Key Insights

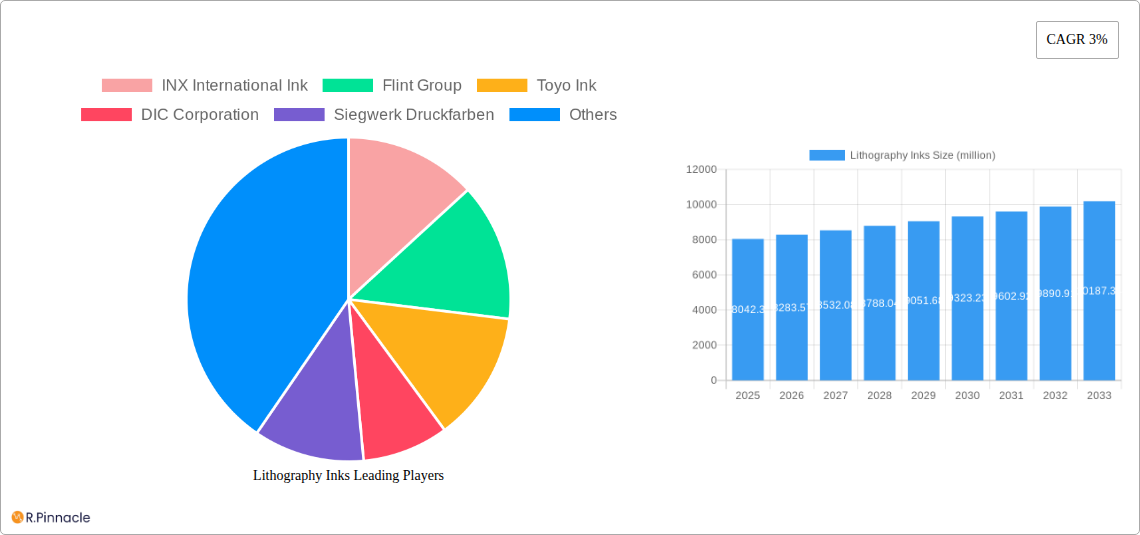

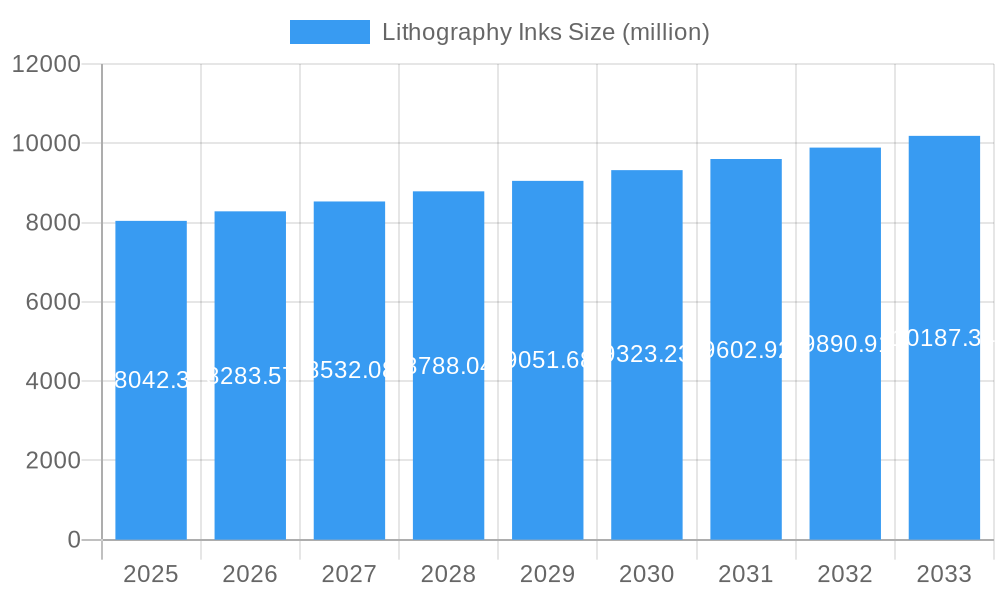

The global Lithography Inks market is poised for steady expansion, projected to reach an estimated $8,042.3 million by 2025. This growth is underpinned by a CAGR of 3% over the forecast period of 2025-2033. Key drivers fueling this market include the sustained demand from the packaging sector, where the visual appeal and durability of lithographically printed materials remain paramount. The commercial printing segment also contributes significantly, driven by marketing collateral, point-of-sale displays, and other print-based advertising initiatives. Furthermore, the publication segment, while evolving, still relies on lithography for its cost-effectiveness and quality in producing magazines, books, and newspapers. Emerging economies, particularly in the Asia Pacific region, are expected to be significant contributors to this growth due to increasing industrialization and a rising middle class with greater purchasing power.

Lithography Inks Market Size (In Billion)

Technological advancements in ink formulations, particularly in developing eco-friendly and sustainable options like water-based inks, are shaping market trends. These advancements address growing environmental concerns and regulatory pressures, making them increasingly attractive to manufacturers and consumers alike. The market also benefits from innovations in printing equipment that enhance efficiency and precision in lithographic printing. However, challenges such as the increasing adoption of digital printing technologies, which offer faster turnaround times and personalization for certain applications, and fluctuations in raw material prices, could potentially restrain market growth. Despite these hurdles, the established reliability, cost-effectiveness, and quality of lithography ensure its continued relevance and a positive outlook for the lithography inks market.

Lithography Inks Company Market Share

Comprehensive Report: Lithography Inks Market Analysis (2019–2033)

This in-depth report offers a definitive analysis of the global Lithography Inks market, a critical component for the printing industry. With a study period spanning from 2019 to 2033, a base and estimated year of 2025, and a robust forecast period of 2025–2033, this research provides unparalleled insights into market dynamics, growth drivers, and future trajectories. We meticulously examine key segments such as Commercial Printing, Packaging, and Publication, alongside ink types including Water-based and Solvent-based. Featuring data on leading companies like INX International Ink, Flint Group, and Toyo Ink, this report is an indispensable resource for stakeholders seeking to navigate and capitalize on the evolving Lithography Inks landscape.

Lithography Inks Market Structure & Innovation Trends

The Lithography Inks market, valued at approximately XXX million in the base year of 2025, exhibits a moderately concentrated structure. Leading entities such as INX International Ink, Flint Group, and Toyo Ink collectively hold a significant market share, estimated to be around 60 million. Innovation in this sector is primarily driven by the increasing demand for sustainable and eco-friendly ink formulations, advancements in color management technology, and the development of inks with enhanced durability and faster drying times. Regulatory frameworks, particularly those concerning VOC emissions and food-grade compliance for packaging inks, are playing an increasingly crucial role in shaping product development and market entry strategies. Product substitutes, while present in niche applications, are largely unable to replicate the performance and cost-effectiveness of lithographic inks in their primary domains. End-user demographics are shifting towards industries requiring high-quality, consistent print outputs, such as premium packaging and specialized commercial printing. Mergers and acquisitions (M&A) remain a strategic avenue for consolidation and market expansion, with recent deal values estimated in the range of XX million, fostering greater market integration and technological synergy.

- Market Concentration: Moderately concentrated with a few key players dominating.

- Innovation Drivers: Sustainability, enhanced performance (durability, drying), advanced color management.

- Regulatory Frameworks: VOC emission standards, food-grade compliance, environmental certifications.

- Product Substitutes: Limited in core lithographic applications, but emerging in digital printing.

- End-User Demographics: Growing demand from premium packaging, commercial printing, and publications.

- M&A Activities: Strategic for market expansion and technological integration, with estimated deal values of XX million.

Lithography Inks Market Dynamics & Trends

The Lithography Inks market is poised for consistent growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033, reaching a market size of nearly XXX million by the forecast period's end. This growth is underpinned by several key market dynamics and trends. A primary growth driver is the persistent demand from the packaging industry, fueled by the rise of e-commerce and the need for attractive, protective, and informative packaging solutions. Lithography's ability to deliver high-quality, cost-effective printing for high-volume packaging runs makes it a preferred choice. Furthermore, advancements in printing technology, including faster press speeds and improved ink-substrate compatibility, are enhancing the efficiency and appeal of lithographic printing. Consumer preferences are also indirectly influencing the market, with a growing demand for visually appealing products and sustainable packaging, pushing ink manufacturers to develop eco-friendly and high-impact formulations. Technological disruptions, while significant, are largely centered around enhancing existing lithographic processes rather than outright replacement, with innovations focusing on UV-curing inks, low-migration inks for food packaging, and digital integration for color consistency. Competitive dynamics are characterized by intense price competition, a strong emphasis on product innovation, and strategic partnerships to expand global reach. Market penetration for specialized lithography inks, such as those used in security printing and functional coatings, is also on the rise, indicating a diversification of applications. The resurgence of certain print applications and the need for consistent, high-quality output across various substrates continue to solidify the position of lithography inks. The increasing focus on brand differentiation through vibrant and durable print finishes further stimulates demand. The development of smart packaging solutions, incorporating functional inks with unique properties, also presents a growing area of opportunity, driving innovation in substrate compatibility and performance. The global supply chain for raw materials is a critical factor, with manufacturers continuously seeking stable and cost-effective sourcing.

Dominant Regions & Segments in Lithography Inks

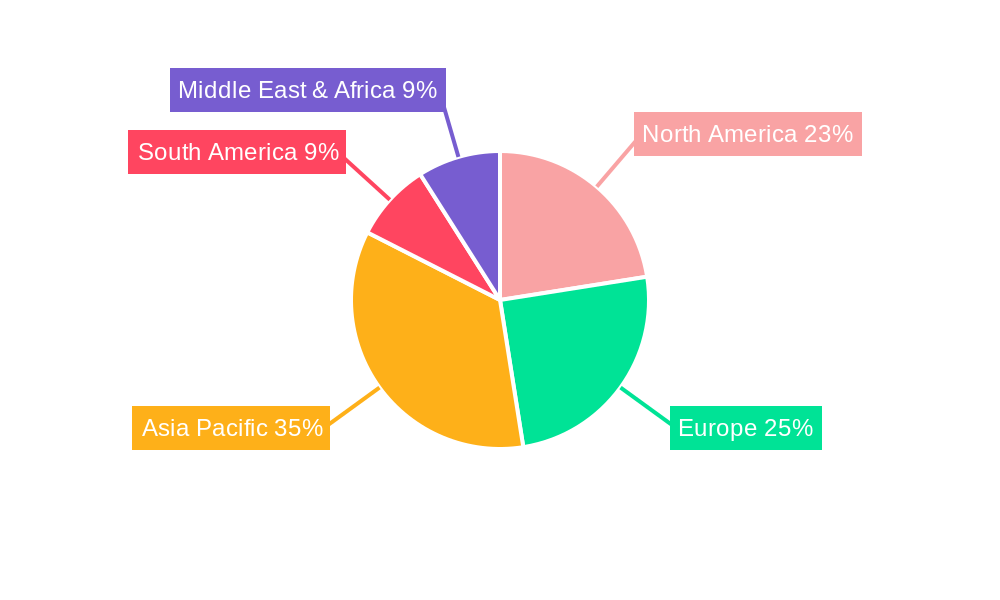

The Lithography Inks market demonstrates significant regional and segmental dominance, driven by a confluence of economic, technological, and regulatory factors. Asia-Pacific stands out as the dominant region, accounting for an estimated market share of over 40 million in 2025. This dominance is attributed to the region's robust manufacturing sector, burgeoning consumer markets, and significant investments in printing infrastructure. Countries like China and India are key contributors, propelled by rapid industrialization and a growing demand for printed materials across commercial, packaging, and publication sectors.

Within this region, the Packaging segment exhibits the strongest growth and market penetration, projected to reach a value of XX million by 2025. This surge is directly linked to the expansion of the food and beverage, pharmaceutical, and consumer goods industries, all of which rely heavily on high-quality, compliant lithographic printing for their packaging needs. The increasing adoption of e-commerce further amplifies the demand for durable and aesthetically pleasing packaging.

Among ink types, Water-based inks are gaining significant traction, driven by stringent environmental regulations and a growing consumer preference for sustainable products. While Solvent-based inks continue to hold a substantial market share, particularly in applications requiring rapid drying and high durability, the environmental advantages of water-based alternatives are increasingly influencing purchasing decisions and R&D investments. The Water-based segment is projected to witness a CAGR of XX% over the forecast period.

- Leading Region: Asia-Pacific (China, India) – Driven by manufacturing prowess and growing consumer base.

- Dominant Application Segment: Packaging – Fueled by e-commerce, consumer goods, and stringent compliance needs.

- Key Drivers: Economic growth, rising disposable incomes, demand for product differentiation.

- Growing Ink Type: Water-based – Propelled by environmental regulations and sustainability trends.

- Key Drivers: VOC emission reduction, health and safety concerns, brand sustainability initiatives.

- Other Segments: Commercial Printing and Publication, while mature, continue to be significant consumers of lithography inks, driven by demand for marketing materials and educational content.

Lithography Inks Product Innovations

Recent product innovations in Lithography Inks are centered on enhancing sustainability, performance, and digital integration. Manufacturers are actively developing low-VOC (Volatile Organic Compound) and water-based ink formulations to meet stringent environmental regulations and growing consumer demand for eco-friendly printing solutions. Advancements in UV-curing inks offer faster drying times, improved scratch resistance, and enhanced print quality across a wider range of substrates, providing a competitive advantage for printers. Furthermore, the development of low-migration inks specifically for food packaging applications ensures compliance with safety standards. These innovations address evolving market needs, offering printers greater flexibility, improved operational efficiency, and the ability to produce visually striking and environmentally responsible printed products.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Lithography Inks market, segmented by application and ink type. The Application segmentation includes Commercial Printing, Packaging, Publication, and Others. The Packaging segment, projected to reach a market size of approximately XX million by 2025, is expected to witness robust growth driven by the expanding e-commerce sector and demand for attractive consumer goods packaging. Commercial Printing is a mature but significant segment, valued at around XX million, serving various marketing and promotional needs. The Publication segment, while facing digital competition, continues to be relevant for magazines, newspapers, and books. The Others segment encompasses niche applications like security printing and decorative printing.

The Type segmentation comprises Water-based, Solvent-based, and Others. Water-based inks are experiencing accelerated growth, driven by environmental regulations and a preference for sustainable solutions, with an estimated market size of XX million in 2025. Solvent-based inks, while still dominant in certain applications requiring high durability and fast drying, are facing increasing scrutiny. The Others category includes specialty inks like UV-curable and energy-curable inks.

Key Drivers of Lithography Inks Growth

The growth of the Lithography Inks market is propelled by several key factors. The expanding global packaging industry, driven by the e-commerce boom and the increasing demand for visually appealing and informative product packaging, is a primary catalyst. Technological advancements in lithographic printing equipment, leading to faster speeds, greater precision, and enhanced substrate compatibility, further boost ink consumption. A growing emphasis on sustainable printing practices and a rising consumer preference for eco-friendly products are accelerating the adoption of water-based and low-VOC inks. Furthermore, the consistent demand from the commercial printing sector for high-quality marketing collateral and promotional materials, coupled with the enduring need for printed publications, provides a stable foundation for market expansion. Regulatory support for environmentally conscious manufacturing processes also influences product development and market adoption.

Challenges in the Lithography Inks Sector

The Lithography Inks sector faces several significant challenges that can temper market growth. Increasingly stringent environmental regulations regarding VOC emissions and the use of certain chemicals necessitate substantial investment in R&D for compliance, potentially increasing production costs. Fluctuations in raw material prices, such as pigments, resins, and solvents, can impact profitability and pricing strategies. Intense competition from alternative printing technologies, particularly digital printing, especially in shorter run lengths and personalized applications, poses a continuous threat. Supply chain disruptions, exacerbated by geopolitical events and global logistical complexities, can affect the availability and cost of essential raw materials. Furthermore, the mature nature of some end-user segments, like traditional publication printing, limits substantial volume growth.

Emerging Opportunities in Lithography Inks

Emerging opportunities within the Lithography Inks market lie in the development of specialized and functional inks. The burgeoning demand for sustainable packaging solutions presents a significant avenue for growth, particularly for biodegradable and compostable ink formulations. Advancements in digital printing technologies are also creating opportunities for hybrid printing solutions that combine the benefits of lithography with digital printing's flexibility. The increasing focus on brand differentiation and unique product aesthetics is driving demand for specialty inks with enhanced visual effects, such as metallic, pearlescent, and textured finishes. Furthermore, the growing smart packaging trend, incorporating conductive inks or inks with antimicrobial properties, opens up new high-value market segments.

Leading Players in the Lithography Inks Market

- INX International Ink

- Flint Group

- Toyo Ink

- DIC Corporation

- Siegwerk Druckfarben

- FUJIFILM Holdings America

- HuberGroup

- Tokyo Printing Ink

- T&K Toka

- Wikoff Color

Key Developments in Lithography Inks Industry

- 2023 Q4: Launch of new range of low-migration UV-curable inks for food packaging by Flint Group, addressing stringent safety regulations.

- 2023 Q3: Toyo Ink announces strategic partnership with a leading paper manufacturer to develop sustainable ink-substrate solutions.

- 2023 Q2: INX International Ink invests heavily in R&D for bio-based ink formulations, aiming to reduce reliance on petrochemicals.

- 2023 Q1: DIC Corporation expands its portfolio of water-based inks, targeting the commercial printing segment with eco-friendly options.

- 2022 Q4: Siegwerk Druckfarben acquires a smaller specialty ink manufacturer, expanding its market reach in niche applications.

- 2022 Q3: FUJIFILM Holdings America introduces enhanced ink formulations for improved print durability in outdoor applications.

- 2022 Q2: HuberGroup unveils innovative color management software integrated with their lithography ink offerings for greater precision.

- 2022 Q1: T&K Toka develops high-opacity white inks for dark substrate printing, catering to premium packaging demands.

- 2021 Q4: Wikoff Color enhances its technical support services to assist printers in optimizing lithographic ink performance.

- 2021 Q3: Tokyo Printing Ink focuses on expanding its distribution network for water-based inks in emerging markets.

Future Outlook for Lithography Inks Market

The future outlook for the Lithography Inks market remains positive, driven by continuous innovation and evolving industry demands. The ongoing shift towards sustainable and eco-friendly ink solutions, including water-based and bio-based formulations, will be a dominant trend, aligning with global environmental initiatives and consumer preferences. The packaging sector will continue to be a primary growth engine, with increasing demand for high-quality, safe, and visually appealing packaging solutions. Technological advancements in printing presses and ink formulations, such as UV-curing and low-migration inks, will enhance efficiency, performance, and market applicability. Strategic partnerships, mergers, and acquisitions will likely continue as companies seek to consolidate their market positions, expand their product portfolios, and enhance their global reach. The market is expected to witness steady growth, fueled by these dynamic forces and an unwavering demand for high-quality printed outputs across various industries.

Lithography Inks Segmentation

-

1. Application

- 1.1. Commercial Printing

- 1.2. Packaging

- 1.3. Publication

- 1.4. Others

-

2. Types

- 2.1. Water-based

- 2.2. Solvent-based

- 2.3. Others

Lithography Inks Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Lithography Inks Regional Market Share

Geographic Coverage of Lithography Inks

Lithography Inks REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Printing

- 5.1.2. Packaging

- 5.1.3. Publication

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Water-based

- 5.2.2. Solvent-based

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Lithography Inks Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Printing

- 6.1.2. Packaging

- 6.1.3. Publication

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Water-based

- 6.2.2. Solvent-based

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Lithography Inks Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Printing

- 7.1.2. Packaging

- 7.1.3. Publication

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Water-based

- 7.2.2. Solvent-based

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Lithography Inks Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Printing

- 8.1.2. Packaging

- 8.1.3. Publication

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Water-based

- 8.2.2. Solvent-based

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Lithography Inks Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Printing

- 9.1.2. Packaging

- 9.1.3. Publication

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Water-based

- 9.2.2. Solvent-based

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Lithography Inks Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Printing

- 10.1.2. Packaging

- 10.1.3. Publication

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Water-based

- 10.2.2. Solvent-based

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Lithography Inks Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Commercial Printing

- 11.1.2. Packaging

- 11.1.3. Publication

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Water-based

- 11.2.2. Solvent-based

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 INX International Ink

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Flint Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toyo Ink

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DIC Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Siegwerk Druckfarben

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 FUJIFILM Holdings America

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 HuberGroup

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Tokyo Printing Ink

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 T&K Toka

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Wikoff Color

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 INX International Ink

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Lithography Inks Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Lithography Inks Revenue (million), by Application 2025 & 2033

- Figure 3: North America Lithography Inks Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Lithography Inks Revenue (million), by Types 2025 & 2033

- Figure 5: North America Lithography Inks Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Lithography Inks Revenue (million), by Country 2025 & 2033

- Figure 7: North America Lithography Inks Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Lithography Inks Revenue (million), by Application 2025 & 2033

- Figure 9: South America Lithography Inks Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Lithography Inks Revenue (million), by Types 2025 & 2033

- Figure 11: South America Lithography Inks Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Lithography Inks Revenue (million), by Country 2025 & 2033

- Figure 13: South America Lithography Inks Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Lithography Inks Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Lithography Inks Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Lithography Inks Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Lithography Inks Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Lithography Inks Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Lithography Inks Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Lithography Inks Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Lithography Inks Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Lithography Inks Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Lithography Inks Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Lithography Inks Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Lithography Inks Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Lithography Inks Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Lithography Inks Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Lithography Inks Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Lithography Inks Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Lithography Inks Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Lithography Inks Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Lithography Inks Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Lithography Inks Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Lithography Inks Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Lithography Inks Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Lithography Inks Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Lithography Inks Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Lithography Inks Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Lithography Inks Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Lithography Inks Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lithography Inks?

The projected CAGR is approximately 3%.

2. Which companies are prominent players in the Lithography Inks?

Key companies in the market include INX International Ink, Flint Group, Toyo Ink, DIC Corporation, Siegwerk Druckfarben, FUJIFILM Holdings America, HuberGroup, Tokyo Printing Ink, T&K Toka, Wikoff Color.

3. What are the main segments of the Lithography Inks?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8042.3 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lithography Inks," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lithography Inks report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lithography Inks?

To stay informed about further developments, trends, and reports in the Lithography Inks, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence