Key Insights

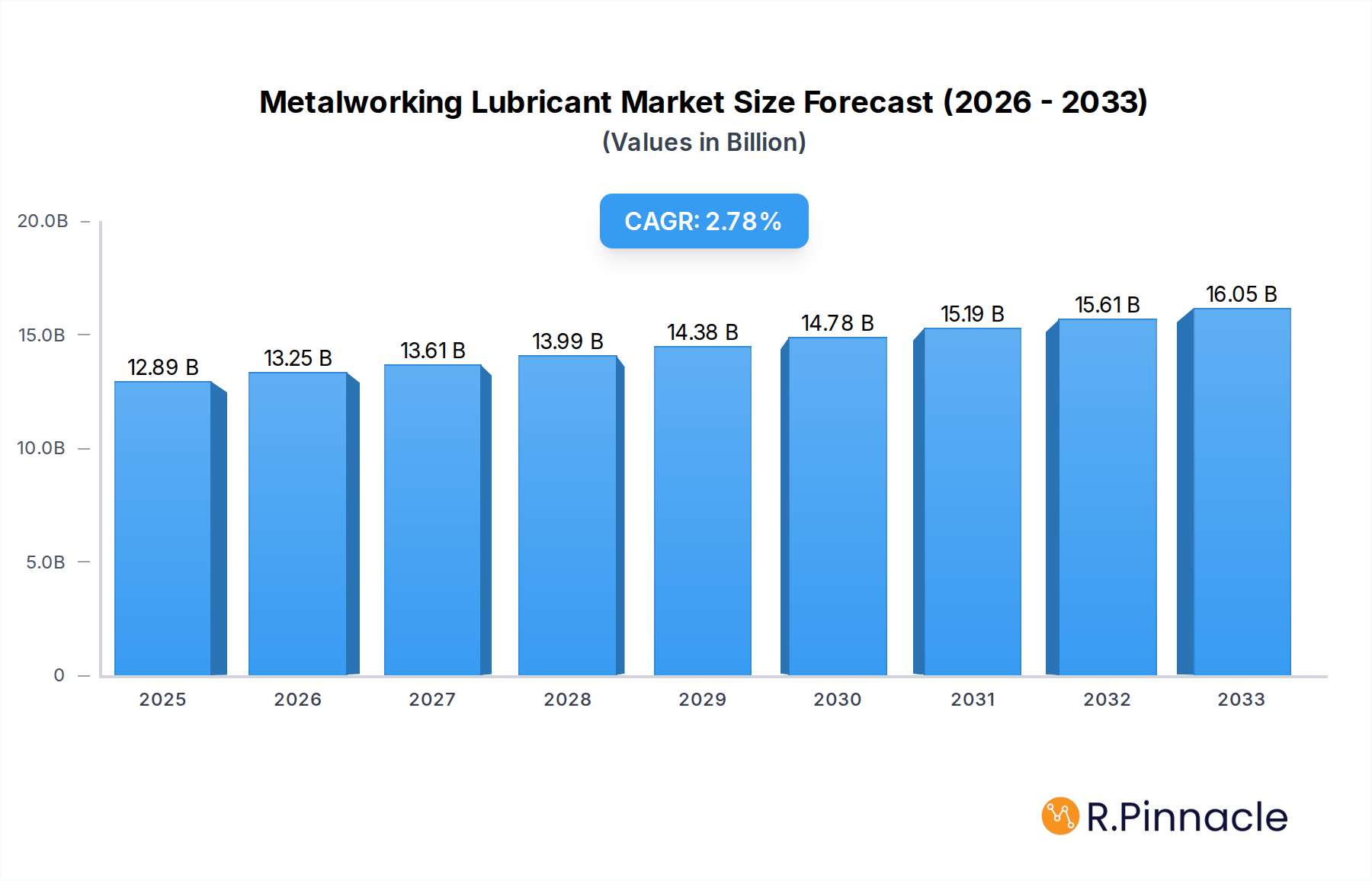

The global Metalworking Lubricant market is poised for steady growth, estimated to reach a substantial USD 12,887.9 million in 2025. This expansion is driven by an increasing demand from key end-use industries, particularly the automotive and machinery sectors, which rely heavily on efficient metal processing for manufacturing and production. The forecast indicates a Compound Annual Growth Rate (CAGR) of 2.7% for the period between 2025 and 2033, suggesting a consistent upward trajectory. Metal cutting fluids and metal forming fluids represent the dominant segments within this market, catering to the critical lubrication needs of machining operations and metal shaping processes respectively. Emerging economies, particularly in the Asia Pacific region, are expected to be significant growth engines due to rapid industrialization and a burgeoning manufacturing base. The market is characterized by a competitive landscape featuring established players like Quaker Houghton, Fuchs, and Exxon Mobil, alongside emerging regional companies, all striving to innovate and capture market share through advanced product formulations and sustainable solutions.

Metalworking Lubricant Market Size (In Billion)

Furthermore, the market's growth is being shaped by several dynamic trends. A growing emphasis on environmentally friendly and sustainable lubricant options is influencing product development, with a focus on bio-based and water-miscible fluids to reduce environmental impact and comply with stringent regulations. Technological advancements in metalworking processes, such as automation and precision machining, are also creating demand for high-performance lubricants that can enhance efficiency, extend tool life, and improve surface finish. While the market presents robust opportunities, certain restraints need to be addressed. The fluctuating raw material prices, particularly for base oils, can impact profitability and pricing strategies. Moreover, the increasing adoption of dry machining techniques in some applications could pose a challenge to traditional lubricant consumption. However, the overall outlook remains positive, supported by continuous innovation and the indispensable role of metalworking lubricants in modern manufacturing.

Metalworking Lubricant Company Market Share

This in-depth report offers an indispensable resource for industry professionals seeking to navigate the evolving landscape of the metalworking lubricant market. With a deep dive into market dynamics, technological advancements, and strategic opportunities, this analysis provides actionable insights to inform your business strategies. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, and a comprehensive forecast period from 2025 to 2033, this report leverages historical data from 2019-2024 to deliver robust projections. Discover the key drivers, challenges, and emerging trends shaping this multi-million dollar industry, and gain a competitive edge in the global market.

Metalworking Lubricant Market Structure & Innovation Trends

The global metalworking lubricant market exhibits a moderately concentrated structure, with leading players such as Quaker Houghton, Fuchs, Exxon Mobil, BP Castrol, Henkel, Yushiro Chemical, Idemitsu Kosan, Blaser Swisslube, TotalEnergies, Tectylasia, Cimcool Industrial Products, Petrofer, Master Fluid Solutions, LUKOIL, SINOPEC, Chervon, ENEOS, Talent, Chemetall, Cosmo Oil Lubricants, and Ashburn Chemical Technologies holding significant market share. Innovation is a primary driver, fueled by the demand for high-performance, eco-friendly, and specialized lubricants across various applications. Regulatory frameworks, particularly concerning environmental impact and worker safety, are increasingly influencing product development and formulation. While direct product substitutes are limited, the broader adoption of advanced manufacturing techniques and alternative lubrication methods presents an indirect challenge. End-user demographics are diverse, ranging from large-scale industrial manufacturers to specialized automotive component producers. Mergers and acquisitions (M&A) remain a strategic tool for consolidation and market expansion. For instance, the metalworking lubricant market has witnessed M&A deals valued in the millions of dollars, aimed at acquiring new technologies or expanding geographical reach. The market share of the top five players is estimated to be over 60 million percentage points.

Metalworking Lubricant Market Dynamics & Trends

The metalworking lubricant market is poised for robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) of XX%. This expansion is underpinned by several key market growth drivers. The relentless advancement in manufacturing technologies, including automation and precision machining, necessitates the use of advanced lubricants that enhance tool life, improve surface finish, and reduce operational costs. The automotive sector continues to be a dominant force, with its ever-increasing demand for specialized lubricants for engine components, transmissions, and stamping operations. Furthermore, the growing emphasis on sustainable manufacturing practices is driving the demand for bio-based and low-VOC (Volatile Organic Compound) lubricants, reflecting shifting consumer preferences towards environmentally responsible products. Technological disruptions, such as the development of nano-lubricants and intelligent lubrication systems, are beginning to penetrate the market, offering unprecedented levels of performance and efficiency. Competitive dynamics are characterized by intense R&D efforts, strategic partnerships, and a focus on customer-centric solutions. Market penetration of high-performance synthetic lubricants is expected to rise steadily, contributing to an overall market valuation in the hundreds of millions of dollars. The increasing adoption of advanced metal forming processes in industries like aerospace and renewable energy also contributes significantly to market growth.

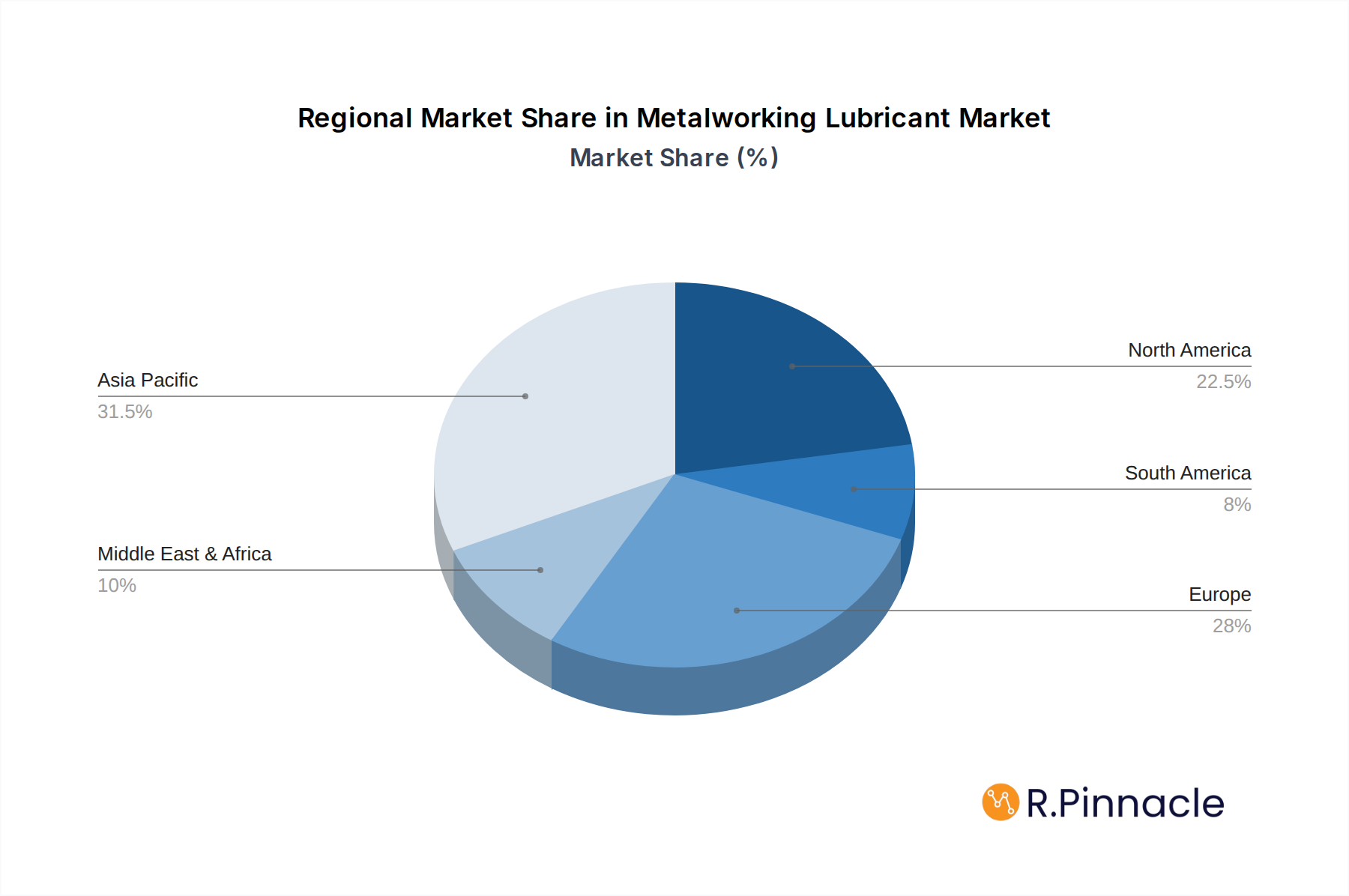

Dominant Regions & Segments in Metalworking Lubricant

The North America region is emerging as a dominant force in the metalworking lubricant market, driven by a strong industrial base, significant automotive manufacturing presence, and a proactive approach to technological innovation. Within this region, the Machinery application segment showcases exceptional growth, owing to the widespread use of sophisticated machinery in industries such as aerospace, defense, and general manufacturing. The demand for Metal Cutting Fluids remains exceptionally high in North America, as these fluids are critical for enhancing the efficiency and longevity of cutting tools in high-precision machining operations. Key drivers for North America's dominance include supportive government policies promoting advanced manufacturing, substantial investments in research and development by leading lubricant manufacturers, and a robust infrastructure that facilitates the efficient distribution of products. The Automotive segment also plays a pivotal role, with ongoing advancements in vehicle design and manufacturing processes demanding specialized lubricants. The Others application segment, encompassing industries like medical device manufacturing and electronics, is also contributing to market expansion.

In terms of product types, Metal Cutting Fluids are experiencing significant demand due to their role in enhancing machining speeds, improving surface quality, and extending tool life in various manufacturing processes. Metal Forming Fluids are also crucial, particularly in industries like automotive and aerospace, where they facilitate complex shaping operations. The increasing focus on efficiency and sustainability is also driving the demand for Metal Protecting Fluids, which offer corrosion resistance and extend the lifespan of manufactured components. Metal Treating Fluids are essential for processes like heat treatment and surface finishing, further contributing to the overall market growth. The synergy between technological advancements and the specific needs of these segments within dominant regions like North America is a key factor in the market's trajectory.

Metalworking Lubricant Product Innovations

Product innovations in the metalworking lubricant market are primarily focused on enhancing performance, improving environmental sustainability, and extending product lifespan. Advancements in synthetic base oils and additive technologies are leading to the development of lubricants that offer superior thermal stability, enhanced lubricity, and improved biodegradability. Key applications benefiting from these innovations include high-speed machining, aerospace component manufacturing, and the production of intricate automotive parts. The competitive advantage lies in developing formulations that meet stringent regulatory requirements while delivering superior operational efficiency and reduced maintenance costs. For example, the development of water-miscible metalworking fluids with improved bio-stability and reduced misting offers significant benefits to end-users.

Report Scope & Segmentation Analysis

This report meticulously analyzes the metalworking lubricant market across key segmentation criteria.

The Machinery application segment is projected for significant growth, driven by the continuous upgrade of industrial equipment and the adoption of advanced manufacturing techniques. Market size is estimated to reach hundreds of millions of dollars by 2033.

The Automotive segment, a cornerstone of the metalworking lubricant market, is expected to maintain steady growth. This is fueled by the increasing production of vehicles and the demand for specialized lubricants in new energy vehicles and advanced component manufacturing.

The Others application segment, encompassing diverse industries like aerospace, electronics, and medical devices, presents considerable growth potential due to specialized lubrication requirements and the expansion of these sectors.

Within product types, Metal Cutting Fluids will continue to dominate, owing to their essential role in precision manufacturing and high-volume production. Projections indicate sustained demand and market share.

Metal Forming Fluids are anticipated to witness robust growth, driven by innovations in metal forming processes and the increasing complexity of manufactured parts.

Metal Protecting Fluids are crucial for corrosion prevention and component longevity, showing steady market expansion driven by industrial maintenance needs and extended product warranties.

Metal Treating Fluids are vital for surface finishing and heat treatment processes, exhibiting consistent demand linked to the overall health of the manufacturing sector.

Key Drivers of Metalworking Lubricant Growth

The metalworking lubricant market is propelled by several pivotal growth drivers. Technologically, the increasing adoption of advanced manufacturing processes like precision machining, additive manufacturing, and high-speed cutting necessitates the development and use of high-performance lubricants that can withstand extreme pressures and temperatures while ensuring superior surface finish and tool life. Economically, the sustained growth in manufacturing output across key sectors such as automotive, aerospace, and heavy machinery directly translates to a higher demand for lubricants. Furthermore, global infrastructure development projects and the increasing production of complex industrial equipment contribute significantly to market expansion. Regulatory factors, while sometimes presenting challenges, also drive innovation by encouraging the development of eco-friendly, biodegradable, and low-VOC lubricants, meeting stricter environmental and health standards. The growing emphasis on operational efficiency and cost reduction for manufacturers also pushes the adoption of advanced lubricant formulations that minimize waste and extend equipment lifespan.

Challenges in the Metalworking Lubricant Sector

The metalworking lubricant sector faces several significant challenges that can impede growth. Stringent environmental regulations worldwide, particularly concerning disposal and emissions, necessitate significant investment in R&D for sustainable alternatives, impacting product development costs. Supply chain disruptions, as witnessed in recent years, can lead to price volatility of raw materials and impact product availability, affecting both manufacturers and end-users. Intense competition from both established players and emerging regional manufacturers can lead to price wars and margin erosion. The high cost of advanced synthetic lubricants can also be a barrier for small and medium-sized enterprises (SMEs) seeking to upgrade their operational capabilities. Furthermore, the slow pace of adoption of new lubricant technologies in certain traditional manufacturing sectors can limit market penetration. The potential for contamination and the need for proper disposal management also present ongoing operational challenges for end-users, impacting overall product lifecycle costs.

Emerging Opportunities in Metalworking Lubricant

The metalworking lubricant market is ripe with emerging opportunities. The increasing demand for bio-based and biodegradable lubricants presents a significant avenue for growth, driven by growing environmental consciousness and stricter regulations. The automotive industry's transition to electric vehicles (EVs) creates new demands for specialized lubricants for EV components, thermal management systems, and battery cooling, opening up a new frontier for innovation. The expansion of additive manufacturing (3D printing) also presents opportunities for novel lubricant formulations designed to optimize printing processes and post-processing treatments. Furthermore, the growing industrialization in emerging economies in Asia and Africa offers substantial untapped market potential for both conventional and advanced lubricants. The development of intelligent lubrication systems that utilize sensors and data analytics to optimize lubricant application and predict maintenance needs represents another significant technological opportunity.

Leading Players in the Metalworking Lubricant Market

- Quaker Houghton

- Fuchs

- Exxon Mobil

- BP Castrol

- Henkel

- Yushiro Chemical

- Idemitsu Kosan

- Blaser Swisslube

- TotalEnergies

- Tectylasia

- Cimcool Industrial Products

- Petrofer

- Master Fluid Solutions

- LUKOIL

- SINOPEC

- Chervon

- ENEOS

- Talent

- Chemetall

- Cosmo Oil Lubricants

- Ashburn Chemical Technologies

Key Developments in Metalworking Lubricant Industry

- 2023 September: Quaker Houghton acquires a specialized coolant manufacturer, expanding its portfolio of high-performance metalworking fluids.

- 2023 July: Fuchs launches a new line of biodegradable metalworking fluids, addressing growing environmental concerns.

- 2022 December: ExxonMobil introduces a new synthetic lubricant series designed for extreme temperature applications in aerospace.

- 2022 October: BP Castrol announces a strategic partnership with an automotive manufacturer to develop custom lubrication solutions.

- 2022 April: Henkel expands its global production capacity for metalworking fluids to meet increasing demand.

- 2021 November: Yushiro Chemical introduces an innovative, low-mist metal cutting fluid for enhanced worker safety.

- 2021 July: Idemitsu Kosan invests in R&D for advanced lubricants for the renewable energy sector.

- 2021 March: Blaser Swisslube unveils a new water-miscible coolant with extended service life.

- 2020 September: TotalEnergies acquires a stake in a specialty chemical company, strengthening its lubricant offerings.

- 2020 May: Tectylasia launches a new range of temporary protective coatings for metal components.

- 2019 October: Cimcool Industrial Products expands its presence in the Asian market with a new manufacturing facility.

- 2019 August: Petrofer develops an advanced lubricant for additive manufacturing processes.

- 2019 April: Master Fluid Solutions introduces a new generation of metal forming fluids for high-strength alloys.

- 2019 January: LUKOIL expands its offering of industrial lubricants for the mining sector.

Future Outlook for Metalworking Lubricant Market

The future outlook for the metalworking lubricant market is highly promising, driven by continuous technological advancements and evolving industry demands. The growing emphasis on sustainability will continue to fuel the development and adoption of eco-friendly, bio-based, and recyclable lubricants, creating significant market opportunities. The burgeoning electric vehicle sector will necessitate new and specialized lubricant solutions, representing a substantial growth area. Furthermore, the increasing integration of smart manufacturing technologies and the Industrial Internet of Things (IIoT) will lead to the development of intelligent lubrication systems that offer predictive maintenance and optimized performance. Strategic investments in R&D, coupled with a focus on catering to niche applications and emerging markets, will be crucial for market leaders to maintain their competitive edge and capitalize on the expanding global demand for advanced metalworking lubricants.

Metalworking Lubricant Segmentation

-

1. Application

- 1.1. Machinery

- 1.2. Automotive

- 1.3. Others

-

2. Type

- 2.1. Metal Cutting Fluids

- 2.2. Metal Forming Fluids

- 2.3. Metal Protecting Fluids

- 2.4. Metal Treating Fluids

Metalworking Lubricant Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Metalworking Lubricant Regional Market Share

Geographic Coverage of Metalworking Lubricant

Metalworking Lubricant REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Machinery

- 5.1.2. Automotive

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Metal Cutting Fluids

- 5.2.2. Metal Forming Fluids

- 5.2.3. Metal Protecting Fluids

- 5.2.4. Metal Treating Fluids

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Machinery

- 6.1.2. Automotive

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Metal Cutting Fluids

- 6.2.2. Metal Forming Fluids

- 6.2.3. Metal Protecting Fluids

- 6.2.4. Metal Treating Fluids

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Machinery

- 7.1.2. Automotive

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Metal Cutting Fluids

- 7.2.2. Metal Forming Fluids

- 7.2.3. Metal Protecting Fluids

- 7.2.4. Metal Treating Fluids

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Machinery

- 8.1.2. Automotive

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Metal Cutting Fluids

- 8.2.2. Metal Forming Fluids

- 8.2.3. Metal Protecting Fluids

- 8.2.4. Metal Treating Fluids

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Machinery

- 9.1.2. Automotive

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Metal Cutting Fluids

- 9.2.2. Metal Forming Fluids

- 9.2.3. Metal Protecting Fluids

- 9.2.4. Metal Treating Fluids

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Metalworking Lubricant Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Machinery

- 10.1.2. Automotive

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Metal Cutting Fluids

- 10.2.2. Metal Forming Fluids

- 10.2.3. Metal Protecting Fluids

- 10.2.4. Metal Treating Fluids

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Quaker Houghton

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Fuchs

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Exxon Mobil

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BP Castrol

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Henkel

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Yushiro Chemical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Idemitsu Kosan

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Blaser Swisslube

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 TotalEnergies

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tectylasia

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cimcool Industrial Products

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Petrofer

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Master Fluid Solutions

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 LUKOIL

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 SINOPEC

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Chervon

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 ENEOS

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Talent

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Chemetall

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Cosmo Oil Lubricants

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Ashburn Chemical Technologies

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Quaker Houghton

List of Figures

- Figure 1: Global Metalworking Lubricant Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Metalworking Lubricant Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Metalworking Lubricant Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Metalworking Lubricant Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Metalworking Lubricant Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Metalworking Lubricant Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Metalworking Lubricant Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Metalworking Lubricant Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Metalworking Lubricant Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Metalworking Lubricant Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Metalworking Lubricant Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Metalworking Lubricant Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Metalworking Lubricant Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Metalworking Lubricant Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Metalworking Lubricant Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Metalworking Lubricant Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Metalworking Lubricant Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Metalworking Lubricant Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Metalworking Lubricant Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Metalworking Lubricant Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Metalworking Lubricant Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Metalworking Lubricant Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Metalworking Lubricant Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Metalworking Lubricant Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Metalworking Lubricant Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Metalworking Lubricant Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Metalworking Lubricant Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Metalworking Lubricant Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Metalworking Lubricant Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Metalworking Lubricant Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Metalworking Lubricant Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Metalworking Lubricant Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Metalworking Lubricant Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Metalworking Lubricant Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Metalworking Lubricant Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Metalworking Lubricant Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Metalworking Lubricant Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Metalworking Lubricant Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Metalworking Lubricant Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Metalworking Lubricant Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Metalworking Lubricant?

The projected CAGR is approximately 2.7%.

2. Which companies are prominent players in the Metalworking Lubricant?

Key companies in the market include Quaker Houghton, Fuchs, Exxon Mobil, BP Castrol, Henkel, Yushiro Chemical, Idemitsu Kosan, Blaser Swisslube, TotalEnergies, Tectylasia, Cimcool Industrial Products, Petrofer, Master Fluid Solutions, LUKOIL, SINOPEC, Chervon, ENEOS, Talent, Chemetall, Cosmo Oil Lubricants, Ashburn Chemical Technologies.

3. What are the main segments of the Metalworking Lubricant?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Metalworking Lubricant," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Metalworking Lubricant report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Metalworking Lubricant?

To stay informed about further developments, trends, and reports in the Metalworking Lubricant, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence