Key Insights

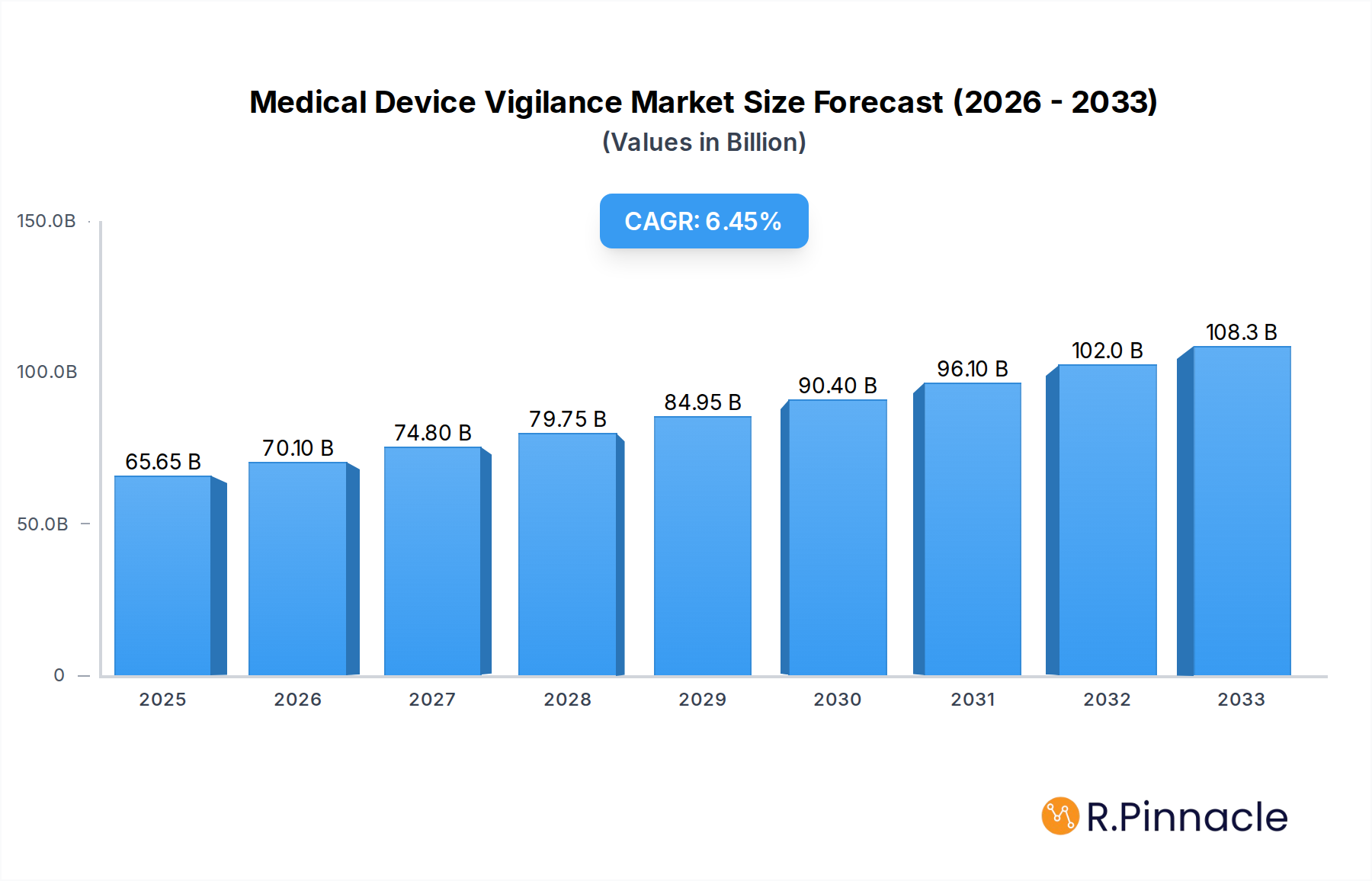

The Medical Device Vigilance market is poised for substantial expansion, projected to reach $65.65 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 10.7% anticipated through 2033. This significant growth is underpinned by a confluence of critical drivers, including increasingly stringent regulatory frameworks worldwide, a rising volume of medical device approvals, and a growing emphasis on patient safety and post-market surveillance by healthcare providers and manufacturers alike. The increasing complexity of medical devices, coupled with the advent of connected health technologies, further necessitates advanced vigilance systems to monitor device performance and identify potential risks proactively. Contract Research Organizations (CROs) and Business Process Outsourcing (BPO) firms are playing an increasingly vital role, offering specialized expertise and scalable solutions for managing the intricate processes of adverse event reporting, risk management, and regulatory compliance. This trend towards outsourcing is particularly prominent in fostering market growth, allowing Original Equipment Manufacturers (OEMs) to focus on innovation and core competencies while ensuring adherence to evolving global standards.

Medical Device Vigilance Market Size (In Billion)

The market is witnessing significant trends such as the widespread adoption of cloud-based vigilance solutions, offering enhanced accessibility, scalability, and data analytics capabilities compared to traditional on-premise systems. Artificial intelligence (AI) and machine learning (ML) are also emerging as transformative technologies within this space, enabling more sophisticated analysis of real-world data, early detection of adverse trends, and predictive risk assessment. While the market presents a promising outlook, certain restraints, such as the high cost of implementing and maintaining advanced vigilance systems and a potential shortage of skilled professionals in regulatory affairs and data analytics, could temper the growth trajectory. However, the persistent demand for robust product safety, coupled with the continuous innovation in both medical devices and vigilance technologies, is expected to outweigh these challenges, ensuring a dynamic and expanding market landscape across key regions like North America, Europe, and Asia Pacific.

Medical Device Vigilance Company Market Share

Medical Device Vigilance Market: Comprehensive Analysis and Future Projections (2019-2033)

This in-depth report provides an unparalleled analysis of the global Medical Device Vigilance market, offering critical insights for stakeholders aiming to navigate this complex and rapidly evolving landscape. Spanning a historical period from 2019 to 2024, with a robust forecast period extending to 2033, this study leverages advanced analytics to deliver precise market valuations and growth trajectories. With a base year of 2025 and an estimated year of 2025, this report ensures the most current and relevant data is at your fingertips. Our expert analysis covers every facet of the market, from intricate regulatory frameworks and technological innovations to dominant regional players and emerging opportunities. Prepare to gain a strategic advantage with actionable intelligence designed to inform your business decisions, product development, and investment strategies within the billion-dollar medical device vigilance ecosystem.

Medical Device Vigilance Market Structure & Innovation Trends

The Medical Device Vigilance market exhibits a dynamic structure characterized by significant innovation drivers, stringent regulatory frameworks, and a growing need for sophisticated safety monitoring solutions. Market concentration varies across different solution types and deployment models, with established players holding substantial market share while innovative startups continuously disrupt the status quo. Key innovation drivers include the increasing complexity of medical devices, the proliferation of connected health technologies (IoT), and the escalating demand for proactive risk management to ensure patient safety and regulatory compliance. Regulatory frameworks, such as those established by the FDA (Food and Drug Administration) and EMA (European Medicines Agency), are paramount, dictating the compliance requirements and the necessary functionalities of vigilance software and services. The threat of product substitutes, while present in the form of manual processes or less integrated solutions, is increasingly mitigated by the clear advantages offered by dedicated vigilance platforms. End-user demographics are diverse, encompassing Original Equipment Manufacturers (OEMs), Contract Research Organizations (CROs), and Business Process Outsourcing (BPO) providers, all of whom face unique challenges and demands. Merger and acquisition (M&A) activities are a significant indicator of market consolidation and strategic expansion, with numerous deals valued in the billions of dollars shaping the competitive landscape. Analyzing these M&A deals, which have reached aggregate values of over $10 billion in recent years, provides crucial insights into market consolidation trends and the strategic priorities of leading companies.

Medical Device Vigilance Market Dynamics & Trends

The Medical Device Vigilance market is projected to witness substantial growth driven by a confluence of critical factors, including an intensifying focus on patient safety, escalating regulatory scrutiny, and the rapid adoption of digital health technologies. The increasing number of medical device recalls and adverse event reports globally underscores the imperative for robust vigilance systems. Technological disruptions, such as the integration of artificial intelligence (AI) and machine learning (ML) for advanced signal detection and predictive analytics, are revolutionizing how adverse events are identified and managed. Consumer preferences are leaning towards safer, more reliable medical devices, compelling manufacturers to invest heavily in post-market surveillance. The competitive dynamics within the market are characterized by intense innovation, with companies vying to offer comprehensive, cloud-based solutions that enhance efficiency and compliance. The global market penetration of specialized vigilance software is still on an upward trajectory, indicating significant untapped potential. The Compound Annual Growth Rate (CAGR) for the medical device vigilance market is estimated to be approximately 15.5 billion dollars, underscoring its robust expansion. This growth is further fueled by the increasing complexity of medical devices, the rise of personalized medicine, and the growing volume of real-world data that requires meticulous monitoring. Regulatory bodies worldwide are also strengthening post-market surveillance requirements, thereby mandating the adoption of advanced vigilance solutions. The proactive identification and mitigation of risks associated with medical devices are becoming a non-negotiable aspect of operations for all stakeholders, from manufacturers to healthcare providers.

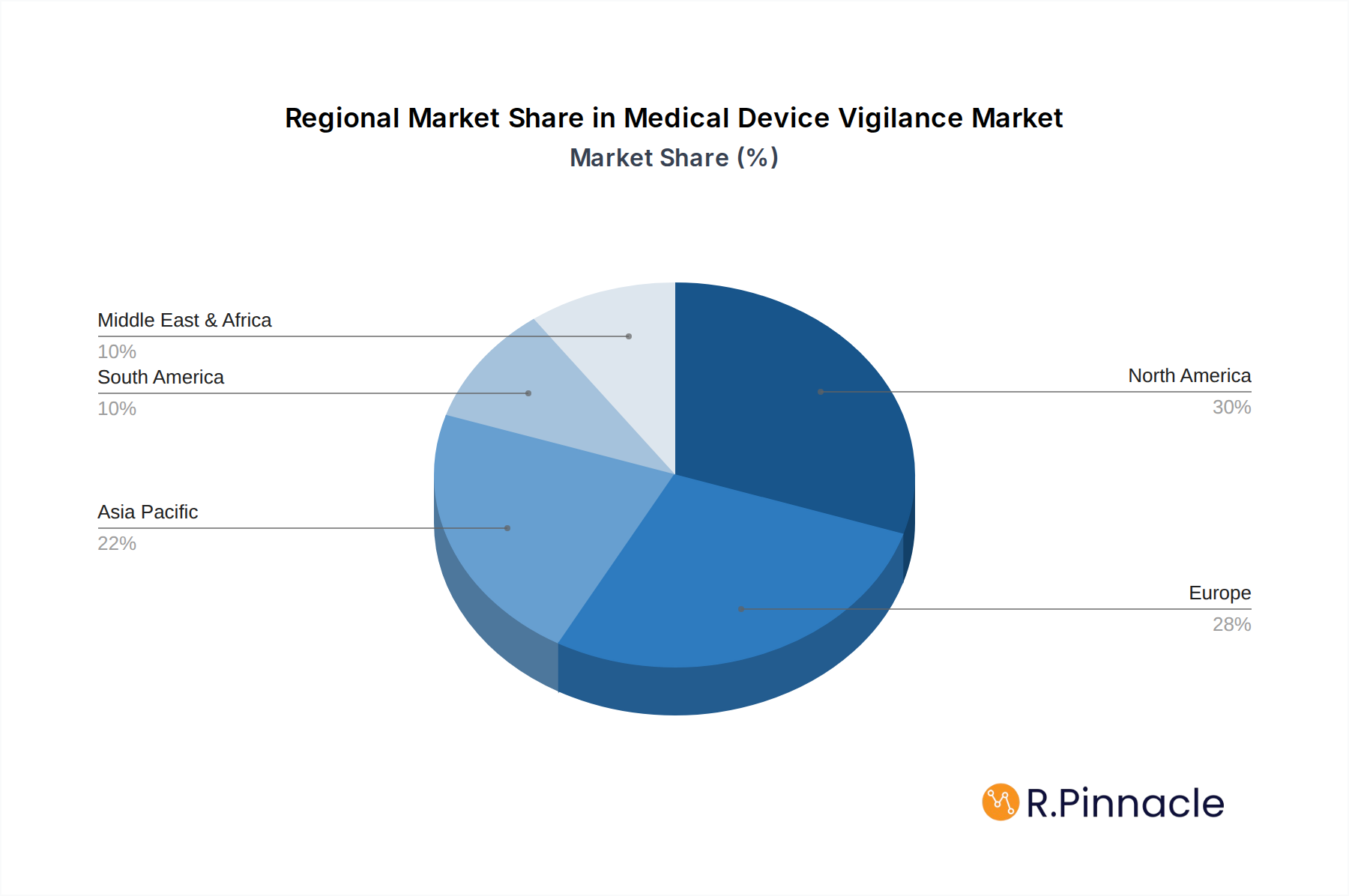

Dominant Regions & Segments in Medical Device Vigilance

North America currently stands as the dominant region in the Medical Device Vigilance market, driven by a highly developed healthcare infrastructure, stringent regulatory oversight from the FDA, and a high concentration of leading medical device manufacturers and CROs. The United States, in particular, plays a pivotal role due to its substantial investment in medical device innovation and a proactive approach to patient safety.

- Key Drivers in North America:

- Robust Regulatory Framework: The FDA's comprehensive guidelines for post-market surveillance and adverse event reporting create a strong demand for vigilance solutions.

- Technological Advancement: The region's leadership in AI, big data analytics, and cloud computing facilitates the adoption of advanced vigilance technologies.

- High R&D Spending: Significant investments in research and development by medical device companies necessitate sophisticated systems for monitoring product performance and safety.

- Presence of Major Players: The concentration of leading medical device manufacturers and CROs in North America fuels market growth and innovation.

The Original Equipment Manufacturers (OEM) segment is a primary driver of market growth across all regions. OEMs are directly responsible for the safety and efficacy of their devices and thus require comprehensive vigilance systems to manage post-market surveillance, report adverse events, and ensure compliance with global regulations. Their market share is substantial, estimated to be over 40 billion dollars, due to the sheer volume of devices they produce and the extensive regulatory obligations they face.

The Cloud deployment type is experiencing rapid growth and is increasingly favored over on-premise solutions. Cloud-based platforms offer scalability, flexibility, remote accessibility, and cost-effectiveness, aligning with the evolving needs of the industry. This segment is projected to capture a significant portion of the market, with projected growth rates of over 18.0 billion dollars annually.

The Contract Research Organization (CRO) segment is also a significant contributor, as many medical device companies outsource their vigilance activities to specialized CROs. These organizations leverage their expertise and technology to manage post-market surveillance for multiple clients, contributing to the market's expansion. The BPO segment, while smaller, also plays a role in providing specialized vigilance services.

Medical Device Vigilance Product Innovations

Recent product innovations in the Medical Device Vigilance sector are centered on enhancing the efficiency, accuracy, and predictive capabilities of post-market surveillance systems. Companies are increasingly integrating AI and machine learning algorithms to automate adverse event detection, identify emerging safety signals, and perform predictive risk assessments. Cloud-based platforms are becoming the industry standard, offering enhanced scalability, accessibility, and data integration capabilities. These advancements enable a more proactive approach to patient safety, moving beyond reactive reporting to predictive risk mitigation. Competitive advantages are being gained through user-friendly interfaces, comprehensive data analytics dashboards, and seamless integration with other regulatory and quality management systems, offering end-to-end solutions valued at over 5 billion dollars.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Medical Device Vigilance market across key segmentation parameters. The Application segment is segmented into Contract Research Organization (CRO), Business Process Outsourcing (BPO), Original Equipment Manufacturers (OEM), and Others. The Type segment is further divided into On-premise and Cloud deployment models. For the Application segment, the OEM segment is projected to hold the largest market share, estimated at over 35 billion dollars by 2033, owing to direct regulatory responsibilities. The CRO segment is anticipated to grow at a CAGR of 16.5 billion dollars, driven by outsourcing trends. In the Type segment, the Cloud segment is expected to dominate, with a projected market size exceeding 50 billion dollars by 2033, reflecting the industry's shift towards flexible and scalable solutions.

Key Drivers of Medical Device Vigilance Growth

The Medical Device Vigilance market's growth is propelled by several interconnected factors. Firstly, escalating regulatory mandates from global health authorities such as the FDA and EMA necessitate robust vigilance systems for post-market surveillance and adverse event reporting, creating a consistent demand for compliance solutions. Secondly, the increasing complexity and connectivity of medical devices, including those integrated with IoT, amplify the potential risks and the need for sophisticated monitoring. Thirdly, a heightened global focus on patient safety and the growing awareness of the consequences of medical device-related adverse events compel manufacturers and healthcare providers to invest in proactive vigilance strategies. The total market value for these drivers is estimated to be in the billions.

Challenges in the Medical Device Vigilance Sector

Despite robust growth, the Medical Device Vigilance sector faces several challenges that can hinder market expansion. Complex and evolving global regulatory landscapes require constant adaptation and significant investment in compliance expertise and technology. Data integration and management across diverse sources and formats present a substantial hurdle, impacting the efficiency of signal detection and analysis. Furthermore, a shortage of skilled professionals with expertise in pharmacovigilance, regulatory affairs, and data science can impede the effective implementation and utilization of vigilance systems, impacting the operational efficiency which is valued in the billions. High implementation costs associated with advanced vigilance software and services can also be a barrier for smaller organizations, limiting their market reach and adoption rates.

Emerging Opportunities in Medical Device Vigilance

Emerging opportunities within the Medical Device Vigilance market are largely driven by technological advancements and evolving healthcare paradigms. The integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics and automated signal detection presents a significant opportunity for enhancing the proactive identification of safety concerns, estimated to add billions in value. The expansion of the Internet of Medical Things (IoMT) generates vast amounts of real-world data, creating a demand for advanced vigilance platforms capable of processing and analyzing this information effectively. Furthermore, the growing trend of global harmonization of regulatory standards, while challenging, also opens avenues for streamlined, single-platform vigilance solutions that can manage compliance across multiple jurisdictions. The increasing focus on real-world evidence (RWE) generation for post-market surveillance also presents a substantial growth area, estimated to be worth billions.

Leading Players in the Medical Device Vigilance Market

- ZEINCRO

- AssurX

- Sparta Systems

- Oracle Corporation

- Xybion Corporation

- Sarjen Systems Pvt. Ltd.

- MDI Consultants

- AB-Cube

- Laerdal Medical

- Omnify Software

- QVigilance

- Qserve

Key Developments in Medical Device Vigilance Industry

- 2023 March: Launch of advanced AI-powered signal detection module by Sparta Systems, enhancing proactive risk identification.

- 2023 February: Oracle Corporation announces strategic partnership with leading CROs to offer integrated vigilance solutions, expanding cloud-based services.

- 2022 December: ZEINCRO acquires a specialized data analytics firm to bolster its real-world evidence capabilities.

- 2022 November: AssurX introduces enhanced mobile reporting features for field-based vigilance data collection.

- 2022 October: Laerdal Medical expands its product portfolio with a new software suite for patient monitoring and safety.

- 2022 September: MDI Consultants launches a comprehensive cloud solution for global regulatory compliance management.

- 2022 August: Qserve receives certification for its advanced vigilance platform, validating its adherence to stringent quality standards.

Future Outlook for Medical Device Vigilance Market

The future outlook for the Medical Device Vigilance market is exceptionally bright, characterized by continued innovation and strategic growth. The ongoing digital transformation within healthcare, coupled with increasing regulatory demands for robust post-market surveillance, will serve as significant growth accelerators. The widespread adoption of cloud-based solutions, AI-driven analytics, and the growing emphasis on real-world evidence will redefine how medical device safety is managed, leading to more proactive and predictive approaches. Strategic opportunities lie in the development of integrated, end-to-end vigilance platforms that seamlessly connect data across the product lifecycle and cater to the evolving needs of a globalized market, potentially reaching market values in the hundreds of billions.

Medical Device Vigilance Segmentation

-

1. Application

- 1.1. Contract Research Organization (CRO)

- 1.2. Business Process Outsourcing (BPO)

- 1.3. Original Equipment Manufacturers (OEM)

- 1.4. Others

-

2. Type

- 2.1. On-premise

- 2.2. Cloud

Medical Device Vigilance Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Device Vigilance Regional Market Share

Geographic Coverage of Medical Device Vigilance

Medical Device Vigilance REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Contract Research Organization (CRO)

- 5.1.2. Business Process Outsourcing (BPO)

- 5.1.3. Original Equipment Manufacturers (OEM)

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. On-premise

- 5.2.2. Cloud

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Contract Research Organization (CRO)

- 6.1.2. Business Process Outsourcing (BPO)

- 6.1.3. Original Equipment Manufacturers (OEM)

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. On-premise

- 6.2.2. Cloud

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Contract Research Organization (CRO)

- 7.1.2. Business Process Outsourcing (BPO)

- 7.1.3. Original Equipment Manufacturers (OEM)

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. On-premise

- 7.2.2. Cloud

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Contract Research Organization (CRO)

- 8.1.2. Business Process Outsourcing (BPO)

- 8.1.3. Original Equipment Manufacturers (OEM)

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. On-premise

- 8.2.2. Cloud

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Contract Research Organization (CRO)

- 9.1.2. Business Process Outsourcing (BPO)

- 9.1.3. Original Equipment Manufacturers (OEM)

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. On-premise

- 9.2.2. Cloud

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Device Vigilance Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Contract Research Organization (CRO)

- 10.1.2. Business Process Outsourcing (BPO)

- 10.1.3. Original Equipment Manufacturers (OEM)

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. On-premise

- 10.2.2. Cloud

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ZEINCRO

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AssurX

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sparta Systems

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Oracle Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Xybion Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sarjen Systems Pvt. Ltd.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 MDI Consultants

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AB-Cube

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Laerdal Medical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Omnify Software

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 QVigilance

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Qserve

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 ZEINCRO

List of Figures

- Figure 1: Global Medical Device Vigilance Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Device Vigilance Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Device Vigilance Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Device Vigilance Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Medical Device Vigilance Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Device Vigilance Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Device Vigilance Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Device Vigilance Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Device Vigilance Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Device Vigilance Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Medical Device Vigilance Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Device Vigilance Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Device Vigilance Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Device Vigilance Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Device Vigilance Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Device Vigilance Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Medical Device Vigilance Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Device Vigilance Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Device Vigilance Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Device Vigilance Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Device Vigilance Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Device Vigilance Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Device Vigilance Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Device Vigilance Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Device Vigilance Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Device Vigilance Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Device Vigilance Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Device Vigilance Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Device Vigilance Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Device Vigilance Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Device Vigilance Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Medical Device Vigilance Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Medical Device Vigilance Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Medical Device Vigilance Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Medical Device Vigilance Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Medical Device Vigilance Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Device Vigilance Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Device Vigilance Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Medical Device Vigilance Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Device Vigilance Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Device Vigilance?

The projected CAGR is approximately 10.7%.

2. Which companies are prominent players in the Medical Device Vigilance?

Key companies in the market include ZEINCRO, AssurX, Sparta Systems, Oracle Corporation, Xybion Corporation, Sarjen Systems Pvt. Ltd., MDI Consultants, AB-Cube, Laerdal Medical, Omnify Software, QVigilance, Qserve.

3. What are the main segments of the Medical Device Vigilance?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Device Vigilance," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Device Vigilance report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Device Vigilance?

To stay informed about further developments, trends, and reports in the Medical Device Vigilance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence