Key Insights

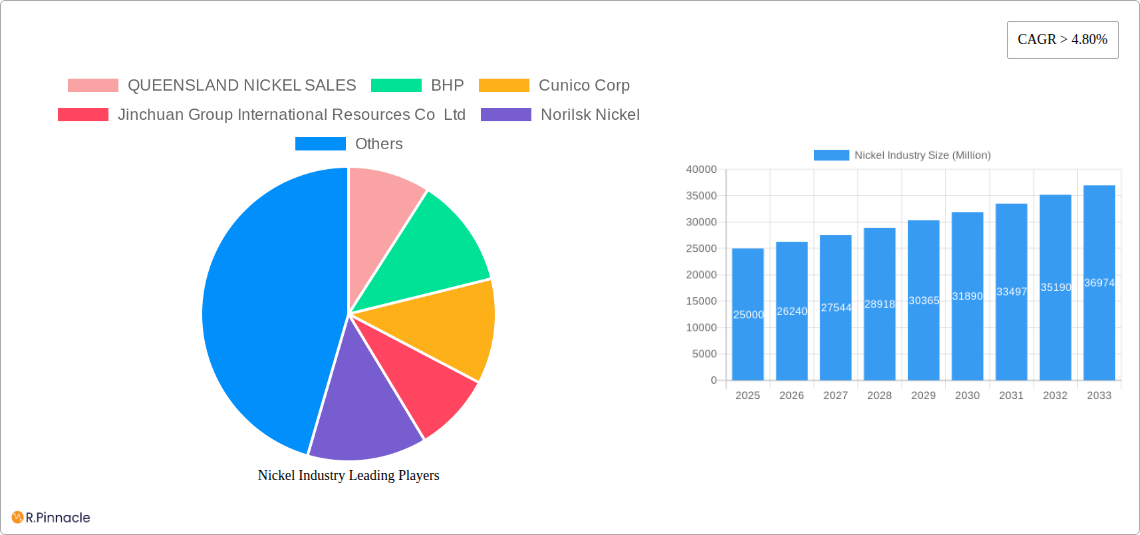

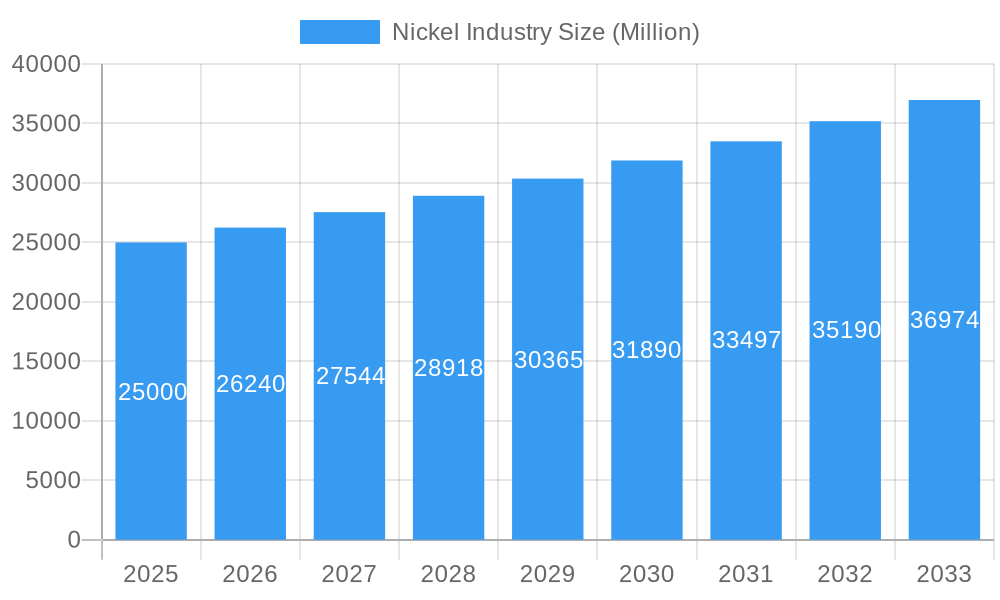

The global Nickel Industry is poised for robust expansion, projected to reach a market size of approximately $XX million by 2025, with a Compound Annual Growth Rate (CAGR) exceeding 4.80% through 2033. This significant growth is primarily fueled by the insatiable demand from the stainless steel sector, which historically accounts for the largest share of nickel consumption. Furthermore, the burgeoning electric vehicle (EV) market is emerging as a critical growth driver, with nickel-rich battery chemistries becoming indispensable for enhancing EV range and performance. Government initiatives promoting clean energy and sustainable transportation solutions are expected to further accelerate this trend, creating substantial opportunities for nickel producers and suppliers. The increasing adoption of alloys in aerospace, marine, and industrial applications also contributes to the sustained demand for nickel.

Nickel Industry Market Size (In Billion)

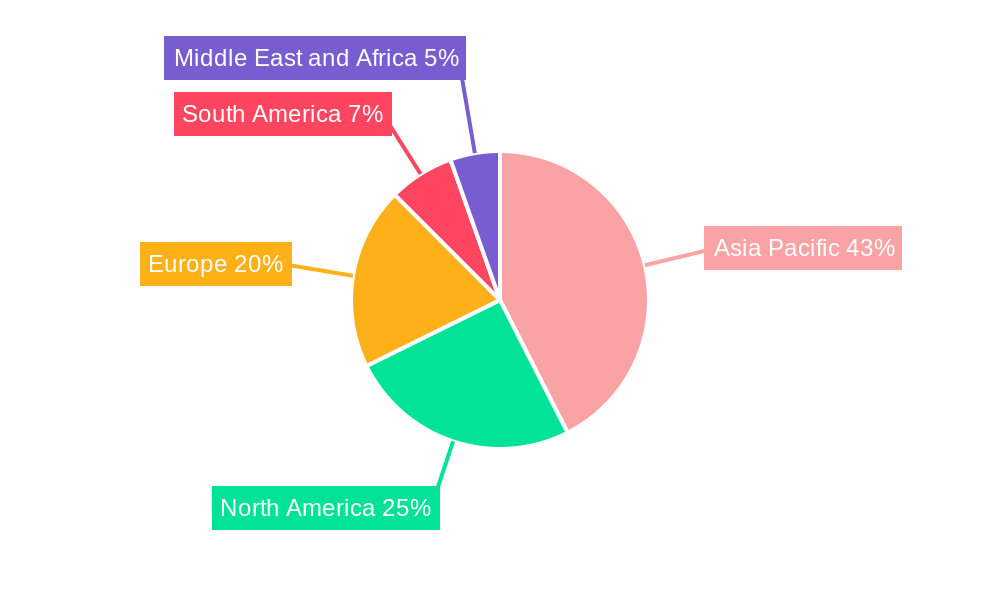

Despite the optimistic outlook, the Nickel Industry faces certain challenges. Volatility in nickel prices, influenced by global supply-demand dynamics and geopolitical factors, can impact profitability and investment decisions. Environmental concerns and stringent regulations surrounding nickel extraction and processing necessitate continuous investment in sustainable practices and advanced technologies. Geographically, the Asia Pacific region, particularly China and India, is expected to dominate the market due to its large industrial base and rapid EV adoption. North America and Europe are also significant contributors, driven by their advanced manufacturing sectors and strong focus on green technologies. Key players like Glencore, Norilsk Nickel, and BHP are strategically positioned to capitalize on these market dynamics through vertical integration and strategic investments in new mining projects and battery recycling initiatives. The forecast period from 2025 to 2033 will witness a strong emphasis on innovation in nickel processing and an expansion of its use in emerging technologies.

Nickel Industry Company Market Share

Here is an SEO-optimized, reader-centric report description for the Nickel Industry, designed for immediate use without modification:

Nickel Industry Market Structure & Innovation Trends

The global Nickel Industry is characterized by a moderately concentrated market structure, with a few key players holding significant market share. Innovation is largely driven by the increasing demand for high-purity nickel in battery applications and advancements in sustainable mining and processing technologies. Regulatory frameworks, particularly those concerning environmental impact and ethical sourcing, are shaping industry practices. Product substitutes, while present in some niche applications, face significant technical and cost barriers in large-scale adoption for core uses like stainless steel. End-user demographics are shifting towards electric vehicle manufacturers and renewable energy storage providers, alongside traditional industrial consumers. Merger and acquisition (M&A) activities remain robust, with major players consolidating to secure supply chains and enhance operational efficiencies. Estimated M&A deal values in recent years have reached into the billions of dollars, reflecting the strategic importance of nickel assets. Key areas of innovation include the development of lower-carbon footprint nickel production methods and advancements in recycling technologies.

Nickel Industry Market Dynamics & Trends

The Nickel Industry is experiencing a dynamic growth trajectory, fueled by several overarching market trends and influential drivers. The escalating global demand for electric vehicles (EVs) is a paramount growth engine, with nickel-sulphate-rich battery chemistries becoming increasingly crucial for enhanced energy density and performance. This surge in EV adoption directly translates into a higher market penetration for battery-grade nickel. Technological disruptions are playing a significant role, including advancements in hydrometallurgical processing that enable the extraction of nickel from lower-grade ores, thereby expanding resource availability. Furthermore, innovations in direct-to-metal (DTM) plating processes are opening up new applications. Consumer preferences are increasingly leaning towards products with a lower environmental footprint, compelling nickel producers to invest in sustainable sourcing and reduced emission technologies. This is reflected in a growing demand for "green nickel." Competitive dynamics are intensifying, with established mining giants and emerging battery material suppliers vying for market dominance. The CAGR for the nickel market is projected to be robust, driven by these powerful underlying forces. Strategic partnerships and collaborations are becoming more common as companies seek to secure long-term supply agreements and share technological expertise. The overall market penetration of nickel in critical sectors like energy storage is expected to witness substantial expansion throughout the forecast period.

Dominant Regions & Segments in Nickel Industry

The Stainless Steel segment continues to be a dominant force in the Nickel Industry, driven by its widespread use in construction, automotive, and consumer goods. Its resilience is underpinned by global economic growth and infrastructure development. However, the Batteries segment is rapidly emerging as a key growth driver and is poised to become the most significant segment in the coming years, primarily due to the exponential rise in electric vehicle (EV) production and the growing demand for energy storage solutions. This segment's dominance is propelled by technological advancements in battery chemistries that require high-purity nickel.

- Leading Region: Asia-Pacific, particularly China, remains a dominant region due to its massive manufacturing base and substantial consumption of nickel across various industries, including stainless steel and electronics, and its leading position in EV battery production.

- Key Drivers for Batteries Segment Dominance:

- Economic Policies: Government incentives for EV adoption and renewable energy storage projects.

- Infrastructure Development: Expansion of charging infrastructure for EVs, further boosting demand.

- Technological Advancements: Development of next-generation battery technologies requiring higher nickel content.

- Environmental Regulations: Increasing pressure to reduce carbon emissions, favoring EVs and sustainable energy solutions.

The Alloys segment also holds significant importance, with nickel being a critical component in superalloys used in aerospace and industrial gas turbines, where high-temperature strength and corrosion resistance are paramount. The Plating segment, while smaller, is vital for enhancing the durability and aesthetics of various products. Other Applications, encompassing catalysts, magnets, and chemicals, contribute to the diverse demand profile of the nickel market.

Nickel Industry Product Innovations

Product innovations in the Nickel Industry are primarily focused on enhancing purity and sustainability. Advances in hydrometallurgical and pyrometallurgical processing are yielding higher-grade nickel suitable for demanding applications like lithium-ion batteries. The development of lower-carbon footprint nickel production methods, including the utilization of renewable energy in mining and processing, is a significant trend. Innovations in nickel recycling technologies are also gaining traction, offering a circular economy approach. These developments provide competitive advantages by meeting the stringent requirements of the EV sector and aligning with global sustainability goals.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Nickel Industry, segmented by its key applications.

- Stainless Steel: This segment represents a substantial portion of nickel consumption, driven by its widespread use in construction, automotive, and consumer durables. Growth is projected to be steady, influenced by global manufacturing output.

- Alloys: Nickel alloys are crucial for high-performance applications in aerospace, defense, and industrial machinery, demanding specialized properties. Growth in this segment is tied to advancements in these high-tech sectors.

- Plating: Used for corrosion resistance and aesthetic appeal, nickel plating serves industries ranging from automotive to electronics. Its market dynamics are influenced by product design trends and durability requirements.

- Batteries: This is the fastest-growing segment, propelled by the electric vehicle revolution and the demand for energy storage systems. High-purity nickel is essential for advanced battery chemistries, and this segment is expected to see significant market size expansion and high growth projections.

- Other Applications: This category includes diverse uses such as catalysts, magnets, and chemicals. While individually smaller, collectively they contribute to the overall market diversification and stability.

Key Drivers of Nickel Industry Growth

The Nickel Industry's growth is propelled by a confluence of factors. The most significant driver is the escalating demand for electric vehicles (EVs), which necessitates substantial quantities of high-purity nickel for battery production. Technological advancements in battery chemistries, enabling higher energy density and faster charging, further amplify this demand. Government policies promoting clean energy and carbon emission reductions are creating a favorable environment for nickel-based technologies. Furthermore, innovations in nickel extraction and processing are expanding resource availability and improving cost-effectiveness, making nickel more accessible for a wider range of applications. Economic development and industrialization in emerging economies also contribute to sustained demand for nickel in traditional sectors like stainless steel and construction.

Challenges in the Nickel Industry Sector

Despite robust growth prospects, the Nickel Industry faces several significant challenges. Regulatory hurdles related to environmental impact and sustainable mining practices can lead to increased operational costs and project delays. Supply chain disruptions, often stemming from geopolitical instability and logistical complexities, can impact the availability and price of nickel. Competitive pressures from substitute materials, while often facing technical limitations, can still influence market dynamics in certain applications. Furthermore, the capital-intensive nature of nickel mining and processing requires substantial investment, and fluctuations in commodity prices can create financial uncertainties. The ethical sourcing of nickel and concerns over labor practices in some mining regions also present reputational challenges that need to be addressed.

Emerging Opportunities in Nickel Industry

The Nickel Industry is poised for significant growth driven by emerging opportunities. The burgeoning electric vehicle market presents a colossal opportunity for battery-grade nickel, with demand projected to soar. Advancements in battery technology, such as solid-state batteries, could further boost nickel consumption. The increasing focus on renewable energy storage solutions, including grid-scale batteries, also opens new avenues for nickel demand. Furthermore, innovations in nickel recycling offer a sustainable and cost-effective source of the metal, creating a circular economy model. Emerging markets with rapid industrialization and infrastructure development will continue to provide sustained demand for nickel in traditional applications like stainless steel. The development of new nickel deposits and advancements in processing lower-grade ores also present opportunities to expand supply.

Leading Players in the Nickel Industry Market

- QUEENSLAND NICKEL SALES

- BHP

- Cunico Corp

- Jinchuan Group International Resources Co Ltd

- Norilsk Nickel

- INDEPENDENCE GROUP NL

- Votorantim

- Anglo American

- Terrafame

- Eramet

- Sumitomo Metal Mining Co Ltd

- Glencore

- Sherritt International Corporation

- Pacific Metal Company

- Vale

Key Developments in Nickel Industry Industry

- August 2022: NMDC Ltd. announced its decision to explore opportunities overseas in a bid to mine lithium, nickel, and cobalt in order to meet the growing demand in India. The state-run iron-ore producer is planning to start mining in Australia, as it holds a 90.02% stake in the country's Legacy Iron Ore Ltd.

- December 2021: Mitsui & Co. Mineral Resources Development (Asia) Corp. (MMRDA) and Sojitz will sell all their shares in CBNC (36% in total to Sumitomo Metal Mining Co. Ltd (SMM). With the sales of the shares, SMM's shareholding ratio in CBNC will increase from the current 54% of the outstanding shares to 90%.

- October 2021: Renault Group announced the signing of a Memorandum of Understanding (MoU) with Terrafame, for a future supply of nickel sulphate. With this agreement, Renault Group will secure a significant annual supply of nickel sulphate from Terrafame, representing up to 15 GWh of annual capacity.

- July 2021: BHP announced the signing of a nickel supply agreement from its Nickel West asset in Western Australia, with one of the world's leading sustainable energy company, Tesla Inc.

Future Outlook for Nickel Industry Market

The future outlook for the Nickel Industry is exceptionally bright, characterized by sustained and robust growth. The insatiable demand from the electric vehicle sector will continue to be the primary growth accelerator, driving significant expansion in the battery-grade nickel market. Advancements in battery technology are expected to further enhance nickel's role in energy storage. Investments in sustainable mining practices and recycling technologies will not only address environmental concerns but also create new, cost-effective supply channels. Emerging markets will continue to contribute to demand growth in traditional sectors. Strategic partnerships and mergers will likely shape the competitive landscape, leading to greater supply chain integration and efficiency. The overall market potential remains immense, with nickel poised to be a critical metal in the transition to a greener, more sustainable global economy.

Nickel Industry Segmentation

-

1. Application

- 1.1. Stainless Steel

- 1.2. Alloys

- 1.3. Plating

- 1.4. Casting

- 1.5. Batteries

- 1.6. Other Applications

Nickel Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Nickel Industry Regional Market Share

Geographic Coverage of Nickel Industry

Nickel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 4.80% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Stainless Steel

- 5.1.2. Alloys

- 5.1.3. Plating

- 5.1.4. Casting

- 5.1.5. Batteries

- 5.1.6. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Nickel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Stainless Steel

- 6.1.2. Alloys

- 6.1.3. Plating

- 6.1.4. Casting

- 6.1.5. Batteries

- 6.1.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Asia Pacific Nickel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Stainless Steel

- 7.1.2. Alloys

- 7.1.3. Plating

- 7.1.4. Casting

- 7.1.5. Batteries

- 7.1.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. North America Nickel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Stainless Steel

- 8.1.2. Alloys

- 8.1.3. Plating

- 8.1.4. Casting

- 8.1.5. Batteries

- 8.1.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Nickel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Stainless Steel

- 9.1.2. Alloys

- 9.1.3. Plating

- 9.1.4. Casting

- 9.1.5. Batteries

- 9.1.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. South America Nickel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Stainless Steel

- 10.1.2. Alloys

- 10.1.3. Plating

- 10.1.4. Casting

- 10.1.5. Batteries

- 10.1.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East and Africa Nickel Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Stainless Steel

- 11.1.2. Alloys

- 11.1.3. Plating

- 11.1.4. Casting

- 11.1.5. Batteries

- 11.1.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 QUEENSLAND NICKEL SALES

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 BHP

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cunico Corp

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Jinchuan Group International Resources Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Norilsk Nickel

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 INDEPENDENCE GROUP NL

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Votorantim

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Anglo American

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Terrafame

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Eramet

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sumitomo Metal Mining Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Glencore

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sherritt International Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Pacific Metal Company

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Vale

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 QUEENSLAND NICKEL SALES

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Nickel Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Nickel Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Nickel Industry Revenue (Million), by Application 2025 & 2033

- Figure 4: Asia Pacific Nickel Industry Volume (K Tons), by Application 2025 & 2033

- Figure 5: Asia Pacific Nickel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Nickel Industry Volume Share (%), by Application 2025 & 2033

- Figure 7: Asia Pacific Nickel Industry Revenue (Million), by Country 2025 & 2033

- Figure 8: Asia Pacific Nickel Industry Volume (K Tons), by Country 2025 & 2033

- Figure 9: Asia Pacific Nickel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Nickel Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: North America Nickel Industry Revenue (Million), by Application 2025 & 2033

- Figure 12: North America Nickel Industry Volume (K Tons), by Application 2025 & 2033

- Figure 13: North America Nickel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Nickel Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Nickel Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Nickel Industry Volume (K Tons), by Country 2025 & 2033

- Figure 17: North America Nickel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Nickel Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Nickel Industry Revenue (Million), by Application 2025 & 2033

- Figure 20: Europe Nickel Industry Volume (K Tons), by Application 2025 & 2033

- Figure 21: Europe Nickel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Nickel Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: Europe Nickel Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Nickel Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: Europe Nickel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Nickel Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: South America Nickel Industry Revenue (Million), by Application 2025 & 2033

- Figure 28: South America Nickel Industry Volume (K Tons), by Application 2025 & 2033

- Figure 29: South America Nickel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: South America Nickel Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: South America Nickel Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: South America Nickel Industry Volume (K Tons), by Country 2025 & 2033

- Figure 33: South America Nickel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Nickel Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Middle East and Africa Nickel Industry Revenue (Million), by Application 2025 & 2033

- Figure 36: Middle East and Africa Nickel Industry Volume (K Tons), by Application 2025 & 2033

- Figure 37: Middle East and Africa Nickel Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East and Africa Nickel Industry Volume Share (%), by Application 2025 & 2033

- Figure 39: Middle East and Africa Nickel Industry Revenue (Million), by Country 2025 & 2033

- Figure 40: Middle East and Africa Nickel Industry Volume (K Tons), by Country 2025 & 2033

- Figure 41: Middle East and Africa Nickel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Nickel Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 3: Global Nickel Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Nickel Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 7: Global Nickel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Global Nickel Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 9: China Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: China Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 11: India Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: India Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 13: Japan Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Japan Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: South Korea Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: South Korea Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Rest of Asia Pacific Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Asia Pacific Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 21: Global Nickel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: Global Nickel Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 23: United States Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: United States Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Canada Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Canada Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Mexico Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Mexico Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 30: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 31: Global Nickel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Global Nickel Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 33: Germany Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Germany Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: United Kingdom Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: United Kingdom Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 37: Italy Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 39: France Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: France Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 44: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 45: Global Nickel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 46: Global Nickel Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 47: Brazil Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Brazil Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Argentina Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Argentina Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Rest of South America Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Rest of South America Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 53: Global Nickel Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 54: Global Nickel Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 55: Global Nickel Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Nickel Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: Saudi Arabia Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Saudi Arabia Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: South Africa Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Africa Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 61: Rest of Middle East and Africa Nickel Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Middle East and Africa Nickel Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Nickel Industry?

The projected CAGR is approximately > 4.80%.

2. Which companies are prominent players in the Nickel Industry?

Key companies in the market include QUEENSLAND NICKEL SALES, BHP, Cunico Corp, Jinchuan Group International Resources Co Ltd, Norilsk Nickel, INDEPENDENCE GROUP NL, Votorantim, Anglo American, Terrafame, Eramet, Sumitomo Metal Mining Co Ltd, Glencore, Sherritt International Corporation, Pacific Metal Company, Vale.

3. What are the main segments of the Nickel Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Corrosion Resistant Alloys in the Oil and Gas Industry; Other Drivers.

6. What are the notable trends driving market growth?

Increasing Demand for Stainless Steel.

7. Are there any restraints impacting market growth?

Volatility in the Supply Demand Scenario; Environmental Considerations During Mining Activities.

8. Can you provide examples of recent developments in the market?

August 2022: NMDC Ltd. announced its decision to explore opportunities overseas in a bid to mine lithium, nickel, and cobalt in order to meet the growing demand in India. The state-run iron-ore producer is planning to start mining in Australia, as it holds a 90.02% stake in the country's Legacy Iron Ore Ltd.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Nickel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Nickel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Nickel Industry?

To stay informed about further developments, trends, and reports in the Nickel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence