Key Insights

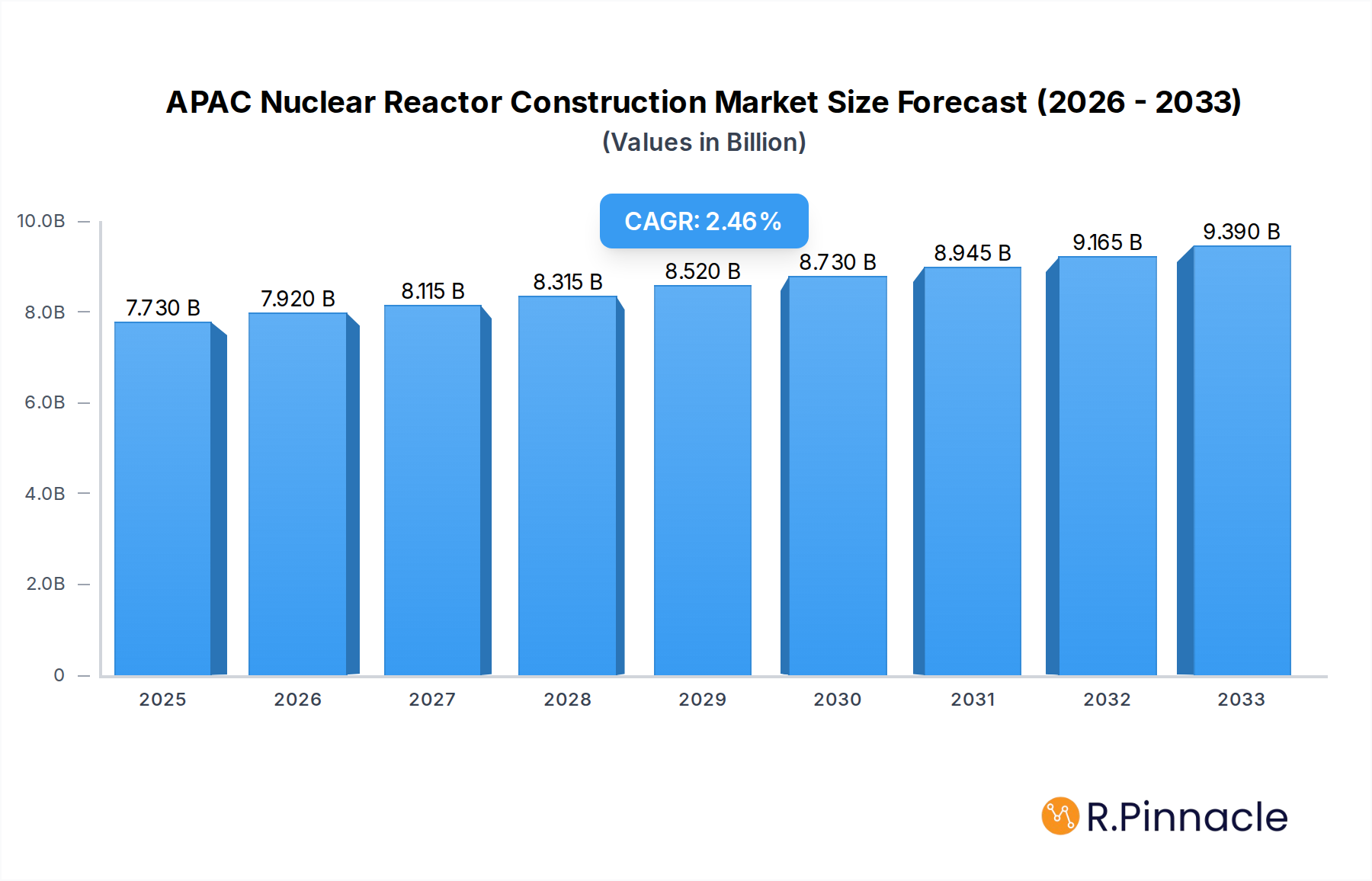

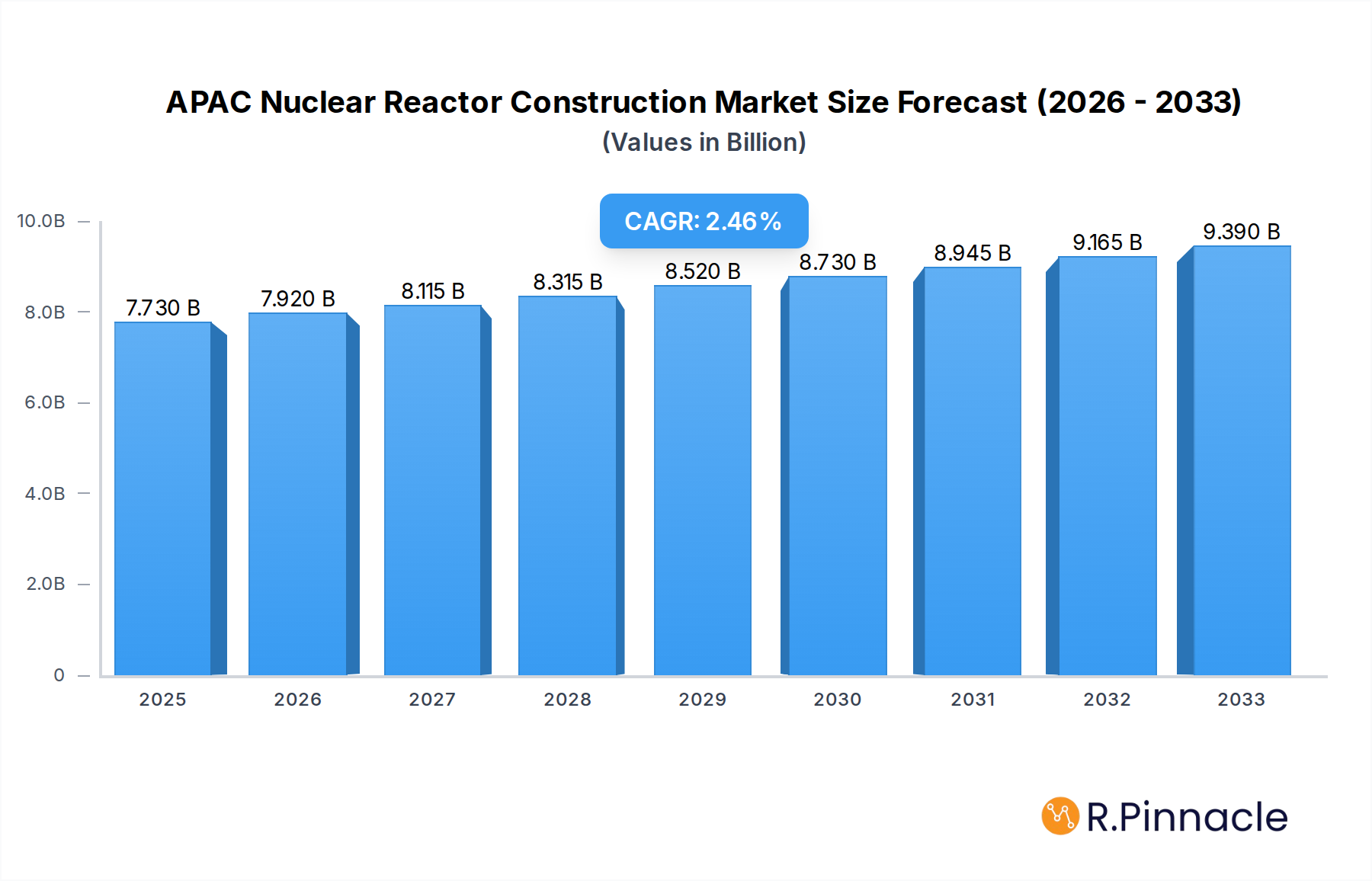

The APAC Nuclear Reactor Construction Market is poised for significant expansion, estimated to reach $7.73 billion in 2025. Driven by an increasing demand for clean and reliable energy sources, coupled with supportive government policies aimed at bolstering nuclear power capacity, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 2.47% from 2019 to 2033. This growth is underpinned by a strategic shift towards diversifying energy portfolios and reducing carbon emissions across the region. Key factors fueling this expansion include substantial investments in infrastructure, technological advancements in reactor designs such as Pressurized Water Reactors (PWRs) and Boiling Water Reactors (BWRs), and the ongoing development of advanced reactor types like High-temperature Gas Cooled Reactors (HTGRs). The Asia-Pacific region, particularly China and India, is at the forefront of this nuclear renaissance, owing to their escalating energy needs and ambitious nuclear power development plans.

APAC Nuclear Reactor Construction Market Market Size (In Billion)

The market's trajectory is further shaped by a dynamic interplay of drivers and restraints. While the growing need for baseload power, energy security concerns, and the declining cost competitiveness of fossil fuels act as primary drivers, regulatory hurdles, public perception regarding nuclear safety, and the management of nuclear waste present significant challenges. Despite these restraints, the strong emphasis on sustainable development and the pursuit of energy independence are expected to propel the market forward. Leading players like China National Nuclear Corporation, Dongfang Electric Corporation, and Larsen & Toubro are actively involved in expanding their footprint through strategic partnerships and the development of advanced reactor technologies. The market segments, encompassing various reactor types and service offerings like equipment and installation, are expected to witness robust growth, reflecting the diverse energy strategies being adopted across the Asia-Pacific landscape.

APAC Nuclear Reactor Construction Market Company Market Share

APAC Nuclear Reactor Construction Market: A Comprehensive Analysis (2019-2033)

This in-depth report provides a granular analysis of the APAC Nuclear Reactor Construction Market, offering critical insights for stakeholders navigating this rapidly evolving sector. We explore market dynamics, competitive landscapes, and future trajectories, driven by robust demand for clean and reliable energy solutions. The study encompasses a comprehensive historical overview, current market assessment, and a detailed forecast period, making it an indispensable resource for industry professionals, investors, and policymakers. The market is poised for significant expansion, fueled by national energy security agendas, decarbonization efforts, and technological advancements in reactor design. The total market value is projected to reach $XXX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period (2025-2033).

APAC Nuclear Reactor Construction Market Market Structure & Innovation Trends

The APAC Nuclear Reactor Construction Market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, alongside a growing number of specialized engineering and construction firms. Innovation is primarily driven by advancements in reactor safety features, operational efficiency, and modular construction techniques. Regulatory frameworks are a crucial determinant, with stringent safety standards and licensing procedures shaping project timelines and costs. The development of Small Modular Reactors (SMRs) represents a key innovation trend, promising faster deployment and reduced upfront investment. Product substitutes, such as renewable energy sources, are increasingly competitive, necessitating continuous technological evolution and cost optimization within the nuclear sector. End-user demographics are evolving, with a growing demand for reliable baseload power from emerging economies and established industrial sectors. Merger and acquisition (M&A) activities are anticipated to increase as companies seek to consolidate expertise, expand geographical reach, and secure crucial supply chain access. Key M&A deal values are estimated to be in the range of $XX billion to $XXX billion over the forecast period.

- Market Concentration: Dominated by a few large multinational corporations, with a growing presence of regional players.

- Innovation Drivers: Enhanced safety protocols, increased efficiency, SMR development, advanced fuel cycles.

- Regulatory Frameworks: Strict adherence to international atomic energy agency standards and national nuclear safety regulations.

- Product Substitutes: Growing competition from solar, wind, and energy storage solutions.

- End-User Demographics: Industrial manufacturers, utility companies, government entities prioritizing energy security and decarbonization.

- M&A Activities: Strategic consolidations to leverage technological expertise and market access, with estimated deal values ranging from $XX billion to $XXX billion.

APAC Nuclear Reactor Construction Market Market Dynamics & Trends

The APAC Nuclear Reactor Construction Market is experiencing a robust growth trajectory, propelled by a confluence of compelling market dynamics and evolving trends. A primary growth driver is the escalating demand for clean and reliable baseload power to meet the burgeoning energy needs of a rapidly industrializing and urbanizing Asia-Pacific region. National energy security imperatives, coupled with ambitious decarbonization targets set by governments, are significantly bolstering investments in nuclear power generation. Technological advancements are playing a pivotal role, with a continuous push towards developing safer, more efficient, and cost-effective reactor designs. The emergence and maturation of Small Modular Reactor (SMR) technology, promising faster deployment, scalability, and enhanced safety features, are revolutionizing the construction landscape. Furthermore, significant investments in research and development by key industry players are leading to innovations in fuel enrichment, waste management, and advanced reactor concepts, such as High-temperature Gas Cooled Reactors (HTGRs).

Consumer preferences, while still evolving in the nuclear sector, are increasingly influenced by the global push for sustainability and the need for stable energy grids capable of supporting the integration of intermittent renewable sources. Utilities and governments are prioritizing energy sources that offer predictability and low carbon emissions, positioning nuclear power as a critical component of a diversified energy portfolio. Competitive dynamics within the market are characterized by intense competition among established global leaders and increasingly capable regional manufacturers. Strategic partnerships, joint ventures, and technology licensing agreements are becoming common strategies to gain a competitive edge, share risks, and access new markets. The ongoing development of indigenous nuclear capabilities in countries like China and India is reshaping the competitive landscape, fostering greater self-reliance and driving down construction costs.

The market penetration of nuclear power is set to increase significantly across the APAC region, driven by supportive government policies, favorable economics for large-scale projects, and a growing public acceptance of nuclear energy as a vital solution for a sustainable future. The market is projected to witness a CAGR of XX.X% during the forecast period (2025-2033). The estimated market size in the base year 2025 is $XXX billion, projected to grow to $XXX billion by 2033. This expansion is underpinned by substantial ongoing and planned projects across the region, reflecting a strong commitment to nuclear energy as a cornerstone of future power generation.

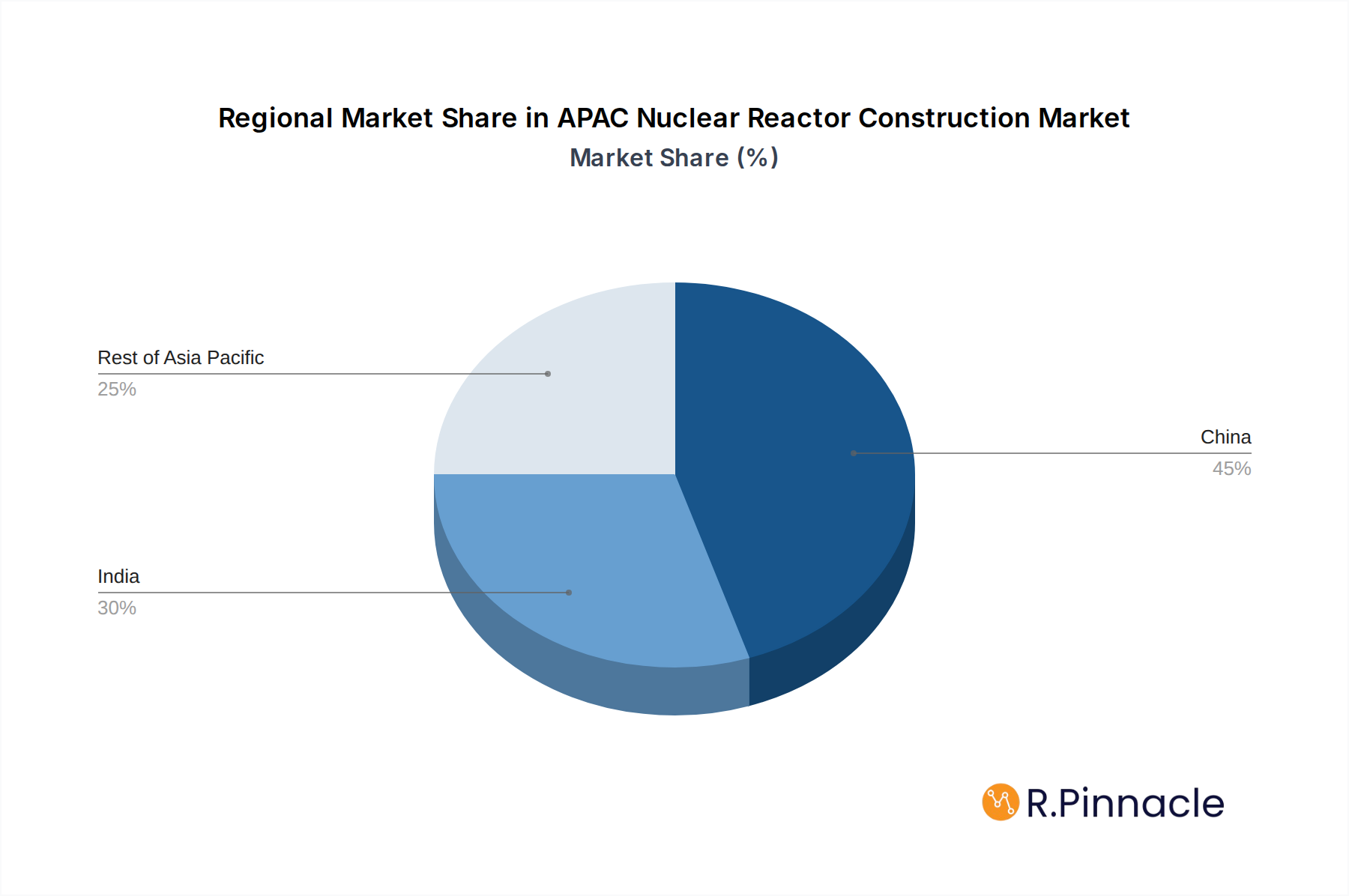

Dominant Regions & Segments in APAC Nuclear Reactor Construction Market

The APAC Nuclear Reactor Construction Market is characterized by distinct regional dominance and segment preferences, driven by a complex interplay of economic policies, infrastructure development, and national energy strategies.

China: The Unrivaled Leader

China stands as the undisputed dominant region in the APAC Nuclear Reactor Construction Market. This leadership is underpinned by several key drivers:

- Aggressive Energy Transition Policies: China has set ambitious targets for carbon emission reduction and aims to significantly increase its nuclear power capacity to complement its vast renewable energy installations and phase out coal.

- Massive Domestic Demand: The country's enormous population and rapidly growing industrial base create an insatiable demand for reliable and consistent baseload power, which nuclear energy is ideally positioned to provide.

- Government Support and Investment: The Chinese government has made substantial financial commitments and provided unwavering policy support for the development and expansion of its domestic nuclear industry. This includes funding for research, development, and construction of new plants.

- Indigenous Technological Advancement: Companies like China National Nuclear Corporation (CNNC) and Dongfang Electric Corporation Limited have made significant strides in developing their own reactor technologies (e.g., Hualong One) and have built extensive manufacturing and construction capabilities, reducing reliance on foreign expertise and technology.

- Large-Scale Project Execution: China possesses the experience and capacity to undertake and execute multiple large-scale nuclear reactor construction projects simultaneously, significantly contributing to its market dominance.

The dominance of China translates into substantial market share in the overall APAC nuclear reactor construction value, estimated to account for over XX% of the total market during the forecast period. The country is a primary hub for the construction of Pressurized Water Reactors (PWRs), which are the most common type globally and well-suited for large-scale power generation. However, there is also a growing interest and investment in advanced reactor types, reflecting China's commitment to nuclear innovation.

India: The Ascending Powerhouse

India is rapidly emerging as a key player and a significant growth engine within the APAC Nuclear Reactor Construction Market. Its ascendancy is driven by:

- Energy Security and Diversification: India relies heavily on imported fossil fuels. Nuclear power is seen as a crucial element for enhancing energy security, reducing import dependence, and diversifying its energy mix.

- Growing Energy Demand: Similar to China, India's large and growing population, coupled with economic development, is driving a substantial increase in energy demand.

- Supportive Government Initiatives: The Indian government, through the Department of Atomic Energy and the Nuclear Power Corporation of India Limited (NPCIL), has a clear roadmap for expanding nuclear power capacity.

- Focus on Pressurized Heavy Water Reactors (PHWRs): India has developed strong expertise and indigenous capabilities in Pressurized Heavy Water Reactors (PHWRs), utilizing its abundant thorium reserves for future fuel cycles. This specialized focus makes PHWRs a dominant reactor type in India's nuclear program.

- International Collaborations: India is actively pursuing collaborations with international nuclear power providers and technology suppliers, fostering technology transfer and accelerating project development.

The market share of India is projected to grow steadily, contributing significantly to the overall APAC market expansion, particularly in the PHWR segment.

Rest of Asia-Pacific: Emerging Markets and Niche Players

The Rest of Asia-Pacific region, encompassing countries like South Korea, Japan, and emerging markets such as Vietnam, Indonesia, and Thailand, presents a more diverse and dynamic landscape.

- South Korea: A highly developed nuclear power sector with advanced technological capabilities, primarily focused on Pressurized Water Reactors (PWRs). Companies like KEPCO Engineering & Construction are key players.

- Japan: Despite the Fukushima incident, Japan maintains significant nuclear infrastructure and is gradually revisiting its nuclear energy strategy, with a focus on safety and advanced reactor technologies.

- Emerging Markets: Countries like Vietnam and Indonesia are exploring nuclear power for their future energy needs, often looking towards international partnerships and proven reactor technologies, primarily Pressurized Water Reactors (PWRs).

- Specialized Reactor Types: While PWRs and PHWRs dominate, there is growing interest in High-temperature Gas Cooled Reactors (HTGRs) for industrial applications and potentially for power generation in certain advanced economies within this region.

The segments of Equipment and Installation are paramount across all regions, with Pressurized Water Reactors (PWRs) being the most frequently constructed type due to their established track record and widespread adoption. However, the strategic importance of Pressurized Heavy Water Reactors (PHWRs) in India and the potential for High-temperature Gas Cooled Reactors (HTGRs) and Liquid Metal Fast Breeder Reactors (LMFBRs) in specific research and development contexts cannot be overlooked. The market for Boiling Water Reactors (BWRs), while less prevalent than PWRs, still holds a presence in certain established nuclear programs.

APAC Nuclear Reactor Construction Market Product Innovations

Product innovations in the APAC Nuclear Reactor Construction Market are central to enhancing safety, efficiency, and economic viability. A key trend is the development and deployment of Small Modular Reactors (SMRs), offering faster construction times, reduced upfront capital, and improved scalability for diverse power needs. Advanced reactor designs are focusing on passive safety systems, inherent stability, and enhanced fuel utilization to minimize waste. Companies are also innovating in construction methodologies, embracing modular fabrication and digital twin technologies to streamline project execution and reduce costs. These advancements aim to improve the competitive positioning of nuclear energy against other power sources and address public concerns regarding safety and environmental impact.

Report Scope & Segmentation Analysis

This report meticulously segments the APAC Nuclear Reactor Construction Market across critical dimensions, providing a comprehensive understanding of its intricate structure and growth potential.

- Service Segmentation: The market is analyzed based on key services including Equipment (procurement and manufacturing of nuclear components) and Installation (construction, assembly, and commissioning of nuclear power plants).

- Reactor Type Segmentation: Detailed analysis is provided for various reactor types, including the widely adopted Pressurized Water Reactor (PWR), India's focus on Pressurized Heavy Water Reactor (PHWR), the established Boiling Water Reactor (BWR), emerging High-temperature Gas Cooled Reactor (HTGR), and advanced Liquid Metal Fast Breeder Reactor (LMFBR).

- Geographical Segmentation: The market is broken down into three key geographical areas: the dominant market of China, the rapidly growing market of India, and the collective Rest of Asia-Pacific, which includes key nuclear nations and emerging markets.

Each segment is evaluated for its current market size, projected growth rates, and the competitive dynamics shaping its evolution.

Key Drivers of APAC Nuclear Reactor Construction Market Growth

The APAC Nuclear Reactor Construction Market is propelled by several interconnected drivers:

- Energy Security Imperatives: Nations are prioritizing stable and indigenous energy sources to reduce reliance on volatile global fuel markets.

- Decarbonization Goals: Ambitious climate targets are driving the adoption of low-carbon energy solutions, with nuclear power offering reliable baseload generation.

- Growing Energy Demand: Rapid industrialization, urbanization, and population growth in the APAC region necessitate significant expansion of power generation capacity.

- Technological Advancements: Innovations in reactor design, safety features, and construction methodologies are making nuclear power more efficient, safer, and economically attractive.

- Government Support and Policy Frameworks: Favorable government policies, including subsidies, streamlined regulatory processes, and long-term energy planning, are crucial enablers of nuclear projects.

Challenges in the APAC Nuclear Reactor Construction Market Sector

Despite its growth potential, the APAC Nuclear Reactor Construction Market faces significant challenges:

- Stringent Regulatory Hurdles: Obtaining necessary permits and approvals from regulatory bodies can be a lengthy and complex process, leading to project delays and cost overruns.

- High Upfront Capital Costs: The substantial initial investment required for nuclear power plant construction remains a significant barrier, particularly for emerging economies.

- Public Perception and Acceptance: Concerns regarding nuclear safety, waste disposal, and security can lead to public opposition, impacting project timelines and government support.

- Supply Chain Vulnerabilities: The specialized nature of nuclear components and materials can lead to supply chain disruptions and price volatility.

- Competition from Renewable Energy: The decreasing costs of solar and wind power, coupled with advancements in energy storage, present a growing competitive challenge to nuclear energy.

Emerging Opportunities in APAC Nuclear Reactor Construction Market

The APAC Nuclear Reactor Construction Market is ripe with emerging opportunities:

- Small Modular Reactors (SMRs): The development and deployment of SMRs offer a more flexible and accessible pathway to nuclear power, particularly for smaller grids and industrial applications.

- Advanced Reactor Designs: Innovations in HTGRs and LMFBRs present opportunities for enhanced efficiency, inherent safety, and potentially novel applications like hydrogen production.

- Life Extension of Existing Plants: Many aging nuclear power plants in the region are candidates for life extension projects, offering significant refurbishment and upgrade opportunities.

- Digitalization and Automation: The adoption of digital technologies, artificial intelligence, and automation in construction and operation can improve efficiency, reduce costs, and enhance safety.

- Green Hydrogen Production: Nuclear power's ability to provide stable, carbon-free electricity makes it an ideal partner for the burgeoning green hydrogen industry.

Leading Players in the APAC Nuclear Reactor Construction Market Market

- Dongfang Electric Corporation Limited

- Larsen & Toubro Limited

- Doosan Heavy Industries & Construction Co Ltd

- Bilfinger SE

- China National Nuclear Corporation

- Electricite de France SA (EDF)

- KEPCO Engineering & Construction

- Westinghouse Electric Company LLC (Toshiba)

- Shanghai Electric Group Company Limited

- Rosatom State Nuclear Energy Corporation

- Mitsubishi Heavy Industries Ltd

- GE-Hitachi Nuclear Energy Inc

Key Developments in APAC Nuclear Reactor Construction Market Industry

- 2023/Q4: China announces plans to expedite the construction of new nuclear power plants, aiming to increase its installed nuclear capacity significantly by 2030.

- 2023/Q3: India commissions its largest indigenously built Pressurized Heavy Water Reactor (PHWR), showcasing its growing domestic capabilities.

- 2023/Q2: South Korea and the UAE sign a memorandum of understanding for cooperation in nuclear energy, including potential export opportunities for Korean reactor technology.

- 2023/Q1: GE-Hitachi Nuclear Energy announces advancements in its SMR design, focusing on enhanced safety features and modular construction.

- 2022/Q4: Rosatom State Nuclear Energy Corporation successfully completes the construction of a new reactor unit in an APAC nation, highlighting its global project execution capacity.

- 2022/Q3: Bilfinger SE secures a significant contract for the maintenance and refurbishment of several nuclear power facilities in the Asia-Pacific region.

- 2022/Q2: Mitsubishi Heavy Industries Ltd unveils its latest advancements in High-temperature Gas Cooled Reactor (HTGR) technology, emphasizing its potential for industrial heat applications.

- 2022/Q1: Larsen & Toubro Limited expands its nuclear fabrication capabilities to meet the growing demand for critical nuclear components in India and neighboring countries.

- 2021/Q4: Westinghouse Electric Company LLC (Toshiba) and its partners secure a key contract for the supply of fuel for a prominent nuclear power plant in the APAC region.

- 2021/Q3: Electricite de France SA (EDF) engages in strategic partnerships to explore opportunities for developing advanced nuclear technologies in emerging APAC markets.

Future Outlook for APAC Nuclear Reactor Construction Market Market

The future outlook for the APAC Nuclear Reactor Construction Market is exceptionally positive, driven by a confluence of factors that position nuclear power as a critical component of the region's energy future. The escalating demand for clean, reliable, and baseload electricity, coupled with ambitious climate action goals, will continue to fuel significant investment in new nuclear projects. The maturation and increasing acceptance of Small Modular Reactor (SMR) technology present a transformative opportunity, enabling faster deployment, enhanced flexibility, and broader market penetration. Furthermore, ongoing advancements in reactor safety, efficiency, and fuel cycle management will further solidify nuclear energy's competitive standing. Strategic government policies, robust technological innovation, and growing international collaborations will collectively accelerate market growth, paving the way for a substantial expansion of nuclear power capacity across the Asia-Pacific region.

APAC Nuclear Reactor Construction Market Segmentation

-

1. Service

- 1.1. Equipment

- 1.2. Installation

-

2. Reactor Type

- 2.1. Pressurized Water Reactor

- 2.2. Pressurized Heavy Water Reactor

- 2.3. Boiling Water Reactor

- 2.4. High-temperature Gas Cooled Reactor

- 2.5. Liquid Metal Fast Breeder Reactor

-

3. Geography

- 3.1. China

- 3.2. India

- 3.3. Rest of Asia-Pacific

APAC Nuclear Reactor Construction Market Segmentation By Geography

- 1. China

- 2. India

- 3. Rest of Asia Pacific

APAC Nuclear Reactor Construction Market Regional Market Share

Geographic Coverage of APAC Nuclear Reactor Construction Market

APAC Nuclear Reactor Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Equipment

- 5.1.2. Installation

- 5.2. Market Analysis, Insights and Forecast - by Reactor Type

- 5.2.1. Pressurized Water Reactor

- 5.2.2. Pressurized Heavy Water Reactor

- 5.2.3. Boiling Water Reactor

- 5.2.4. High-temperature Gas Cooled Reactor

- 5.2.5. Liquid Metal Fast Breeder Reactor

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Global APAC Nuclear Reactor Construction Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Equipment

- 6.1.2. Installation

- 6.2. Market Analysis, Insights and Forecast - by Reactor Type

- 6.2.1. Pressurized Water Reactor

- 6.2.2. Pressurized Heavy Water Reactor

- 6.2.3. Boiling Water Reactor

- 6.2.4. High-temperature Gas Cooled Reactor

- 6.2.5. Liquid Metal Fast Breeder Reactor

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. India

- 6.3.3. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. China APAC Nuclear Reactor Construction Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service

- 7.1.1. Equipment

- 7.1.2. Installation

- 7.2. Market Analysis, Insights and Forecast - by Reactor Type

- 7.2.1. Pressurized Water Reactor

- 7.2.2. Pressurized Heavy Water Reactor

- 7.2.3. Boiling Water Reactor

- 7.2.4. High-temperature Gas Cooled Reactor

- 7.2.5. Liquid Metal Fast Breeder Reactor

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. India

- 7.3.3. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Service

- 8. India APAC Nuclear Reactor Construction Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service

- 8.1.1. Equipment

- 8.1.2. Installation

- 8.2. Market Analysis, Insights and Forecast - by Reactor Type

- 8.2.1. Pressurized Water Reactor

- 8.2.2. Pressurized Heavy Water Reactor

- 8.2.3. Boiling Water Reactor

- 8.2.4. High-temperature Gas Cooled Reactor

- 8.2.5. Liquid Metal Fast Breeder Reactor

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. India

- 8.3.3. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Service

- 9. Rest of Asia Pacific APAC Nuclear Reactor Construction Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service

- 9.1.1. Equipment

- 9.1.2. Installation

- 9.2. Market Analysis, Insights and Forecast - by Reactor Type

- 9.2.1. Pressurized Water Reactor

- 9.2.2. Pressurized Heavy Water Reactor

- 9.2.3. Boiling Water Reactor

- 9.2.4. High-temperature Gas Cooled Reactor

- 9.2.5. Liquid Metal Fast Breeder Reactor

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. India

- 9.3.3. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Service

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Dongfang Electric Corporation Limited

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Larsen & Toubro Limited

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Doosan Heavy Industries & Construction Co Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Bilfinger SE

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 China National Nuclear Corporation

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Electricite de France SA (EDF)

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 KEPCO Engineering & Construction

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Westinghouse Electric Company LLC (Toshiba)

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Shanghai Electric Group Company Limited

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Rosatom State Nuclear Energy Corporation

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Mitsubishi Heavy Industries Ltd

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 GE-Hitachi Nuclear Energy Inc

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.1 Dongfang Electric Corporation Limited

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global APAC Nuclear Reactor Construction Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: China APAC Nuclear Reactor Construction Market Revenue (billion), by Service 2025 & 2033

- Figure 3: China APAC Nuclear Reactor Construction Market Revenue Share (%), by Service 2025 & 2033

- Figure 4: China APAC Nuclear Reactor Construction Market Revenue (billion), by Reactor Type 2025 & 2033

- Figure 5: China APAC Nuclear Reactor Construction Market Revenue Share (%), by Reactor Type 2025 & 2033

- Figure 6: China APAC Nuclear Reactor Construction Market Revenue (billion), by Geography 2025 & 2033

- Figure 7: China APAC Nuclear Reactor Construction Market Revenue Share (%), by Geography 2025 & 2033

- Figure 8: China APAC Nuclear Reactor Construction Market Revenue (billion), by Country 2025 & 2033

- Figure 9: China APAC Nuclear Reactor Construction Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: India APAC Nuclear Reactor Construction Market Revenue (billion), by Service 2025 & 2033

- Figure 11: India APAC Nuclear Reactor Construction Market Revenue Share (%), by Service 2025 & 2033

- Figure 12: India APAC Nuclear Reactor Construction Market Revenue (billion), by Reactor Type 2025 & 2033

- Figure 13: India APAC Nuclear Reactor Construction Market Revenue Share (%), by Reactor Type 2025 & 2033

- Figure 14: India APAC Nuclear Reactor Construction Market Revenue (billion), by Geography 2025 & 2033

- Figure 15: India APAC Nuclear Reactor Construction Market Revenue Share (%), by Geography 2025 & 2033

- Figure 16: India APAC Nuclear Reactor Construction Market Revenue (billion), by Country 2025 & 2033

- Figure 17: India APAC Nuclear Reactor Construction Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue (billion), by Service 2025 & 2033

- Figure 19: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue Share (%), by Service 2025 & 2033

- Figure 20: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue (billion), by Reactor Type 2025 & 2033

- Figure 21: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue Share (%), by Reactor Type 2025 & 2033

- Figure 22: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue (billion), by Geography 2025 & 2033

- Figure 23: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of Asia Pacific APAC Nuclear Reactor Construction Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 2: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 3: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 6: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 7: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 10: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 11: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 14: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 15: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Global APAC Nuclear Reactor Construction Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Nuclear Reactor Construction Market?

The projected CAGR is approximately 2.47%.

2. Which companies are prominent players in the APAC Nuclear Reactor Construction Market?

Key companies in the market include Dongfang Electric Corporation Limited, Larsen & Toubro Limited, Doosan Heavy Industries & Construction Co Ltd, Bilfinger SE, China National Nuclear Corporation, Electricite de France SA (EDF), KEPCO Engineering & Construction, Westinghouse Electric Company LLC (Toshiba), Shanghai Electric Group Company Limited, Rosatom State Nuclear Energy Corporation, Mitsubishi Heavy Industries Ltd, GE-Hitachi Nuclear Energy Inc.

3. What are the main segments of the APAC Nuclear Reactor Construction Market?

The market segments include Service, Reactor Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.73 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Demand for Renewable Energy4.; Upcoming Investments in the Energy Sector and Supportive Renewable Energy Policies.

6. What are the notable trends driving market growth?

Pressurized Water Reactor to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Initial Investment Cost and Long Investment Return Period on Projects.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Nuclear Reactor Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Nuclear Reactor Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Nuclear Reactor Construction Market?

To stay informed about further developments, trends, and reports in the APAC Nuclear Reactor Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence