation fuels and the electrification of heating and cooling systems represent significant growth avenues. Investment in circular economy principles for renewable energy components also offers a promising and sustainable future.

Leading Players in the Europe Renewable Energy Industry Market

- Électricité de France S.A.

- Enel Green Power S.p.A.

- Repsol S.A.

- Hanwha Q Cells Co Ltd

- ContourGlobal PLC

- Acciona S.A.

- Abengoa SA

- Andritz AG

Key Developments in Europe Renewable Energy Industry Industry

- September 2022: Orsted AS entered into an agreement to acquire a 100% equity interest in OSTWIND Erneuerbare Energien GmbH, OSTWINDpark Rotmainquelle GmbH & Co. K.G., OSTWIND International S.A.S., and OSTWIND Engineering S.A.S., a developer of wind and solar PV projects in Germany and France. This strategic move underscores Orsted's commitment to expanding its renewable energy portfolio.

- September 2022: Mercedes-Benz announced plans to build a wind farm in the northwestern German state of Lower Saxony, scheduled for completion by 2025. This wind farm will have a capacity of 100 megawatts, capable of producing over 15% of the carmaker's annual electricity demand in Germany, highlighting a growing trend of corporate investment in direct renewable energy generation.

Future Outlook for Europe Renewable Energy Industry Market

The future outlook for the Europe Renewable Energy Industry is exceptionally positive, driven by sustained policy support, rapid technological advancements, and increasing market demand. Projections indicate continued strong growth in wind and solar power, with significant expansion in offshore wind and distributed solar generation. The development of the green hydrogen economy is expected to become a major growth accelerator, supported by EU initiatives and substantial investment. Enhanced grid infrastructure and sophisticated energy storage solutions will be critical in managing the increasing share of renewables. The industry is also likely to see further consolidation through strategic M&A activities as companies aim to secure market position and leverage economies of scale. The pursuit of energy independence and ambitious climate targets will continue to fuel innovation and investment, ensuring a dynamic and expanding European renewable energy market.

Europe Renewable Energy Industry Segmentation

-

1. Type

- 1.1. Hydropower

- 1.2. Solar

- 1.3. Wind

- 1.4. Others

Europe Renewable Energy Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. Spain

- 5. France

- 6. Rest of Europe

Europe Renewable Energy Industry Regional Market Share

Geographic Coverage of Europe Renewable Energy Industry

Europe Renewable Energy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hydropower

- 5.1.2. Solar

- 5.1.3. Wind

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Germany

- 5.2.2. United Kingdom

- 5.2.3. Italy

- 5.2.4. Spain

- 5.2.5. France

- 5.2.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Hydropower

- 6.1.2. Solar

- 6.1.3. Wind

- 6.1.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Germany Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Hydropower

- 7.1.2. Solar

- 7.1.3. Wind

- 7.1.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. United Kingdom Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Hydropower

- 8.1.2. Solar

- 8.1.3. Wind

- 8.1.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Italy Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Hydropower

- 9.1.2. Solar

- 9.1.3. Wind

- 9.1.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Hydropower

- 10.1.2. Solar

- 10.1.3. Wind

- 10.1.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. France Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Hydropower

- 11.1.2. Solar

- 11.1.3. Wind

- 11.1.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Europe Europe Renewable Energy Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Hydropower

- 12.1.2. Solar

- 12.1.3. Wind

- 12.1.4. Others

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Électricité de France S A

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Enel Green Power S p A

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Repsol S A *List Not Exhaustive

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Hanwha Q Cells Co Ltd

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 ContourGlobal PLC

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Acciona S A

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Abengoa SA

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Andritz AG

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Électricité de France S A

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Europe Renewable Energy Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Renewable Energy Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 3: Europe Renewable Energy Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Region 2020 & 2033

- Table 5: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 7: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 9: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 11: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 13: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 15: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 17: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 19: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 21: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 23: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 25: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 27: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Renewable Energy Industry?

The projected CAGR is approximately 14.6%.

2. Which companies are prominent players in the Europe Renewable Energy Industry?

Key companies in the market include Électricité de France S A, Enel Green Power S p A, Repsol S A *List Not Exhaustive, Hanwha Q Cells Co Ltd, ContourGlobal PLC, Acciona S A, Abengoa SA, Andritz AG.

3. What are the main segments of the Europe Renewable Energy Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1711.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Integration of Renewable Energy4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Wind Energy Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

High infrastructure costs.

8. Can you provide examples of recent developments in the market?

In September 2022, Orsted AS entered into an agreement with Ostwind, a developer of wind and solar PV projects in Germany and France, to acquire a 100 per cent equity interest in OSTWIND Erneuerbare Energien GmbH, OSTWINDpark Rotmainquelle GmbH & Co. K.G., OSTWIND International S.A.S., and OSTWIND Engineering S.A.S.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Gigawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Renewable Energy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Renewable Energy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Renewable Energy Industry?

To stay informed about further developments, trends, and reports in the Europe Renewable Energy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence