Key Insights

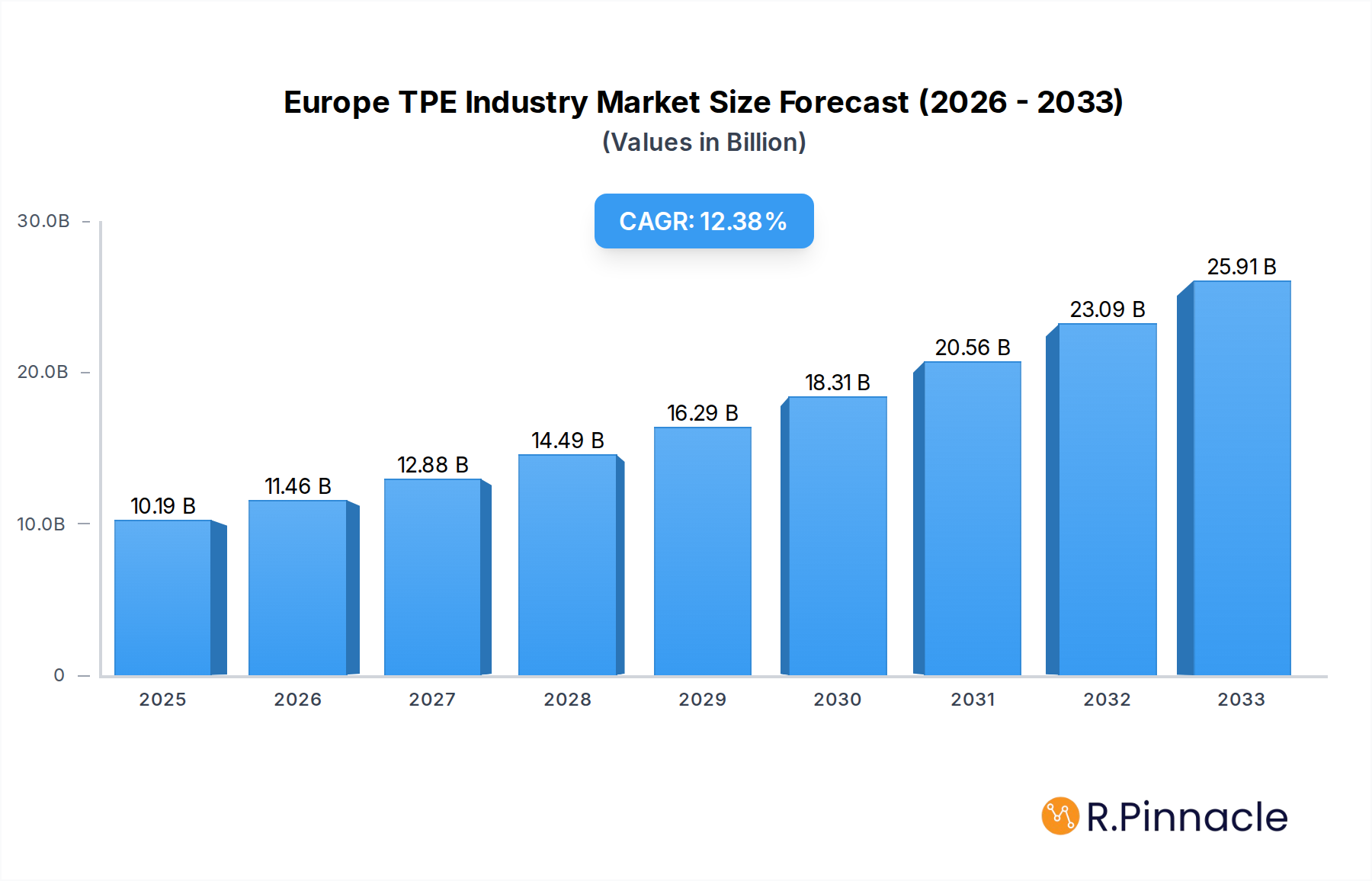

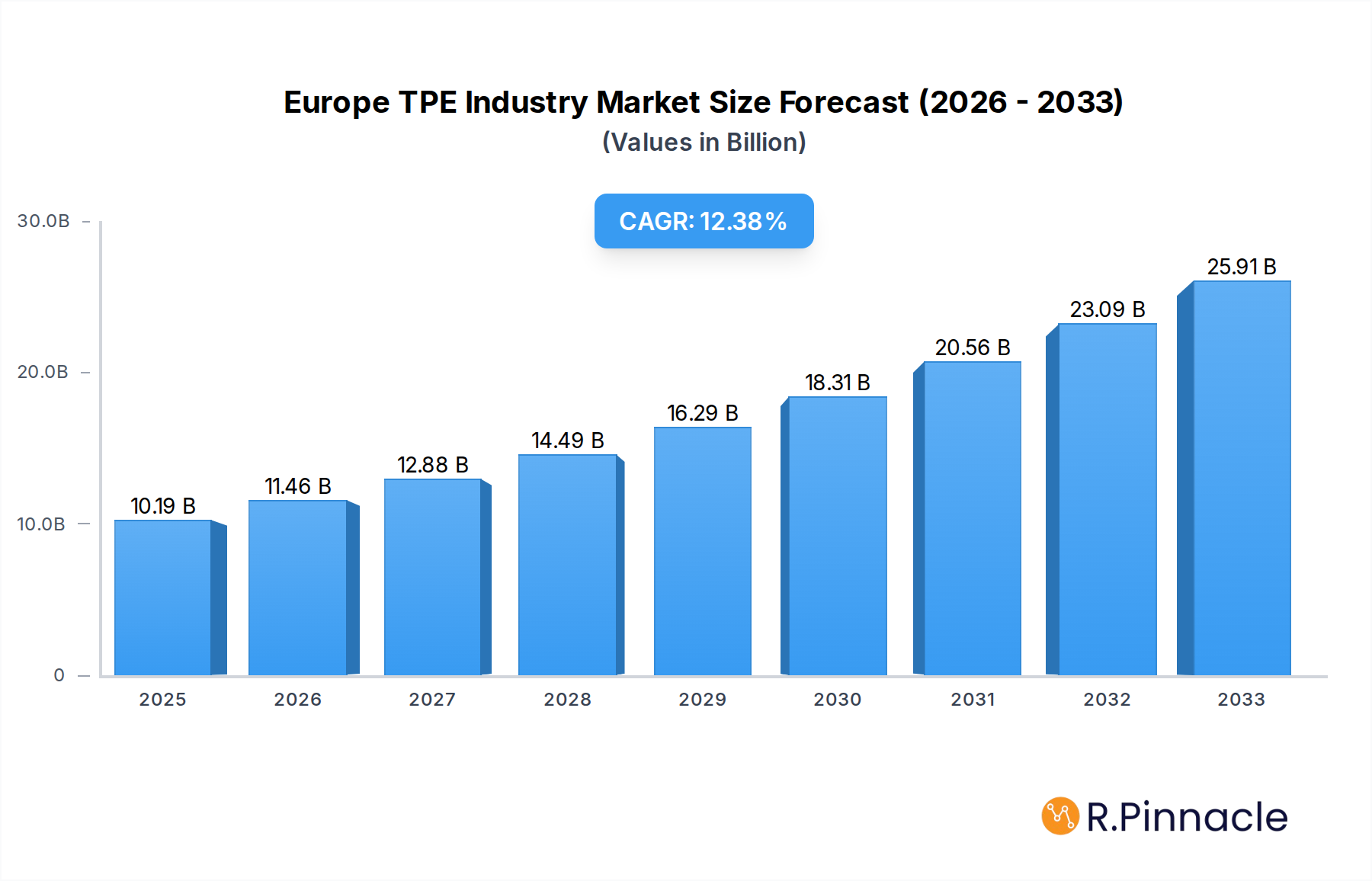

The European Thermoplastic Elastomer (TPE) market is poised for significant expansion, driven by robust demand across diverse end-use industries. With a current market size estimated at USD 10.19 billion in 2025, the industry is projected to witness a remarkable compound annual growth rate (CAGR) of 12.42%, reaching substantial value by 2033. This dynamic growth is fueled by the inherent versatility and performance benefits of TPEs, which offer a unique blend of rubber-like elasticity and thermoplastic processability. Key drivers include the increasing adoption of TPEs in the automotive sector for lightweighting and interior components, the burgeoning construction industry for sealants and gaskets, and the medical field for its biocompatibility and flexibility. Furthermore, the growing consumer demand for sustainable and recyclable materials is propelling the use of TPEs as a viable alternative to traditional materials.

Europe TPE Industry Market Size (In Billion)

The European TPE landscape is characterized by a diverse product segmentation, with Styrenic Block Copolymer (TPE-S) and Thermoplastic Olefin (TPE-O) holding significant market shares due to their widespread applications. However, niche segments like Thermoplastic Polyurethane (TPU) and Elastomeric Alloys (TPE-V or TPV) are exhibiting particularly strong growth trajectories, driven by their specialized performance attributes. The market also faces certain restraints, including price volatility of raw materials and the need for continuous innovation to meet evolving regulatory standards. Despite these challenges, the overarching trend towards advanced material solutions, coupled with supportive government initiatives promoting sustainable manufacturing, indicates a highly promising future for the European TPE industry, with key players like Arkema, BASF SE, and DuPont spearheading innovation and market penetration.

Europe TPE Industry Company Market Share

Europe TPE Industry Report: Market Analysis, Trends, and Forecasts (2019-2033)

This comprehensive report delves into the dynamic Europe TPE (Thermoplastic Elastomer) industry, providing an in-depth analysis of market structure, dynamics, key segments, and future outlook. Leveraging high-ranking keywords such as "Europe TPE market," "thermoplastic elastomers Europe," "TPE applications," and "TPE market trends," this report is designed to equip industry professionals, investors, and stakeholders with actionable insights for strategic decision-making. Our study covers the period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, offering robust data for informed planning. The European market for TPEs is projected to reach substantial billion-dollar valuations, driven by innovation and diverse application demands.

Europe TPE Industry Market Structure & Innovation Trends

The European TPE market exhibits a moderately concentrated structure, characterized by the presence of major global players and a growing number of specialized manufacturers. Innovation is a key driver, with companies continuously investing in R&D to develop advanced TPE formulations that meet stringent performance requirements and evolving sustainability mandates. Regulatory frameworks, particularly those concerning environmental impact and material safety, are shaping product development and market access. Product substitutes, such as traditional rubbers and thermoset plastics, pose a competitive challenge, but the inherent advantages of TPEs – recyclability, ease of processing, and a broad performance spectrum – are expanding their adoption. End-user demographics are shifting towards sectors demanding high-performance, lightweight, and eco-friendly materials. Merger and acquisition (M&A) activities, with estimated deal values in the hundreds of billions of Euros, are actively consolidating the market and fostering technological advancements. Key M&A trends indicate a strategic focus on expanding product portfolios, enhancing geographic reach, and securing access to novel TPE technologies.

Europe TPE Industry Market Dynamics & Trends

The Europe TPE industry is experiencing robust growth, fueled by a confluence of powerful market drivers and transformative trends. A primary growth catalyst is the escalating demand from the automotive sector, where lightweight TPEs are crucial for fuel efficiency and emissions reduction. The increasing adoption of electric vehicles (EVs) further amplifies this demand, as TPEs are utilized in battery components, charging infrastructure, and interior fittings. Technological disruptions are continuously reshaping the market, with advancements in polymerization techniques and compounding leading to the development of TPEs with enhanced properties like improved temperature resistance, chemical inertness, and superior tactile feel. Consumer preferences are increasingly aligned with sustainability, driving the demand for bio-based and recycled TPE materials. This trend is supported by stringent EU environmental regulations and a growing consumer awareness of the ecological footprint of products. The competitive dynamics are characterized by intense innovation, strategic partnerships, and a focus on value-added solutions. Market penetration of TPEs is steadily increasing across various applications, replacing traditional materials due to their cost-effectiveness and performance benefits. The compound annual growth rate (CAGR) for the Europe TPE market is robust, projected to be in the high single digits over the forecast period, signaling significant expansion. This growth is underpinned by continuous product development and an expanding application base, making the Europe TPE market a compelling landscape for investment and innovation.

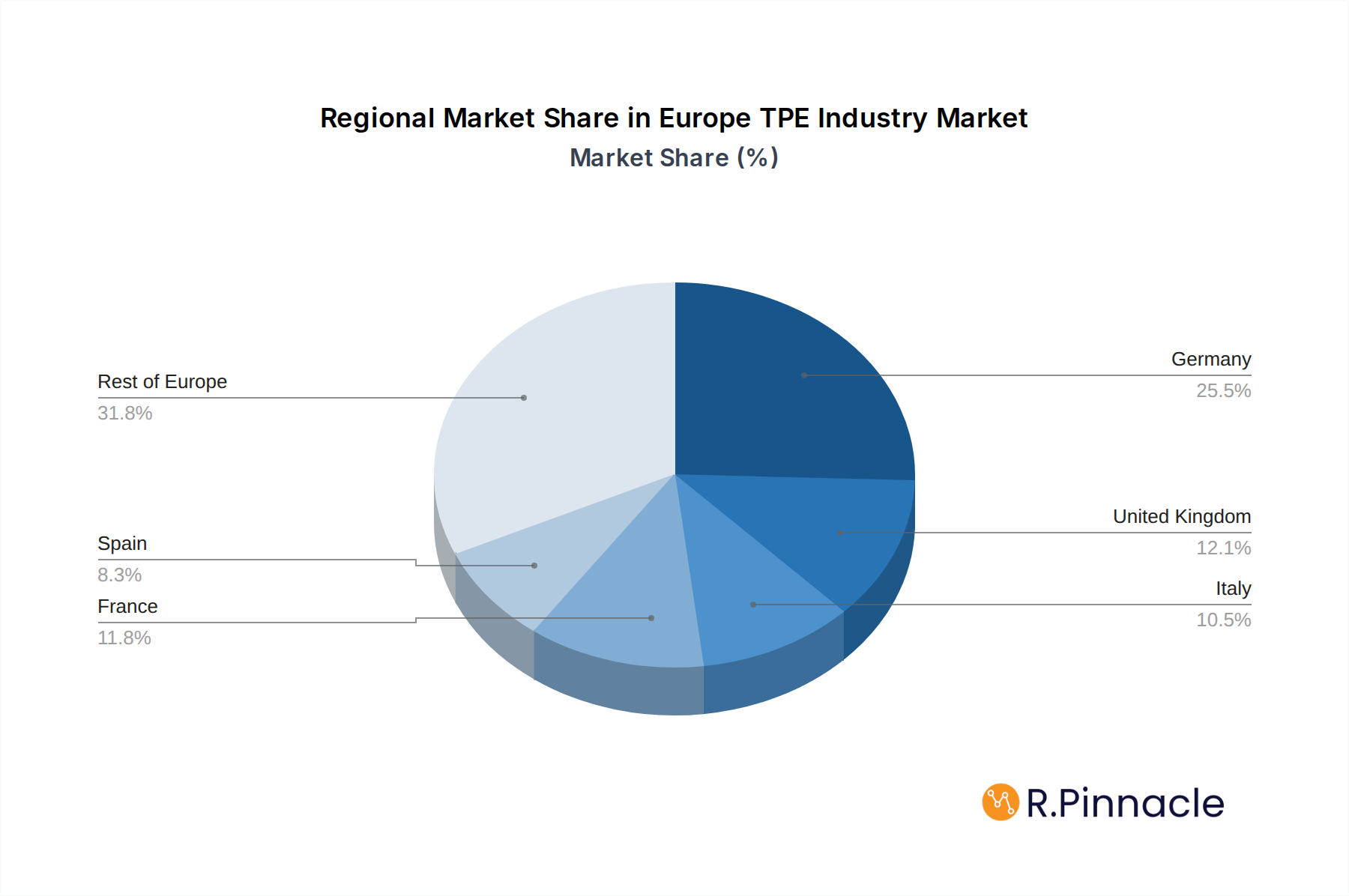

Dominant Regions & Segments in Europe TPE Industry

The Automotive and Transportation segment remains a dominant force within the European TPE industry. Key drivers for this segment's dominance include stringent EU regulations on vehicle emissions, driving the demand for lightweight materials to improve fuel efficiency, and the rapid expansion of the electric vehicle market which requires specialized TPEs for battery components, charging cables, and interior applications. Economic policies that promote manufacturing and infrastructure development also play a crucial role.

Germany stands out as a leading country within the Europe TPE market. Its strong automotive manufacturing base, coupled with a highly industrialized economy and a commitment to innovation and sustainability, makes it a critical hub for TPE consumption and production. Significant investment in research and development by major chemical companies headquartered or with a strong presence in Germany further solidifies its leadership.

In terms of Product Type, Styrenic Block Copolymer (TPE-S) currently holds a significant market share. This is attributed to its versatility, cost-effectiveness, and widespread use in applications ranging from consumer goods to automotive components and medical devices. Its balance of rubber-like elasticity and thermoplastic processability makes it an attractive material for a broad array of end-users.

Conversely, Thermoplastic Polyurethane (TPU) is a rapidly growing segment, driven by its exceptional abrasion resistance, high tensile strength, and flexibility. Its dominance is particularly evident in high-performance applications within the automotive, footwear, and industrial sectors, where durability and resilience are paramount.

The Medical application segment is experiencing exceptional growth, propelled by an aging population, increasing healthcare expenditure, and the demand for advanced medical devices and biocompatible materials. Strict regulatory approvals and the need for sterile, high-purity materials are driving innovation and investment in specialized TPEs for this sector.

Europe TPE Industry Product Innovations

Recent product innovations in the Europe TPE industry focus on enhancing performance, sustainability, and application specificity. Manufacturers are developing TPEs with improved temperature resistance, chemical inertness, and UV stability to meet demanding industrial and automotive requirements. A significant trend is the development of bio-based and recycled TPEs, aligning with market demands for sustainable materials. These innovations offer competitive advantages by reducing environmental impact and enabling companies to meet corporate sustainability goals. The market fit for these new TPE grades is strong, particularly in sectors prioritizing eco-friendly solutions and high-performance attributes.

Report Scope & Segmentation Analysis

This report comprehensively segments the Europe TPE industry across key product types and applications.

Product Types:

- Styrenic Block Copolymer (TPE-S): Expected to maintain a significant market share due to its broad applicability and cost-effectiveness, with steady growth projected.

- Thermoplastic Olefin (TPE-O): Anticipated to witness moderate growth, driven by its use in less demanding applications and as a cost-effective alternative.

- Elastomeric Alloy (TPE-V or TPV): Projected for strong growth, particularly in automotive sealing applications, due to its excellent chemical and heat resistance.

- Thermoplastic Polyurethane (TPU): Forecasted to exhibit robust expansion, driven by its superior mechanical properties in high-performance applications.

- Thermoplastic Copolyester: Expected to see steady growth, especially in applications requiring flexibility and chemical resistance.

- Thermoplastic Polyamide: Anticipated for moderate growth, finding its niche in specialized applications requiring high strength and temperature resistance.

Applications:

- Automotive and Transportation: The largest and fastest-growing segment, driven by lightweighting trends and EV adoption.

- Building and Construction: Steady growth expected, with increasing use in sealing, roofing, and insulation.

- Footwear: Moderate growth, with TPEs offering comfort, durability, and design flexibility.

- Electrical and Electronics: Growing demand for insulation, connectors, and housing components.

- Medical: Significant high-growth potential due to increasing demand for advanced medical devices and biocompatible materials.

- Household Appliances: Consistent demand for durable and aesthetically pleasing components.

- HVAC: Growing application in seals, gaskets, and flexible tubing.

- Adhesives, Sealants, and Coatings: Steady demand for flexible and durable bonding solutions.

- Other Applications: Encompassing diverse niche markets with varied growth rates.

Key Drivers of Europe TPE Industry Growth

The Europe TPE industry's growth is propelled by several interconnected factors. Technologically, advancements in polymerization and compounding techniques are yielding TPEs with enhanced properties and cost efficiencies. Economically, the increasing demand for lightweight materials in automotive for fuel efficiency and emissions reduction, coupled with the burgeoning electric vehicle market, is a significant driver. Furthermore, the rising consumer demand for sustainable and recyclable materials is pushing manufacturers to develop eco-friendly TPE solutions. Regulatory mandates from the EU, encouraging the use of safer and more environmentally responsible materials, also play a crucial role in shaping market growth and directing innovation towards greener alternatives.

Challenges in the Europe TPE Industry Sector

Despite its growth trajectory, the Europe TPE industry faces notable challenges. Regulatory hurdles related to chemical safety and environmental impact, while driving innovation, can also lead to increased compliance costs and longer product development cycles. Supply chain disruptions, including raw material price volatility and availability issues, can impact production efficiency and profitability. Intense competitive pressures from established players and emerging markets necessitate continuous innovation and cost optimization. Furthermore, the established infrastructure and lower costs associated with traditional materials like rubber can present a barrier to widespread TPE adoption in certain price-sensitive applications. The increasing cost of energy in Europe also poses a challenge to energy-intensive TPE manufacturing processes.

Emerging Opportunities in Europe TPE Industry

The Europe TPE industry is poised for significant opportunities driven by evolving market trends and technological advancements. The increasing focus on sustainability is creating a strong demand for bio-based and recycled TPEs, opening new market segments for manufacturers leveraging circular economy principles. The rapidly expanding medical device sector presents substantial opportunities for high-purity, biocompatible TPEs. Furthermore, the ongoing electrification of transportation, including electric vehicles and autonomous driving systems, is generating demand for specialized TPEs with enhanced electrical insulation and thermal management properties. Emerging technologies in additive manufacturing (3D printing) also present opportunities for customized TPE solutions.

Leading Players in the Europe TPE Industry Market

- Grupo Dynasol

- Arkema

- Sumitomo Chemicals Co Ltd

- Mitsui Chemicals Inc

- Asahi Kasei Corporation

- Exxon Mobil Corporation

- KURARAY CO LTD

- Mitsubishi Chemical Corporation

- Evonik Industries AG

- LANXESS

- BASF SE

- Huntsman International LLC

- SABIC

- DSM

- LG Chem

- DuPont

- The Lubrizol Corporation

- KRATON CORPORATION

- Apar Industries Ltd

- Covestro AG

- LyondellBasell Industries Holdings BV

- Sirmax SpA

Key Developments in Europe TPE Industry Industry

- November 2022: HEXPOL TPE officially launched bio-attributed medicinal TPEs, expanding their portfolio of materials that enable a transition away from fossil feedstocks. Mass balancing allows for a progressive increase in bio-circular share utilizing existing infrastructure to reduce fossil resource usage gradually. Because the resulting TPE material is a drop-in solution with equivalent qualities, HEXPOL TPE identified mass balance as a promising alternative for their medical customers. It is because renewable monomers have the same quality and purity as those derived from fossil sources.

- October 2021: DuPont launched Liveo Pharma Bottle Closures - one-piece silicone stoppers and tubings manufactured from biomedical-grade silicone elastomers - a welcome addition to the company's existing over-molded assembly offering for biopharma processing applications. Liveo Pharma Bottle Closures are designed to seal the threaded glass, plastic bottles, and containers used in biopharmaceutical and biotechnology processes for essential fluid transfer, media and buffer pooling and storage, and sample collecting.

Future Outlook for Europe TPE Industry Market

The future outlook for the Europe TPE industry is exceptionally positive, characterized by sustained growth and evolving market dynamics. Key growth accelerators include the continued push for lightweighting and sustainability in the automotive sector, the robust expansion of the medical device industry, and the increasing demand for high-performance materials across various industrial applications. The industry's commitment to innovation, particularly in developing bio-based and recycled TPEs, will further solidify its market position and attract environmentally conscious consumers and businesses. Strategic opportunities lie in expanding into emerging applications, capitalizing on digitalization for enhanced supply chain management, and fostering collaborations to drive material science advancements. The market is projected to reach multi-billion dollar valuations, offering substantial potential for stakeholders investing in this dynamic sector.

Europe TPE Industry Segmentation

-

1. Product Type

- 1.1. Styrenic Block Copolymer (TPE-S)

- 1.2. Thermoplastic Olefin (TPE-O)

- 1.3. Elastomeric Alloy (TPE-V or TPV)

- 1.4. Thermoplastic Polyurethane (TPU)

- 1.5. Thermoplastic Copolyester

- 1.6. Thermoplastic Polyamide

-

2. Application

- 2.1. Automotive and Transportation

- 2.2. Building and Construction

- 2.3. Footwear

- 2.4. Electrical and Electronics

- 2.5. Medical

- 2.6. Household Appliances

- 2.7. HVAC

- 2.8. Adhesives, Sealants, and Coatings

- 2.9. Other Applications

Europe TPE Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Spain

- 6. Rest of Europe

Europe TPE Industry Regional Market Share

Geographic Coverage of Europe TPE Industry

Europe TPE Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Styrenic Block Copolymer (TPE-S)

- 5.1.2. Thermoplastic Olefin (TPE-O)

- 5.1.3. Elastomeric Alloy (TPE-V or TPV)

- 5.1.4. Thermoplastic Polyurethane (TPU)

- 5.1.5. Thermoplastic Copolyester

- 5.1.6. Thermoplastic Polyamide

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive and Transportation

- 5.2.2. Building and Construction

- 5.2.3. Footwear

- 5.2.4. Electrical and Electronics

- 5.2.5. Medical

- 5.2.6. Household Appliances

- 5.2.7. HVAC

- 5.2.8. Adhesives, Sealants, and Coatings

- 5.2.9. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. Italy

- 5.3.4. France

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe TPE Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Styrenic Block Copolymer (TPE-S)

- 6.1.2. Thermoplastic Olefin (TPE-O)

- 6.1.3. Elastomeric Alloy (TPE-V or TPV)

- 6.1.4. Thermoplastic Polyurethane (TPU)

- 6.1.5. Thermoplastic Copolyester

- 6.1.6. Thermoplastic Polyamide

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive and Transportation

- 6.2.2. Building and Construction

- 6.2.3. Footwear

- 6.2.4. Electrical and Electronics

- 6.2.5. Medical

- 6.2.6. Household Appliances

- 6.2.7. HVAC

- 6.2.8. Adhesives, Sealants, and Coatings

- 6.2.9. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Styrenic Block Copolymer (TPE-S)

- 7.1.2. Thermoplastic Olefin (TPE-O)

- 7.1.3. Elastomeric Alloy (TPE-V or TPV)

- 7.1.4. Thermoplastic Polyurethane (TPU)

- 7.1.5. Thermoplastic Copolyester

- 7.1.6. Thermoplastic Polyamide

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Automotive and Transportation

- 7.2.2. Building and Construction

- 7.2.3. Footwear

- 7.2.4. Electrical and Electronics

- 7.2.5. Medical

- 7.2.6. Household Appliances

- 7.2.7. HVAC

- 7.2.8. Adhesives, Sealants, and Coatings

- 7.2.9. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Kingdom Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Styrenic Block Copolymer (TPE-S)

- 8.1.2. Thermoplastic Olefin (TPE-O)

- 8.1.3. Elastomeric Alloy (TPE-V or TPV)

- 8.1.4. Thermoplastic Polyurethane (TPU)

- 8.1.5. Thermoplastic Copolyester

- 8.1.6. Thermoplastic Polyamide

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Automotive and Transportation

- 8.2.2. Building and Construction

- 8.2.3. Footwear

- 8.2.4. Electrical and Electronics

- 8.2.5. Medical

- 8.2.6. Household Appliances

- 8.2.7. HVAC

- 8.2.8. Adhesives, Sealants, and Coatings

- 8.2.9. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Styrenic Block Copolymer (TPE-S)

- 9.1.2. Thermoplastic Olefin (TPE-O)

- 9.1.3. Elastomeric Alloy (TPE-V or TPV)

- 9.1.4. Thermoplastic Polyurethane (TPU)

- 9.1.5. Thermoplastic Copolyester

- 9.1.6. Thermoplastic Polyamide

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Automotive and Transportation

- 9.2.2. Building and Construction

- 9.2.3. Footwear

- 9.2.4. Electrical and Electronics

- 9.2.5. Medical

- 9.2.6. Household Appliances

- 9.2.7. HVAC

- 9.2.8. Adhesives, Sealants, and Coatings

- 9.2.9. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. France Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Styrenic Block Copolymer (TPE-S)

- 10.1.2. Thermoplastic Olefin (TPE-O)

- 10.1.3. Elastomeric Alloy (TPE-V or TPV)

- 10.1.4. Thermoplastic Polyurethane (TPU)

- 10.1.5. Thermoplastic Copolyester

- 10.1.6. Thermoplastic Polyamide

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Automotive and Transportation

- 10.2.2. Building and Construction

- 10.2.3. Footwear

- 10.2.4. Electrical and Electronics

- 10.2.5. Medical

- 10.2.6. Household Appliances

- 10.2.7. HVAC

- 10.2.8. Adhesives, Sealants, and Coatings

- 10.2.9. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Styrenic Block Copolymer (TPE-S)

- 11.1.2. Thermoplastic Olefin (TPE-O)

- 11.1.3. Elastomeric Alloy (TPE-V or TPV)

- 11.1.4. Thermoplastic Polyurethane (TPU)

- 11.1.5. Thermoplastic Copolyester

- 11.1.6. Thermoplastic Polyamide

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Automotive and Transportation

- 11.2.2. Building and Construction

- 11.2.3. Footwear

- 11.2.4. Electrical and Electronics

- 11.2.5. Medical

- 11.2.6. Household Appliances

- 11.2.7. HVAC

- 11.2.8. Adhesives, Sealants, and Coatings

- 11.2.9. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe Europe TPE Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Styrenic Block Copolymer (TPE-S)

- 12.1.2. Thermoplastic Olefin (TPE-O)

- 12.1.3. Elastomeric Alloy (TPE-V or TPV)

- 12.1.4. Thermoplastic Polyurethane (TPU)

- 12.1.5. Thermoplastic Copolyester

- 12.1.6. Thermoplastic Polyamide

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Automotive and Transportation

- 12.2.2. Building and Construction

- 12.2.3. Footwear

- 12.2.4. Electrical and Electronics

- 12.2.5. Medical

- 12.2.6. Household Appliances

- 12.2.7. HVAC

- 12.2.8. Adhesives, Sealants, and Coatings

- 12.2.9. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Grupo Dynasol

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Arkema

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Sumitomo Chemicals Co Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Mitsui Chemicals Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Asahi Kasei Corporation

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Exxon Mobil Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 KURARAY CO LTD

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Mitsubishi Chemical Corporation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Evonik Industries AG

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 LANXESS

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 BASF SE

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Huntsman International LLC

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 SABIC

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 DSM

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 LG Chem

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 DuPont

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 The Lubrizol Corporation*List Not Exhaustive

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 KRATON CORPORATION

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 Apar Industries Ltd

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.20 Covestro AG

- 13.1.20.1. Company Overview

- 13.1.20.2. Products

- 13.1.20.3. Company Financials

- 13.1.20.4. SWOT Analysis

- 13.1.21 LyondellBasell Industries Holdings BV

- 13.1.21.1. Company Overview

- 13.1.21.2. Products

- 13.1.21.3. Company Financials

- 13.1.21.4. SWOT Analysis

- 13.1.22 Sirmax SpA

- 13.1.22.1. Company Overview

- 13.1.22.2. Products

- 13.1.22.3. Company Financials

- 13.1.22.4. SWOT Analysis

- 13.1.1 Grupo Dynasol

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Europe TPE Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe TPE Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Europe TPE Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 11: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Europe TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 21: Europe TPE Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe TPE Industry?

The projected CAGR is approximately 12.42%.

2. Which companies are prominent players in the Europe TPE Industry?

Key companies in the market include Grupo Dynasol, Arkema, Sumitomo Chemicals Co Ltd, Mitsui Chemicals Inc, Asahi Kasei Corporation, Exxon Mobil Corporation, KURARAY CO LTD, Mitsubishi Chemical Corporation, Evonik Industries AG, LANXESS, BASF SE, Huntsman International LLC, SABIC, DSM, LG Chem, DuPont, The Lubrizol Corporation*List Not Exhaustive, KRATON CORPORATION, Apar Industries Ltd, Covestro AG, LyondellBasell Industries Holdings BV, Sirmax SpA.

3. What are the main segments of the Europe TPE Industry?

The market segments include Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.19 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Construction Industry; Growing Applications in the HVAC Industry.

6. What are the notable trends driving market growth?

Increasing Usage in the Automotive and Transportation Applications.

7. Are there any restraints impacting market growth?

Market Saturation in Applications; Unfavorable Conditions Arising due to the Impact of COVID-19.

8. Can you provide examples of recent developments in the market?

November 2022: HEXPOL TPE officially launched bio-attributed medicinal TPEs. Increasing their portfolio of materials that enable a transition away from fossil feedstocks. Mass balancing allows for a progressive increase in bio-circular share utilizing existing infrastructure to reduce fossil resource usage gradually. Because the resulting TPE material is a drop-in solution with equivalent qualities, HEXPOL TPE identified mass balance as a promising alternative for their medical customers. It is because renewable monomers have the same quality and purity as those derived from fossil sources.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe TPE Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe TPE Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe TPE Industry?

To stay informed about further developments, trends, and reports in the Europe TPE Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence