Key Insights

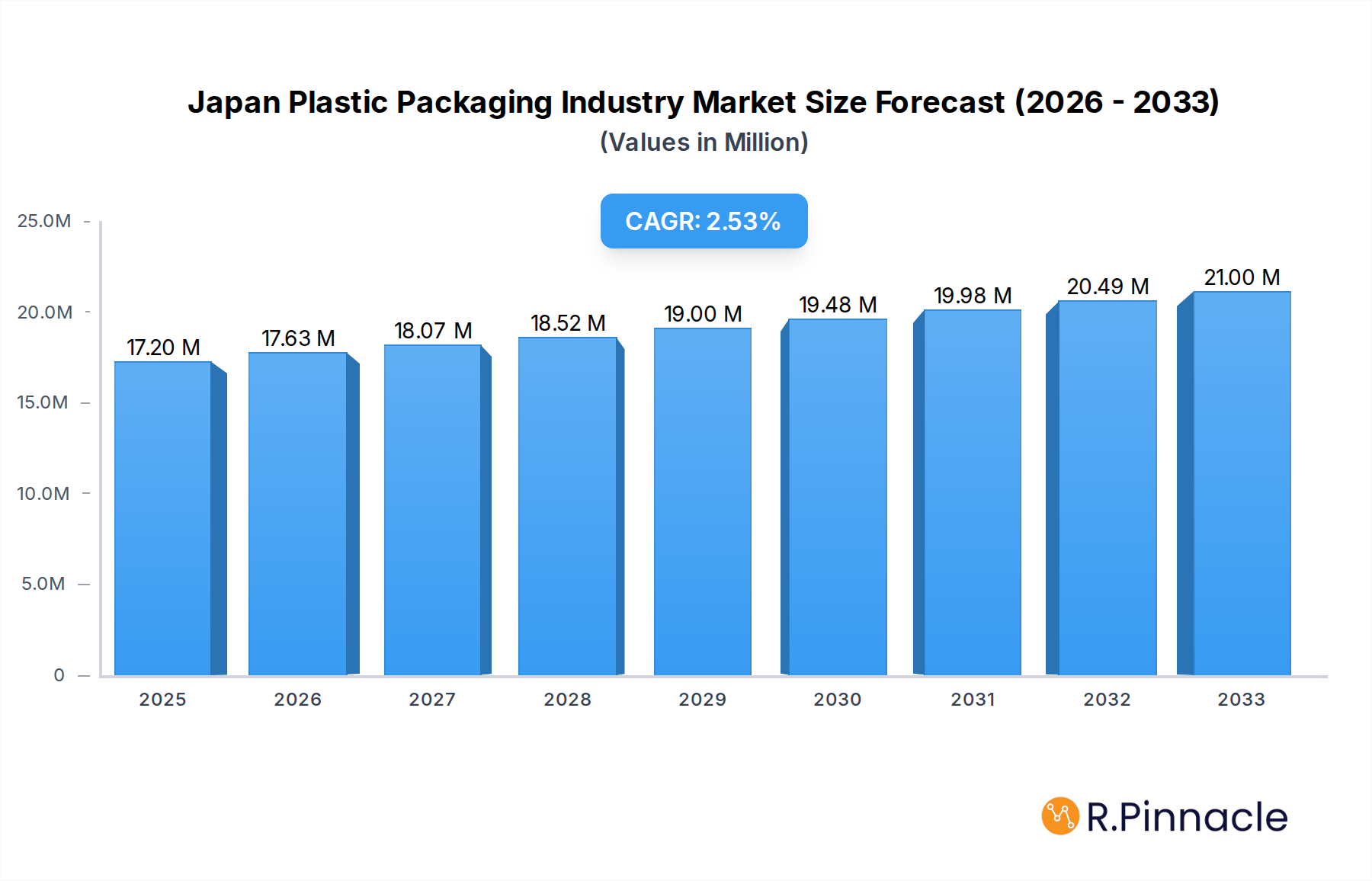

The Japan Plastic Packaging Industry is poised for steady growth, with a projected market size of $17.2 million in 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 2.53% through 2033. This expansion is primarily driven by the increasing demand for lightweight, durable, and cost-effective packaging solutions across various end-user verticals. The food and beverage sector continues to be a dominant force, fueled by consumer preferences for convenient, single-serving, and extended shelf-life products, necessitating advanced plastic packaging technologies. Furthermore, the healthcare industry's growing need for sterile, protective packaging for pharmaceuticals and medical devices, coupled with the personal care and household segments' focus on attractive and functional product presentation, will significantly contribute to market impetus. The ongoing emphasis on sustainable packaging solutions, including the development of recyclable and biodegradable plastics, will also play a crucial role in shaping market dynamics, encouraging innovation and investment.

Japan Plastic Packaging Industry Market Size (In Million)

Despite the positive outlook, the industry faces certain restraints. Increasing environmental regulations and a growing consumer consciousness regarding plastic waste pose significant challenges. The industry is responding by investing in research and development for eco-friendly alternatives and advanced recycling technologies. Flexible plastic packaging, particularly pouches and films, is expected to dominate due to its versatility and cost-effectiveness, while rigid packaging, such as bottles and jars, will maintain its importance in specific applications. Key players like Amcor Japan, Toyo Seikan Group Holding Ltd, and Rengo Co Ltd are actively innovating to meet evolving consumer demands and regulatory landscapes, focusing on improved functionality, aesthetics, and sustainability in their product offerings. The industry's resilience lies in its ability to adapt to these evolving demands and capitalize on emerging opportunities for innovative and environmentally responsible packaging solutions.

Japan Plastic Packaging Industry Company Market Share

Japan Plastic Packaging Industry Report: Comprehensive Market Analysis & Forecast (2019-2033)

Unlock critical insights into the dynamic Japan Plastic Packaging Industry with our in-depth market report. This comprehensive analysis, spanning from 2019 to 2033, provides strategic intelligence for industry professionals seeking to navigate growth drivers, emerging trends, and competitive landscapes. The report details market size and share projections for key segments including Flexible Plastic Packaging and Rigid Plastic Packaging, with further segmentation by Bottles and Jars, Trays and Containers, Pouches, Bags, Films and Wraps, and Other Product Types. We also delve into the crucial End-user Verticals: Food, Beverage, Healthcare, Personal Care and Household, and Other End-user Verticals. The base year for analysis is 2025, with projections extending through 2033, offering a robust forecast period built on historical data from 2019-2024.

Japan Plastic Packaging Industry Market Structure & Innovation Trends

The Japan Plastic Packaging Industry exhibits a moderately concentrated market structure, with leading players continually investing in innovation to maintain competitive advantages. Key innovation drivers include the pursuit of sustainable packaging solutions, enhanced barrier properties for extended product shelf-life, and lightweighting for reduced material usage and logistics costs. Regulatory frameworks, particularly those focusing on environmental impact and recycling, significantly influence product development and manufacturing processes. The threat of product substitutes, such as paper-based packaging or glass, is managed through continuous technological advancements in plastic materials and design. End-user demographics are evolving, with increasing demand for convenience, on-the-go options, and visually appealing packaging across all verticals. Mergers and acquisitions (M&A) activity, while present, is strategically focused on acquiring advanced manufacturing capabilities or expanding market reach. For instance, a significant M&A event involved Graham Partners' acquisition of Berry Global Group Inc. in December 2020, integrating it with their flexible packaging portfolio company. This strategic move underscores the industry's emphasis on consolidating expertise and technological prowess to address evolving market needs. M&A deal values are expected to reflect the strategic importance of acquiring companies with advanced manufacturing technologies and established market presence within the Japanese context, potentially reaching hundreds of millions.

Japan Plastic Packaging Industry Market Dynamics & Trends

The Japan Plastic Packaging Industry is propelled by a confluence of robust growth drivers, technological disruptions, evolving consumer preferences, and intense competitive dynamics, painting a vibrant picture of market evolution. A primary growth catalyst is the burgeoning demand from the Food and Beverage sectors, driven by an aging population, increasing single-person households, and a rising interest in premium and convenience food products. This translates to a sustained demand for versatile packaging formats like Pouches, Bags, and innovative Bottles and Jars designed for portion control and extended shelf-life. The Healthcare sector also presents a significant growth avenue, fueled by an increase in medical advancements, the growing demand for pharmaceuticals, and the need for sterile and protective packaging solutions. The Personal Care and Household segment continues its upward trajectory, with consumers seeking aesthetically pleasing, functional, and increasingly sustainable packaging.

Technological advancements are profoundly reshaping the industry. The widespread adoption of advanced extrusion and injection molding techniques allows for the production of highly customized and functional packaging. Innovations in material science are leading to the development of high-barrier films and wraps that significantly extend product shelf life, reducing food waste and enhancing product integrity. Furthermore, the industry is witnessing a strong push towards circular economy principles, with significant investments in research and development for biodegradable, compostable, and recycled plastic materials. The market penetration of these sustainable solutions, while still growing, is a key trend indicating a shift in manufacturing priorities.

Consumer preferences are increasingly leaning towards convenience, functionality, and sustainability. The demand for lightweight, easy-to-open, and resealable packaging is paramount, particularly within the Food and Personal Care segments. Consumers are also becoming more environmentally conscious, actively seeking products packaged in recyclable or reduced plastic materials, influencing brand choices and driving innovation in eco-friendly packaging. This consumer-led demand is a powerful force encouraging manufacturers to invest in sustainable alternatives and transparent labeling.

The competitive landscape is characterized by a mix of large, established players and agile niche manufacturers. Companies are strategically investing in capacity expansion, technological upgrades, and product diversification to capture market share. Partnerships and collaborations are becoming increasingly common as companies seek to leverage each other's expertise in areas such as material innovation, recycling technologies, and market access. The projected Compound Annual Growth Rate (CAGR) for the Japan Plastic Packaging Industry is estimated to be between 3.5% and 4.5% over the forecast period, reflecting a steady and sustainable expansion driven by these interconnected factors. The market penetration of advanced and sustainable packaging solutions is expected to grow significantly, potentially reaching over 60% for certain product categories by 2033.

Dominant Regions & Segments in Japan Plastic Packaging Industry

The Kanto region, encompassing Tokyo and its surrounding prefectures, stands as the dominant geographical hub within the Japan Plastic Packaging Industry. This dominance is attributed to its high population density, robust economic activity, and the concentration of major end-user industries, including Food, Beverage, Healthcare, and Personal Care and Household. The region benefits from superior logistical infrastructure, access to a skilled workforce, and a vibrant ecosystem of research and development institutions, fostering innovation and early adoption of new packaging technologies. Economic policies within the Kanto region often support advanced manufacturing and export-oriented businesses, further bolstering the plastic packaging sector.

Within the packaging types, Flexible Plastic Packaging commands a significant share, driven by its versatility, cost-effectiveness, and suitability for a wide range of applications. This segment is further propelled by the growing demand for Pouches and Bags, especially in the Food industry for snacks, ready-to-eat meals, and confectionery, as well as in the Personal Care and Household sector for detergents and cleaning supplies. The lightweight nature of flexible packaging also aligns with sustainability goals by reducing material usage and transportation emissions.

In terms of product types, Films and Wraps are a cornerstone of the industry, serving critical functions in product protection, preservation, and branding across virtually all end-user verticals. The Food and Beverage sectors are major consumers, utilizing films for sealing trays, wrapping produce, and creating innovative pouch designs. Bottles and Jars, particularly those made from PET and HDPE, continue to be essential for liquid products in the Beverage and Personal Care markets. The increasing preference for lightweight, shatter-resistant, and convenient dispensing solutions ensures their sustained relevance.

The Food vertical is unequivocally the largest end-user segment for Japan's plastic packaging. This is driven by the sheer volume of packaged food products consumed domestically and for export. The demand spans from fresh produce and processed foods to beverages and dairy products, all requiring specialized packaging solutions to ensure safety, freshness, and extended shelf-life. The Beverage sector is another substantial contributor, with a strong demand for bottles, cans, and flexible packaging for water, soft drinks, alcoholic beverages, and juices.

Key drivers underpinning the dominance of these segments include:

- Economic Policies: Government initiatives promoting domestic manufacturing, export growth, and sustainable practices directly benefit the plastic packaging industry.

- Infrastructure: Advanced logistics networks, including efficient transportation and warehousing facilities, are crucial for the distribution of packaged goods, particularly within densely populated regions like Kanto.

- Consumer Preferences: Evolving consumer lifestyles, a growing emphasis on convenience, and increasing environmental awareness continuously shape product demand and packaging design.

- Technological Advancements: Ongoing innovation in material science, processing technologies, and sustainable solutions allows manufacturers to meet the increasingly sophisticated demands of end-user industries.

The Healthcare segment, while smaller in overall volume compared to Food and Beverage, exhibits high growth potential due to stringent regulatory requirements and the demand for specialized, high-performance packaging solutions for pharmaceuticals, medical devices, and diagnostics. The Personal Care and Household segment also demonstrates consistent growth, fueled by product innovation and consumer spending on personal hygiene and home care products.

Japan Plastic Packaging Industry Product Innovations

Product innovation in the Japan Plastic Packaging Industry is primarily focused on enhancing sustainability, functionality, and performance. Key developments include the introduction of advanced barrier films that significantly extend the shelf-life of food products, thereby reducing waste. There is a growing adoption of recycled content (r-PET, r-PE) in bottles, jars, and films, driven by both regulatory pressure and consumer demand. Lightweighting remains a critical trend, leading to the design of thinner yet stronger packaging solutions for bottles and trays. Furthermore, innovations in active and intelligent packaging, which can monitor product freshness or indicate tampering, are gaining traction, offering enhanced product safety and consumer trust. These advancements provide a significant competitive advantage by meeting stringent industry standards and aligning with market demands for eco-friendly and high-performance packaging.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the Japan Plastic Packaging Industry, meticulously segmenting the market to provide granular insights. The Packaging Type segmentation includes Flexible Plastic Packaging and Rigid Plastic Packaging. Further segmentation by Product Type encompasses Bottles and Jars, Trays and Containers, Pouches, Bags, Films and Wraps, and Other Product Types. The End-user Vertical analysis covers Food, Beverage, Healthcare, Personal Care and Household, and Other End-user Verticals. Each segment is analyzed for market size, growth projections, and competitive dynamics, offering a detailed view of specific market opportunities and challenges. For instance, the Flexible Plastic Packaging segment is projected to grow at a CAGR of approximately 4.0%, driven by its widespread use in the food and personal care industries, with a market size estimated to reach over ten thousand million yen by 2033.

Key Drivers of Japan Plastic Packaging Industry Growth

Several key drivers are fueling the growth of the Japan Plastic Packaging Industry. Technological advancements in material science and manufacturing processes are enabling the creation of more sustainable, efficient, and functional packaging solutions. The increasing demand for convenience and premiumization in the Food and Beverage sectors, coupled with an aging population and growing single-person households, creates a sustained need for innovative packaging formats like pouches and smaller portioned containers. Stringent food safety regulations and the growing emphasis on extending product shelf-life also drive demand for advanced barrier packaging. Furthermore, government initiatives promoting recycling and the circular economy are encouraging the adoption of recycled and biodegradable plastics, opening new avenues for growth.

Challenges in the Japan Plastic Packaging Industry Sector

The Japan Plastic Packaging Industry faces several significant challenges. Growing environmental concerns and stricter regulations regarding plastic waste are pressuring manufacturers to innovate and adopt more sustainable alternatives, which can involve higher initial investment costs. The fluctuating prices of raw materials, primarily derived from crude oil, introduce volatility into production costs. Intense competition from both domestic and international players, as well as from alternative packaging materials like paper and glass, necessitates continuous innovation and cost optimization. Supply chain disruptions, exacerbated by global events, can impact the availability and cost of raw materials and finished goods. Overcoming these hurdles requires strategic investment in R&D, efficient supply chain management, and a proactive approach to sustainability.

Emerging Opportunities in Japan Plastic Packaging Industry

Emerging opportunities in the Japan Plastic Packaging Industry are closely tied to sustainability and technological advancements. The increasing consumer demand for eco-friendly packaging presents a significant opportunity for companies developing and implementing biodegradable, compostable, and high-recycled content plastic solutions. The growth of e-commerce also drives demand for specialized, protective, and lightweight packaging for shipping and handling. Innovations in smart packaging, offering features like traceability and tamper-evidence, cater to the Food and Healthcare sectors. Furthermore, the expanding Healthcare and Personal Care markets, driven by an aging population and a focus on hygiene, offer substantial growth potential for specialized and high-barrier packaging solutions.

Leading Players in the Japan Plastic Packaging Industry Market

- Dong Nai Plastics

- Sekisui Kasei Co Ltd

- Mondi Tokyo

- Toyo Seikan Group Holding Ltd

- Takemoto Yohki Co Ltd

- Hosokawa Yoko Co Ltd

- Takigawa Corporation

- Rengo Co Ltd

- Amcor Japan

- Gunze Limited

- Cosmo Films Japan LLC

- Toppan Inc

- Toyobo Co Ltd

- JSP Corporation Japan

- Sealed Air Japan

- Sonoco Japan

Key Developments in Japan Plastic Packaging Industry Industry

- Dec 2020: Private investment firm Graham Partners continues its targeted investments in technology-driven advanced manufacturing companies and has acquired Berry Global Group Inc. The business will be combined with Graham Partners' flexible packaging portfolio company, Advanced Barrier Extrusions LLC (ABX), which Graham Partners acquired in August 2018. The business will operate under the ABX name in the future.

- March 2021: Greiner Packaging announced that it has expanded its range of sanitizer bottles to meet the increased demand. The new product range includes 16 bottles, including sanitizers, and comes in different sizes and shapes with capacities ranging between 100 and 1000 milliliters. These bottles are all produced using the ISBM process and have round bodies, which can be made from up to 100% r-PET.

Future Outlook for Japan Plastic Packaging Industry Market

The future outlook for the Japan Plastic Packaging Industry remains positive, driven by sustained demand from key end-user verticals and a strong emphasis on innovation and sustainability. The industry is expected to witness continued growth, with a significant shift towards advanced materials, including those with enhanced barrier properties and higher recycled content. The adoption of circular economy principles will accelerate, leading to increased investment in recycling technologies and the development of more easily recyclable packaging designs. Technological advancements in areas such as smart packaging and customized solutions will further shape market offerings. Strategic collaborations and potential M&A activities are anticipated as companies seek to expand their capabilities and market reach in this evolving landscape. The industry's ability to adapt to evolving regulatory frameworks and consumer preferences will be crucial for long-term success, with potential for the market size to exceed several hundred thousand million yen by the end of the forecast period.

Japan Plastic Packaging Industry Segmentation

-

1. Packaging Type

- 1.1. Flexible Plastic Packaging

- 1.2. Rigid Plastic Packaging

-

2. Product Type

- 2.1. Bottles and Jars

- 2.2. Trays and containers

- 2.3. Pouches

- 2.4. Bags

- 2.5. Films and Wraps

- 2.6. Other Product Types

-

3. End-user Vertical

- 3.1. Food

- 3.2. Beverage

- 3.3. Healthcare

- 3.4. Personal care and Household

- 3.5. Other End-user Verticals

Japan Plastic Packaging Industry Segmentation By Geography

- 1. Japan

Japan Plastic Packaging Industry Regional Market Share

Geographic Coverage of Japan Plastic Packaging Industry

Japan Plastic Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 5.1.1. Flexible Plastic Packaging

- 5.1.2. Rigid Plastic Packaging

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles and Jars

- 5.2.2. Trays and containers

- 5.2.3. Pouches

- 5.2.4. Bags

- 5.2.5. Films and Wraps

- 5.2.6. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.3. Healthcare

- 5.3.4. Personal care and Household

- 5.3.5. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6. Japan Plastic Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6.1.1. Flexible Plastic Packaging

- 6.1.2. Rigid Plastic Packaging

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Bottles and Jars

- 6.2.2. Trays and containers

- 6.2.3. Pouches

- 6.2.4. Bags

- 6.2.5. Films and Wraps

- 6.2.6. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.3. Healthcare

- 6.3.4. Personal care and Household

- 6.3.5. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Dong Nai Plastics

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sekisui Kasei Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mondi Tokyo*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Toyo Seikan Group Holding Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Takemoto Yohki Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hosokawa Yoko Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Takigawa Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Rengo Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Amcor Japan

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Gunze Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Cosmo Films Japan LLC

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Toppan Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Toyobo Co Ltd

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 JSP Corporation Japan

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Sealed Air Japan

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Sonoco Japan

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.1 Dong Nai Plastics

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Plastic Packaging Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Japan Plastic Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Plastic Packaging Industry Revenue million Forecast, by Packaging Type 2020 & 2033

- Table 2: Japan Plastic Packaging Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 3: Japan Plastic Packaging Industry Revenue million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Japan Plastic Packaging Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Japan Plastic Packaging Industry Revenue million Forecast, by Packaging Type 2020 & 2033

- Table 6: Japan Plastic Packaging Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 7: Japan Plastic Packaging Industry Revenue million Forecast, by End-user Vertical 2020 & 2033

- Table 8: Japan Plastic Packaging Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Plastic Packaging Industry?

The projected CAGR is approximately 2.53%.

2. Which companies are prominent players in the Japan Plastic Packaging Industry?

Key companies in the market include Dong Nai Plastics, Sekisui Kasei Co Ltd, Mondi Tokyo*List Not Exhaustive, Toyo Seikan Group Holding Ltd, Takemoto Yohki Co Ltd, Hosokawa Yoko Co Ltd, Takigawa Corporation, Rengo Co Ltd, Amcor Japan, Gunze Limited, Cosmo Films Japan LLC, Toppan Inc, Toyobo Co Ltd, JSP Corporation Japan, Sealed Air Japan, Sonoco Japan.

3. What are the main segments of the Japan Plastic Packaging Industry?

The market segments include Packaging Type, Product Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.2 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Lightweight-packaging Methods; Increased Eco-friendly Packaging and Recycled Plastic.

6. What are the notable trends driving market growth?

Increase in Adoption of Light-Weight Packaging.

7. Are there any restraints impacting market growth?

Monitoring issues and lack of standardization.

8. Can you provide examples of recent developments in the market?

Dec 2020- Private investment firm Graham Partners continues its targeted investments in technology-driven advanced manufacturing companies and has acquired Berry Global Group Inc. The business will be combined with Graham Partners' flexible packaging portfolio company, Advanced Barrier Extrusions LLC (ABX), which Graham Partners acquired in August 2018. The business will operate under the ABX name in the future.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Plastic Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Plastic Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Plastic Packaging Industry?

To stay informed about further developments, trends, and reports in the Japan Plastic Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence