Key Insights

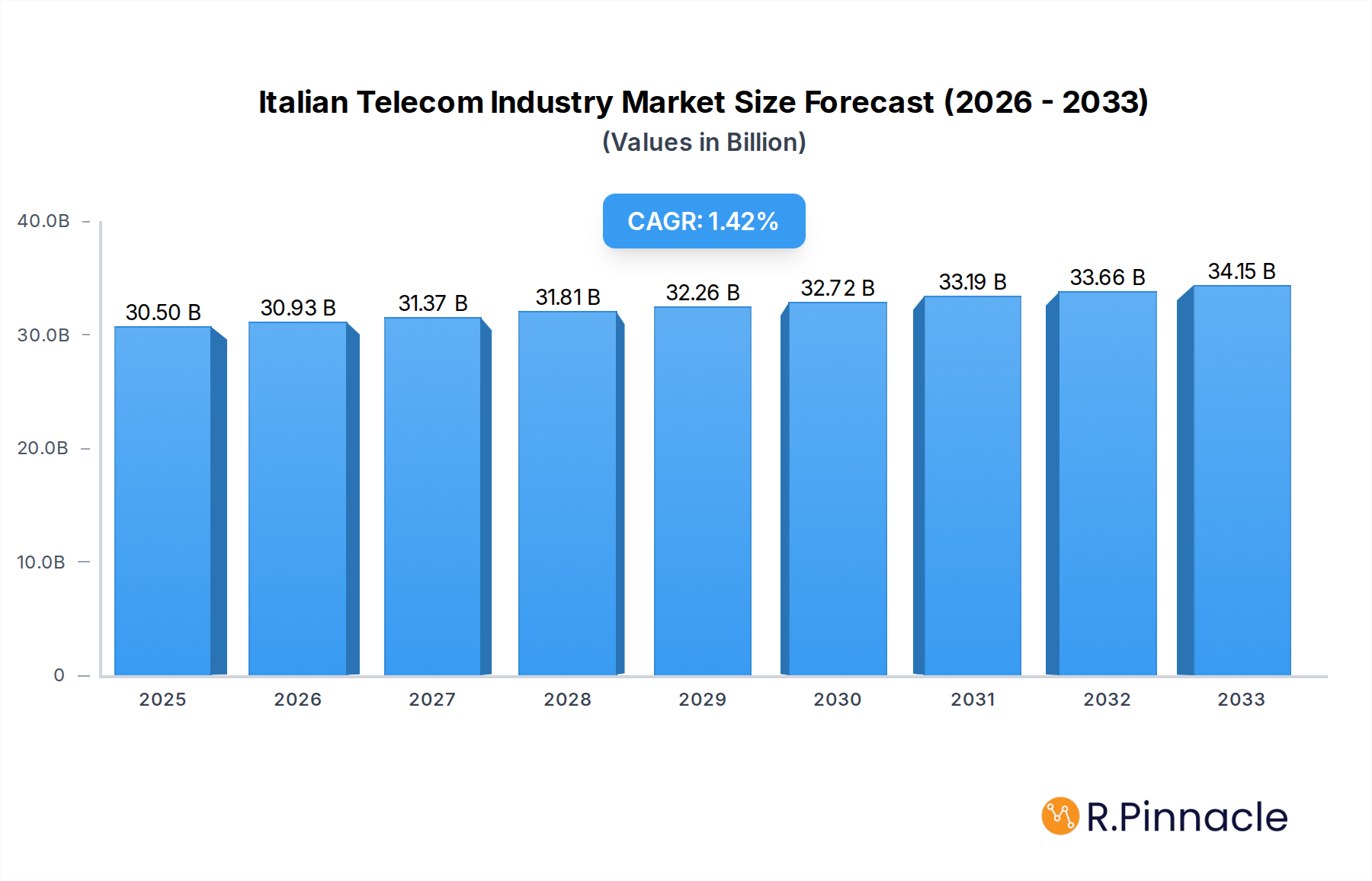

The Italian telecommunications industry is poised for steady growth, with a projected market size of $30.5 billion in 2025, expanding at a Compound Annual Growth Rate (CAGR) of 1.4% through 2033. This modest but consistent expansion is underpinned by several key drivers, including the ongoing digital transformation across various sectors, increasing demand for high-speed data services, and the continued evolution of Over-The-Top (OTT) and Pay TV offerings. The penetration of smartphones and the growing reliance on digital communication and entertainment platforms are further bolstering market growth. Major players like TIM, Vodafone, and Iliad Italia are actively investing in network infrastructure, particularly 5G deployment, which is crucial for enabling advanced services and supporting the ever-increasing data traffic. The competitive landscape is dynamic, with established operators and new entrants vying for market share, driving innovation and service diversification.

Italian Telecom Industry Market Size (In Billion)

Despite the positive outlook, the market faces certain restraints that may temper its growth trajectory. These include the high cost of 5G spectrum acquisition and infrastructure rollout, coupled with the need for significant capital expenditure. Regulatory hurdles and the complex licensing processes in Italy can also present challenges for new market entrants and existing players looking to expand. Furthermore, the increasing commoditization of basic voice and data services leads to price pressures, impacting revenue streams. However, the shift towards value-added services, such as cloud solutions, IoT connectivity, and enhanced cybersecurity offerings, is expected to mitigate these challenges. The robust growth in data consumption, fueled by video streaming, online gaming, and the proliferation of connected devices, remains a significant opportunity for the Italian telecom sector to explore and capitalize on.

Italian Telecom Industry Company Market Share

Unlock critical insights into the Italian telecom industry with this comprehensive report. Delve into market structure, dynamics, leading players, and future trends shaping the Italian telecommunications market. Featuring analysis of Voice Services (Wired, Wireless), Data Services, and OTT and PayTV Services, this report provides actionable intelligence for industry professionals. Covering the study period 2019–2033, with a base year of 2025, it offers in-depth analysis of market concentration, innovation, regulatory frameworks, and M&A activities, with M&A deal values estimated in billions. Explore technological disruptions, consumer preferences, and competitive dynamics, including market penetration metrics and a projected CAGR. Identify dominant regions and segments, supported by key drivers like economic policies and infrastructure development. Discover product innovations and their competitive advantages, alongside detailed segmentation analysis with market size projections. Understand key growth drivers, including technological advancements and regulatory factors, and confront challenges such as supply chain issues and competitive pressures. Uncover emerging opportunities in new markets and technologies, and gain a deep understanding of the leading Italian telecom companies including TIM, Vodafone, Iliad Italia, Fastweb, Wind Tre, Cellnex, INWIT, Telecom Italia Sparkle, Sielte SPA, Huawei Technologies Italia SRL, Tiscali, and Ericsson. Analyze pivotal Italian telecom industry developments such as Fastweb's 5G upgrade, TIM's 3G network switch-off, and the Iliad Italy-Fastweb FTTH expansion, and prepare for the future outlook with strategic insights into market potential.

Italian Telecom Industry Market Structure & Innovation Trends

The Italian telecom industry exhibits a dynamic market structure characterized by a mix of established giants and agile challengers, influencing innovation drivers and regulatory frameworks. Market concentration is evident, with a few key players holding significant market share, estimated to be over 70% for the top three operators in terms of revenue. Innovation is largely driven by the relentless pursuit of next-generation network capabilities, particularly 5G deployment and fiber-to-the-home (FTTH) expansion, pushing technological boundaries and creating new service offerings. Regulatory frameworks, overseen by bodies like AGCOM, play a crucial role in shaping competition and ensuring fair market access, impacting aspects like spectrum allocation and infrastructure sharing. Product substitutes are increasingly prevalent, especially with the rise of Over-The-Top (OTT) services impacting traditional voice and messaging revenues. End-user demographics are shifting towards a younger, digitally native population demanding high-speed data and seamless connectivity, influencing service development and marketing strategies. Mergers and acquisitions (M&A) activities are a constant feature, driven by the need for consolidation, scale, and strategic positioning. Recent M&A deal values are estimated to be in the billions, reflecting the strategic importance and investment appetite within the sector.

- Market Share Dynamics: Top operators command substantial market share, driving investment in network upgrades and service diversification.

- Innovation Ecosystem: Driven by 5G, fiber, and AI integration, fostering new service models.

- Regulatory Landscape: AGCOM influences competition, spectrum, and infrastructure access, with policy shifts impacting market entry and expansion.

- Product Substitutes: Proliferation of OTT services challenges traditional telco revenue streams, emphasizing the need for new value propositions.

- End-User Demographics: Growing demand for high-speed data, mobile services, and integrated digital experiences.

- M&A Activities: Ongoing consolidation and strategic partnerships valued in the billions to enhance market position and technological capabilities.

Italian Telecom Industry Market Dynamics & Trends

The Italian telecom industry is experiencing robust growth, propelled by a confluence of market growth drivers, significant technological disruptions, evolving consumer preferences, and intense competitive dynamics. The widespread adoption of high-speed broadband and the ongoing rollout of 5G networks are foundational to this expansion, enabling a richer digital ecosystem. The increasing demand for data-intensive services, fueled by video streaming, cloud computing, and the burgeoning Internet of Things (IoT) sector, acts as a primary growth catalyst. Technological disruptions, such as advancements in network virtualization, artificial intelligence for network management, and the increasing integration of fiber optics, are fundamentally reshaping the infrastructure and service delivery models. This leads to enhanced efficiency, lower operational costs, and the ability to offer more sophisticated and personalized services.

Consumer preferences are rapidly evolving, with Italian users increasingly prioritizing speed, reliability, and value for money. There is a growing expectation for seamless connectivity across multiple devices and a demand for bundled services that encompass mobile, broadband, and entertainment. The shift towards digital-first interactions and the increasing reliance on mobile devices for daily activities further underscore these evolving preferences. The competitive dynamics within the Italian telecom market are fierce, characterized by price wars, aggressive promotional campaigns, and a continuous race to upgrade network capabilities. Key players are investing heavily in network infrastructure and innovative service portfolios to capture market share and maintain customer loyalty. This intense competition, while benefiting consumers through improved services and competitive pricing, also necessitates strategic agility and significant capital expenditure from operators. The CAGR for the Italian telecom market is projected to be around 5-7% over the forecast period. Market penetration for mobile services is already high, exceeding 130%, while broadband penetration continues to rise, particularly with the expansion of FTTH. The adoption of 5G services is also gaining momentum, contributing to the overall growth trajectory of the sector. The industry's ability to adapt to these changing dynamics and leverage emerging technologies will be critical for sustained success.

Dominant Regions & Segments in Italian Telecom Industry

The Italian telecom industry is characterized by distinct regional strengths and segment dominance, driven by a complex interplay of economic policies, infrastructure development, and evolving consumer behaviors. Data Services currently represents the dominant segment, driven by an insatiable demand for high-speed internet access, mobile data consumption, and the growth of cloud-based applications. This dominance is underpinned by significant investments in fiber optic infrastructure and the rapid expansion of 5G networks across the country. Economic policies that promote digital transformation and incentivize infrastructure investment have been pivotal in fostering this growth. Furthermore, government initiatives aimed at bridging the digital divide, particularly in underserved rural areas, are expanding the reach and penetration of data services, contributing to a projected market size of over €20 billion for this segment by 2028.

Voice Services (Wired and Wireless), while historically the bedrock of the telecommunications industry, are undergoing a transformation. Wireless voice services continue to hold a substantial share, driven by widespread mobile adoption, but are increasingly intertwined with data bundles. Wired voice services are seeing a decline in traditional landline subscriptions, with a gradual shift towards IP-based voice solutions delivered over broadband networks. The market for these services, while mature, is expected to maintain a steady presence, with a market size estimated to be around €8 billion by 2028, largely sustained by enterprise solutions and bundled offerings.

OTT and PayTV Services represent a rapidly growing segment, directly benefiting from the enhanced data infrastructure. As consumers seek richer entertainment experiences, the demand for streaming services, on-demand content, and integrated PayTV solutions is surging. Telecom operators are increasingly partnering with content providers or launching their own OTT platforms to capture a share of this lucrative market. The synergy between broadband connectivity and digital content consumption is a key driver, propelling this segment's growth and a projected market size of over €15 billion by 2028.

- Dominance of Data Services:

- Key Drivers: Proliferation of smartphones, IoT adoption, cloud computing, and demand for high-speed internet.

- Infrastructure Development: Extensive fiber optic network expansion and rapid 5G deployment across urban and suburban areas.

- Economic Policies: Government incentives for digital infrastructure and broadband rollout, particularly in underserved regions.

- Consumer Behavior: Increasing reliance on online streaming, social media, and digital communication.

- Transformation of Voice Services:

- Wireless Voice: Strong penetration driven by mobile adoption, often bundled with data plans.

- Wired Voice: Gradual decline in traditional landlines, with a shift towards IP-based solutions over broadband.

- Enterprise Solutions: Continued demand for reliable voice communication from businesses.

- Growth of OTT and PayTV Services:

- Content Demand: Escalating consumer appetite for on-demand streaming, movies, series, and live sports.

- Bundling Strategies: Telecom operators integrating content offerings with internet and mobile packages to enhance value.

- Technological Synergy: Enhanced data speeds and network reliability enabling seamless streaming experiences.

Italian Telecom Industry Product Innovations

Product innovations in the Italian telecom industry are predominantly focused on enhancing network capabilities and delivering advanced digital services. The widespread deployment of 5G technology is a prime example, offering significantly higher speeds, lower latency, and increased capacity. This enables applications such as enhanced mobile broadband, mission-critical communications, and massive IoT deployments, creating new revenue streams for operators. Furthermore, the continued expansion of Fiber-to-the-Home (FTTH) networks is a critical innovation, providing consumers and businesses with ultra-fast and reliable internet connectivity, crucial for supporting bandwidth-intensive applications. Innovations in network virtualization and software-defined networking (SDN) are also transforming how networks are managed, offering greater flexibility, scalability, and efficiency. These advancements not only improve operational performance but also pave the way for the development of innovative digital services, including edge computing, enhanced cybersecurity solutions, and immersive entertainment experiences, providing a significant competitive advantage.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Italian telecom industry across its core service segments. The primary segmentation includes Voice Services (Wired, Wireless), examining the evolving landscape of traditional voice communication and its integration with digital platforms. Data Services forms another critical segment, encompassing mobile data, broadband internet, and the burgeoning IoT connectivity market, with strong growth projections driven by increasing data consumption. The OTT and PayTV Services segment captures the rapidly expanding market for streaming entertainment, on-demand content, and integrated television offerings, benefiting significantly from enhanced connectivity. Each segment's market size, growth projections, and competitive dynamics are thoroughly investigated to provide a granular understanding of the Italian telecom market's multifaceted nature.

Key Drivers of Italian Telecom Industry Growth

The growth of the Italian telecom industry is propelled by several interconnected factors. Technologically, the ongoing rollout and enhancement of 5G networks and the extensive expansion of Fiber-to-the-Home (FTTH) infrastructure are fundamental accelerators, enabling higher speeds, lower latency, and new service possibilities. Economically, government initiatives promoting digital transformation, coupled with increasing consumer and business demand for high-speed connectivity and digital services, are significant drivers. The digitalization of businesses, including the adoption of cloud computing and remote work solutions, further fuels demand for robust and reliable telecommunications. Regulatory support for infrastructure investment and competition also plays a crucial role in fostering a conducive environment for growth.

Challenges in the Italian Telecom Industry Sector

Despite robust growth, the Italian telecom industry faces significant challenges. Regulatory hurdles, including complex permitting processes for infrastructure deployment and spectrum allocation policies, can impede the pace of network expansion. Supply chain issues, exacerbated by global demand and geopolitical factors, can impact the availability and cost of essential network equipment, potentially delaying upgrades. Intense competitive pressures among operators lead to price wars and require substantial ongoing investment in network modernization and service innovation, impacting profitability. Furthermore, the substantial capital expenditure required for 5G and fiber deployment, coupled with a need to monetize these investments effectively, presents a continuous financial challenge.

Emerging Opportunities in Italian Telecom Industry

The Italian telecom industry is ripe with emerging opportunities. The continued build-out of 5G standalone networks will unlock new enterprise use cases, including private networks for industries, enhanced IoT applications, and immersive augmented and virtual reality experiences, estimated to create billions in new revenue. The government's push for digitalization and smart city initiatives presents significant opportunities for B2B and B2G services, focusing on connected infrastructure, public safety, and efficient resource management. The growing demand for over-the-top (OTT) content and digital entertainment provides telcos with avenues for content partnerships and service bundling. Furthermore, advancements in edge computing and AI-driven network optimization offer the potential for developing innovative, low-latency services and improving operational efficiency.

Leading Players in the Italian Telecom Industry Market

- TIM

- Vodafone

- Iliad Italia

- Fastweb

- Wind Tre

- Cellnex

- INWIT

- Telecom Italia Sparkle

- Sielte SPA

- Huawei Technologies Italia SRL

- Tiscali

- Ericsson

Key Developments in Italian Telecom Industry Industry

- October 2022: Fastweb upgraded its 5G network maximum download speed up to 1.6 Gbps. Through this development, the company can offer high-speed 5G services to customers.

- October 2022: Telecom Italia (TIM) switched off its 3G network. The company aims to offer future 4G and 5G services.

- October 2022: Iliad Italy signed an agreement with Fastweb. The company jointly works to expand its fiber-to-the-home (FTTH) service footprint. This project is expected to be completed by the end of 2025. The expanded fiber-to-the-home (FTTH) service is to cover more than ten million homes across Italy.

Future Outlook for Italian Telecom Industry Market

The future outlook for the Italian telecom industry is exceptionally promising, driven by sustained technological advancements and evolving market demands. The ongoing 5G rollout and densification will continue to be a major growth accelerator, enabling a new wave of innovative applications across consumer and enterprise sectors. The widespread adoption of fiber optic networks, particularly FTTH, will underpin this growth by providing the necessary high-bandwidth, low-latency connectivity. Strategic opportunities lie in monetizing these advanced networks through converged services, IoT solutions, and private network deployments for various industries. The increasing integration of artificial intelligence and machine learning in network management and customer service promises enhanced efficiency and personalized user experiences. The market's trajectory points towards a more connected, intelligent, and service-rich digital ecosystem, with significant revenue potential estimated in the billions.

Italian Telecom Industry Segmentation

-

1. Services

-

1.1. Voice Services

- 1.1.1. Wired

- 1.1.2. Wireless

- 1.2. Data and

- 1.3. OTT and PayTV Services

-

1.1. Voice Services

Italian Telecom Industry Segmentation By Geography

- 1. Italia

Italian Telecom Industry Regional Market Share

Geographic Coverage of Italian Telecom Industry

Italian Telecom Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Voice Services

- 5.1.1.1. Wired

- 5.1.1.2. Wireless

- 5.1.2. Data and

- 5.1.3. OTT and PayTV Services

- 5.1.1. Voice Services

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Italia

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Italian Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Voice Services

- 6.1.1.1. Wired

- 6.1.1.2. Wireless

- 6.1.2. Data and

- 6.1.3. OTT and PayTV Services

- 6.1.1. Voice Services

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sielte SPA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 INWIT

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Telecom Italia Sparkle

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Huawei Technologies Italia SRL

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Fastweb

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TIM

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Vodafone

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Tiscali*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wind Tre

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Cellnex

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ericsson

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Iliad Italia

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Sielte SPA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italian Telecom Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Italian Telecom Industry Share (%) by Company 2025

List of Tables

- Table 1: Italian Telecom Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 2: Italian Telecom Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Italian Telecom Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 4: Italian Telecom Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italian Telecom Industry?

The projected CAGR is approximately 1.4%.

2. Which companies are prominent players in the Italian Telecom Industry?

Key companies in the market include Sielte SPA, INWIT, Telecom Italia Sparkle, Huawei Technologies Italia SRL, Fastweb, TIM, Vodafone, Tiscali*List Not Exhaustive, Wind Tre, Cellnex, Ericsson, Iliad Italia.

3. What are the main segments of the Italian Telecom Industry?

The market segments include Services.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for 5G; Growth of IoT Usage in Telecom.

6. What are the notable trends driving market growth?

Rising Demand for Fixed Broadband Services.

7. Are there any restraints impacting market growth?

High Costs And Limited Commercialization.

8. Can you provide examples of recent developments in the market?

October 2022: Fastweb upgraded its 5G network maximum download speed up to 1.6 Gbps. Through this development, the company can offer high-speed 5G services to customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italian Telecom Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italian Telecom Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italian Telecom Industry?

To stay informed about further developments, trends, and reports in the Italian Telecom Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence