Key Insights

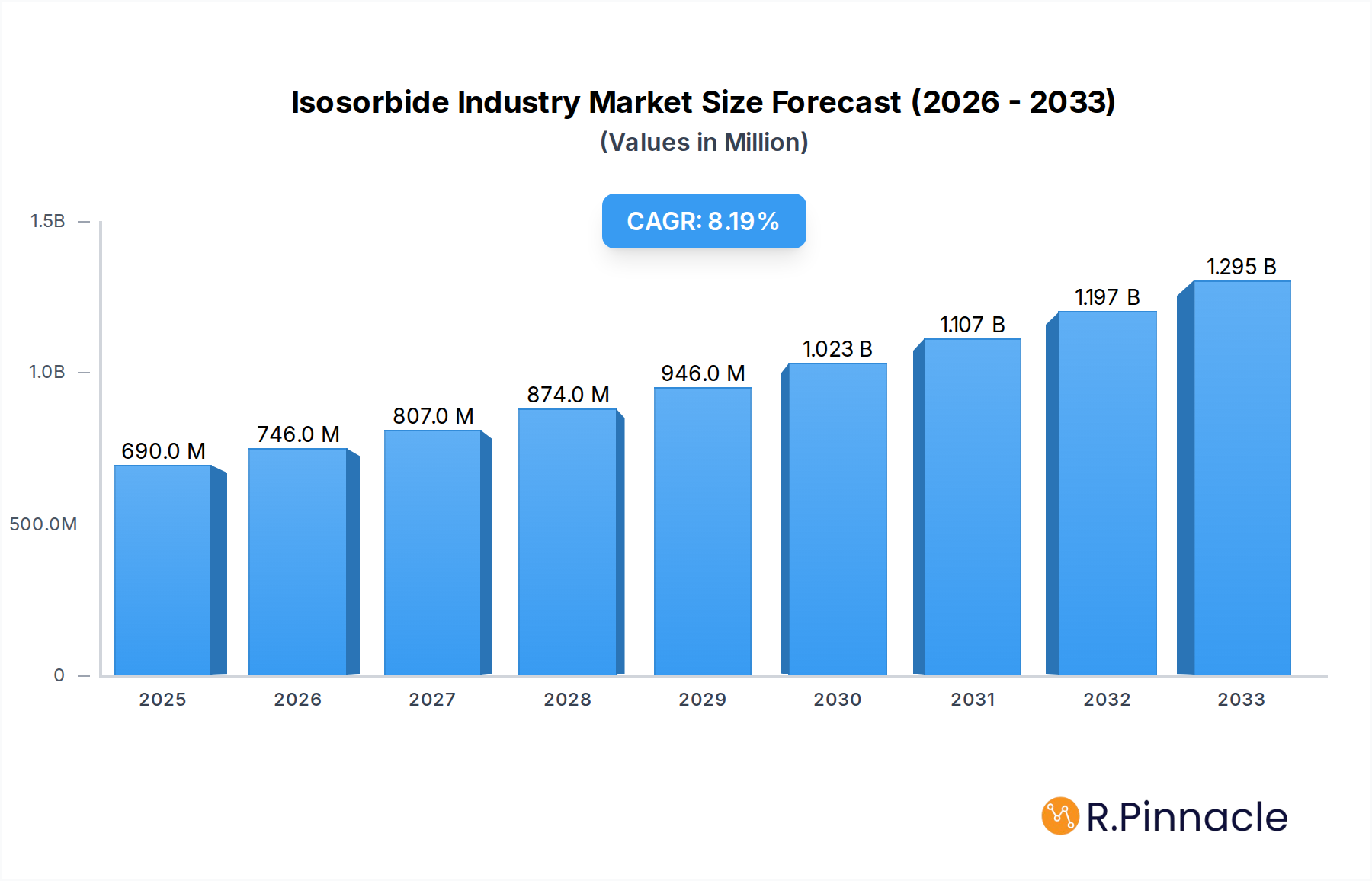

The global Isosorbide market is poised for significant expansion, projected to reach USD 690 million in 2025 with a robust Compound Annual Growth Rate (CAGR) of 8.03%. This impressive growth trajectory is fueled by a confluence of factors, primarily driven by the increasing demand for sustainable and bio-based materials across various industries. The growing environmental consciousness among consumers and stringent government regulations promoting the use of eco-friendly alternatives are key catalysts. The versatility of isosorbide, a furan-based diol derived from renewable resources, allows for its integration into a wide array of applications. Key growth drivers include its extensive use in the production of high-performance polymers such as Polyethylene Isosorbide Terephthalate (PEIT), Polycarbonate, and various polyesters. These materials offer enhanced properties like improved thermal stability, mechanical strength, and biodegradability, making them attractive substitutes for petroleum-based plastics. Furthermore, the pharmaceutical sector's increasing reliance on isosorbide for drug delivery systems and as a chiral building block contributes significantly to market dynamism. The expanding polymer and resin industry, coupled with the rising adoption of isosorbide as an additive to enhance material performance, further solidifies its market position.

Isosorbide Industry Market Size (In Million)

The market's expansion is not without its challenges, with certain restraints potentially moderating its growth. High production costs associated with bio-based chemical manufacturing, coupled with the availability of established and cost-effective petroleum-based alternatives, can pose significant hurdles. However, ongoing research and development efforts aimed at optimizing production processes and reducing costs are expected to mitigate these limitations. Emerging trends like the development of novel isosorbide derivatives with tailored properties and the increasing exploration of its potential in advanced materials and composites are creating new avenues for growth. Geographically, the Asia Pacific region, led by China and India, is expected to dominate the market due to its large manufacturing base and growing adoption of sustainable practices. North America and Europe are also significant contributors, driven by strong regulatory frameworks and consumer demand for eco-friendly products. The competitive landscape features prominent players like ADM, Ecogreen Oleochemicals GmbH, and Mitsubishi Chemical Corporation, who are actively engaged in expanding their production capacities and product portfolios to cater to the burgeoning global demand for isosorbide.

Isosorbide Industry Company Market Share

This in-depth report provides a detailed analysis of the global Isosorbide industry, covering market structure, dynamics, key players, and future outlook. Spanning the study period from 2019 to 2033, with a base year of 2025, this report offers invaluable insights for industry professionals seeking to understand market trends, growth drivers, and competitive landscapes. We delve into critical segments including applications like Polyethylene Isosorbide Terephthalate (PEIT), Polycarbonate, Polyurethane, Polyesters Isosobide Succinate, Isosorbide Diesters, and Other Applications, as well as end-user industries such as Polymers and Resins, Additives, Pharmaceuticals, and Other End-user Industries.

Isosorbide Industry Market Structure & Innovation Trends

The isosorbide market exhibits a moderate concentration, with key players like ADM, Ecogreen Oleochemicals GmbH, and Mitsubishi Chemical Corporation holding significant market shares. Innovation is largely driven by the demand for sustainable and bio-based alternatives in the polymers and resins sector, particularly for applications like PEIT and bio-based polyurethanes. Regulatory frameworks promoting the use of renewable materials are also acting as a significant innovation catalyst. The threat of product substitutes, while present from traditional petroleum-based chemicals, is gradually diminishing due to the enhanced performance and environmental benefits of isosorbide derivatives. End-user demographics are shifting towards industries prioritizing sustainability and reduced carbon footprints. Mergers and acquisitions (M&A) activity, while not extensive, have been strategic, focusing on expanding production capacity and vertical integration. For instance, strategic acquisitions aimed at securing feedstock or enhancing downstream processing capabilities are projected to see an increase, with estimated deal values reaching hundreds of millions of dollars. The market share of leading manufacturers is anticipated to consolidate further as companies invest in R&D and production scale.

Isosorbide Industry Market Dynamics & Trends

The global isosorbide market is poised for substantial growth, driven by an increasing demand for bio-based and sustainable materials across various industries. The projected Compound Annual Growth Rate (CAGR) for the forecast period 2025–2033 is estimated to be between 8% and 10%, indicating a robust expansion trajectory. Key growth drivers include the rising environmental consciousness among consumers and governments, leading to stricter regulations on petrochemical-based products and a greater impetus for the adoption of renewable alternatives. Technological advancements in isosorbide production and its downstream processing are continuously improving efficiency and reducing costs, making it a more economically viable option. Consumer preferences are increasingly tilting towards products with a lower environmental impact, thereby boosting the demand for isosorbide-based materials in packaging, textiles, and automotive components. Competitive dynamics are intensifying as established chemical giants and emerging bio-based material companies vie for market share. Market penetration of isosorbide derivatives is expected to accelerate, especially in regions with strong governmental support for green initiatives. Innovations in catalysis and polymerization techniques are enhancing the performance characteristics of isosorbide-based polymers, making them competitive with traditional materials. The growing emphasis on circular economy principles further fuels the adoption of bio-derived building blocks like isosorbide, promising sustained market expansion. The integration of isosorbide into a wider range of high-performance applications, such as advanced composites and specialty polycarbonates, will be a significant trend.

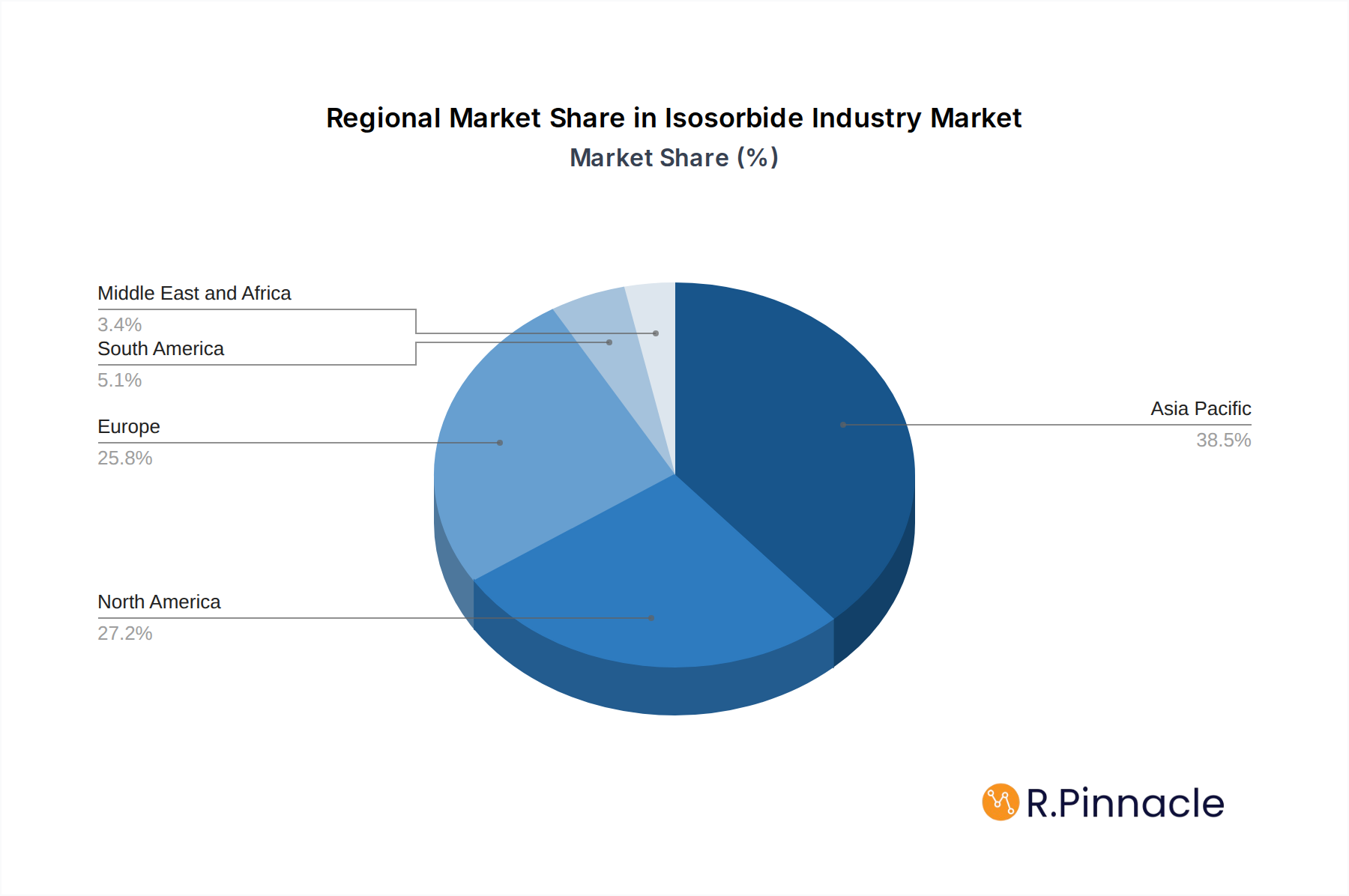

Dominant Regions & Segments in Isosorbide Industry

North America and Europe currently dominate the isosorbide market, largely due to stringent environmental regulations, strong consumer demand for sustainable products, and well-established research and development infrastructure. The United States and Germany are at the forefront, benefiting from supportive government policies that incentivize the use of bio-based chemicals and significant investments in green technologies. Asia-Pacific, particularly China and India, represents a rapidly growing region, driven by increasing industrialization, a large manufacturing base, and a burgeoning middle class with a growing awareness of environmental issues.

Application Dominance:

- Polyethylene Isosorbide Terephthalate (PEIT): This segment is a major growth engine due to its versatility as a PET alternative in packaging, films, and fibers, offering improved properties like enhanced barrier resistance and biodegradability. The demand is driven by the food and beverage industry's push for sustainable packaging solutions.

- Polyurethane: The use of isosorbide in bio-based polyurethanes for applications in foams, coatings, and adhesives is gaining significant traction, appealing to industries seeking to reduce their reliance on petroleum-derived isocyanates. Key drivers include the automotive and construction sectors' focus on sustainability.

- Polyesters Isosobide Succinate: This segment is crucial for its use in biodegradable plastics and as a plasticizer. Growth is propelled by the increasing demand for compostable materials in agricultural films and single-use plastics.

- Other Applications: This includes niche uses in pharmaceuticals, personal care products, and as a building block for novel bio-polymers, demonstrating the wide-ranging potential of isosorbide.

End-user Industry Dominance:

- Polymers and Resins: This segment is the largest consumer of isosorbide, with extensive use in the production of bio-plastics and advanced polymer materials. The push for sustainability in the packaging, textile, and automotive industries directly fuels this demand.

- Pharmaceuticals: Isosorbide derivatives are utilized in pharmaceutical formulations, acting as excipients or active ingredients. The growing global healthcare sector and the demand for safer, more bio-compatible materials support this segment.

- Additives: Isosorbide is finding applications as a functional additive in various materials, enhancing properties such as UV resistance and flame retardancy.

Isosorbide Industry Product Innovations

Recent product innovations in the isosorbide industry focus on developing high-performance bio-based polymers with properties that rival or surpass their petrochemical counterparts. Advancements in polymerization techniques have enabled the creation of isosorbide-based polycarbonates and polyesters with superior thermal stability, mechanical strength, and optical clarity. These new materials are finding applications in demanding sectors like electronics, automotive interiors, and medical devices, offering a sustainable alternative without compromising on performance. Competitive advantages stem from the inherent biodegradability and reduced carbon footprint of isosorbide derivatives, appealing to environmentally conscious manufacturers and consumers.

Report Scope & Segmentation Analysis

This report comprehensively segments the isosorbide market by application and end-user industry. The Application segments include Polyethylene Isosorbide Terephthalate (PEIT), Polycarbonate, Polyurethane, Polyesters Isosobide Succinate, Isosorbide Diesters, and Other Applications. PEIT is projected to exhibit a market size of over ten billion dollars by 2033, driven by its widespread use in packaging. The End-user Industry segments encompass Polymers and Resins, Additives, Pharmaceuticals, and Other End-user Industries. The Polymers and Resins segment is expected to dominate, with a projected market size exceeding fifteen billion dollars by 2033, fueled by the increasing adoption of bio-plastics. Each segment's growth projections and market sizes are detailed, alongside an analysis of competitive dynamics within them.

Key Drivers of Isosorbide Industry Growth

The isosorbide industry's growth is propelled by a confluence of factors. Technologically, advancements in bio-refining processes and catalytic conversion methods are improving production efficiency and cost-effectiveness. Economically, the increasing price volatility and environmental concerns associated with fossil fuels are making bio-based alternatives like isosorbide more attractive. Regulatory factors, including government incentives for renewable energy and mandates for sustainable product sourcing, are crucial drivers. For instance, policies promoting the use of bio-plastics in single-use packaging directly stimulate demand for isosorbide.

Challenges in the Isosorbide Industry Sector

Despite the positive growth trajectory, the isosorbide industry faces several challenges. High initial production costs compared to established petrochemicals can be a barrier to widespread adoption, although these are decreasing. Supply chain complexities in sourcing biomass feedstocks and ensuring consistent quality can impact production volumes. Intense competition from existing petroleum-based materials and the need for further research and development to enhance specific performance characteristics in niche applications also pose hurdles. Regulatory hurdles in certain regions and the need for greater consumer awareness and acceptance of bio-based products can also slow market penetration.

Emerging Opportunities in Isosorbide Industry

Emerging opportunities in the isosorbide industry are abundant, particularly in the development of novel bio-polymers and advanced materials. The growing trend towards a circular economy presents a significant avenue for isosorbide-based products with enhanced recyclability or biodegradability. New market applications in areas like advanced composites for aerospace and lightweight automotive components are opening up. Furthermore, consumer preferences for natural and sustainable ingredients in cosmetics and personal care products offer expansion potential. Technological advancements in areas like chemical recycling of isosorbide-based plastics could unlock further value.

Leading Players in the Isosorbide Industry Market

- ADM

- Ecogreen Oleochemicals GmbH

- Mitsubishi Chemical Corporation

- Par Pharmaceutical

- J&K Scientific Ltd

- TCI Chemicals (India) Pvt Ltd

- Roquette Frères

- Novaphene

- Thermo Fisher Scientific India Pvt Ltd

- J P Laboratories Pvt Ltd

- Jinan Hongbaifeng Industry & Trade Co Ltd

Key Developments in Isosorbide Industry Industry

- 2023: Launch of new bio-based polyurethane formulations for furniture and automotive interiors by leading manufacturers, responding to increasing demand for sustainable materials.

- 2022: Significant investment in research and development for enhanced biodegradability of isosorbide-based packaging films, aiming to address plastic waste concerns.

- 2021: Expansion of production capacity for isosorbide derivatives by several key players to meet growing market demand, with some expansions exceeding hundreds of millions of dollars.

- 2020: Introduction of novel isosorbide-based plasticizers offering improved performance and environmental profiles for PVC applications.

- 2019: Increased focus on strategic partnerships and collaborations to accelerate the development and commercialization of isosorbide applications in niche markets.

Future Outlook for Isosorbide Industry Market

The future outlook for the isosorbide industry is exceptionally bright, characterized by sustained growth and expanding market penetration. The increasing global commitment to sustainability, coupled with favorable regulatory landscapes and ongoing technological innovation, will act as significant growth accelerators. The development of new, high-performance isosorbide-based materials will unlock opportunities in advanced applications, driving market value beyond an estimated twenty billion dollars by 2033. Strategic investments in R&D, capacity expansion, and market penetration will be key for companies aiming to capitalize on the burgeoning demand for bio-based and eco-friendly chemical solutions.

Isosorbide Industry Segmentation

-

1. Application

- 1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 1.2. Polycarbonate

- 1.3. Polyurethane

- 1.4. Polyesters Isosobide Succinate

- 1.5. Isosorbide Diesters

- 1.6. Other Applications

-

2. End-user Industry

- 2.1. Polymers and Resins

- 2.2. Additives

- 2.3. Pharmaceuticals

- 2.4. Other End-user Industries

Isosorbide Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Isosorbide Industry Regional Market Share

Geographic Coverage of Isosorbide Industry

Isosorbide Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.03% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 5.1.2. Polycarbonate

- 5.1.3. Polyurethane

- 5.1.4. Polyesters Isosobide Succinate

- 5.1.5. Isosorbide Diesters

- 5.1.6. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Polymers and Resins

- 5.2.2. Additives

- 5.2.3. Pharmaceuticals

- 5.2.4. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Isosorbide Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 6.1.2. Polycarbonate

- 6.1.3. Polyurethane

- 6.1.4. Polyesters Isosobide Succinate

- 6.1.5. Isosorbide Diesters

- 6.1.6. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Polymers and Resins

- 6.2.2. Additives

- 6.2.3. Pharmaceuticals

- 6.2.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Asia Pacific Isosorbide Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 7.1.2. Polycarbonate

- 7.1.3. Polyurethane

- 7.1.4. Polyesters Isosobide Succinate

- 7.1.5. Isosorbide Diesters

- 7.1.6. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Polymers and Resins

- 7.2.2. Additives

- 7.2.3. Pharmaceuticals

- 7.2.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. North America Isosorbide Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 8.1.2. Polycarbonate

- 8.1.3. Polyurethane

- 8.1.4. Polyesters Isosobide Succinate

- 8.1.5. Isosorbide Diesters

- 8.1.6. Other Applications

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Polymers and Resins

- 8.2.2. Additives

- 8.2.3. Pharmaceuticals

- 8.2.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Isosorbide Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 9.1.2. Polycarbonate

- 9.1.3. Polyurethane

- 9.1.4. Polyesters Isosobide Succinate

- 9.1.5. Isosorbide Diesters

- 9.1.6. Other Applications

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Polymers and Resins

- 9.2.2. Additives

- 9.2.3. Pharmaceuticals

- 9.2.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. South America Isosorbide Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 10.1.2. Polycarbonate

- 10.1.3. Polyurethane

- 10.1.4. Polyesters Isosobide Succinate

- 10.1.5. Isosorbide Diesters

- 10.1.6. Other Applications

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Polymers and Resins

- 10.2.2. Additives

- 10.2.3. Pharmaceuticals

- 10.2.4. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East and Africa Isosorbide Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Polyethylene Isosorbide Terephthalate (PEIT)

- 11.1.2. Polycarbonate

- 11.1.3. Polyurethane

- 11.1.4. Polyesters Isosobide Succinate

- 11.1.5. Isosorbide Diesters

- 11.1.6. Other Applications

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Polymers and Resins

- 11.2.2. Additives

- 11.2.3. Pharmaceuticals

- 11.2.4. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ADM

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ecogreen Oleochemicals GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mitsubishi Chemical Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Par Pharmaceutical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 J&K Scientific Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TCI Chemicals (India) Pvt Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Roquette Frères

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Novaphene

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Thermo Fisher Scientific India Pvt Ltd *List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 J P Laboratories Pvt Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Jinan Hongbaifeng Industry & Trade Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 ADM

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Isosorbide Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Isosorbide Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: Asia Pacific Isosorbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: Asia Pacific Isosorbide Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Isosorbide Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Isosorbide Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Isosorbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Isosorbide Industry Revenue (billion), by Application 2025 & 2033

- Figure 9: North America Isosorbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Isosorbide Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Isosorbide Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Isosorbide Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Isosorbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Isosorbide Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Isosorbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Isosorbide Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Isosorbide Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Isosorbide Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Isosorbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Isosorbide Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: South America Isosorbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: South America Isosorbide Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: South America Isosorbide Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: South America Isosorbide Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Isosorbide Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Isosorbide Industry Revenue (billion), by Application 2025 & 2033

- Figure 27: Middle East and Africa Isosorbide Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Middle East and Africa Isosorbide Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Isosorbide Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Isosorbide Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Isosorbide Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Isosorbide Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Isosorbide Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 13: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Isosorbide Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Isosorbide Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 27: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Isosorbide Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Isosorbide Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global Isosorbide Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Isosorbide Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Isosorbide Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Isosorbide Industry?

The projected CAGR is approximately 8.03%.

2. Which companies are prominent players in the Isosorbide Industry?

Key companies in the market include ADM, Ecogreen Oleochemicals GmbH, Mitsubishi Chemical Corporation, Par Pharmaceutical, J&K Scientific Ltd, TCI Chemicals (India) Pvt Ltd, Roquette Frères, Novaphene, Thermo Fisher Scientific India Pvt Ltd *List Not Exhaustive, J P Laboratories Pvt Ltd, Jinan Hongbaifeng Industry & Trade Co Ltd.

3. What are the main segments of the Isosorbide Industry?

The market segments include Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.69 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Trend of Bio-based Products; Increasing Demand from Pharmaceutical Sector.

6. What are the notable trends driving market growth?

Increasing Demand from the Polymer and Resins Segment.

7. Are there any restraints impacting market growth?

; Side Effects of Isosorbide Derivatives on Health; Unfavorable Conditions Arising due to COVID-19 Outbreak.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Isosorbide Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Isosorbide Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Isosorbide Industry?

To stay informed about further developments, trends, and reports in the Isosorbide Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence