Key Insights

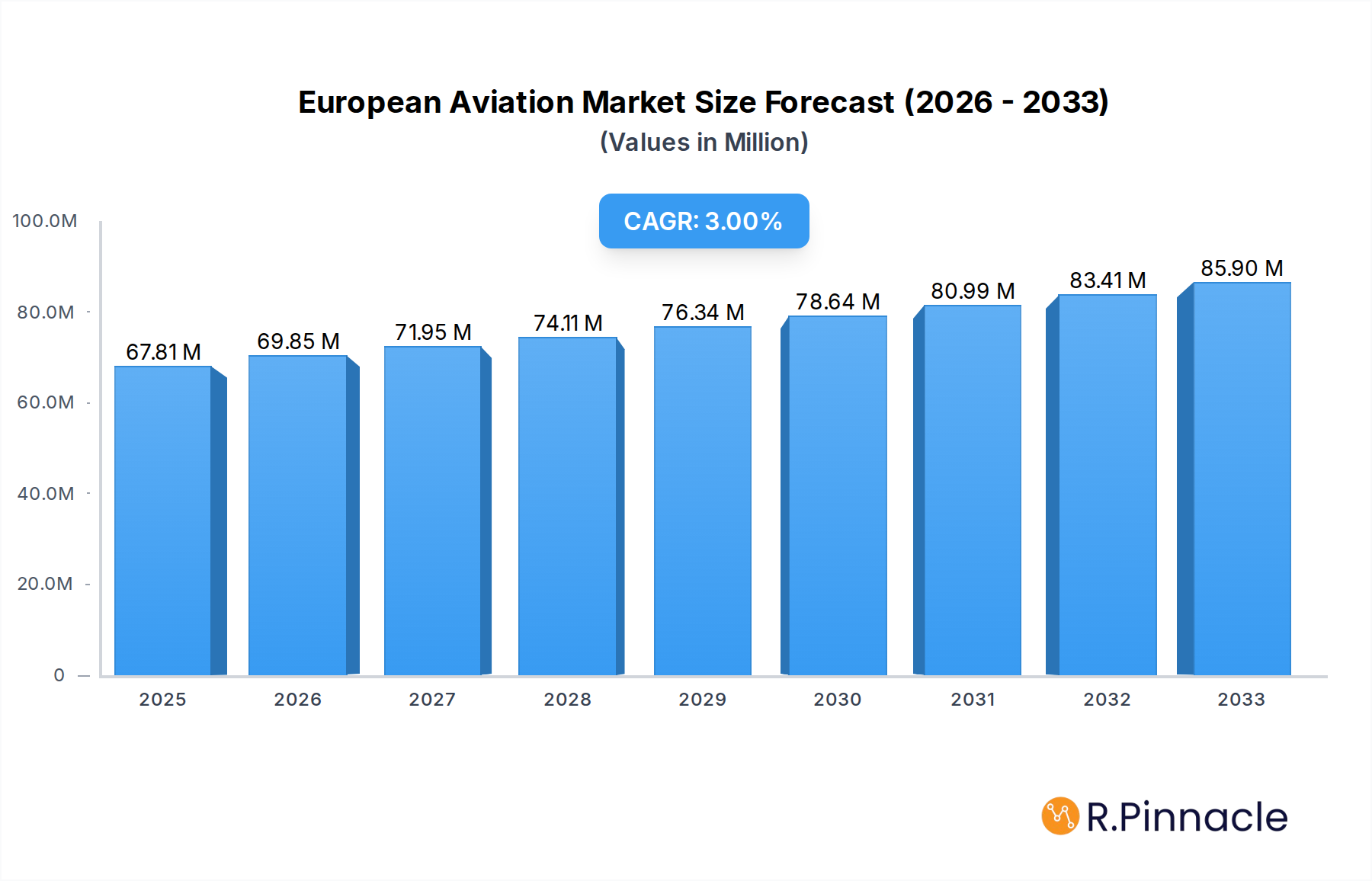

The European Aviation Market is poised for steady growth, currently valued at 67.81 Million and projected to expand at a Compound Annual Growth Rate (CAGR) of 2.98% through 2033. This growth is fueled by several key drivers, including the increasing demand for air travel across commercial segments, a robust defense spending outlook for military aviation, and the sustained popularity of general aviation for business and leisure. The ongoing fleet modernization efforts by major airlines, coupled with significant investments in new aircraft technologies such as sustainable fuels and advanced avionics, are expected to further bolster market expansion. Furthermore, the recovery in air traffic post-pandemic is a significant contributor, with both passenger and cargo volumes steadily returning to pre-pandemic levels and showing signs of exceeding them. The ongoing development and introduction of next-generation aircraft by leading manufacturers like Airbus and Boeing, focusing on fuel efficiency and reduced environmental impact, will also play a crucial role in shaping market dynamics.

European Aviation Market Market Size (In Million)

Despite the positive outlook, certain restraints could temper the market's full potential. These include escalating operational costs, particularly fuel prices and labor expenses, alongside stringent environmental regulations that necessitate significant investment in greener technologies. Geopolitical uncertainties and their impact on global trade and travel can also introduce volatility. However, the strong underlying demand, coupled with technological advancements and strategic investments, is anticipated to largely offset these challenges. The market is segmented across Commercial Aviation (Passenger and Freighter Aircraft), Military Aviation (Combat and Non-combat Aircraft), and General Aviation (Helicopters, Piston Fixed-wing Aircraft, Turboprop Aircraft, and Business Jets). The European region, with established players like Airbus, Dassault Aviation, and Leonardo S.p.A., is a significant hub for both manufacturing and operations, driving innovation and demand across all segments.

European Aviation Market Company Market Share

Unlock the Future of European Aviation: A Comprehensive Market Analysis (2019-2033)

This in-depth report provides a definitive overview of the European aviation market, spanning from 2019 to 2033, with a robust focus on the base year 2025 and an extended forecast period from 2025 to 2033. Delve into crucial industry trends, market dynamics, product innovations, and the strategic landscape shaped by leading players and pivotal developments. With a wealth of actionable insights and high-ranking keywords, this report is essential for aerospace manufacturers, airlines, defense contractors, and investors seeking to navigate and capitalize on this dynamic sector.

European Aviation Market Market Structure & Innovation Trends

The European aviation market is characterized by a high degree of concentration, dominated by a few key global players. Innovation remains a primary driver, fueled by advancements in sustainable aviation technologies, digitalization, and autonomous systems. Regulatory frameworks, while complex, are increasingly emphasizing environmental sustainability and enhanced safety standards, influencing both market entry and product development. Substitutes, though limited in core aviation functions, are emerging in the form of advanced simulation and virtual training, impacting the demand for certain training aircraft. End-user demographics are evolving, with a growing demand for personalized travel experiences in commercial aviation and specialized capabilities in military and general aviation. Mergers and acquisitions (M&A) activities continue to shape the landscape, with significant deal values aimed at consolidating market share and acquiring technological expertise. For instance, major M&A activities are anticipated to reach over several hundred million dollars annually throughout the forecast period, reshaping competitive landscapes and fostering strategic alliances.

European Aviation Market Market Dynamics & Trends

The European aviation market is poised for substantial growth, driven by a confluence of factors including increasing air passenger traffic, rising defense expenditures, and a burgeoning demand for general aviation services. The projected Compound Annual Growth Rate (CAGR) for the overall market is estimated to be between 4% and 6% for the forecast period. Technological disruptions are at the forefront, with the integration of artificial intelligence (AI), advanced materials, and electric/hybrid propulsion systems revolutionizing aircraft design and operational efficiency. Consumer preferences are shifting towards more sustainable and personalized travel options, compelling airlines to invest in fuel-efficient fleets and enhanced passenger amenities. The competitive dynamics are intensifying, with established giants like Airbus SE and The Boeing Company vying for market dominance against agile innovators and specialized manufacturers such as Embraer S. and Pilatus Aircraft Ltd. Market penetration for advanced avionics and connectivity solutions is expected to exceed 75% by 2033. The increasing focus on urban air mobility (UAM) and eVTOL (electric Vertical Take-Off and Landing) aircraft represents a significant emerging trend, with substantial investment flowing into research and development. Furthermore, the ongoing modernization of military fleets across European nations is a critical growth catalyst, driving demand for advanced combat and non-combat aircraft.

Dominant Regions & Segments in European Aviation Market

The Commercial Aviation segment, particularly Passenger Aircraft, consistently holds the largest market share within the European aviation landscape, projected to account for over 60% of the total market value by 2033. This dominance is underpinned by robust economic policies promoting air travel, extensive airport infrastructure development, and a growing middle class across Europe. Key drivers include increasing intra-European travel, long-haul routes connecting to global hubs, and the continuous demand for fleet modernization to enhance fuel efficiency and passenger comfort. Major airlines' fleet expansion plans and replacement cycles are critical determinants of growth in this segment.

The Military Aviation segment, encompassing both Combat Aircraft and Non-combat Aircraft, represents the second-largest and a strategically vital segment. The increasing geopolitical tensions and modernization initiatives by European defense ministries are significant drivers. Germany's procurement of F-35A aircraft, valued at USD 8.4 billion, exemplifies the substantial investments in advanced fighter jets. The UK's trials of new Protector surveillance aircraft highlight the growing emphasis on unmanned aerial vehicles (UAVs) for surveillance and reconnaissance. Economic factors, defense budgets, and national security strategies heavily influence this segment's growth trajectory. The demand for advanced electronic warfare capabilities and intelligence, surveillance, and reconnaissance (ISR) platforms remains high.

The General Aviation segment, while smaller in overall market value, is crucial for its diverse applications, including Helicopters, Piston Fixed-wing Aircraft, Turboprop Aircraft, and Business Jets. This segment is driven by private ownership, corporate travel, medical evacuation services, and specialized aerial work. The increasing adoption of business jets by high-net-worth individuals and corporations, coupled with the demand for helicopters in emergency services and logistics, contributes to steady growth. The forecast period anticipates robust expansion in the turboprop aircraft market, driven by their versatility and cost-effectiveness for regional operations. Regulatory ease and infrastructure availability in specific regions play a pivotal role in segment expansion.

European Aviation Market Product Innovations

Recent product innovations in the European aviation market are heavily focused on sustainability and technological advancement. The development of more fuel-efficient engines, lightweight composite materials, and advanced aerodynamics are enhancing aircraft performance and reducing environmental impact. The increasing integration of AI in flight management systems and predictive maintenance is improving operational efficiency and safety. Furthermore, the growing interest in electric and hybrid-electric propulsion systems for both commercial and general aviation is a significant trend, promising quieter and cleaner flight operations. These innovations offer distinct competitive advantages by addressing regulatory demands, reducing operational costs, and meeting evolving customer expectations for greener air travel.

European Aviation Market Market Scope & Segmentation Analysis

The European Aviation Market is segmented across Commercial Aviation (Passenger Aircraft, Freighter Aircraft), Military Aviation (Combat Aircraft, Non-combat Aircraft), and General Aviation (Helicopters, Piston Fixed-wing Aircraft, Turboprop Aircraft, Business Jet). The Commercial Aviation segment, encompassing passenger and freighter aircraft, is projected to experience a CAGR of approximately 5% to 7% through 2033, driven by increasing passenger demand and global trade. Military Aviation is anticipated to grow at a CAGR of 3% to 5%, fueled by defense modernization programs and geopolitical security concerns. General Aviation is expected to witness a CAGR of 4% to 6%, propelled by the demand for private travel and specialized aerial services. Competitive dynamics vary significantly across these segments, with established OEMs dominating commercial and military, while a more fragmented landscape exists in general aviation.

Key Drivers of European Aviation Market Growth

Several key factors are propelling the growth of the European aviation market. Technological advancements, particularly in sustainable aviation fuels (SAFs), electric propulsion, and advanced manufacturing techniques, are creating new opportunities. Economic recovery and rising disposable incomes globally are boosting air travel demand, directly benefiting commercial aviation. Government initiatives and increased defense spending across European nations are stimulating the military aviation sector. Furthermore, a growing emphasis on innovation and research and development, supported by European Union funding and national programs, fosters a conducive environment for market expansion. The development of advanced air traffic management systems is also crucial for accommodating increased air traffic efficiently.

Challenges in the European Aviation Market Sector

Despite its growth potential, the European aviation market faces significant challenges. Stringent environmental regulations and the push towards net-zero emissions necessitate substantial investment in green technologies, posing a financial burden. Supply chain disruptions, exacerbated by geopolitical events and raw material shortages, continue to impact production timelines and costs. Intense competition among established players and the emergence of new entrants create pricing pressures. Labor shortages in skilled aviation professions, from engineers to pilots, also present a restraint. The significant upfront cost of new aircraft and infrastructure development, coupled with potential economic downturns, can also hinder market expansion.

Emerging Opportunities in European Aviation Market

Emerging opportunities in the European aviation market are abundant, driven by innovation and evolving market demands. The rapid development of urban air mobility (UAM) and eVTOL aircraft presents a transformative opportunity for intra-city transport. The increasing adoption of SAFs and the pursuit of sustainable aviation technologies offer significant market potential for companies at the forefront of this revolution. The digitalization of aviation, including the use of AI for operational efficiency and predictive maintenance, is another key area of growth. Furthermore, the growing demand for advanced training solutions and simulation technologies, especially in the military and commercial pilot training sectors, provides lucrative avenues for specialized providers.

Leading Players in the European Aviation Market Market

- Textron Inc

- General Dynamics Corporation

- Embraer S

- Lockheed Martin Corporation

- Airbus SE

- Dassault Aviation SA

- Pilatus Aircraft Ltd

- Daher

- Leonardo S p A

- Bombardier Inc

- Saab AB

- The Boeing Company

Key Developments in European Aviation Market Industry

- October 2023: The UK announced trials for 16 new Protector aircraft surveillance aircraft, with test flights expected to conclude in late 2024, marking a significant step in the integration of uncrewed global surveillance capabilities for the RAF.

- October 2022: Jet2, a British airline, placed an order for 35 A320neo family aircraft, with an option for an additional 36. This order, valued at approximately USD 3.9 billion (potentially rising to USD 8 billion if options are exercised), highlights continued investment in modern, fuel-efficient passenger aircraft, with deliveries anticipated in 2031.

- July 2022: The US State Department approved the foreign military sale of up to 35 F-35A aircraft to Germany for USD 8.4 billion. This acquisition is crucial for Germany's nuclear deterrence mission and will replace its aging Tornado fleet, signaling a significant upgrade in European military air power.

Future Outlook for European Aviation Market Market

The future outlook for the European aviation market is exceptionally strong, driven by an unwavering commitment to innovation and sustainability. The ongoing transition towards net-zero emissions will accelerate investments in electric and hybrid aircraft, SAFs, and advanced materials, creating new market niches and revenue streams. The persistent demand for air travel, coupled with strategic defense investments, will ensure robust growth in commercial and military aviation. The emergence of urban air mobility and advancements in digital aviation technologies will further diversify the market and unlock new operational efficiencies. Strategic partnerships and collaborations among industry players will be crucial for navigating the evolving landscape and capitalizing on emerging opportunities, positioning the European aviation market for sustained global leadership.

European Aviation Market Segmentation

-

1. Type

-

1.1. Commercial Aviation

- 1.1.1. Passenger Aircraft

- 1.1.2. Freighter Aircraft

-

1.2. Military Aviation

- 1.2.1. Combat Aircraft

- 1.2.2. Non-combat Aircraft

-

1.3. General Aviation

- 1.3.1. Helicopters

- 1.3.2. Piston Fixed-wing Aircraft

- 1.3.3. Turboprop Aircraft

- 1.3.4. Business Jet

-

1.1. Commercial Aviation

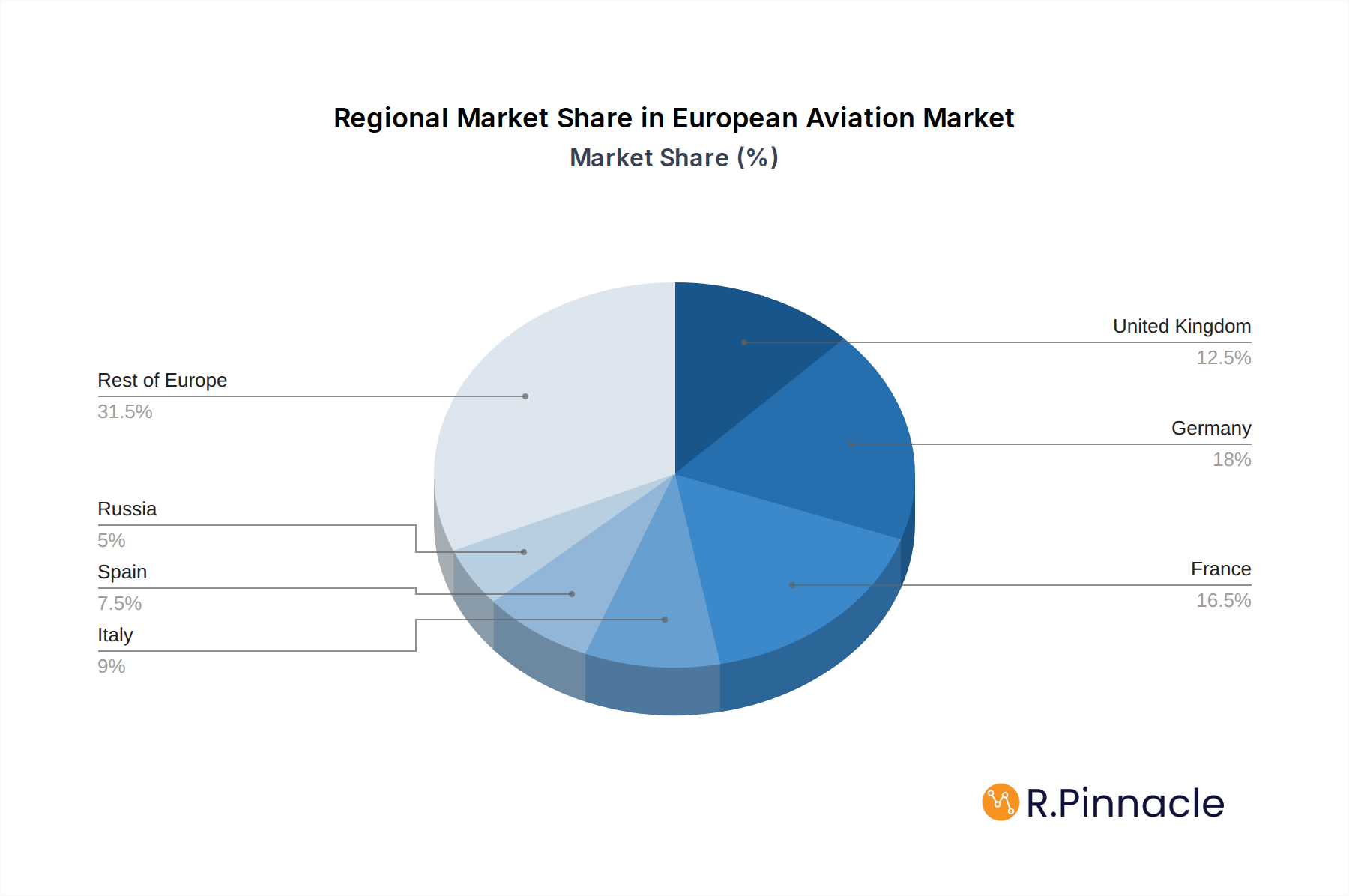

European Aviation Market Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. France

- 4. Italy

- 5. Spain

- 6. Russia

- 7. Rest of Europe

European Aviation Market Regional Market Share

Geographic Coverage of European Aviation Market

European Aviation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. Passenger Aircraft

- 5.1.1.2. Freighter Aircraft

- 5.1.2. Military Aviation

- 5.1.2.1. Combat Aircraft

- 5.1.2.2. Non-combat Aircraft

- 5.1.3. General Aviation

- 5.1.3.1. Helicopters

- 5.1.3.2. Piston Fixed-wing Aircraft

- 5.1.3.3. Turboprop Aircraft

- 5.1.3.4. Business Jet

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United Kingdom

- 5.2.2. Germany

- 5.2.3. France

- 5.2.4. Italy

- 5.2.5. Spain

- 5.2.6. Russia

- 5.2.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. European Aviation Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. Passenger Aircraft

- 6.1.1.2. Freighter Aircraft

- 6.1.2. Military Aviation

- 6.1.2.1. Combat Aircraft

- 6.1.2.2. Non-combat Aircraft

- 6.1.3. General Aviation

- 6.1.3.1. Helicopters

- 6.1.3.2. Piston Fixed-wing Aircraft

- 6.1.3.3. Turboprop Aircraft

- 6.1.3.4. Business Jet

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Kingdom European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Commercial Aviation

- 7.1.1.1. Passenger Aircraft

- 7.1.1.2. Freighter Aircraft

- 7.1.2. Military Aviation

- 7.1.2.1. Combat Aircraft

- 7.1.2.2. Non-combat Aircraft

- 7.1.3. General Aviation

- 7.1.3.1. Helicopters

- 7.1.3.2. Piston Fixed-wing Aircraft

- 7.1.3.3. Turboprop Aircraft

- 7.1.3.4. Business Jet

- 7.1.1. Commercial Aviation

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Germany European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Commercial Aviation

- 8.1.1.1. Passenger Aircraft

- 8.1.1.2. Freighter Aircraft

- 8.1.2. Military Aviation

- 8.1.2.1. Combat Aircraft

- 8.1.2.2. Non-combat Aircraft

- 8.1.3. General Aviation

- 8.1.3.1. Helicopters

- 8.1.3.2. Piston Fixed-wing Aircraft

- 8.1.3.3. Turboprop Aircraft

- 8.1.3.4. Business Jet

- 8.1.1. Commercial Aviation

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. France European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Commercial Aviation

- 9.1.1.1. Passenger Aircraft

- 9.1.1.2. Freighter Aircraft

- 9.1.2. Military Aviation

- 9.1.2.1. Combat Aircraft

- 9.1.2.2. Non-combat Aircraft

- 9.1.3. General Aviation

- 9.1.3.1. Helicopters

- 9.1.3.2. Piston Fixed-wing Aircraft

- 9.1.3.3. Turboprop Aircraft

- 9.1.3.4. Business Jet

- 9.1.1. Commercial Aviation

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Italy European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Commercial Aviation

- 10.1.1.1. Passenger Aircraft

- 10.1.1.2. Freighter Aircraft

- 10.1.2. Military Aviation

- 10.1.2.1. Combat Aircraft

- 10.1.2.2. Non-combat Aircraft

- 10.1.3. General Aviation

- 10.1.3.1. Helicopters

- 10.1.3.2. Piston Fixed-wing Aircraft

- 10.1.3.3. Turboprop Aircraft

- 10.1.3.4. Business Jet

- 10.1.1. Commercial Aviation

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Spain European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Commercial Aviation

- 11.1.1.1. Passenger Aircraft

- 11.1.1.2. Freighter Aircraft

- 11.1.2. Military Aviation

- 11.1.2.1. Combat Aircraft

- 11.1.2.2. Non-combat Aircraft

- 11.1.3. General Aviation

- 11.1.3.1. Helicopters

- 11.1.3.2. Piston Fixed-wing Aircraft

- 11.1.3.3. Turboprop Aircraft

- 11.1.3.4. Business Jet

- 11.1.1. Commercial Aviation

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Russia European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Commercial Aviation

- 12.1.1.1. Passenger Aircraft

- 12.1.1.2. Freighter Aircraft

- 12.1.2. Military Aviation

- 12.1.2.1. Combat Aircraft

- 12.1.2.2. Non-combat Aircraft

- 12.1.3. General Aviation

- 12.1.3.1. Helicopters

- 12.1.3.2. Piston Fixed-wing Aircraft

- 12.1.3.3. Turboprop Aircraft

- 12.1.3.4. Business Jet

- 12.1.1. Commercial Aviation

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Rest of Europe European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Type

- 13.1.1. Commercial Aviation

- 13.1.1.1. Passenger Aircraft

- 13.1.1.2. Freighter Aircraft

- 13.1.2. Military Aviation

- 13.1.2.1. Combat Aircraft

- 13.1.2.2. Non-combat Aircraft

- 13.1.3. General Aviation

- 13.1.3.1. Helicopters

- 13.1.3.2. Piston Fixed-wing Aircraft

- 13.1.3.3. Turboprop Aircraft

- 13.1.3.4. Business Jet

- 13.1.1. Commercial Aviation

- 13.1. Market Analysis, Insights and Forecast - by Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Textron Inc

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 General Dynamics Corporation

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Embraer S

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Lockheed Martin Corporation

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Airbus SE

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Dassult Aviation SA

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Pilatus Aircraft Ltd

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Daher

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Leonardo S p A

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Bombardier Inc

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Saab AB

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 The Boeing Company

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.1 Textron Inc

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: European Aviation Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: European Aviation Market Share (%) by Company 2025

List of Tables

- Table 1: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: European Aviation Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 4: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 5: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 6: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 10: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 11: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 12: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 14: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 15: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 16: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Aviation Market?

The projected CAGR is approximately 2.98%.

2. Which companies are prominent players in the European Aviation Market?

Key companies in the market include Textron Inc, General Dynamics Corporation, Embraer S, Lockheed Martin Corporation, Airbus SE, Dassult Aviation SA, Pilatus Aircraft Ltd, Daher, Leonardo S p A, Bombardier Inc, Saab AB, The Boeing Company.

3. What are the main segments of the European Aviation Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.81 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Military Segment to Showcase Remarkable Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

October 2023: The UK announced that the country will likely start trials of new 16 Protector aircraft surveillance aircraft. Aircraft is expected to undergo test flights until entering service in late 2024. A new uncrewed RAF aircraft is capable of global surveillance operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Aviation Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Aviation Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Aviation Market?

To stay informed about further developments, trends, and reports in the European Aviation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence