Key Insights

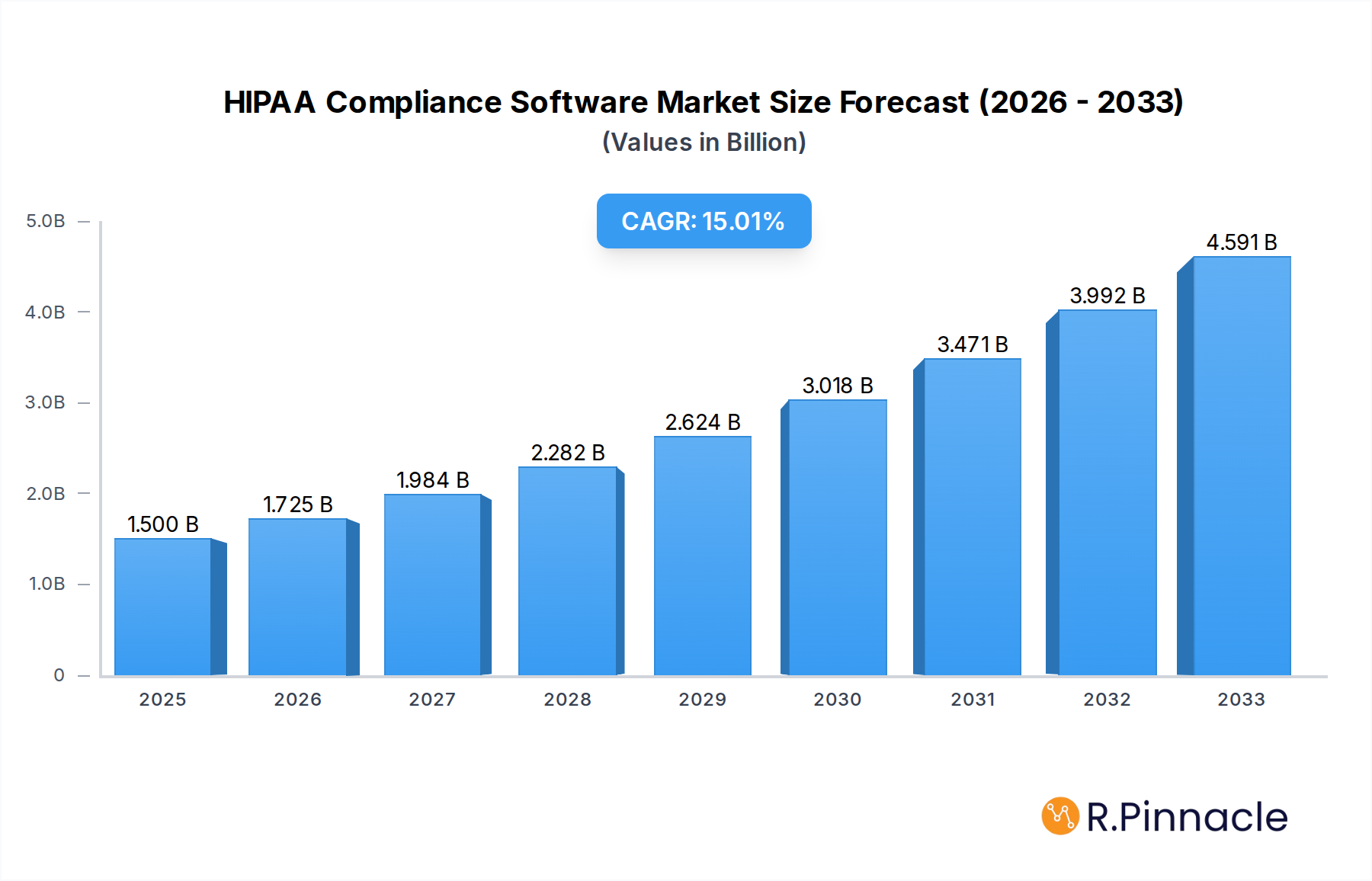

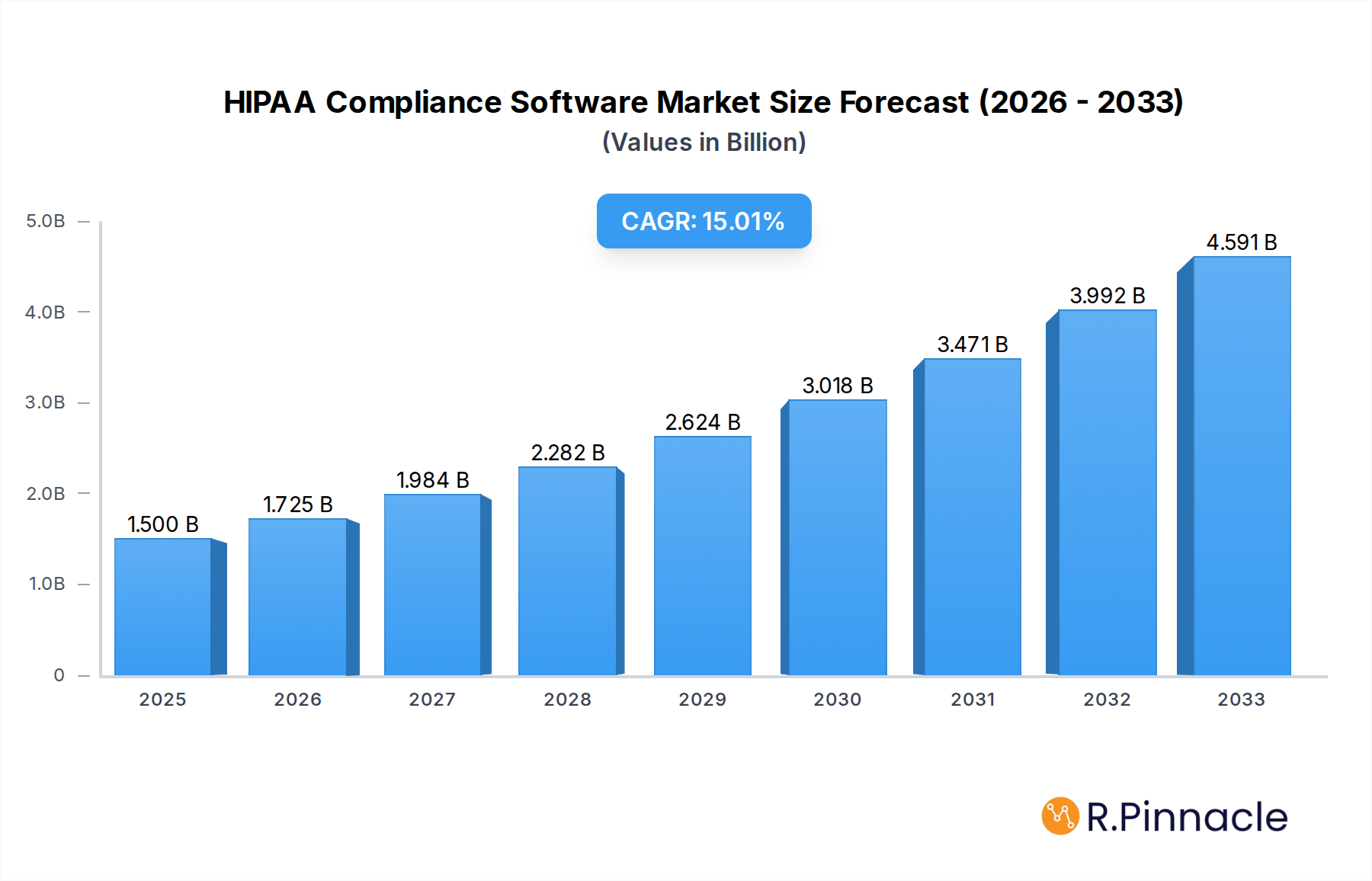

The HIPAA Compliance Software market is poised for substantial expansion, with an estimated market size of $1.5 billion in 2025. This robust growth is projected to continue at a compound annual growth rate (CAGR) of 15% throughout the forecast period, reaching significant valuations by 2033. This upward trajectory is primarily fueled by escalating healthcare data breaches, stringent regulatory enforcement, and the increasing adoption of digital health technologies. Healthcare organizations, research institutes, and even cloud service providers are investing heavily in sophisticated compliance solutions to safeguard sensitive patient information and avoid hefty penalties. The growing emphasis on data privacy and security, coupled with the complexity of HIPAA regulations, necessitates the use of specialized software.

HIPAA Compliance Software Market Size (In Billion)

The market's dynamism is further shaped by key trends such as the surge in cloud-based solutions offering scalability and cost-effectiveness, alongside the continued demand for on-premises deployments for organizations with specific security mandates. These solutions are instrumental in automating compliance tasks, conducting risk assessments, managing access controls, and ensuring data encryption, thereby streamlining operations for healthcare providers. While the market exhibits strong growth drivers, potential restraints include the high initial investment costs for some advanced solutions and the ongoing challenge of keeping pace with evolving regulatory landscapes and technological advancements. The competitive landscape is characterized by a mix of established players and innovative startups, all vying to provide comprehensive and user-friendly HIPAA compliance software tailored to diverse organizational needs.

HIPAA Compliance Software Company Market Share

This comprehensive report offers an in-depth analysis of the HIPAA Compliance Software Market, a critical sector for healthcare organizations safeguarding Protected Health Information (PHI). Delve into market structure, dynamic trends, regional dominance, and cutting-edge product innovations. Understand the key drivers, challenges, and emerging opportunities that are shaping the future of HIPAA compliance. This report is essential for IT professionals, compliance officers, security analysts, and decision-makers within hospitals, research institutes, and other healthcare entities.

HIPAA Compliance Software Market Structure & Innovation Trends

The HIPAA Compliance Software market exhibits a moderately concentrated structure, with a mix of established vendors and emerging innovators. The presence of market leaders like Ostendio and Congruity 360 alongside specialized providers such as DriveStrike and LifeOmic indicates a dynamic competitive landscape. Innovation is primarily driven by the increasing sophistication of cyber threats, the growing volume of digital health data, and evolving regulatory interpretations. Key innovation trends include the integration of AI and machine learning for anomaly detection, automated risk assessments, and streamlined auditing processes. Regulatory frameworks, particularly those enforced by the Office for Civil Rights (OCR), remain the cornerstone of market development, compelling continuous adaptation and investment in compliance solutions. Product substitutes, such as manual compliance processes or generalized cybersecurity platforms, are becoming increasingly inadequate given the specialized needs of HIPAA. End-user demographics span a wide range, from small clinics to large hospital networks and research institutions, each with distinct compliance requirements and budget considerations. Mergers and acquisitions (M&A) activities, while not always publicly disclosed in terms of precise deal values, are strategically significant, consolidating market share and expanding product portfolios. For instance, advancements in cloud-based solutions have driven a shift from on-premises deployments, influencing the strategic focus of companies like Azalea Health and SecPod Technologies. The overall market is projected to see significant M&A activity in the coming years, with estimated deal values in the low billion range, as larger players seek to acquire innovative technologies and expand their customer base.

HIPAA Compliance Software Market Dynamics & Trends

The HIPAA Compliance Software Market is poised for robust growth, fueled by a confluence of escalating data security concerns and stringent regulatory mandates. The market is experiencing a significant upward trajectory, with a projected Compound Annual Growth Rate (CAGR) of approximately 15% to 18% during the forecast period of 2025–2033. This impressive growth is underpinned by several key market dynamics. Firstly, the sheer volume and sensitivity of healthcare data continue to expand exponentially, making robust compliance solutions not just a best practice but a necessity. The increasing adoption of telehealth, remote patient monitoring, and electronic health records (EHRs) by entities like Vicarius and Zenefits amplifies the attack surface and, consequently, the demand for comprehensive HIPAA compliance software. Secondly, technological disruptions are playing a pivotal role. The integration of Artificial Intelligence (AI) and Machine Learning (ML) is transforming the way organizations achieve and maintain compliance, enabling proactive threat detection, automated vulnerability assessments, and more efficient policy management, as exemplified by solutions from MedTrainer and EMS Healthcare Informatics. Furthermore, evolving consumer preferences for secure and private healthcare data are pushing organizations to invest more heavily in compliance. Patients are increasingly aware of their data rights and expect healthcare providers to adhere to the highest standards of security. The competitive dynamics within the market are intense, characterized by continuous product development, strategic partnerships, and a focus on user experience. Companies are differentiating themselves through specialized features, ease of implementation, and superior customer support. The market penetration of HIPAA compliance solutions is still growing, particularly among small to medium-sized healthcare providers who may have previously lacked the resources or expertise to implement comprehensive compliance programs. Leading providers such as HIPAA One, Hushmail, and Progress Software are actively innovating to address these diverse needs, offering scalable and cost-effective solutions. The shift towards cloud-based solutions is a dominant trend, offering greater flexibility, scalability, and cost-efficiency compared to traditional on-premises deployments, a trend that is further accelerated by the needs of entities like PCIHIPAA and Inviscid Software.

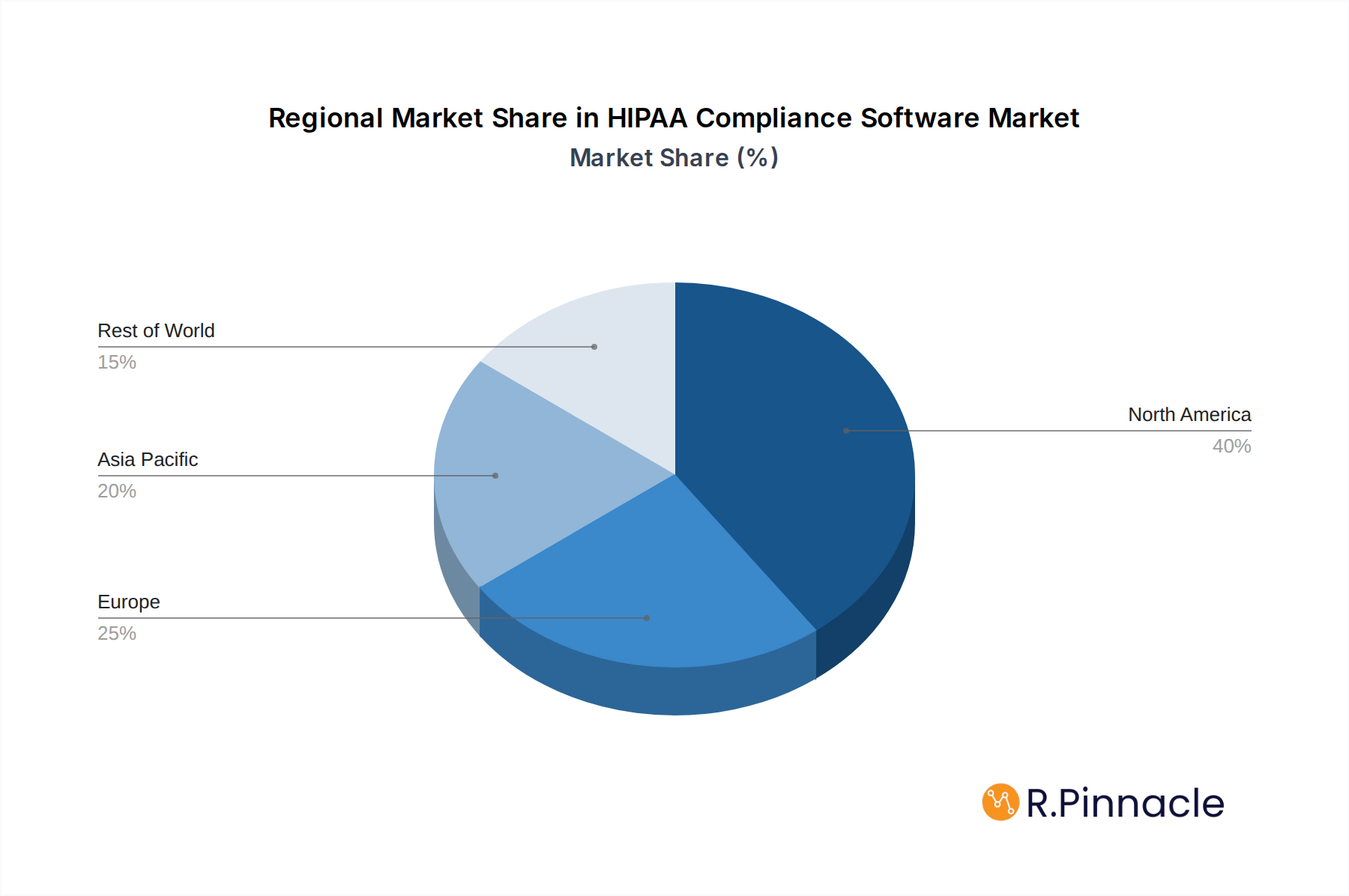

Dominant Regions & Segments in HIPAA Compliance Software

The HIPAA Compliance Software Market demonstrates a clear regional and segment dominance, driven by economic policies, established healthcare infrastructure, and stringent regulatory enforcement. The North America region, particularly the United States, stands as the undisputed leader in this market. This dominance is intrinsically linked to the foundational HIPAA legislation itself, which mandates strict adherence to data privacy and security standards for all covered entities. The concentration of major healthcare providers, extensive research institutes, and a mature technology ecosystem within the US fuels substantial demand for advanced HIPAA compliance solutions. Economic policies in the US have consistently prioritized healthcare innovation and patient data protection, creating a fertile ground for companies like Virtru and HIPAAMATE to thrive. Furthermore, the robust digital transformation within the US healthcare sector, encompassing widespread adoption of EHRs, telemedicine, and cloud-based healthcare platforms, directly translates into increased reliance on specialized compliance software.

Within North America, specific segments are particularly influential:

- Application Segment: Hospital: Hospitals, as primary custodians of sensitive patient data, represent the largest application segment. The complexity of hospital operations, the sheer volume of data handled, and the high risk of breaches necessitate comprehensive and sophisticated HIPAA compliance software. Companies like Paubox and LogicManager cater extensively to this segment, offering solutions for risk management, incident response, and policy enforcement. The increasing integration of IoT devices and AI-driven diagnostics within hospital settings further elevates the demand for advanced security and compliance measures.

- Types Segment: Cloud-Based: The cloud-based deployment model has emerged as the dominant type, outpacing on-premises solutions. This is attributed to the inherent scalability, flexibility, and cost-effectiveness offered by cloud platforms. For healthcare organizations, the ability to access and manage compliance data remotely, integrate with various cloud-based healthcare applications, and benefit from vendor-managed updates makes cloud solutions highly attractive. Providers such as Accountable and HIPAAtrek are largely focused on delivering SaaS-based HIPAA compliance solutions, recognizing the market's strong preference for this model. The ease of deployment and ongoing maintenance associated with cloud solutions also appeals to organizations of all sizes, from smaller practices to large hospital networks.

- Application Segment: Research Institute: Research institutes, while also covered by HIPAA, present unique compliance challenges due to their focus on data analysis, de-identification, and sharing of research findings. The need to balance data access for research with stringent privacy requirements drives demand for specialized compliance tools that can facilitate secure data de-identification, audit trails, and consent management. While smaller than the hospital segment, the research institute sector represents a significant and growing market for HIPAA compliance software, with companies like Promisec and Abyde offering tailored solutions.

- Types Segment: On-Premises: While cloud-based solutions are ascendant, on-premises deployments still hold relevance for organizations with specific data sovereignty concerns or existing heavy investments in on-premises infrastructure. These deployments often cater to larger, more established healthcare systems that require granular control over their data environment. However, the trend clearly favors cloud adoption due to its inherent advantages in agility and cost management.

The dominance of North America, particularly the US, is further reinforced by the active role of regulatory bodies like the Department of Health and Human Services (HHS) and the Office for Civil Rights (OCR), which consistently enforce HIPAA regulations. This regulatory pressure compels organizations to invest in robust compliance software, ensuring sustained market growth and innovation in these dominant regions and segments.

HIPAA Compliance Software Market Product Innovations

HIPAA compliance software is witnessing rapid product innovation, driven by the need for more automated, integrated, and intelligent solutions. Key developments include the integration of AI/ML for advanced threat detection, automated risk assessments, and real-time vulnerability management. Solutions are increasingly offering end-to-end compliance lifecycle management, from policy creation and training to incident response and audit preparedness. Companies are focusing on enhancing user experience through intuitive dashboards, customizable workflows, and seamless integration with existing EHR and IT systems. Competitive advantages are being forged through specialized features like automated business associate agreement (BAA) management, robust data encryption capabilities, and proactive compliance monitoring. The market is also seeing the rise of comprehensive platforms that bundle various compliance functionalities, offering a one-stop-shop solution for healthcare organizations.

Report Scope & Segmentation Analysis

This report meticulously segments the HIPAA Compliance Software Market across critical dimensions to provide granular insights.

Application Segment: Hospital: This segment encompasses hospitals of all sizes, from small community hospitals to large multi-facility health systems. The market size for HIPAA compliance software within the hospital segment is substantial, driven by the continuous need to manage vast amounts of sensitive patient data, comply with complex regulations, and mitigate the risk of costly data breaches. Projections indicate strong growth as hospitals increasingly adopt digital health technologies. Competitive dynamics here are characterized by a need for scalable, comprehensive solutions that can integrate with existing EHR systems and manage diverse compliance requirements.

Application Segment: Research Institute: This segment includes academic research institutions, pharmaceutical companies, and other entities involved in medical research. The market size here is driven by the unique compliance needs of handling research data, ensuring de-identification protocols are met, and maintaining secure data sharing frameworks. Growth projections for this segment are positive, as research increasingly relies on digital data management. Competition focuses on specialized features for data anonymization, consent management, and robust audit trails for research data.

Types Segment: Cloud-Based: This segment covers HIPAA compliance software delivered via a Software-as-a-Service (SaaS) model. The market size for cloud-based solutions is the largest and fastest-growing, owing to their inherent scalability, accessibility, and cost-effectiveness. Growth projections are extremely high as healthcare organizations embrace digital transformation. Competitive dynamics revolve around ease of integration, vendor reliability, security certifications, and ongoing feature updates.

Types Segment: On-Premises: This segment includes HIPAA compliance software installed and managed on an organization's own servers. While smaller in market size and growth compared to cloud-based solutions, it remains relevant for organizations with strict data sovereignty requirements or existing on-premises infrastructure investments. Growth in this segment is slower, and competition centers on advanced customization, control over the IT environment, and integration with legacy on-premises systems.

Key Drivers of HIPAA Compliance Software Growth

The growth of the HIPAA Compliance Software market is propelled by several interconnected factors. Increasingly sophisticated cyber threats targeting healthcare data, including ransomware and phishing attacks, necessitate robust security and compliance measures. Stringent regulatory enforcement by bodies like the Office for Civil Rights (OCR), with significant penalties for non-compliance, acts as a powerful catalyst for investment. The accelerated digital transformation in healthcare, marked by the widespread adoption of EHRs, telehealth, and cloud computing, expands the attack surface and elevates the demand for compliance solutions. Furthermore, growing patient awareness and demand for data privacy are pressuring healthcare organizations to strengthen their security postures. The ever-expanding volume of healthcare data itself, coupled with the need for secure data analytics and sharing for research and improved patient care, also drives the market.

Challenges in the HIPAA Compliance Software Sector

Despite robust growth, the HIPAA Compliance Software sector faces significant challenges. The complexity and constant evolution of HIPAA regulations require continuous adaptation and investment, which can be a burden, especially for smaller organizations. The high cost of implementing and maintaining comprehensive compliance programs, including software, personnel, and training, remains a barrier. A shortage of skilled cybersecurity and compliance professionals further exacerbates these challenges. Integration complexities with disparate legacy healthcare IT systems can hinder seamless implementation. Additionally, the evolving nature of cyber threats means that compliance solutions must constantly be updated to remain effective, creating an ongoing arms race. The supply chain for essential security components can also be vulnerable, impacting the delivery of compliant solutions.

Emerging Opportunities in HIPAA Compliance Software

The HIPAA Compliance Software market is ripe with emerging opportunities. The growing adoption of AI and machine learning presents a significant opportunity for developing more intelligent, proactive, and automated compliance solutions, such as predictive analytics for risk identification. The expansion of telehealth and remote patient monitoring creates a demand for specialized compliance tools designed for distributed healthcare environments. There is a growing need for integrated solutions that offer a holistic approach to cybersecurity and compliance, encompassing risk management, data protection, and incident response. Furthermore, as the market matures, there is an opportunity for vendors to offer specialized compliance solutions tailored to niche healthcare sectors, such as dental practices, mental health providers, or specialized clinics. The increasing focus on data interoperability and secure data sharing for research purposes also opens avenues for innovative compliance tools.

Leading Players in the HIPAA Compliance Software Market

- Ostendio

- Congruity 360

- DriveStrike

- LifeOmic

- Azalea Health

- SecPod Technologies

- Vicarius

- Zenefits

- MedTrainer

- EMS Healthcare Informatics

- HIPAA One

- Hushmail

- Progress Software

- PCIHIPAA

- Inviscid Software

- Virtru

- HIPAAMATE

- Paubox

- LogicManager

- Accountable

- HIPAAtrek

- Promisec

- Abyde

- SecurityMetrics

- HIPAA Survival Guide

Key Developments in HIPAA Compliance Software Industry

- 2023 September: Introduction of AI-powered automated risk assessment features by LogicManager, enhancing proactive compliance.

- 2023 August: Paubox announces enhanced encryption protocols for email security, addressing growing concerns over PHI transmission.

- 2023 July: Ostendio expands its platform with advanced incident response management tools, streamlining breach notification processes.

- 2023 June: SecPod Technologies launches a new vulnerability management module, enabling continuous monitoring and remediation for healthcare IT infrastructure.

- 2023 May: Congruity 360 introduces a cloud-based HIPAA compliance platform designed for small to medium-sized healthcare practices, increasing accessibility.

- 2023 April: HIPAA One rolls out enhanced business associate management features, simplifying vendor risk assessment.

- 2023 March: MedTrainer integrates telehealth compliance modules, supporting the growing remote care ecosystem.

- 2023 February: Vicarius releases an updated threat intelligence feed specifically for healthcare, bolstering defense against emerging attack vectors.

- 2023 January: Abyde introduces an intuitive compliance dashboard for easier navigation and reporting.

- 2022 December: Virtru strengthens its data protection capabilities with advanced end-to-end encryption for cloud-based storage.

- 2022 November: Zenefits expands its HR compliance offerings to include specific HIPAA training modules for healthcare employers.

- 2022 October: HIPAAtrek partners with EHR providers to facilitate seamless integration of compliance workflows.

- 2022 September: Promisec focuses on strengthening endpoint security solutions for research institutes handling sensitive data.

- 2022 August: Progress Software announces its commitment to supporting HIPAA compliance within its application development platforms.

- 2022 July: LifeOmic showcases its secure cloud platform designed for managing health data compliant with HIPAA.

- 2022 June: Hushmail enhances its secure messaging features to ensure compliance with HIPAA email requirements.

- 2022 May: DriveStrike introduces mobile device management capabilities to enforce HIPAA compliance on portable devices.

- 2022 April: Azalea Health continues to integrate HIPAA compliance into its EHR solutions for comprehensive data management.

- 2022 March: EMS Healthcare Informatics focuses on providing auditing and reporting tools for healthcare compliance.

- 2022 February: PCIHIPAA refines its risk assessment tools to better address the evolving threat landscape.

- 2022 January: Inviscid Software develops more robust data loss prevention (DLP) features.

- 2021 December: HIPAAMATE introduces simplified workflows for policy updates and employee training.

- 2021 November: Accountable enhances its platform with features for continuous compliance monitoring.

- 2021 October: SecurityMetrics provides enhanced security audit services for healthcare organizations.

- 2021 September: HIPAA Survival Guide offers updated resources and guidance on navigating the latest HIPAA enforcement actions.

Future Outlook for HIPAA Compliance Software Market

The future outlook for the HIPAA Compliance Software Market is exceptionally promising, characterized by sustained and accelerated growth. The market is expected to be a significant growth engine within the broader cybersecurity and healthcare technology landscape. Key growth accelerators include the escalating adoption of cloud-native architectures, the pervasive integration of AI and machine learning for predictive compliance and threat mitigation, and the increasing demand for unified platforms that consolidate various compliance functions. As telehealth continues its expansion and the volume of digital health data explodes, the need for robust, scalable, and adaptable HIPAA compliance solutions will only intensify. Strategic opportunities lie in developing solutions that offer greater automation, seamless interoperability with evolving healthcare IT ecosystems, and advanced analytics capabilities for proactive risk management. Vendors that can effectively address the evolving regulatory landscape and provide intuitive, cost-effective, and comprehensive compliance management will be best positioned for success in this dynamic and critical market.

HIPAA Compliance Software Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Research Institute

-

2. Types

- 2.1. Cloud-Based

- 2.2. On-Premises

HIPAA Compliance Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

HIPAA Compliance Software Regional Market Share

Geographic Coverage of HIPAA Compliance Software

HIPAA Compliance Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Research Institute

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud-Based

- 5.2.2. On-Premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Research Institute

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud-Based

- 6.2.2. On-Premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Research Institute

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud-Based

- 7.2.2. On-Premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Research Institute

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud-Based

- 8.2.2. On-Premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Research Institute

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud-Based

- 9.2.2. On-Premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific HIPAA Compliance Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Research Institute

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud-Based

- 10.2.2. On-Premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Ostendio

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Congruity 360

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 DriveStrike

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 LifeOmic

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Azalea Health

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SecPod Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Vicarius

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Zenefits

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MedTrainer

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 EMS Healthcare Informatics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 HIPAA One

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Hushmail

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Progress Software

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 PCIHIPAA

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Inviscid Software

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Virtru

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 HIPAAMATE

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Paubox

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 LogicManager

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Accountable

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 HIPAAtrek

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Promisec

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Abyde

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 SecurityMetrics

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 HIPAA Survival Guide

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.1 Ostendio

List of Figures

- Figure 1: Global HIPAA Compliance Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America HIPAA Compliance Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America HIPAA Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America HIPAA Compliance Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America HIPAA Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America HIPAA Compliance Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America HIPAA Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America HIPAA Compliance Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America HIPAA Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America HIPAA Compliance Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America HIPAA Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America HIPAA Compliance Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America HIPAA Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe HIPAA Compliance Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe HIPAA Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe HIPAA Compliance Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe HIPAA Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe HIPAA Compliance Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe HIPAA Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa HIPAA Compliance Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa HIPAA Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa HIPAA Compliance Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa HIPAA Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa HIPAA Compliance Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa HIPAA Compliance Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific HIPAA Compliance Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific HIPAA Compliance Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific HIPAA Compliance Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific HIPAA Compliance Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific HIPAA Compliance Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific HIPAA Compliance Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global HIPAA Compliance Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global HIPAA Compliance Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global HIPAA Compliance Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global HIPAA Compliance Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global HIPAA Compliance Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global HIPAA Compliance Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global HIPAA Compliance Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global HIPAA Compliance Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific HIPAA Compliance Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the HIPAA Compliance Software?

The projected CAGR is approximately 7.9%.

2. Which companies are prominent players in the HIPAA Compliance Software?

Key companies in the market include Ostendio, Congruity 360, DriveStrike, LifeOmic, Azalea Health, SecPod Technologies, Vicarius, Zenefits, MedTrainer, EMS Healthcare Informatics, HIPAA One, Hushmail, Progress Software, PCIHIPAA, Inviscid Software, Virtru, HIPAAMATE, Paubox, LogicManager, Accountable, HIPAAtrek, Promisec, Abyde, SecurityMetrics, HIPAA Survival Guide.

3. What are the main segments of the HIPAA Compliance Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "HIPAA Compliance Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the HIPAA Compliance Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the HIPAA Compliance Software?

To stay informed about further developments, trends, and reports in the HIPAA Compliance Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence